![]()

(Validating Constitutional backing of Central Excise and Service Tax)

Prelude:-

Model GST law is in public domain since June 2016, President has given his assent to 101st Constitution Amendment Act, 2016 giving Central and State Govts power to levy GST on 08th September, 2016. However, till then there was nobody talking about the Excise Duty and its existence. GST has not yet been rolled out. Even the law is under preparation as yet. Then suddenly on 16.09.2016 what happened that everybody seems to be talking about it. Revenue secretary Mr. Hasmukh Adhia is tweeting one after another. So the big question as of now is that what happened which lead to such controversy and why everybody is discussing the very constitutional validity of Excise and Service Tax. The answer lies with the notification dated 16th September, 2016 which notified the 19 sections of the Constitution (One Hundred and First Amendment) Act, 2016.

Notification:-

Central Govt on 16.09.2016 issued a notification by which it notified the date of commencement of Constitution Amendment Act, enabling GST Law, which read as follows:-

“In exercise of the powers conferred by sub-section (2) of section 1 of the Constitution (One Hundred and First Amendment) Act, 2016, the Central Government hereby appoints the 16th day of September, 2016 as the date on which the provisions of Sections 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 13, 14, 15, 16, 17, 18, 19 and 20 of the said Act, shall come into force.”

Thus the above notification enables the Govt. to legislate the new GST Laws, remove all the Constitutionals hurdles to create a nationwide Goods and Service Tax regime subsuming various central and state taxes.

Other Articles on Controversy Surrounding GST

Controversial to excise duty farewell

Whether GST Council is constituted without Powers and is ILLEGAL?

No Excise from 16.09.2016 on goods other than Petroleum & Tobacco Products

Why this Controversy?

The controversy starts with section 17 which substitutes entry no. 84 of union list in place of earlier one. Earlier entry read as follows:-

“Duties of excise on tobacco and other goods manufactured or produced in India except………”

With powers of this entry the Central Government was allowed to levy excise on all the goods manufactured or produced in India.

Now the new entry substituted by Constitution (One Hundred and First Amendment) Act, 2016 is as follows:-

“84. Duties of excise on the following goods manufactured or produced in India, namely:—

(a) petroleum crude;

(b) high speed diesel;

(c) motor spirit (commonly known as petrol);

(d) natural gas;

(e) aviation turbine fuel; and

(f) tobacco and tobacco products.”;

This new entry substituted in place of earlier one which entitles Central Govt to levy Excise on these 6 items only. There is no entry in the Central list, which directly enable the Central Govt to levy duty of excise on goods other than the 6 mentioned above.

Govt. response to the Controversy

Ending days of confusion, the government has clarified that the notification of the provisions of the Constitution amendment Act for the goods and services tax (GST) does not take away the power of the central government to levy excise duty and service tax.

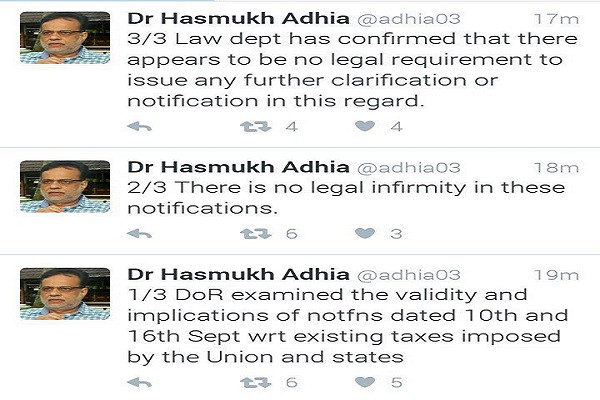

“DoR (department of revenue) examined the validity and implications of notifications dated 10th and 16th September with respect to existing taxes imposed by the Union and states. There is no legal infirmity in these notifications,” revenue secretary Hasmukh Adhia wrote on Twitter.

“Law department has confirmed that there appears to be no legal requirement to issue any further clarification or notification in this regard,” he said.

They cited section 19 of the amendment act which read as follows:-

“Notwithstanding anything in this Act, any provision of any law relating to tax on goods or services or on both in force in any state immediately before the commencement of this Act, which is inconsistent with the provisions of the Constitution as amended by this Act, shall continue to be in force until amended or repealed by a competent legislature or other competent authority or until expiration of one year from such commencement, whichever is earlier.”

Is Govt response correct ?

Govt response keeping section 19 in the forefront of all the controversy is challengeable. This section 19 talks about laws in force in any state. Not in the whole India. Thus there is a view that this provision does not cover central levies.

However the second leg of this section comes to save the Govt view once again, which says that earlier provisions shall continue to be in force until amended or repealed by a competent legislature or other competent authority. Thus this means that the laws amended by this Act shall not be amended so until such laws are repealed or one year elapses since the commencement of this act i.e. w.e.f. 15.09.2017 they shall automatically be repealed if not done so specifically.

Further, there is another entry No. 97 to the Union List, which is a residuary entry in that list

“97. Any other matter not enumerated in List II or List III including any tax not mentioned in either of those Lists.”

The Govt can also contemplate to include levy of excise in this entry as currently service tax is also told to be enabled via this entry only.

So, What should one do

Thus in my opinion, however the Govt have made a blunder in notifying sec 17 to this act w.e.f. 16.09.2016 still one should not take a view otherwise and at the same time should not take the risk of not depositing excise. Even if someone gets some relief from the court of laws, Govt can always go for retrospective amendments if they seem fit (as done earlier for Vodafone case).

Is the same issue is with levy of Service Tax since entry no. 92C has also been deleted?

Entry no. 92C reads as follows:-

“92C. Taxes on services.”

This entry has also been deleted by Govt. This entry was brought into the constitution by the Constitution (Eighty-eighth Amendment) Act, 2003 to give service tax a constitutional backing, which till then was governed by entry no. 97 only(residuary entry in Union List).

With this entry Govt also introduced one article no. 268A by the said act of 2003 to give central Govt absolute power to levy service tax which read as follows:-

268A 1) Taxes on services shall be levied by the Government of India and such tax shall be collected and appropriated by the Government of India and the States in the manner provided in clause (2).

(2) The proceeds in any financial year of any such tax levied in accordance with the provisions of clause (1) shall be—

(a) collected by the Government of India and theStates;

(b) appropriated by the Government of India andthe States, in accordance with such principles of collection and appropriation as may be formulated by Parliament by law.

This article 268A is also deleted by sec 7 of Constitution (101st) Amendment Act, 2016.

The website of the CBEC also displays the above 2 provisions to establish the constitutional validity of service tax law.

From the above discussion we can feel that due to deletion of these 2 provisions Service Tax will also be in peril like in case of Excise.

BUT there is a technical glitch made by Govt in 2003, which saved it now. Govt in 2003-04 forgot to notify this 88th amendment act and since then its commencement date has not yet been notified. Thus till now service tax law is constitutionally backed by entry no. 97 only and hence saved from controversy, when excise’s applicability might be in peril.

A positive take from the analysis

There is a positive take from sec 19 of constitution amendment act which says that laws shall be in force until amended or repealed by a competent legislature or other competent authority or until expiration of one year from such commencement, whichever is earlier.

This means that the validity of Excise, Service Tax and State VAT Laws shall cease w.e.f. 15.09.2017 and Govt shall have to roll out GST regime by that date. There is no going back since if in worst case scenario, Govt wants to go back, they will have to make Constitutional amendment once again, which is not going to be easy anyway. The same will then have to be passed by 50% state legislatures also. Thus I think it breaks all the predictions of GST being applicable w.e.f. 01.10.2017. It has to be rolled out completely before 15.09.2017

I hope the article will be helpful in understanding the controversy.

(CA Ranjan Mehta, +91-9672372075, ranjanmehta21@gmail.com)

A plot inherited by my mother was sold two months back and now with the amount we want to purchase a flat. Can I and my mother purchase the flat jointly? I want to keep her as second co-purchaser. Is it possible or there will be any tax implication?

Guide us so that the flat can be in my name directly without any tax implication to my mother due to sale of plot.

Looking forward to a speedy reply.