What we knows:

What we knows:

The Constitution Amendment Bill for Goods and Services Tax (hereinafter referred to as “GST”) has been approved by the President of India post its passage in the Parliament (by Rajya Sabha and by Lok Sabha) and has also been ratified by more than 50 percent of state legislatures. The Government of India is committed to replace all the indirect taxes levied on goods and services by the Centre and States and to implement GST by April 2017.

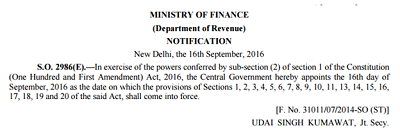

Notification from the Govt.

From the above notification dated 16/09/2016 brought in effect all the sections of Constitutional (One Hundred and First Amendment) Act, 2016, which will result in rolling out of Goods & Service Tax. We all welcome this footstep of GST era and it shall be appreciated.

Article 265 of the Constitution of India provides that no tax shall be levied or collected except by the authority of law. Furthermore, insertion of new article 246A makes a clear division of power to make laws with respect to goods and services tax imposed by the Union or by such State, as enumerated in the Seventh Schedule of the Constitution.

Whether GST Council is constituted without Powers and is ILLEGAL?

No Excise from 16.09.2016 on goods other than Petroleum & Tobacco Products

What Old provision says:

Prior to the said amendment, the Excise duty was levied and collected by the Central Government, which was constitutionally backed by entry 84 of List-I (Union List) of the Seventh Schedule of the Constitution, which is extracted herein below for ready reference–

“84. Duties of excise on tobacco and other goods manufactured or produced in India except—

a) alcoholic liquors for human consumption;

b) opium, Indian hemp and other narcotic drugs and narcotics,

but including medicinal and toilet preparations containing alcohol or any substance included in sub-paragraph (b) of this entry.”

Amended Provision

Entry 84 is now amended by the Section 17 of the Constitutional (One Hundred and First Amendment) Act, 2016 and would now read as–

“84. Duties of excise on the following goods manufactured or produced in India, namely:—

a) petroleum crude;

b) high speed diesel;

c) motor spirit (commonly known as petrol);

d) natural gas;

e) aviation turbine fuel; and

f) tobacco and tobacco products.”

Ramification to amendment

Due to this amendment in the entry 84 of the Seventh Schedule of the Constitution, the power of the Central Government has been brought to a limited extent. Now, the Central Government has power to legislate had been curtailed and now the Central Government can only levy duty of excise on specified products. As a result of this, the Central Excise Act, 1944 shall become ultra vires to the extent inconsistent with the Constitution, Which means that the Central Excise Act, 1944 shall remain valid/ enforceable for only specified goods and the rest of goods shall now be out of scope of levy of Excise Duty.

Has the Government lost the power to levy of excise duty?

After reading the above said new amendment of the Constitution, we are understanding that the Central Government to levy excise duty only on mentioned six items. Moreover, there is no entry in the Central list, which directly enables the Central Government to levy duty of excise on goods other than the mentioned six items.

Transitional provision

There is a counter to this, by saying that Section 19 of Constitutional (One Hundred and First Amendment) Act, 2016 provides from transitional provision, states that; –

“19. Notwithstanding anything in this Act, any provision of any law relating to tax on goods or services or on both in force in any State immediately before the commencement of this Act, which is inconsistent with the provisions of the Constitution as amended by this Act shall continue to be in force until amended or repealed by a competent Legislature or other competent authority or until expiration of one year from such commencement, whichever is earlier.”

After reading this underlined provision, a controversial view of Government is coming. This provision states that the earlier provisions shall continue to be in force until amended or repealed by a competent legislature or other competent authority. Thus, it means that the provision amended in the Constitution shall not be amended, until such laws are repealed by a competent legislature or other competent authority or one year elapses since the commencement of this act i.e. 15th Sep.2017.

Controversial things

One of my views is that Central Government can still use the underlined phrase for levy of Excise duty and second view is that the Central Government can still draw power from entry 97 of List I of Seventh Schedule, the same entry which enables it to collect Service Tax. Having said this, this awkward situation was completely avoidable if the notification were issued with little more precautions.

Government response to the amendment:

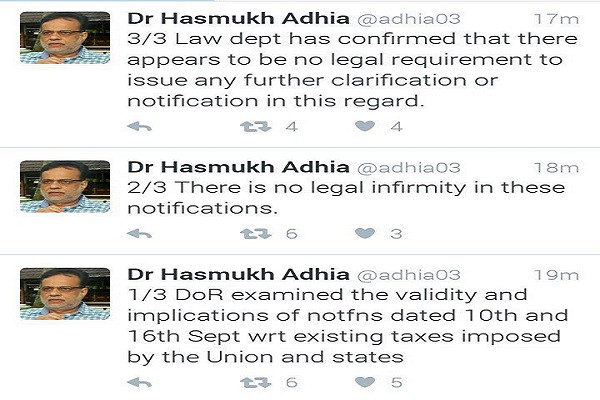

After many rumors spread around the public, to say good bye to Excise duty. Thanks to the Revenue secretary of GoI, Dr. Hasmukh Adhia, who tweeted and clarified via tweet states that “Department of Revenue examined the validity and implications of notifications dated 10th and 16th September with reference to existing taxes imposed by the Union and states. There is no legal infirmity in these notifications. Law department has confirmed that there appears to be no legal requirement to issue any further clarification or notification in this regard.”

Conclusion:

For this I would like to bring it to your attention that the scope of this transitory provision shall be limited to the taxes levied under an act enacted by the Legislature or any other authority (Eg. Municipal Corporations). It shall not cover within its ambit the taxes which are legislated by the Parliament.

The Central government can still levy Excise duty production or manufacture of all goods under the cover of above underlined phrase Section 19 of the Constitution. Thus the article is based on the interpretation of the said Constitutional Amendment.

(The author is Prafful Lalwani, qualified Company Secretary. His areas of specialization includes Corporate law and Taxation and offering all type of consultancies. Should you have any query/ clarification feel free to contact him, he can be reached at prafful.lalwani@gmail.com)