CBIC amend notification No. 12/2017- Central Tax (Rate) so as to implement recommendations made by GST Council in its 45th meeting held on 17.09.2021 related to Changes in CGST exemption on Supply of services WEF 01.10.2021 vide Notification No. 07/2021- Central Tax (Rate) | Dated: 30th September, 2021.

Exemptions in services

♦ S. No. 19A, 19B; Heading 9965- Services by way of transportation of goods by an aircraft/ vessel from customs station of clearance in India to a place outside India

- Nil GST Rate

- Existing exemption of Export Freight extended from Sept 2021 to Sept 2022

♦ S. No. 61A; Heading 9991- Services by way of granting National Permit to a goods carriage to operate through-out India / contiguous States

- Nil GST rate

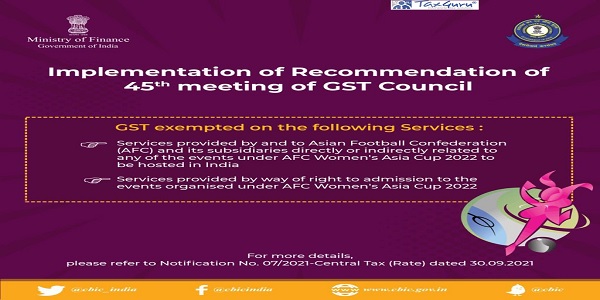

AFC Women’s Asia Cup 2022 to be hosted in India

♦ S. No. 9AB; Chapter 99 – Services provided by and to Asian Football Confederation (AFC) and its subsidiaries directly or indirectly related to any of the events under AFC Women’s Asia Cup 2022 to be hosted in India.

- Nil GST Rate

- Subject to Certification by Director (Sports), Ministry of Youth Affairs and Sports

♦ S. No. 82B, Heading 9996- Services by way of right to admission to the events organised under AFC Women’s Asia Cup 2022

- Nil GST Rate

Services provided by way of granting National Permit to a goods carriage to operate throughout India/contiguous States exempted from GST.

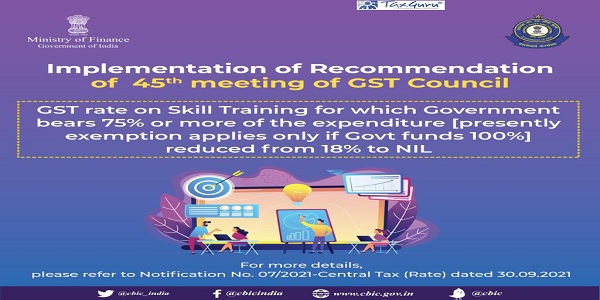

GST rate on Skill Training for which Government bears 75% or more of the expenditure reduced from 18% to NIL.

GST exemption with reference to services provided by and to Asian Football Confederation for events under AFC Women’s Asia Cup 2022 to be held in India

Government of India

Ministry of Finance

(Department of Revenue)

Notification No. 07/2021- Central Tax (Rate)

New Delhi, the 30th September, 2021

G.S.R.687(E) – In exercise of the powers conferred by sub-sections (3) and (4) of section 9, sub-section (1) of section 11, sub-section (5) of section 15 and section 148 of the Central Goods and Services Tax Act, 2017 (12 of 2017), the Central Government, on being satisfied that it is necessary in the public interest so to do, on the recommendations of the Council, hereby makes the following further amendments in the notification of the Government of India, in the Ministry of Finance (Department of Revenue), No. 12/2017- Central Tax (Rate), dated the 28th June, 2017, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 691(E), dated the 28th June, 2017, namely:—

In the said notification, in the Table, –

(i) against serial number 1, in column (3), after the figures and letters “12AA”, the word, figures and letters ” or 12AB” shall be inserted;

(ii) against serial number 9AA, in column (3), after the words “hosted in India”, the words “whenever rescheduled” shall be inserted;

(iii) after serial number 9AA and the entries relating thereto, the following shall be inserted, namely : –

| (1) | (2) | (3) | (4) (5) | |

| “9AB | Chapter 99 | Services provided by and to Asian

Football Confederation (AFC) and its subsidiaries directly or indirectly related to any of the events under AFC Women’s Asia Cup 2022 to be hosted in India |

Nil | Provided that Director (Sports), Ministry of Youth Affairs and Sports certifies that the services are directly or indirectly related to any of the events under AFC Women’s Asia Cup 2022.”; |

(iv) against serial numbers 9D and 13, in column (3), after the figures and letters “12AA”, the word, figures and letters ” or 12AB” shall be inserted;

(v) against serial numbers 19A and 19B, in column (5), for the figures “2021”, the figures “2022” shall be substituted;

(vi) serial number 43 and the entries relating thereto shall be omitted;

(vii) after serial number 61 and the entries relating thereto, the following shall be inserted, namely:-

| (1) | (2) | (3) | (4) | (5) |

| “61A | Heading 9991 | Services by way of granting National Permit to a goods carriage to operate through-out India / contiguous States. | Nil | Nil”; |

(viii) against serial number 72, in column (3), after the words “for which”, the figures, symbol and words “75% or more of the” shall be inserted;

(ix) against serial numbers 74A and 80, in column (3), after the figures and letters “12AA”, word, figures and letters ” or 12AB” shall be inserted;

(x) after serial number 82A and the entries relating thereto, the following shall be inserted, namely : –

| (1) | (2) | (3) | (4) | (5) |

| “82B | Heading 9996 | Services by way of right to admission to the events organised under AFC Women’s Asia Cup 2022 | Nil | Nil”; |

2. This notification shall come into force with effect from the 1st day of October, 2021.

[F. No. 354/207/2021-TRU]

(Rajeev Ranjan)

Under Secretary to the Government of India

Note: The principal notification No. 12/2017 – Central Tax (Rate), dated the 28th June, 2017 was published in the Gazette of India, Extraordinary, vide number G.S.R. 691 (E), dated the 28th June, 2017 and was last amended by notification No. 05/2020 – Central Tax (Rate), dated the 16th October, 2020, published vide number G.S.R. 643(E), dated the 16th October, 2020.