CA Rockey

In this article I have discussed the provisions related to Input Tax Credit (ITC), Returns and Matching of ITC as proposed in report of Sub-Committee-II on Model GST Law.

In this article I have discussed the provisions related to Input Tax Credit (ITC), Returns and Matching of ITC as proposed in report of Sub-Committee-II on Model GST Law.

A. Input Tax Credit:-Section 18 of GST Act, 2016, deals with provisions related to Input Tax Credit (ITC). Sec. 2(36) states that Input tax means IGST/CGST/SGST paid/charged on supply of Goods/Services which are used, or are to be used, in the course or furtherance of his business.

Sec. 2(37) stipulates that ITC means taking credit of input tax.

Therefore ITC means taking credit of IGST/CGST/SGST paid on supply of goods/services.

Sec. 18 states that Every taxable person shall, subject to such conditions and restrictions as may be prescribed in this behalf, be entitled to take credit of input tax and may deduct the amount of admissible credit in respect of a tax period from the output tax for the same period and pay the remaining amount, if any, to the credit of the appropriate Government (i.e. Central Government in case of the IGST and the CGST, and the State Government in case of the SGST) within such time and in such manner, as may be prescribed.

Pre-Conditions for claiming ITC:

1. Taxable person must be in possession of a Tax invoice issued by supplier.

2. Tax charged in respect of such supply has been paid to the credit of the appropriate Government (either in cash or through utilization of ITC) by the supplier.

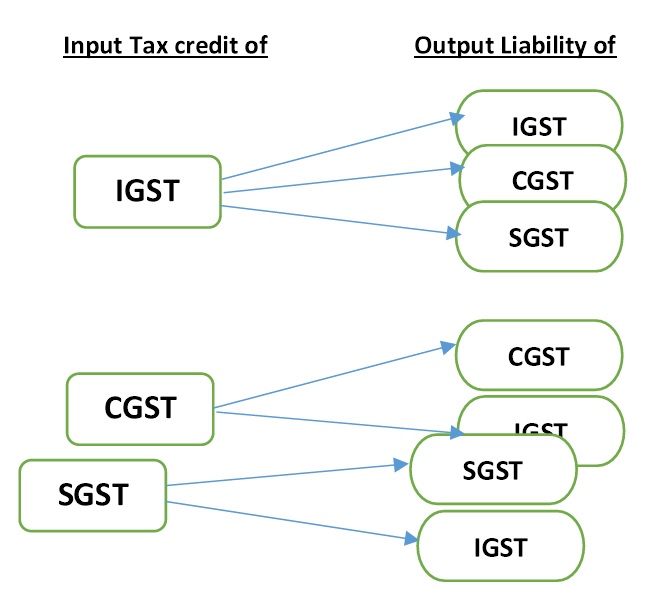

Manner of taking credit of IGST/CGST/SGST:

1. IGST paid on interstate purchase shall first be utilised towards payment of IGST; then (if amount remaining) towards payment of CGST and SGST.

2. CGST paid on purchase shall first be utilised towards payment of CGST; then (if amount remaining) towards payment of IGST.

3. SGST paid on purchase shall first be utilised towards payment of SGST; then (if amount remaining) towards payment of IGST.

4. ITC of CGST cannot be utilised towards payment of SGST.

5. ITC of SGST cannot be utilised towards payment of CGST.

Where ITC in a tax period is more than Output tax liability in that period then such excess credit may be carried forward for adjustment against the output tax of the subsequent tax period in the same manner.

Refund of unadjusted ITC:-Refund can be claimed only in following cases:

1. Export (except where the goods exported out of India are subjected to export duty).

2. Where the credit has accumulated on account of rate of tax on inputs being higher than the rate of tax on outputs.

Restrictions on ITC:-In followings case ITC shall not be available:

(a) Motor vehicles, except when they are supplied in the usual course of business or are used for providing the following taxable services—

(i) Transportation of passengers,

(ii) Transportation of goods,

(iii) Imparting training on motor driving skills;

(b) High speed diesel oil, motor spirit (commonly known as petrol), and aviation turbine Fuel, petroleum crude oil and aviation gasoline;

(c) goods or services provided in relation to outdoor catering, beauty treatment, health services, cosmetic and plastic surgery, membership of a club, health and fitness Centre, life insurance, health insurance and travel benefits extended to employees on vacation such as leave or home travel concession, when such goods and/or services are used primarily for personal use or consumption of any employee;

(d) Goods and/or services acquired by the principal in the execution of works contract when such contract results in construction of immovable property, other than plant and machinery;

(e) goods acquired by a principal, the property in which is not transferred (whether as goods or in some other form) to any other person, which are used in the construction of immovable property, other than plant and machinery;

(f) Goods and/or services on which tax has been paid under section 8 of the Act; and

(g) Goods and/or services used for private or personal consumption, to the extent they are so consumed.

These restrictions are similar to those provided in Existing Cenvat Credit Rule, 2004.

B. Returns under GST Law:-

| S. No. | Form No. | Purpose | Due Date |

| 1. | GSTR-1 | Outward supplies made by supplier (other than compounding taxpayer and ISD) | 10th of the next month |

| 2. | GSTR-2 | Inward supplies received by a taxpayer (other than compounding taxpayer and ISD) | 15th of the next month |

| 3. | GSTR-3 | Monthly return (other than compounding taxpayer and ISD) | 20th of the next month |

| 4. | GSTR-4 | Quarterly return for compounding taxpayer | 18th of the next month |

| 5. | GSTR-5 | Periodic return by Non-resident foreign tax payer | Last day of registration |

| 6. | GSTR-6 | Return for ISD | 15th of the next month |

| 7. | GSTR-7 | Return for TDS | 10th of the next month |

| 8. | GSTR-8 | Annual Return | 31st December of Next FY |

Procedure to file Return for a taxpayer other than compounding taxpayer and ISD

a. First of all a taxable person need to file details of his outward supplies (i.e. sale) in a tax period In from GSTR-1 within 10 days from the end of that tax period.

b. Then taxable person need to furnish details of his inward supplies (i.e. purchase) in a tax period in form GSTR-2 within 15 days from the end of that tax period.

c. After that he has to file monthly return in from GSTR-3 within 20 days from the end of that tax period.

d. At the last Annual return has to be filed in from GSTR-8 within 31st December of next Financial Year.

a. Details/return of outward supplies:- 34 deals with provision related to furnishing the details of outward supplies by the supplier as follows:

1. Every registered taxable person (except compounding taxpayer) shall furnish electronically, the details of all outward supplies (including Credit/Debit notes issued by him) affected by him during the tax period.

2. Details of outward supplies furnished by supplies shall be communicated to all corresponding recipient/buyer of such supply within 15th day of the month.

3. Correction in details/return of outward supplies: A register person upon discovery of any error in the GSTR-1 relating to

i) tax paid by him or

ii) input tax credit availed of by the recipient but remaining unmatched under section 38 (discussed herein after),

rectify such error in the tax period during which such error is noticed and shall pay the tax and interest, if any, in case there was a short payment of tax on account of such error, in the return to be furnished for such tax period.

b. Details/return of inward supplies:- 35 deals with provision related to furnishing the details of inward supplies by the recipient/buyer as follows:

1. Every register taxable person shall receive a pre-filled GSTR-2 (i.e. details/return of inward supply/purchase).

2. Every register taxable person shall verify, validate, modify or, if required, delete the outward supplies and credit or debit notes communicated in pre-filled GSTR-2 to prepare details of his inward supplies.

3. Every registered taxable person shall furnish, electronically, the details of inward supplies of taxable goods and/or services, including inward supplies of services on which the tax is payable on reverse charge basis in GSTR-2 within 15 days from the end of the month.

4. Correction in details/return of inward supplies: A register person upon discovery of any error in the GSTR-2 relating to

i) input tax credit availed of by him or

ii) tax paid by the supplier but remaining unmatched under section 38 (discussed herein after),

rectify such error in the tax period during which such error is noticed and shall pay the tax and interest, if any, in case there was a short payment of tax on account of such error, in the return to be furnished for such tax period.

c) Return u/s 36:-36 contains the provision parting to monthly detailed return to be filed by every registered taxable person as follows:

1. After filing the details of outward supplies in GSTR-1 and Details of inward supplies in GSTR-2, every registered taxable person is required to file electronically followings details in GSTR-3 within 20 days from the end of the month.

i) Inward and outward supplies of goods and/or services,

ii) input tax credit availed,

iii) tax payable,

iv) tax paid and

v) other particulars as may be prescribed

Note: A registered taxable person shall not be allowed to furnish return for a tax period if return for any previous tax period has not been furnished by him. (I.e. if a registered taxable person want to file return for the month of Aug-2016 and he has not filed return for the month of Jul-2016 (where he is liable to file) then he cannot file the return for the month of Aug-2016 until he file return for the previous period that is jul-2016.

2. Every registered taxable person has to file a valid return for allowing input tax credit in respect of supplies made by him. A Valid return refer to a return in which full tax due as per return has been paid.

Note: If Mr. X purchase goods of rs. 1,00,000/- from Mr. Y and paid rs. 15,000/- as CGST/SGST to Mr. Y.

In this case, Mr. X can take the credit of Input tax of rs. 15,000/- paid by him only if Mr. Y filed a valid return (assuming the all conditions are complied with).

3. If there is no sale/purchase during the tax period then every such registered taxable person are required to file a nil return.

4. Correction in Return: If any registered taxable person after filling the return discovers any omission or incorrect particulars therein, other than as a result of audit, inspection or enforcement activity by the tax authorities, he shall rectify such omission or incorrect particulars in the return to be filed for the month or quarter, as the case may be, during which such omission or incorrect particulars are noticed.

d. Annual Return:-

1. Every registered taxable person, other than a casual or non-resident taxable person, shall furnish an annual return for every financial year electronically in such form and in such manner as may be prescribed on or before the thirty first day of December following the end of such financial year.

2. Every taxable person who is required to get his accounts audited under subsection (4) of section 32 shall furnish, electronically, the annual return along with the audited copy of the annual accounts and a reconciliation statement, reconciling the value of supplies declared in the returns furnished for the year with the audited annual financial statement, and such other particulars as may be prescribed.

e. Final Return:-

1. Every registered taxable person who applies for cancellation of registration shall furnish a final return along with the application for cancellation of registration in such form and in such manner as may be prescribed.

Levy of late fee:

Any registered taxable person who fails to furnish the details of outward or inward supplies or return required under this GST Act by the due date shall be liable to a late fee of rupees one hundred for every day during which such failure continues subject to a maximum of rupees five thousand.

C. Matching of Input Tax Credit (including Credit/Debit Notes):-This is the very significant and different feature of model GST law. In the proposed scheme of allowing credit of input tax paid on purchase, it is ensure that before finally allowing such credit Government has received the payment of such input tax claimed by recipient/buyer. This is simple that now department wants to link invoice to invoice for allowing ITC to eliminate any ambit for revenue leakage.

Scheme of propose allowing input tax credit is as follows;

i. On filling of the return in GSTR-3, ITC shall be provisionally allowed as claimed in GSTR-3 and credited to the input tax ledger of such person.

ii. ITC as claimed in GSTR-3 shall be finally allowed after matching of ITC as per the provision of sec. 38.

iii. If there is any duplicity in the claim of ITC or ITC as claim is not paid by the corresponding supplier then ITC claimed shall be reversed by such amount.

iv. Such reversed ITC shall be allowed finally if corresponding amount of such reversed ITC is paid by corresponding/relevant supplier.

Matching and reversal of ITC: Scheme of Matching of ITC is as follows:-

1. After due date of GSTR-3 (i.e. 20th of the following month) the ITC claimed by the taxable person shall be verified to check:

i. Duplication of claims and

ii. matched with the corresponding outward supply and/or debit note declared by the supplier in his valid return for the same or any previous tax period.

2. When claim of ITC matched with the tax paid on corresponding outward supply declared by the supplier in his valid return, then such claim shall be finally allowed and communicated to the taxable person claiming such ITC.

3. If clam of ITC does not match with the corresponding outward supply declared by the supplier in his valid return then the discrepancy shall be notified to both such taxable person.

4. Where the taxable person making the outward supply does not rectify the discrepancy communicated in point 3 (above) in his valid return for the tax period succeeding the period in which the input tax credit was claimed by the recipient, the input tax credit provisionally allowed earlier shall stand reduced to the extent of discrepancy in the input tax credit ledger of the recipient.

5. Where input tax credit is reduced on account of failure to rectify the discrepancy as communicated, the taxable person claiming the input tax credit shall be informed in the manner prescribed.

3. On being informed, the taxable person shall pay an amount equal to the input tax credit reduced along with applicable interest in the return for the tax period in which the reduction is communicated.

The concept of Matching and reversal of ITC

(Author can be contacted at M- 08287392720 or on Email: carockey99@gmail.com)

Click Here to Read Other Articles of CA Rockey

Author Bio

RESPECTED AUTHOR, IT WAS CLARIFIED FROM THE OFFICIAL SOURCES THAT THERE IS NO SUCH MODEL LAW DRAFT RELEASED EXCEPT 4 (REGISTRATION,RETURNS,PAYMENTS & REFUNDS) REPORTS BY THE JOINT COMMITEE OF GST. IN MY OPINION REFERRING AND RELYING UPON SUCH UNPUBLISHED MATERIAL IS NOT CORRECT.

Thank you

sir many many thanks for your good efforts

Sir very usefull information gud keep it up