Understand the intricacies of RERA Section 4(2)(l)(D) requiring real estate promoters to deposit 70% of funds in a separate account. Explore the purpose, compliance process, and the role of professionals like architects, engineers, and CAs. Learn about the regulations, rules, and directions issued by RERA authorities, ensuring transparency and protecting the interests of real estate consumers.

In this article, I will be discussing about the requirement of depositing 70% of money received from allottees of a real estate project in a separate bank account as per section 4(2)(l)(D) of RERA.

Purpose of RERA

- Regulation and promotion of real estate sector.

- Ensure sale of real estate project in an efficient and transparent manner.

- Protect the interest of consumers in the real estate sector.

- Establish an adjudicating mechanism for speedy dispute redressal.

Under which Ministry the law is enacted?

Ministry of Housing & Urban Poverty Alleviation, Government of India.

Acts and Rules in Kerala

a. The Real Estate (Regulation and Development) Act, 2016 (hereinafter referred to as RERA)

RERA is a Central Act enacted by Parliament and the same is to be implemented by the State Governments/Union Territories. The rules and regulation making power is with the State Government. The State Government also has to appoint Regulatory Authority and set up the Appellate Tribunal. Each state will take into account the special circumstances of the State within the broad parameters laid down in the Act.

b. The Kerala Real Estate (Regulation and Development) Rules, 2018 (hereinafter referred to as Rules)

The Government of Kerala established K-RERA (Authority). In exercise of power conferred by Section 84 of RERA, the Kerala Government formulated rules in the year 2018.

c. Kerala Real Estate Regulatory Authority (General) Regulations, 2020 (hereinafter referred to as Regulation)

In exercise of power conferred by section 85 of RERA, the K-RERA formulated regulations in the year 2020.

What RERA Section 42LD says?

Section 4(2)(l)(D) of RERA

1. Declaration is to be submitted by the promoter to the Authority that

a. 70% of the amounts realized for the project from the allottees, from time to time, shall be deposited in a separate account (I will call as 70% RERA account) to be maintained in a scheduled bank to cover the cost of construction and land cost and shall be used only for that purpose

b. Promoter shall withdraw the amounts from this 70% account, to cover the cost of project in proportion to the percentage of completion.

c. Certificate from Engineer, Architect, and a CA in practice that the withdrawal is in proportion to the % of completion.

2. Promoter shall get his accounts audited

-

- within 6 months after the end of every FY

- by a CA in practice and

- shall produce a statement of accounts

- CA shall also certify that amounts collected for project have been utilized and withdrawal has been in compliance with the proportion to the % of completion

What Kerala Rules 2018 Says?

Rule 6 – This rules speaks about what is land cost and construction cost for the purpose of Section 4(2)(l)(D)

What Kerala Regulations 2020 says?

a. Regulation No. 4(1) – Promoter shall maintain separate bank account for each project

b. Regulation No. 4(2) – Promoter shall furnish a certificate from the bank on bank’s letter head in Form 1, stating that the account number is a separate account in compliance with section 4(2)(l)(D) of RERA.

c. Regulation No. 4(3)

Certificate in Form 2 – Issued by Architect – of % of completion

Certificate in Form 3 – Issued by Engineer – of estimated cost and cost incurred

Certificate in Form 4 – Issued by CA in practice – of estimated cost and cost incurred. Amount withdrawable from 70% account. Amount already withdrawn and balance that can be withdrawn.

d. Regulation No 4(4)

Annual report on statement of accounts in Form 5 – Certified by CA in Practice. To be uploaded by Promoter in RERA webpage on or before 31st October.

(Heading in the Form 2, 3 and 4 also states that these certificates has to uploaded in the webpage before withdrawal of money)

Role of Banks in designing accounts in compliance with RERA

a. Most of the banks have designed opening and operation of accounts, in order to ensure compliance with section 4(2)(l)(D).

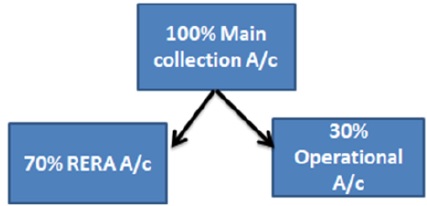

b. Bank will open three accounts

a. 100% Main Collection account – 100% amount collected from allottees will be deposited in this account. At the End Of Day (EOD) of collection, 70% will automatically get sweeped to RERA account and 30% to Operational Current account.

b. 70% RERA Account – Fund transferred from Main collection account. This account will be informed and registered with RERA Authority through Form 1 (Supra). There will be a separate word ‘’RERA” mentioned in this account.

3. 30% Operational Account. Fund in this account will be freely available for utilization for project cost and for day to day operation.

c. For 100% Main and 70% RERA account, bank will not give Cheque book facility and Debit card. Internet banking facility will be given only with viewing rights.

d. Amongst other things, bank will ask for

a. Special agreement from Promoter regarding compliance of RERA.

b. Indemnity clause that Promoter will indemnify the bank against all losses.

c. Details of Architect, Engineer and CA of the promoter with their signature and seal.

d. At the time of withdrawal from 70% RERA account, bank may rely on the certificate from Architect, Engineer and CA & an undertaking from Promoter that withdrawal is in compliance with RERA.

e. Closure of these special accounts will be permitted provided project is completed and completion certificate has been obtained from RERA Authority.

e. Name of RERA modeled bank account will be the Project name (not Firm or Companies Name). For example, the name of the Promoter is “M/s ABC Builder Private Limited” and the name of the project is “ABC OCEAN VIEW APARTMENT”. RERA account name will be “ABC OCEAN VIEW APARTMENT”

Sample fund flow model on deposit and withdrawal

Assume allottee gave Rs 1 Crore in 100% Main collection Account. End of the day Rs 70 lakhs will be automatically transferred to 70% RERA account and Rs 30 lakhs to 30% Operational account.

Withdrawal 1 – Promoter is entitled to use Rs 30 lakh lying in 30% operational account. Once Rs 30 lakhs is utilized for the project, she can withdraw another Rs 30 lakhs from 70% RERA account. Promoter should get ready with Certificate from Architect, Engineer and CA in practice.

Withdrawal 2 – Once Rs 30 lakh from withdrawal 1 is also exhausted for project, she can withdraw another Rs 30 lakh from 70% RERA account.

42LD’s Purpose

- Prevent siphoning of fund.

- If promoter has own fund or loan fund, she can spend from that also and then withdraw the same from 70% RERA a/c.

- RERA Authority is telling the Promoter like this (Author’s imagination) – “First spend from the money already lying in your hand. Then you can withdraw the balance from 70%. Why we will not allow you to use 100% freely? It is allottee’s hard earned money. We want to ensure its protection.”

- Moral of the story – First spend. Then withdraw.

FAQ issued under RERA

Question 34 – Is the promoter required to maintain an ‘escrow account’ or a ‘separate account’? Is a ‘separate account’ to be maintained for every project or it can be for one or more projects? What are the purposes for which the promoter can withdraw the money from the separate account?

Answer – Section 4(2)(l)(D) provides that the promoter shall maintain a ‘separate account’ for every project undertaken by him wherein seventy percent of the money received from the allottees shall be deposited for the purposes of construction and land cost. The account has to be self-maintained and is not an escrow account requiring the approval of the Authority for withdrawal. Section 4(2)(l)(D) clearly provides that the funds can only be used for construction and land cost.

Role of CA

i. In Form 4, CA is certifying about the amount that can be withdrawn from 70% RERA account based on records, documents, management explanation and books of accounts.

ii. In Form 5, CA is certifying fund flow of 70% RERA account.

iii. CA has to ensure that the RERA account is indeed a 70% RERA account and not a normal current account.

iv. Ensure that RERA account is informed to Authority in Form 1 (supra). Get a copy of Form 1.

v. Cross check Form 2 and Form 3 (Architect and Engineer certificate) (supra).

Statutory auditor cannot certify Form 4

As per regulation 4(5), promoter shall designate an Architect, an Engineer, a CA who issues certificate regarding compliance of section 4(2)(l)(D) of RERA. These professionals cannot be changed without intimation to the Authority.

Explanation 1 to regulation 4(5) states that CA certifying progress of work for withdrawal of amounts from the separate account should be a ‘’different entity” than CA who is the statutory auditor.

Explanation 2 to regulation 4(5) further states that if Form 5 issued by the CA reveals that any certificate in Form 2,3 and 4 is false, the RERA authority may bring the matter to the concerned regulatory body of Architect, Engineer or CA for necessary penal action against them.

Penalty for Non Compliance

- Section 60

- If promoter provides false information or contravenes section 4

- Penalty may extend upto 5% of the estimated cost of the project

Haryana RERA’s detailed direction on RERA bank account

H-RERA has observed in one prominent builder’s case that, the promoter has maintained only a single escrow account and deposited the entire sale proceeds in the said account. The promoter has also allowed lenders of the project to withdraw amounts from such account for loan repayment.

After instances of irregularities in fund management by certain promoters, Haryana RERA has issued detailed directions to promoters with regard to opening of bank accounts as per RERA. It is called “The Haryana Real Estate Regulatory Authority, Gurugram Real Estate Bank Accounts for the Registered Projects Directions, 2019” vide notification dated 10.05.2019.

Amongst other things, the above direction has mandated requirement of maintaining MASTER account, RERA account and FREE account in the same bank branch. MASTER and RERA account shall also be free from all encumbrances, lien, loan and control of any third party ie lender/bank/financial institutions. The direction has specifically stated that funds from 70% RERA account shall be released upon submission of relevant certificates as per the provision of RERA.

Conclusion

42LD is one such serious section which is to be very strictly complied with by the promoters of the project. The responsibility of the professionals is also very huge since one of the very purposes of RERA is to protect customers’ hard earned money and avoid its misuse.

The author can be reached at sivaraman004@gmail.com

Author Bio