This article analyses the eligibility of Input Tax Credit (ITC) on purchase of two-wheelers and similar vehicles for normal traders or manufacturers who are not engaged in passenger transport, vehicle trading, leasing, or driving training. Under Section 17(5)(a) of the GST Act, ITC is blocked on motor vehicles used for transportation of persons having seating capacity up to 13, which covers most two-wheelers. ITC is allowed only if such vehicles are used for further supply, passenger transport, or driving training. Although ITC is not blocked for vehicles used for transportation of goods, claiming ITC on two-wheelers for goods transport is difficult without a valid goods carriage permit under the Motor Vehicles Act, 1988. E-scooters are treated as motor vehicles and face the same restriction. However, full-pedal bicycles and pedal-assisted e-bikes are not motor vehicles, hence ITC is fully available. Forklifts are also eligible for ITC as they are excluded from the definition of motor vehicles.

Assumption about the business

For the purpose of this discussion, the analysis is restricted to a normal trader or manufacturer who:

- is not engaged in passenger transportation,

- is not engaged in imparting training on driving motor vehicles, and

- is not engaged in the further supply of motor vehicles, meaning:

-not a dealer or manufacturer of motor vehicles, and

-not engaged in renting, leasing, or hiring of motor vehicles.

Majority of businesses are normal traders or manufacturers. Accordingly, this article is written specifically from the point of view of such taxpayers.

Q.1 Am I eligible to take ITC on a normal bike/scooter purchased for office purposes?

Ans:

- No, merely calling it “office purpose” does not help.

- Two-wheelers are normally meant for transportation of persons.

- Section 17(5)(a) of GST Act blocks ITC on motor vehicles used for transportation of persons.

Q.2 What is Section 17(5)(a)? Please explain it to me in detailed and simple manner

Ans: Section 17(5)(a) of the GST Act is a blocking provision. As per section 17(5)(a):

- ITC is NOT allowed on motor vehicles used for transporting persons

- This applies when the vehicle has seating capacity of 13 or less (driver included)

Two-wheelers automatically fall here, because it is:

- Motor vehicles

- Used mainly for transporting persons

- Seating capacity is far below 13

ITC on motor vehicles used for transportation of persons is allowed only when the vehicle is used for:

- Further supply of such motor vehicles (i.e., trading or leasing of vehicles),

- Transportation of passengers (e.g., taxi, cab, bus operations), or

- Imparting training on driving such motor vehicles (e.g., driving schools).

Q.3 Section 17(5)(a) blocks ITC if motor vehicles are used for transportation of persons. What about motor vehicles used for transportation of goods?

Ans: Section 17(5)(a) does NOT block ITC for motor vehicles used for transportation of goods.

Q.4 But I am going to use the two-wheeler for transportation of goods, not persons. So Am I not eligible for ITC?

Ans:

- In theory – ITC may be available

- In practice – very difficult to prove

Why?

- Two-wheelers are inherently designed for carrying persons

- Department will presume personal transport

Q.5 What proof is required to show if it is used for goods transportation?

Ans:

- Mere internal declaration is not sufficient

- Strongest documentary proof comes from the Motor Vehicles Act. Goods carriage requires permit under Motor Vehicles Act 1988

Relevant provisions of MV Act 1988:

- Section 66 – says Permit compulsory for using the vehicle as transport vehicle in any public place

- 3rd proviso of Section 66 – Goods transport for business is legally recognised only when backed by a goods carriage permit.

- Section 77 – deals with – Application for goods carriage permit

- Section 78 – deals with – Consideration of application

- Section 79 – deals with – Grant of goods carriage permit

Q.6 I am using it only for goods transport but I don’t have a permit. Whether the GST act says that permit as per MV Act is required?

Ans: No, the GST Act does not talk about MVA permits.

If the MV Act requires a permit, absence of permit weakens your case.

Q.7 Swiggy/Zomato riders carry goods(foods). Do they have permits?

Ans:

- As per Motor Vehicles Act – permit is required

- Section 66 third proviso clearly allows:

carriage of goods for business, subject to permit conditions

Law vs practice:

- Practice may differ

- Law is very clear – permit required

Q.8 Is my two-wheeler a ‘motor vehicle’ for section 17(5)(a)?

Ans: Yes

- Section 2(76) of CGST Act adopts definition of Motor Vehicle from MV Act 1988

- Section 2(28) of Motor Vehicles Act, 1988 defines Motor vehicle

Motor vehicle means:

- Any mechanically propelled vehicle

- Adapted for use on roads

- Powered by propulsion from internal or external source

It includes:

- Chassis, even if body is not attached

- Trailer attached to a vehicle

The following are excluded from Motor Vehicle:

- Vehicles running on fixed rails (train, tram, metro)

- Vehicles of special type, used only inside factory or enclosed premises (Forklift)

- Vehicles having less than 4 wheels with engine capacity below 25 cc

Q.9 Is two wheeler a motor cycle? Is it different from motor vehicle?

Ans:

- Section 2(27) of MV Act says Motor-cycle means a two-wheeled motor vehicle

So every motor cycle is a motor vehicle.

Q.10 What is a mechanically propelled vehicle?

Ans: A motor vehicle driven by petrol, oil, steam, or electricity1

Q.11 Are E-Scooters and Electric Bicycles mechanically propelled?

Ans: Yes

E-scooters2 are mechanically propelled vehicles

Electric bicycles2 are slightly different from e-scooters where a bicycle has an electric motor attached and the motor can be used as an alternate means of propulsion. The vehicle is treated as a mechanically propelled vehicle under the Road Traffic Acts (Ireland). This applies whether or not the motor is actually being used

Conclusion:

- E-scooters → mechanically propelled

- Electric bicycles (with motor assistance) → mechanically propelled

So ITC restrictions on E-Scooters and Electric Bicycles are the same as the normal bike/scooter given in the first question.

Q.12 What is a vehicle having less than 4 wheels with engines capacity less than 25cc?

Ans: Such vehicles are so small and low-powered

- They are often used as toys or recreational mini-bikes

- These are not regular commuter bikes or scooters

- These are usually off-road or private-use mini vehicles and not common on public roads

- These are typically found in Fun parks / theme parks

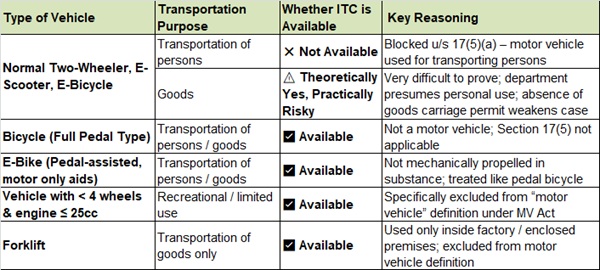

Vehicles with engine ≤ 25 cc and less than four wheels are not treated as motor vehicles under the Motor Vehicles Act. So they are not affected by Section 17(5) blocking provisions. So ITC is available.

Q.13 Whether ITC is available on purchase of a Bicycle (Full Pedal Type)?

Ans: Yes, ITC is available. No conditions.

Why?

- A full-pedal bicycle is not mechanically propelled

- Hence, it is not a “motor vehicle” under the Motor Vehicles Act

- Since it is not a motor vehicle, Section 17(5) blocking provision does not apply

Bottom line:

- It does not matter whether the bicycle is used for:

- transporting persons, or

- transporting goods

ITC is fully allowed without any restriction.

Q.14 Whether ITC is available on purchase of an E-Bike?

Ans. To answer this, we must first understand what an e-bike actually is.

As per Article 1(h) of EU Directive 2002/24/EC2, an e-bike is defined as:

A cycle with pedal assistance, equipped with an auxiliary electric motor of maximum continuous rated power of 0.25 kW, where the motor output is progressively reduced and cut off once the vehicle reaches 25 km/h or when the rider stops pedalling.

It means

- Pedalling is mandatory

- The electric motor is only an assist, not the main propulsion

- The vehicle cannot move on motor power alone

- Human effort remains the primary source of movement

Is an e-bike a mechanically propelled vehicle?

- No, in substance, it functions like a pedal bicycle

- The electric motor merely supports the rider

- Propulsion still comes from human effort

Hence, an e-bike is treated at par with a fully pedal-operated bicycle.

GST impact – Section 17(5)

- Section 17(5) blocks ITC only for motor vehicles

- A pedal-assisted e-bike does not qualify as a motor vehicle

- Therefore, the blocking provision does not apply

Q.15 Whether ITC is available on purchase of a forklift?

Ans: Yes. Section 17(5)(a) blocking provision does not apply. ITC is available on purchase of a forklift

- The primary purpose of a forklift is transportation of goods, not persons.

- A forklift is not a motor vehicle under the Motor Vehicles Act.

- It falls squarely under the exclusion in the definition of motor vehicle, namely: “Vehicle of special type adapted for use only in a factory or in an enclosed space.”

Since a forklift is excluded from the definition of motor vehicle, it is outside the scope of Section 17(5)(a).

Conclusion Matrix

References:

1. https://www.oxfordreference.com

2. https://www.oireachtas.ie/en/debates/question/2019-05-08/1302/#pq-answers-1302

*****

Disclaimer: The content of this article is the personal views of the author as a knowledge sharing initiative and not professional advice and the author assumes no responsibility for the use of this information. The author can be reached at sivaraman004@gmail.com

Author Bio