A short study called “Implementation of Value Added Tax (VAT) in India-Lessons for transition to GST” was released by the Comptroller & Auditor General (C&AG) of India in June, 2010 which had surveyed several VAT dealers across the country after implementation of VAT Model Act in Sales Tax and found out that several cases of profiteering by dealers by not passing on the benefit of tax rate reduction due to VAT. Hence when the new Goods and Services Tax Regime was sought to be implemented on 1st July, 2017 (referred to as the ‘Appointed Day’) Anti-Porfiteering Measure in the form of Section 171 was included which stated that

“the suppliers of goods and services should pass on the benefit of any reduction in the rate of tax or the benefit of input tax credit to the recipients by way of commensurate reduction in prices. The wilful action of not passing on the above benefits to the recipients in the manner prescribed is known as “profiteering”

Here, both in cases of reduction of tax burden and benefit of increase of input tax credit (ITC) was sought to be passed onto the consumer. In an Indirect Tax Regime it is the consumer who endures the burden of the tax and hence he had to be protected from the profiteering measures which could be levied on by an service provider or goods seller in the transitory phase when the act was being implemented. In the long term , a competitive market with enough players were expected to balance the scales automatically on the principles of a perfect elastic supply and demand.

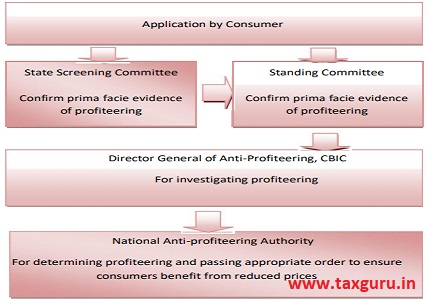

As an Institution Set-up, the National Anti-Profiterring Authority (NAPA) was setup in the Delhi with a Chairman and three other members. There are State Committees which are required to receive consumer complaints and perform a prima-facie investigation. An aggrieved Consumer may file an application, in the prescribed format, before State Standing Committee on Anti-profiteering if the profiteering has all-India character OR before the State Screening Committees if the profiteering is of local nature. Then the same is forwarded to Director General of Anti-Profiteering, Central Board of Indirect Taxes and Customs (CBIC) which does a complete investigation in three months times and forwards the report to NAPA for adjudication.

-Work Flow of an Anti-Profiteering Complain in GST

Initially, the body was introduced for two years but the same has been extended for two more years. Till date, the body has passed 137 orders most of which have found the suppliers guilty of profiteering. There is no appeal provision in the Act but various parties in cases of larger amounts have been preferred Writ Applications in High Courts and generally stay on the order has been granted. In some cases, the appeals have been found to be in favour of the party.

The main issue remains that in a complex business environment where there are hardly any monopolies it is difficult to prove theoretically that the cost structure of the company had remained the same pre and post the rate change or the ITC changes .The Principles of Economics state that in a Perfectly Competitive Market or even an Oligopoly there is an Elastic Relationship between Supply and Demand and hence Profiteering would not be possible. Also, the very question remains the Unit Level at which any profiteering question has to be determined . The NAPA authority has always held that it must be a singular customer and a singular distinctive product that it can determine as he is the one who has been profiteered from. The companies on the other hand have contended that as their business have inter-connected supply chains it would not be possible to determine singular costs. The complex debate of Profiteering and Profits is likely to continue for a few more years to come.

Author Bio

Greetings!

Sir, Please provide us the post regarding issues and discussion on Anti-Profiteering orders