In view of notification No. 2/2019 – Central Tax (Rate) dated 07/03/2019, the Central Government, on the recommendations of the Council, has notified Composition Scheme for Service provider which can be opted from 01/04/2019. Previously, service providers are kept out of ambit of composition scheme u/s 10(1) of CGST Act.

A. Description of Supply:

First supplies of goods or services or both up to an aggregate turnover of fifty lakh rupees made on or after the 1st day of April in any financial year, by a registered person.

Explanation: -For the purposes of this notification, the expression “first supplies of goods or services or both” shall,

a. for the purposes of determining eligibility of a person to pay tax under this notification, include the supplies from the first day of April of a financial year to the date from which he becomes liable for registration under the said Act

Analysis:

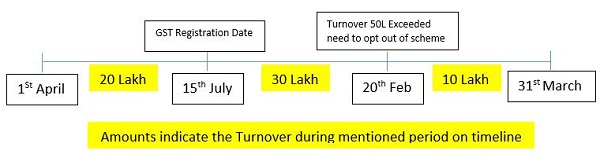

This composition scheme can be availed up to turnover of Rs. 50 lakh.

For Example – If any unregistered service provider exceeds the threshold limit of 20 Lakh under GST Act on 15th July, he needs to get register under GST Act. He can opt for above mentioned composition scheme on date of registration, up to the limit of Rs. 50 Lakh i.e. further turnover Rs. 30 Lakh after registration.

At 20th February, he exceeds the limit of Rs. 50 Lakh = 20 Lakh (till 15th July) + 30 Lakh (from 16th July to 20th February). So after 20th February, he will be ineligible for this composition scheme and has to pay tax as per regular tax payer.

b. for the purpose of determination of tax payable under this notification shall not include the supplies from the first day of April of a financial year to the date from which he becomes liable for registration under the Act.

Continued with example, Service provider has to pay GST at the rate of 6% (3% CGST & 3% SGST) on turnover of Rs. 30 Lakh only, achieved by him during 16th July to 20th February after registration on 15th July.

1. Conditions:

Mentioned Scheme will be applicable to registered person, –

(i) whose aggregate turnover in the preceding financial year was fifty lakh rupees or below;

(ii) who is not eligible to pay tax under sub-section (1) of section 10 of the said Act; – Therefore, this notification will be applicable mainly to Service Providers with certain exceptions u/s 10(2).

(iii) who is not engaged in making any supply which is not leviable to tax under the said Act; – Supplying NON GST Item e.g. petrol, etc

(iv)who is not engaged in making any inter-State outward supply;

(v)who is neither a casual taxable person nor a non-resident taxable person;

(vi)who is not engaged in making any supply through an electronic commerce operator who is required to collect tax at source under section 52; and

(vii) who is not engaged in making supplies of the goods, the description of which is specified in the Table below,

2. Where more than one registered persons are having the same PAN, issued under the Income Tax Act, 1961(43 of 1961), tax on supplies by all such registered persons is paid at the rate of six percent.

Analysis: – Scheme will be applicable to all units of service provider having GST numbers based same PAN. This means service provider can’t keep any unit out of ambit of this scheme, if opted it for any one unit.

3.The registered person shall not collect any tax from the recipient on supplies made by him nor shall he be entitled to any credit of input tax.

Analysis: – Supplier can’t collect tax from buyer & NO ITC available, being composition scheme.

4. The registered person shall issue, instead of tax invoice, a bill of supply as referred to in clause (c) of sub-section (3) of section 31 of the said Act with particulars as prescribed in rule 49 of Central Goods and Services Tax Rules.

5. The registered person shall mention the following words at the top of the bill of supply, namely: – ‘taxable person paying tax in terms of notification No. 2/2019-Central Tax (Rate) dated 07.03.2019, not eligible to collect tax on supplies’.

6. The registered person opting to pay tax under this notification shall be liable to pay tax at the rate of six percent on all outward supplies specified in column (1) notwithstanding any other notification issued under sub-section (1) of section 9 or under section 11 of said Act.

Analysis: –

Section 9(1) – refers to all intra state supply of goods or service or both, except supply of alcoholic liquor.

Section 11 – refers to exempt supply, this means Tax is payable at 6% even on exempt supply.

7. The registered person opting to pay tax under this notification shall be liable to pay tax on inward supplies on which he is liable to pay tax under sub-section (3) or, as the case may be, under sub-section (4) of section 9 of said Act at the applicable rates.

Analysis: – RCM on inward supply related provisions u/s 9(3) & 9(4) will be applicable to those who are opting for this scheme.

B. In computing aggregate turnover in order to determine eligibility of a registered person to pay tax at the rate of six percent under this notification, value of supply of exempt services by way of extending deposits, loans or advances in so far as the consideration is represented by way of interest or discount, shall not be taken into account.

NOTE: Rate of six percent is mentioned herein by assuming corresponding notifications for this scheme will be issued by respective State / UT Govts.

Author Bio

composition scheme available for tours and travel business

Is Composition GSt Scheme is applicable for Multi Gym

Can a software firm(proprietorship), who wants to provide its software services outside its state(Uttarakhand), opt for composition scheme?

indly advise whether composite scheme is applicable for the Coaching Classes

“refers to exempt supply, this means Tax is payable at 6% even on exempt supply ”

If a client is nbfc and opted for composition levy will the 6 % to be charged on int income also ?

Can A Air TKT AGENT DEALS IN ONLY SERVICE CHARGS OPT COMPOSIT SCHEMES IN GST

If I have taken registration as a Regular Dealer. How can I opt the Presumptive Scheme under the Tax Rate@6% i.e.3% CGST & 3% SGST?

is Composition gst scheme applicable for tv serial production firms

While applying the GST registration for Composition scheme for Accounting services it’s not showing HSN code why??

kindly advice whether gst composite scheme is applicable to yoga academy (not a trust)

kindly advise whether composite scheme is applicable for the yoga academy (not a trust)