A. FAQs on Filing of Letter of Undertaking for Export of Goods or Services (FORM GST RFD-11)

Q.1 Who has to furnish a Letter of Undertaking?

Ans: Any registered person availing the option to supply goods or services for export /SEZs without payment of integrated tax has to furnish, prior to export/SEZs supply, a Letter of Undertaking (LUT), if he has not been prosecuted for tax evasion for an amount of Rs 2.5 Crore or above under the CGST Act/IGST Act/Existing law. Example of transactions for which LUT can be used are:

- Zero rated supply to SEZ without payment of IGST.

- Export of goods to a country outside India without payment of IGST.

- Providing services to a client in a country outside India without payment of IGST.

Q.2 How can I file LUT?

Ans: All registered taxpayers who have zero-rated supply of goods or services have to furnish LUT in Form GST RFD-11 on the GST Portal before affecting such supply. Access the GST portal and login using valid credentials. Navigate to Services > User Services > Furnish Letter of Undertaking (LUT) command to file LUT.

Q.3 What is to be filled in LUT?

Ans: GSTIN and Name (Legal Name) of the Taxpayer would get prefilled based on login. Taxpayer needs to select the financial year for which LUT is being filed, enter the name, address and occupation details of two independent and reliable witnesses. Taxpayer also needs to select all the points of self-declaration before filing the LUT.

Q.4 What if I have already furnished a LUT and also got approval for it?

Ans: If a taxpayer has any LUT which was furnished manually and got approved by the Tax Authority for current Financial Year, then he can upload that LUT and file this online application for furnishing LUT to seek the online approval for that previous LUT.

Q.5 Is it mandatory to record the manually approved LUT in online records?

Ans: It is not mandatory, but if you want to record the manually approved LUT to be available in online records then you can furnish it with online application.

Q.6 Is there any limitation regarding the upload of previous LUT?

Ans: Only one previous LUT document not exceeding 2 MB in size can be uploaded in one application. To upload another LUT, taxpayer needs to file a new application.

Q.7 Can I as a taxpayer save the LUT application during the process of filing?

Ans: Taxpayer will have the facility to save the application at any stage for 15 days. Saved application can be retrieved from Dashboard > Services > User Services > My Saved Applications.

Q.8 Can I preview the LUT application?

Ans: Before signing and filing the application, taxpayer will have an option to Preview the application and save it in PDF format.

Q.9 Who has to sign the LUT application?

Ans: Primary authorized signatory/Any other Authorized Signatory needs to sign and file the verification with DSC/EVC. Authorized signatory can be the working partner, the managing director or the proprietor or by a person duly authorized by such working partner or Board of Directors of such company or proprietor to execute the form.

Q.10 How would I know that the process of furnishing LUT has been completed?

Ans: After successful filing, system will generate ARN and acknowledgement. You will be informed about successful filing via SMS and Email and you can also download the acknowledgement as PDF.

Q.11 Can I view my LUT application after filing?

Ans: Taxpayer will be able to see his ARN under the Services > User Services > View My Submitted LUTs.

Q.12 How would the LUT application be processed?

Ans: The processing of LUT is available online for Model 2 States. For Model 1 States, Tax Official may process LUT manually/ online, depending on the facility available at backend of Model 1 States to process the LUT.

Q.13 From where can I reply to notice issued by Tax Official?

Ans: Navigate to Dashboard > Services > User Services > View Additional Notices/Orders to reply to notice issued by Tax Official.

Q.14 From where can I view the order issued by Tax Official?

Ans: Navigate to Dashboard > Services > User Services > View Additional Notices/Orders to view the order issued by Tax Official.

Q.15 What will happen if a Tax Official doesn’t process the LUT application?

Ans: If the LUT application is not processed by Tax Official, or any notice for clarification is not issued by the Tax Official within 3 working days, then the application will be deemed approved and the status of LUT application will change to “Deemed Approved”. When the application is deemed approved, then an order copy will be generated through the GST Portal and order will be available to the taxpayer in the downloadable form under Dashboard > Services > User Services > View Additional Notices/Orders option.

Q.16 What are the various status of the LUT application filed by the taxpayer?

Ans: The list below provides the list of statuses of the LUT application in Form GST RFD-11 ARN, filed by the taxpayer:

1. Submitted: Status of LUT application after Taxpayer submits the application successfully

2. Pending for Clarification: Status of LUT application after LUT Processing officer issues notice for seeking clarification

3. Pending for Order: Status of LUT application after Taxpayer submits the reply for notice within 15 working days Or Taxpayer does not submit the reply for notice after completion of 15 working days and then GST Portal changes the status from pending for clarification to pending for order

4. Approved: Status of LUT application after Tax Official accepts the undertaking furnished by Taxpayer

5. Rejected: Status of LUT application after Tax Official rejects the undertaking furnished by Taxpayer

6. Deemed Approved: Status of LUT application in case Tax Official doesn’t take any action within 3 working days

7. Expired: The status of the LUT application will get changed to Expired at the end of the respective FY.

Q.17 Can a Tax Official disable LUT filing by the taxpayer?

Ans: A Tax Official who is LUT Processing Officer, may disable LUT filing functionality for a taxpayer on the GST Portal. When Tax Official has disabled LUT filing for a taxpayer, taxpayer is intimated through SMS and email.

Q.18 Can a taxpayer raise request from GST Portal to enable LUT?

Ans: If LUT Processing Officer has disabled the furnishing of LUT for some taxpayer, then to get it enabled, taxpayer has to communicate this request to LUT Processing Officer manually. From GST Portal, taxpayer cannot raise the request to enable furnishing of LUT.

Q. No. 19 FAQ is related to Creation of new UT of Ladakh and consequent changes on GST Portal for taxpayers

Q.19 I have received an intimation that a new GSTIN has been assigned to me for UT of Ladakh. I have already filed Letter of Undertaking. What do I do next?

Ans: You need to file a fresh Letter of Undertaking (LUT) for New GSTIN, for the remaining part of the financial year.

Q. No. 20 is FAQ related to Merger of UT of Daman & Diu with UT of Dadra and Nagar Haveli and consequent changes on GST Portal for taxpayers

20 I have received an intimation that a new GSTIN has been assigned to me for UT of Dadra and Nagar Haveli and Daman and Diu. I have already filed Letter of Undertaking. What do I do next?

You need to file a fresh Letter of Undertaking (LUT) for New GSTIN, for the remaining part of the financial year.

B. Manual on Filing of Letter of Undertaking for Export of Goods or Services (FORM GST RFD-11)

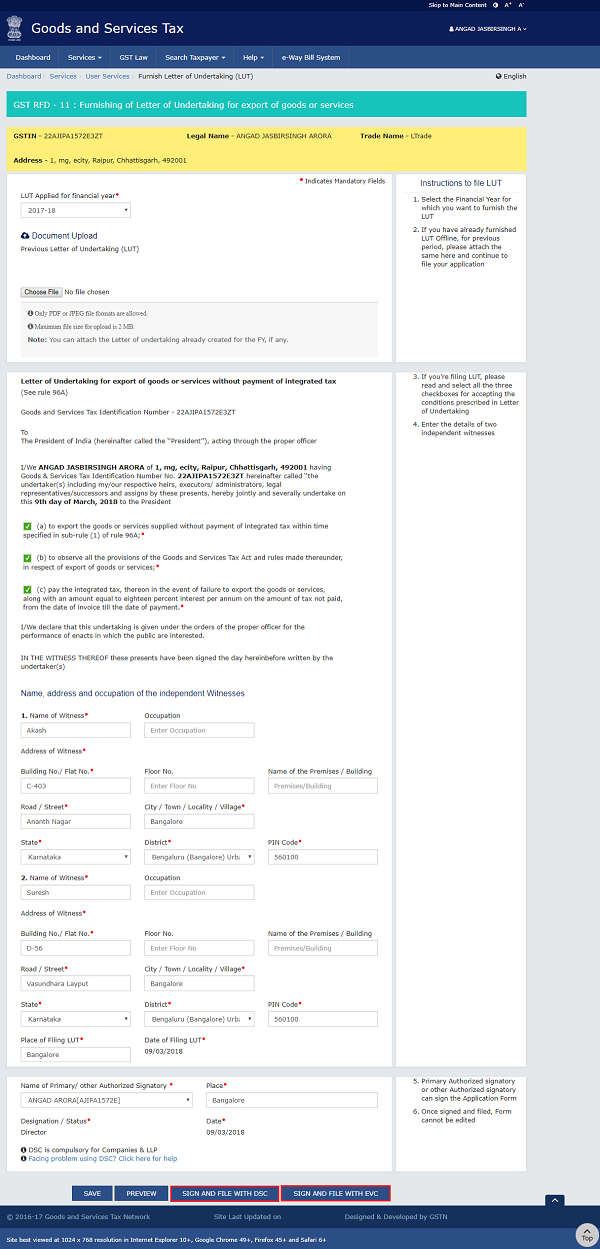

How can I as a taxpayer file the Letter of Undertaking (LUT) for export of goods or services at the GST Portal?

To file the Letter of Undertaking (LUT) for export of goods or services at the GST Portal, perform the following steps:

1. Access the GST Portal at www.gst.gov.in URL. The GST Home page is displayed.

2. Login to the GST Portal with valid credentials.

3. Click the Services > User Services > Furnish Letter of Undertaking (LUT) command.

4. Form GST RFD-11 is displayed. Select the financial year for which LUT is applied for from the LUT Applied for Financial Year drop-down list.

5. Click the Choose File button to upload the previous LUT.

Note:

- Only PDF or JPEG file formats are allowed.

- Maximum file size for upload is 2 MB.

6. Select the declaration checkboxes.

7. In the Name, Address and occupation of the independent and reliable witnesses section, enter the name and address of 2 witnesses.

8. In the Place of Filing LUT field, enter the place.

9. In the Name of Primary/ Other Authorized Signatory drop-down list, select the name of authorized signatory.

10. In the Place field, enter the place where the form is filed.

11. In case you want to save the form and retrieve the form later, click the SAVE button to save the form.

A confirmation message is displayed that application is saved successfully.

Note: You can navigate to Services > User Services > My Saved Applications to retrieve the saved application later.

12. Click the PREVIEW button to preview the form.

The form is displayed in the PDF format.

13. Click the SIGN AND FILE WITH DSC or SIGN AND FILE WITH EVC button.

Note: If you have saved the form and retrieving it later, you need to select the name of authorized signatory and enter the place where the form is filed before filing the form.

14. Click the PROCEED button.

- Submit with DSC: Sign the application using the registered Digital Signature Certificate of the selected authorized signatory.

- Submit with EVC: If the EVC option is selected, the system will trigger an OTP to the registered mobile phone number and e-mail address of the authorized signatory. Enter that OTP in the pop-up to sign the application.

Notes:

- The system generates an ARN and displays a confirmation message.

- GST Portal sends the ARN at registered email and mobile of the Taxpayer by e-mail and SMS.

- You can click the DOWNLOAD button to download the acknowledgement.

Note: You can click the DOWNLOAD button to download the acknowledgement.

(Republished with amendments)

****

Disclaimer: The contents of this article are for information purposes only and does not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

If anybody fails to furnish LuT, then what are the consequences

Kindly confirm source of FAQ. Is it self generated or released by CBEC ?

If by CBEC kindly share notification no or any other relevant source.

Is there any official notification no ?

Is it ARN is Final or any other Confirmation/Acceptance will Come from Dept.