Understand the implications of GST registration cancellation without determining payable amounts by the assessee. Learn from the Gujarat High Court’s ruling.

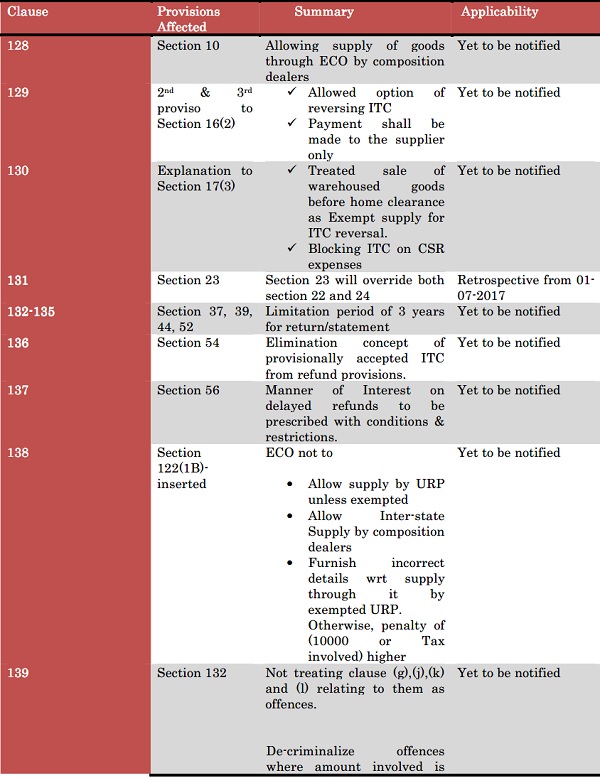

Finance Bill, 2023 presented on 1st of February, 2023 by honourable FM Smt. Nirmala Sitharaman Ji has introduced changes relating to Goods & Services Tax vide Clauses 128-144. Clause 128 to 142 are related to CGST and Clause 143 to 144 are related to IGST.

Clause 128

Proposed Changes

(a) In Section 10(2)(d), the words “goods or” shall be omitted;

(b) In Section 10(2A)(c), the words “goods or” shall be omitted.

Implication

Earlier, the benefit of composition scheme was not available to those who are engaged in supplying goods or services through E-commerce operator. However, after the amendment, the benefit of composition scheme has been extended to Supply of goods through E-commerce operator.

Amended Provision

Section 10(2): The registered person shall be eligible to opt under section 10(1), if-

(d) He is not engaged in making any supply of goods or services through an E-commerce operator who is required to collect tax at source under section 52.

Section 10(2A): Notwithstanding anything to the contrary contained in this Act, but subject to the provisions of sub-sections (3) and (4) of section 9, a registered person, not eligible to opt to pay tax under sub-section (1) and sub-section (2), whose aggregate turnover in the preceding financial year did not exceed fifty lakh rupees, may opt to pay, in lieu of the tax payable by him under sub-section (1) of section 9, an amount of tax calculated at such rate as may be prescribed, but not exceeding three per cent. of the turnover in State or turnover in Union territory, if he is not-

(c) Engaged in making any supply of goods or services through an electronic commerce operator who is required to collect tax at source under section 52.

When E-commerce operator is required to collect TCS u/s 52:

52(1) Read With Explanation

Notwithstanding anything to the contrary contained in this Act, every electronic commerce operator (hereafter in this section referred to as the “operator”), not being an agent, shall collect an amount calculated at such rate not exceeding one per cent., as may be notified by the Government on the recommendations of the Council, of the net value of taxable supplies made through it by other suppliers where the consideration with respect to such supplies is to be collected by the operator.

Explanation- For the purposes of this sub-section, the expression “net value of taxable supplies” shall mean the aggregate value of taxable supplies of goods or services or both, other than services notified under sub-section (5) of section 9, made during any month by all registered persons through the operator reduced by the aggregate value of taxable supplies returned to the suppliers during the said month.

Thus, where ECO collect consideration [except on transactions covered under section 9(5)], it shall be liable to collect TCS as well.

Our Comments:

The restriction is on composition dealers from supplying goods or services through ECO which is liable to collect TCS implying that goods or services can be supplied by them through ECO where it is not collecting the consideration for the supplies affected through it.

Clause 129

Proposed Changes

(i) In second proviso to section 16(2), for the words “added to his output tax liability, along with interest thereon”, the words and figures “paid by him along with interest payable under section 50” shall be substituted.

(ii) In the third proviso to section 16(2), after the words “made by him”, the words “to the supplier” shall be inserted.

Existing Provision

Second Proviso to Section 16(2)

Provided further that where a recipient fails to pay to the supplier of goods or services or both, other than the supplies on which tax is payable on reverse charge basis, the amount towards the value of supply along with tax payable thereon within a period of one hundred and eighty days from the date of issue of invoice by the supplier, an amount equal to the input tax credit availed by the recipient shall be added to his output tax liability, along with interest thereon, in such manner as may be prescribed.

Third Proviso to Section 16(2)

Provided also that the recipient shall be entitled to avail of the credit of input tax on payment made by him of the amount towards the value of supply of goods or services or both along with tax payable thereon.

Amended Provision

Second Proviso to Section 16(2)

Provided further that where a recipient fails to pay to the supplier of goods or services or both, other than the supplies on which tax is payable on reverse charge basis, the amount towards the value of supply along with tax payable thereon within a period of one hundred and eighty days from the date of issue of invoice by the supplier, an amount equal to the input tax credit availed by the recipient shall be paid by him along with interest payable under section 50, in such manner as may be prescribed.

Third Proviso to Section 16(2)

Provided also that the recipient shall be entitled to avail of the credit of input tax on payment made by him to the supplier of the amount towards the value of supply of goods or services or both along with tax payable thereon.

Rule 37 draws power from Second proviso to Section 16(2) which has been amended w.e.f 1st of October, 2022 vide NN 19/2022 dated 28.09.2022 and NN 26/2022 dated 26.12.2022 (retrospective amendment)

Changes made vide NN 19/2022:

> Amended 37(1)

> Amended 37(2)

> Omitted 37(3)

Changes made vide NN 26/2022:

> Amended 37(1) retrospectively from 01.10.2022

Amended Rule 37 after 01.10.2022 – Reversal of input tax credit in the case of non-payment of consideration

37(1) A registered person, who has availed of input tax credit on any inward supply of goods or services or both, other than the supplies on which tax is payable on reverse charge basis, but fails to pay to the supplier thereof, the amount towards the value of such supply [whether wholly or partly,] along with the tax payable thereon, within the time limit specified in the second proviso to sub-section(2) of section 16, shall pay [or reverse] an amount equal to the input tax credit availed in respect of such supply [, proportionate to the amount not paid to the supplier,] along with interest payable thereon under section 50, while furnishing the return in FORM GSTR-3B for the tax period immediately following the period of one hundred and eighty days from the date of the issue of the invoice.

Provided that the value of supplies made without consideration as specified in Schedule I of the said Act shall be deemed to have been paid for the purposes of the second proviso to sub-section (2) of section 16

Provided further that the value of supplies on account of any amount added in accordance with the provisions of clause (b) of sub-section (2) of section 15 shall be deemed to have been paid for the purposes of the second proviso to sub-section (2) of section 16.

37(2) Where the said registered person subsequently makes the payment of the amount towards the value of such supply along with tax payable thereon to the supplier thereof, he shall be entitled to re-avail the input tax credit referred to in sub-rule (1).

| Rule | Provision before 01.10.2022 | Provision after 01.10.2022 | Impact |

| 37(1) | Need to furnish following details in Form GSTR-2:

> Details of inward supply where ITC has been availed but payment is not made to supplier within 180 days > Amount not paid > ITC availed with respect to |

ITC availed wrt unpaid value(wholly/partly) needs to be reversed/added to output tax liability |

As GSTR 2 has not been made applicable at all, Rule 37(1) was rightly amended.ITC reversal option has also been provided whereas earlier the taxpayer has to add the ITC wrt unpaid value to his output liability.RCM exclusion has been included in 37(1) to made it at par with 2nd proviso to section 16(2)Earlier, ITC was not allowable till entire payment is made to the supplier. However, ITC wrt partial payment can be claimed now. |

| 37(2) | Amount of ITC with respect to unpaid value shall be added to output tax liability of the registered person for the month in which details are furnished in GSTR-2 | ITC reversed/added to output tax liability under 37(1) can be availed subsequently when payment is made to the supplier. | To align the rule with 3rd proviso to section 16(2). However, 3rd proviso does not specifically talk about payment to the supplier. |

| 37(3) | Interest needs to be paid u/s 50(1) for the period starting from the date of availing credit on such supplies till the date when the amount in 37(2) is added to the output tax liability. | Omitted | Rule 37 now does not provide for manner of interest calculation directly but in 37(1), it talks about interest calculation as per Section 50. For interest u/s 50, Rule 88B prescribes the manner for the same. |

To align 2nd proviso to section 16(2) with Rule 37(1), Clause 129(i) has allowed for reversal of credit availed for unpaid amount to the supplier along with the option of adding it to output tax liability.

To align 3rd proviso to section 16(2) with Rule 37(2), Clause 129(ii) has specifically mentioned payment to the supplier.

However, where payment is made to any person other than the supplier, then ITC may not be allowed to be re-availed.

As the amendment in the act is yet to be notified, So where rule was amendment even before the principal act, the applicability of the rule for the period of non-uniformity between the act and the rule can be challenged as the rules cannot override the act.

Manner of Interest Calculation after 01.10.2022:

Rule 88B inserted vide NN 14/2022 dated 05.07.2022 with retrospective effect from 01.07.2017

(1) In case, where the supplies made during a tax period are declared by the registered person in the return for the said period and the said return is furnished after the due date in accordance with provisions of section 39, except where such return is furnished after commencement of any proceedings under section 73 or section 74 in respect of the said period, the interest on tax payable in respect of such supplies shall be calculated on the portion of tax which is paid by debiting the electronic cash ledger, for the period of delay in filing the said return beyond the due date, at such rate as may be notified under sub-section (1) of section 50.

(2) In all other cases, where interest is payable in accordance with sub section (1) of section 50, the interest shall be calculated on the amount of tax which remains unpaid, for the period starting from the date on which such tax was due to be paid till the date such tax is paid, at such rate as may be notified under sub-section (1) of section 50.

(3) In case, where interest is payable on the amount of input tax credit wrongly availed and utilised in accordance with sub-section (3) of section 50, the interest shall be calculated on the amount of input tax credit wrongly availed and utilised, for the period starting from the date of utilisation of such wrongly availed input tax credit till the date of reversal of such credit or payment of tax in respect of such amount, at such rate as may be notified under said subsection (3) of section 50.

Explanation —For the purposes of this sub-rule, —

(1) Input tax credit wrongly availed shall be construed to have been utilised, when the balance in the electronic credit ledger falls below the amount of input tax credit wrongly availed, and the extent of such utilisation of input tax credit shall be the amount by which the balance in the electronic credit ledger falls below the amount of input tax credit wrongly availed.

(2) The date of utilisation of such input tax credit shall be taken to be, —

(a) The date, on which the return is due to be furnished under section 39 or the actual date of filing of the said return, whichever is earlier, if the balance in the electronic credit ledger falls below the amount of input tax credit wrongly availed, on account of payment of tax through the said return; or

(b) The date of debit in the electronic credit ledger when the balance in the electronic credit ledger falls below the amount of input tax credit wrongly availed, in all other cases.

| Particulars | 88B(1) | 88B(2) | 88B(3) |

| Situation Covered | GSTR 3B filed after due date except where such return is filed after commencement of 73/74 |

Previous Period Tax Payment in Current period GSTR 3B.

Covers only those cases which are covered in Section 50(1) except already covered in |

ITC wrongly availed & Utilised as per section 50(3) |

| Calculation | Interest shall be calculated only on Net Tax Liability (i.e. payment made using E-cash Ledger) |

Interest shall be paid on Gross Tax Liability | Interest shall be calculated only on ITC utilised. |

| From | Due date of 3B | Due date of Tax Payment | Date of ITC utilisation |

| To | Actual date of 3B | Actual date of Payment | Date of reversal/Tax payment wrt utilised ITC |

| Applicability for interest on ITC availed but payment to supplier not made | Not applicable as covers only GSTR 3B late filing cases | Triggering point is Tax payment after due date Due date for Tax payment as per Rule 37 will be the 3B immediately after completion of 180 days.

Our Comments: As 88B(3) specifically |

Triggering point is wrong utilisation of ITC It shall apply as it is the most appropriate.

Our Comments: However if ITC has not been |

Section 50(1): Every person who is liable to pay tax in accordance with the provisions of this Act or the rules made thereunder, but fails to pay the tax or any part thereof to the Government within the period prescribed, shall for the period for which the tax or any part thereof remains unpaid, pay, on his own, interest at such rate, not exceeding eighteen per cent., as may be notified by the Government on the recommendations of the Council.

Section 50(3): Where the input tax credit has been wrongly availed and utilised, the registered person shall pay interest on such input tax credit wrongly availed and utilised, at such rate not exceeding twenty-four per cent. as may be notified by the Government, on the recommendations of the Council, and the interest shall be calculated, in such manner as may be prescribed.

Clause 130 read with Clause 142

A] In explanation to section 17(3) , for the words and figure “except those specified in paragraph 5 of the said Schedule”, the following shall be substituted, “except-

(i) The value of activities or transactions specified in paragraph 5 of the said Schedule; and

(ii) The value of such activities or transactions as may be prescribed in respect of clause (a) of paragraph 8 of the said Schedule”.

Existing Provision

Section 17(3) read with explanation

The value of exempt supply under sub-section (2) shall be such as may be prescribed, and shall include supplies on which the recipient is liable to pay tax on reverse charge basis, transactions in securities, sale of land and, subject to clause (b) of paragraph 5 of Schedule II, sale of building. Explanation: For the purposes of this sub-section, the expression “value of exempt supply” shall not include the value of activities or transactions specified in Schedule III, except those specified in paragraph 5 of the said Schedule.

Amended Provision

Section 17(3) read with explanation

The value of exempt supply under sub-section (2) shall be such as may be prescribed, and shall include supplies on which the recipient is liable to pay tax on reverse charge basis, transactions in securities, sale of land and, subject to clause (b) of paragraph 5 of Schedule II, sale of building. Explanation: For the purposes of this sub-section, the expression “value of exempt supply” shall not include the value of activities or transactions specified in Schedule III, except-

(i) The value of activities or transactions specified in paragraph 5 of the said Schedule; and

(ii) The value of such activities or transactions as may be prescribed in respect of clause (a) of paragraph 8 of the said Schedule.

Background

As per section 17(2) of CGSTA,2017- Where the registered person uses goods or services or both for both taxable supplies (including Zero rated supplies) and exempt supplies, the input tax credit shall be restricted to such portion which is attributable to taxable supplies (including zero rated supply).

Exempt supply for this purpose means:

1. Exempt supply as per section 2(47) of CGSTA, 2017

2. Those defined in Section 17(3) read with explanation i.e.

- Outward supplies under RCM.

- Transactions in securities (Recently, department is issuing notices to companies for IPO expenses as well by considering them as ‘transaction in securities’ whereas in our view, said expenses are incurred before securities(shares) origination and thus said expenses needs to be classified as “transaction for securities”.

- Sale of land.

- Sale of building where the same is not covered under clause b of paragraph 5 of schedule II i.e. which are specified in paragraph 5 of schedule III.

- Supply of warehoused goods to any person before clearance for home consumption as specified in paragraph 8(a) of schedule III.

Our Comments:

The mere inclusion of paragraph 8(a) in the exempt supply for calculation of ITC reversal under rule 42 & 43 by excluding paragraph 7 & 8(b) are not justifiable.

B] After section 17(5)(f), the following clause shall be inserted, namely:

Section 17(5)(fa)

Goods or services or both received by a taxable person, which are used or intended to be used for activities relating to his obligations under corporate social responsibility referred to in section 135 of the Companies Act, 2013.

Impact

There were several contradictory jurisprudences in relation to CSR activities. Several advance rulings in GST also allowed the credit on such activities pursuant to which the companies were claiming ITC on goods or services used or intended to be used for CSR activities by considering that the said activities are undertaken in the course or furtherance of the business.

As it is a prospective amendment, so the companies can claim ITC with respect to CSR activities till the amendment is notified.

Our Comments

Due to ineligibility of ITC, the companies will start booking the ITC as a part of CSR expense as the same cannot be booked as a recoverable asset after the amendment. As a consequence of which, companies will be able to treat tax paid to the government as CSR spent.

The purpose of CSR is to bind the companies to spent at least 2% of their average profits of preceding 3 years towards the welfare of general public over and above their obligation to pay taxes to the government ( direct and indirect taxes) which is then spent for welfare of people by the government.

Thus after this amendment, the amount not directly spent for welfare of society by companies but given to Govt. as taxes (indirect welfare of society) will also form part of CSR spent.

Clause 142

142(1) Retrospective amendment w.e.f 01/07/2017 has been made in paragraph 7, 8, and explanation 2 thereof, of the schedule III.

explanation 2 thereof, of the schedule III.

Para 7 Supply of goods from a place in the non-taxable territory to another place in the non–taxable territory without such goods entering into India.

Para 8(a) Supply of warehoused goods to any person before clearance for home consumption

Para 8(b) Supply of goods by the consignee to any other person, by endorsement of documents of title to the goods, after the goods have been dispatched from the port of origin located outside India but before clearance for home consumption.

Explanation 2 For the purposes of paragraph 8, the expression “warehoused goods” shall have the same meaning as assigned to it in the Customs Act, 1962.

Para 7, 8(a), 8(b) and explanation 2 were inserted vide CGST (Amendment) Act, 2018 w.e.f 01st February, 2019

Before insertion of above specified transactions in schedule III, GST was levied on above specified transactions, but from 01st Feb, 2019, these transactions were covered under schedule III making them neither the supply of goods nor the supply of services.

The retrospective amendment in schedule III from 01st July, 2017 would lead to refund of tax which has already been paid on above transactions. However vide clause 142(2) , it has been provided that no refund shall be made of all the tax which has been collected before 01st Feb, 2019.

Our Comments:

The restriction for claiming refund is not justified as the genuine taxpayers who have abide the law and paid the taxes is denied refund of the same. Due to which, genuine taxpayers will suffer loss compared to those who does not follow the law.

As per Article 265 of our constitution, tax can be levied or collected only with the authority of law and thus where a retrospective amendment is made in the act to give exemption, the authority to levy or collect law ceases with retrospective effect and thus the denial by the government to refund the tax and retain the same violates the doctrine of unjust enrichment.

Clause 131

Retrospective amendment w.e.f 01/07/2017 has been made in section 23, namely-

Notwithstanding anything to the contrary contained in sub-section (1) of section 22 or section 24 ,

(a) The following persons shall not be liable to registration, namely:––

(i) Any person engaged exclusively in the business of supplying goods or services or both that are not liable to tax or wholly exempt from tax under this Act or under the Integrated Goods and Services Tax Act, 2017;

(ii) An agriculturist, to the extent of supply of produce out of cultivation of land;

(b) The Government may, on the recommendations of the Council, by notification, subject to such conditions and restrictions as may be specified therein, specify the category of persons who may be exempted from obtaining registration under this Act.

Existing Provision Section 23

(1) The following persons shall not be liable to registration, namely:-

(a) Any person engaged exclusively in the business of supplying goods or services or both that are not liable to tax or wholly exempt from tax under this Act or under the Integrated Goods and Services Tax Act;

(b) An agriculturist, to the extent of supply of produce out of cultivation of land.

(2) The Government may, on the recommendations of the Council, by notification, specify the category of persons who may be exempted from obtaining registration under this Act.

Pursuant to section 23(2), NN 05/2017 dated 19-06-2017 has been issued to exempt the persons who are only engaged in providing outward supplies on which tax is payable on RCM basis.

Meaning of agriculturist as per section 2(7) of CGSTA, 2017

“Agriculturist” means an individual or a Hindu Undivided Family who undertakes cultivation of land-

(a) By own labour, or

(b) By the labour of family, or

(c) By servants on wages payable in cash or kind or by hired labour under personal supervision or the personal supervision of any member of the family.

Impact

Earlier, it is interpreted that

- Section 23 overrides section 22(1).

- Section 24 overrides section 23.

Thus, where a person is engaged exclusively in the business of exempt supplies satisfies any clause of section 24, he is required to obtain compulsory registration.

E.g. If he receives any inward RCM supply, then requirement to obtain compulsory registration gets triggered. However, after the above amendment, it is clear that

- Section 23 overrides both section 22(1) and section 24.

Thus, the ambiguity due to conflicting provisions has been removed by inserting a Non -obstante clause in section 23.

Our Comments

There may be some cases where persons making exclusively exempt supplies have obtained registration due to applicability of section 24 of CGSTA, 2017.

As, the amendment in section 23 has been made with retrospective effect, it is advised to such persons to apply for cancellation of their registration under section 29(1)(C).

Section 29(1)(C) deals with the cases of application for cancellation of registration by registered person if they are no longer liable to be registered under section 22 or 24.

Loss to Govt. due to above amendment

Suppose a hospital providing only exempt healthcare services receives legal services from a

lawyer. Value of service is Rs 10,00,000.

Aggregate Turnover of the hospital during preceding Financial year was Rs 5,00,00,000

NN 12/2017 provides that legal services provided to a business entity having turnover in preceding FY <=40L/20L/10L, then the legal services are exempt.

As the turnover of hospital is >20L/10L, legal services are not exempt under NN 12/2017

NN 13/2017 provides that where legal services shall be taxable under RCM where these services are provided to a business entity having turnover in preceding FY >40L/20L/10L.

Position before the amendment vide Clause 131

Hospital will apply for registration due to applicability of section 24 as it overrides section 23. And will discharge tax liability of Rs 180000 (10Lakh*18%) under RCM. However, it will not be eligible to claim ITC on the same as it is not providing any taxable service.

Position after the amendment vide Clause 131

Hospital need not to apply for registration as section 23 overrides section 24. Also, lawyer is not liable for registration due to NN 05/2017. So, government will lose Rs 1,80,000.

So, we can expect related amendment in either NN 13/2017(to remove such scenario from RCM) or NN 05/2017(to not allow registration exemption if services are provided to persons providing exclusively exempt supplies).

Also, the refund scenario will come into picture as the amendment is made in section 23 from retrospective effect.

Clause 132 ,133,134 & 135

New sub-sections have been inserted to restrict the filing of following returns/statements after the expiry of 3YEARS from its due date:

- GSTR 1 [ section 37(5)1

- GSTR 3B [section 39(11)1

- GSTR 9/9A [section 44(2)1

- Statement under section 52 by ECO [section 52(15)1

Provided that the Government may, on the recommendations of the Council, by notification, subject to such conditions and restrictions as may be specified therein, allow the filing of above return/statement even after the expiry of the said period of three years from the due date of furnishing the said return/statement.

Impact

At present, there is no limitation period for filing. However, certain consequences are still present which are as follows:

i) Late fees u/s 47 for late filing of

- GSTR 1

- GSTR 3B

- GSTR 9/9A and 9C

- Statement under section 52 by ECO (GSTR 8)

Maximum late fees for GSTR 1/3B and section 52 return is Rs 5,000.

However, maximum late fees for Annual return u/s 44 can be upto .25% of the Turnover in the state/UT.

ii) Subsequent Period GSTR1/3B cannot be filed unless previous period GSTR1 and GSTR 3B are filed

After the amendment restricting the filing of returns upto 3 years, it can be said that subsequent period returns can be filed once the limitation period is expired. Needless, to say that interest will continue to apply on outward supplies belonging to that period from the due date of 3B till the actual payment of tax.

iii) Cancellation of registration of

–Composition dealer where he fails to file CMP-08 for 3 consecutive tax periods.

-Normal taxpayer where he fails to file return for 6 continuous months.

iv) Restriction on furnishing of information in PART A of FORM GST EWB -01

-Composition dealer where he fails to file CMP-08 for 2 consecutive tax periods.

-Normal taxpayer where he fails to file return for 2 consecutive months.

Our Comments

As the registration is liable for cancellation after failure to file returns (u/s 39) for 3 consecutive tax periods/ 6 consecutive months, it is difficult to understand why the limitation period of 3 Years has been specified via the amendment in section 39.

Clause 136

In section 54(6), the words “excluding the amount of input tax credit provisionally accepted,” shall be omitted.

Existing Provision

Notwithstanding anything contained in sub-section (5), the proper officer may, in the case of any claim for refund on account of zero-rated supply of goods or services or both made by registered persons, other than such category of registered persons as may be notified by the Government on the recommendations of the Council, refund on a provisional basis, ninety per cent of the total amount so claimed, excluding the amount of input tax credit provisionally accepted, in such manner and subject to such conditions, limitations and safeguards as may be prescribed and thereafter make an order under sub-section (5) for final settlement of the refund claim after due verification of documents furnished by the applicant.

Amended Provision

Notwithstanding anything contained in sub-section (5), the proper officer may, in the case of any claim for refund on account of zero-rated supply of goods or services or both made by registered persons, other than such category of registered persons as may be notified by the Government on the recommendations of the Council, refund on a provisional basis, ninety per cent of the total amount so claimed, in such manner and subject to such conditions, limitations and safeguards as may be prescribed and thereafter make an order under sub-section (5) for final settlement of the refund claim after due verification of documents furnished by the applicant.

Background

Section 41 of CGSTA, 2017 has been amended by Finance Act, 2022 vide NN 18-2022 w.e.f

01/10/2022-

Amended provision of section 41

Every registered person shall, subject to such conditions and restrictions as may be prescribed, be entitled to take the credit of eligible input tax, as self-assessed, in his return and such amount shall be credited on a provisional basis to his electronic credit ledger.

Thus, now self-assessment tax gets directly credited to E-credit ledger and the same is treated as Final ITC and not provisional ITC.

Our Comments

Section 54(6) allows provisional refund of 90% on zero rated supplies by excluding ITC provisional accepted. As, the concept of provisional acceptance of ITC has been omitted by Finance Act, 2022 w.e.f 01-10-2022, there is no need to make such reference in section 54(6).

Clause 137

Amendment in Section 56- Interest on delayed refunds

-Manner of computation along with conditions and restrictions may be prescribed

Existing Provision

If any tax ordered to be refunded under sub-section (5) of section 54 to any applicant is not refunded within sixty days from the date of receipt of application under sub-section (1) of that section, interest at such rate not exceeding six per cent. as may be specified in the notification issued by the Government on the recommendations of the Council shall be payable in respect of such refund from the date immediately after the expiry of sixty days from the date of receipt of application under the said sub-section till the date of refund of such tax.

Amended Provision

If any tax ordered to be refunded under sub-section (5) of section 54 to any applicant is not refunded within sixty days from the date of receipt of application under sub-section (1) of that section, interest at such rate not exceeding six per cent. as may be specified in the notification issued by the Government on the recommendations of the Council shall be payable in respect of such refund from the date immediately after the expiry of sixty days from the date of receipt of such application till the date of refund of such tax tax, to be computed in such manner and subject to such conditions and restrictions as may be prescribed”

Our Comments

The amendment has empowered the government to prescribe the manner of computation of interest on delayed refunds and such interest shall be granted subject to certain conditions and restrictions.

Such conditions and restrictions can be linked to regular filing of returns i.e. If the taxpayer is filing returns for regular period, only then he will be allowed the interest on delayed refunds.

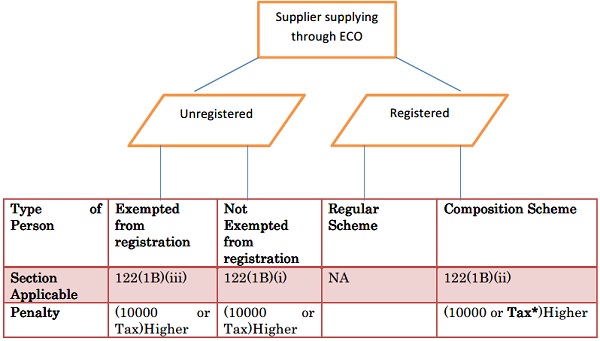

Clause 138

Insertion of section 122(1B)

Any electronic commerce operator who––

(i) Allows a supply of goods or services or both through it by an unregistered person other than a person exempted from registration by a notification issued under this Act to make such supply;

(ii) Allows an inter-State supply of goods or services or both through it by a person who is not eligible to make such inter-State supply; or

(iii) Fails to furnish the correct details in the statement to be furnished under sub-section (4) of section 52 of any outward supply of goods effected through it by a person exempted from obtaining registration under this Act.

Then ECO shall be liable to pay a penalty of ten thousand rupees, or an amount equivalent to the amount of tax involved had such supply been made by a registered person other than a person paying tax under section 10, whichever is higher.

Keywords

√ URP= Unregistered Person

√ Exempted URP= Unregistered Person exempted from obtaining registration

√ ECO= E-commerce operator.

Tax*- Where ECO is allowing inter-state supply of goods by composition dealer, the tax has to be calculated as if tax has to be paid by normal dealer i.e a t the tax rate applicable to goods/services supplied.

However, one can argue that composition dealer will pay tax on such inter-state supply itself at rates specified in section 10 and the tax calculation part of the penalty provided u/s 122(1B) specifically excludes composition dealers and thus Rs10000 will be the penalty on ECO.

Our comments

As and when composition dealer will make inter-state supply through ECO, it will be automatically out from composition scheme and thus ECO shall pay penalty equal to Rs 10000 or tax on such supply considering the tax rates of goods/services and not the section 10 rates. And, Supplier shall also pay tax on such supply himself at the tax rates for those goods/services due to ineligibility of Section 10.

Understanding 122(1B)(i)

ECO shall be liable to pay penalty if it allows a supply of goods or services or both through it by an unregistered person other than a person exempted from obtaining registration by a notification issued under this Act to make such supply.

- Supply (whether inter/intra state, taxable/exempt) by unregistered person(URP)- Not allowed

- Supply (whether inter/intra, taxable/exempt) by URP exempted from registration vide notification- Allowed

- Pursuant to section 23(2), NN 05/2017 dated 19-06-2017 has been issued to exempt the persons from registration who are only engaged in providing outward supplies on which tax is payable on RCM basis.

Possible Interpretations:

Exempted from obtaining registration– Section23 + NN05/2017

Exempted from obtaining registration by a notification– NN05/2017

Exempted from obtaining registration by a notification to make such supply– Notification may come in the future specifying the category of persons who can supply goods/services through ECO without registration.

Our View:

The reference about notification in 122(1B)(i) talks about the notification which allows unregistered persons to make supply of goods/services through ECO.

As, the clause exclude those URP who are exempted from registration vide notification which allow them to make such supply. So, it can be said that the notification will come when this provision will be made applicable notifying the category of persons allowed to make supply through ECO even without registration and may include the persons exempted from registration under section 23 and NN 05/2017.

Impact

Question: Whether in current law, unregistered persons can supply goods through ECO?

Answer: Based on Our View

a) If ECO is collecting TCS- No, due to section 24 However, ECO were allowing such persons to supply goods/services even without checking whether suppliers have obtained registration or not.

After this amendment, this loophole or we can say tax evasion, will be plugged in by the government by levying a penalty on the ECO.

Exception: Persons covered under Section 23 + NN05/2017 are not liable to register after amendment vide Clause 131

b) If ECO is covered under 9(5)- Yes, persons liable for registration on crossing specified limit of turnover

Notification (expected to be issued in this regard) may allow ECOs to supply goods/services for these URP if their turnover is below the threshold limit and make it compulsory for ECOs to conduct due-diligence of the persons supplying goods/services through it.

However, if notification does not cover such scenarios, then ECO will have to pay penalty after allowing such supply (penalty will be on every supply effected) through it, implying that even though the turnover is less than threshold limit, URPs need to get registration if they want to make supply through ECO.

c) If ECO is not collecting TCS and also not covered under 9(5)- Yes, persons liable for registration on crossing specified limit of turnover

Notification (expected to be issued in this regard) may allow ECOs to supply goods/services for these URP if their turnover is below the threshold limit and make it compulsory for ECOs to conduct due-diligence of the persons supplying goods/services through it.

However, if notification does not cover such scenarios, then ECO will have to pay penalty after allowing such supply (penalty will be on every supply effected) through it, implying that even though the turnover is less than threshold limit, URPs need to get registration if they want to make supply through ECO.

Our Comments

Thus, earlier section 24 requires compulsory registration only when supplying good/services through ECO which is liable to collect TCS. However, considering the provisions of section 122(1B)(i), it seems that mandatory registration is envisaged, indirectly, for supplying goods/services through ECO even if it is not liable to collect TCS as the ECO will not on-board such suppliers without registration.

|

TYPES OF ECO

|

A] Covered under 9(5) | B] Not Covered under 9(5) and collecting consideration i.e ECO is liable to collect TCS | C] Not Covered under 9(5) and not collecting consideration i.e ECO isn’t liable to collect TCS |

| Liability to collect TCS u/s 52 | No

Excluded vide Explanation to section 52 |

Yes | No |

| Liability to pay taxes | ECO liable to pay taxes for the supplies effected through it | Supplier liable to pay taxes for the supplies effected through ECO | Supplier liable to pay taxes for the supplies effected through ECO |

| Invoice | ECO shall raise invoice to the recipient for supplies effected through it | Supplies shall raise invoice |

Supplies shall raise invoice |

Understanding 122(1B)(ii)

ECO shall be liable to pay penalty if it allows an inter supply of goods or services or both through it by a person who is not eligible to make such inter-state supply.

-

- Inter-state supply( whether taxable/exempt) by a person not eligible to make inter-state supply‑

Not allowed

- Inter-state supply( whether taxable/exempt) by a person not eligible to make inter-state supply‑

Impact

Question: Who are not eligible for making inter-state supply of goods/services through ECO?

Answer:

As per section 24, compulsory registration is required for inter-state taxable supply of goods/services. Thus, to make inter-state taxable supply, registration is mandatory and URPs are not eligible to make such supply. If ECO allows inter-state taxable supply by URP, then ECO is liable to pay penalty.

Since, section 122(1B)(i) specifically covers supply (whether intra/inter, exempt/taxable) by URP, it can be assumed that it will prevail over 122(1B)(ii).

Exception: Persons covered under Section 23 + NN05/2017 are not liable to register after amendment vide Clause 131

As per section 10, composition dealers are not allowed to make

- Inter-state supply of goods or services (exempt/taxable)

- Supply of goods or services through ECO which is liable to collect TCS u/s 52

- After the amendment vide clause 128 of Finance Bill, 2023, composition dealers can make supply of goods through ECO.

- Composition dealers can supply goods/services through ECO not liable to collect TCS. Even though composition dealers are allowed to supply Goods through ECO (liable to collect TCS) or Goods/services through ECO (not liable to collect TCS), but still they are not allowed to make any interstate supply of goods/services (exempt/taxable) through ECO.

So, if ECO allows inter-state supply of goods or services to composition dealers, then ECO shall be liable for penalty.

| -ECOliable to collect TCS | ECONot liable to collect TCS | |||

| Allowed supply composition dealers |

by | Intra-state supply of goods (clause 128 of Finance bill, 2023) | Intra-state goods/services | supply of |

Understanding 122(1B)(iii)

ECO shall be liable to pay penalty if it fails to furnish correct details (in statement u/s 52(4))of outward

supplies effected through it by a person exempted from obtaining registration under the act. Penalty for incorrect details of supply by exempted URPs

Persons exempted from obtaining registration under the act: Section 23 + NN 05/2017

-

- Exclusively exempt Supplies

- Agriculturist

- Supplying only those outward supplies which are liable to tax under RCM

The details of outward supplies of registered persons (including composition dealers) effected through ECO can be cross-checked with the details furnished by them in their returns. However, same is not possible in case of URPs and the chances of evasion are higher. That’s why section 122(1B)(iii) has been introduced to ensure the genuineness of details of supplies of exempted URPs through ECO.

Clause 139

Omission of Section 132(1)(g), 132(1)(j) and 132(1)(k) implying no prosecution for the offences covered in these clauses.

Section 132(1)(g) Obstructs or prevents any officer in the discharge of his duties under this act.

Section 132(1)(j): Tampers with or destroys any material evidence or documents.

Section 132(1)(k): Fails to supply any information which he is required to supply under this Act or the rules made thereunder or (unless with a reasonable belief, the burden of proving which shall be upon him, that the information supplied by him is true) supplies false information.

The above omission is a welcome step as many officers would cover the taxpayers under the above clauses even in genuine cases.

Also, relief has given to the persons who attempts to commit, or abets the commission of above offences by excluding them from the scope of section 132.

Earlier

1) The persons who attempts to commit, or abets the commission of offences under clause (g) and (j), were liable for punishment with imprisonment upto 6 months or with fine or both without considering the amount of tax evasion/wrongly availed or utiised ITC/refund wrongly taken.

2) Upto 1 year imprisonment along with fine was imposed where amount of tax evasion/wrongly availed or utilised IT C/wrong refunds > lcrore<2crores. However, amendment has been proposed to de-criminalize the offences where amount does not exceed 2crores except for 132(1)(b). Thus, the cases where a person issues any invoice or bill without supply of goods or services or both in violation of the provisions of this Act, or the rules made thereunder leading to wrongful availment or utilisation of input tax credit or refund of tax, shall continue to be treated as criminal offences even though amount <2crores but >lcrore punishable with lyear Jail with fine.

Our Comments:

The amendment seeks to

√ De-criminalize offences where amount involved is upto 2crores except the cases where invoice is issued without any actual supply.

√ Treat clauses (g), (j) and (k) of 132(1) as Non-offences.

√ Treat attempts to commit, or abets the commission of acts covered in above clauses as Non-offence.

However, falsifying or substituting financial records or producing fake accounts or documents or furnishing any false information with an intention to evade payment of tax due under this Act will still be punishable under clause (0 of 132(1) with imprisonment upto 6 months or with fme or both under clause (iv) of 132(1) and that too without considering the amount involved.

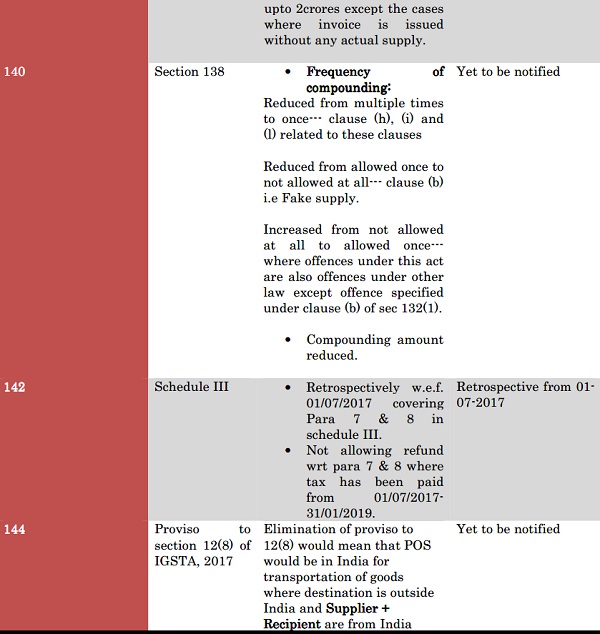

Clause -140 Relating to compounding of Offences

Amendment in Section 138(1)

1) Compounding is allowed only once in respect of offences under clauses (h), (i), and clause (l) relating to clause (h) & (i) section 132(1) after the amendment. Earlier, compounding relating to these clauses was allowed for multiple times as well.

Clause (h):

Acquires possession of, or in any way concerns himself in transporting, removing, depositing, keeping, concealing, supplying, or purchasing or in any other manner deals ,with any goods which he knows or has reasons to believe are liable to confiscation under this Act or the rules made thereunder.

Clause (i):

Receives or is in any way concerned with the supply of, or in any other manner deals with any supply of services which he knows or has reasons to believe are in contravention of any provisions of this Act or the rules made thereunder.

Clause (l) relating to clause (h) & (i):

Attempts to commit, or abets the commission of offences under (h) & (i)

Crux: Now, compounding is allowed only once for all types of offences except those where compounding is not allowed even once.

2) Omission of clause b of section 138(1) as compounding for multiple times is not allowed after the above amendment for any type of offence.

3) Compounding is not allowed even once wrt following offences:

√ A person who has been accused of committing an offence under this Act which is also an offence under any other law for the time being in force

Substituted by:

A person who has been accused of committing an offence under clause (b) of sub-section (1) of section 132

Impact:

Thus, compounding is allowed for those offences under this act which are also an offence under any other law for the time being in force. However, it is not allowed for offence covered in 132(1)(b) i.e. Issuing invoice/bill without actual supply leading to wrong availment or utilisation of ITC or refund of tax.

√ A person who has been convicted for an offence under this Act by a -Nocourt amendment

√ A person who has been accused of committing an offence specified in clause (g) or clause (j) or clause (k) of sub-section (1) of section 132- Omitted as not treated as offences anymore.

Amendment in Section 138(2)

Minimum compounding amount: 25% of Tax involved

Maximum compounding amount: 100%of Tax involved

Earlier

Minimum compounding amount: [10000 or 50% of Tax involved] whichever is higher Maximum compounding amount: [30000 or 150% of Tax involved] whichever is higher

Crux:

Frequency of compounding:

Reduced from multiple times to once— clause (h), (i) and (l) related to these clauses i.e.

[Possess or deal with goods liable to confiscation—which he knows or has reasons to believe]

[Receives or concerns himself in any way with the supply of services which contravene act/rules—which he knows or has reasons to believe]

Reduced from allowed once to not allowed at all– – clause (b) i.e Fake supply.

Increased from not allowed at all to allowed once— where offences under this act are also offences under other law except offence specified under clause b of 132(1).

Amendment in Section 138(2)

Minimum compounding amount: 25% of Tax involved

Maximum compounding amount: 100%of Tax involved

Earlier

Minimum compounding amount: [10000 or 50% of Tax involved] whichever is higher

Maximum compounding amount: [30000 or 150% of Tax involved] whichever is higher

Crux:

Frequency of compounding:

Reduced from multiple times to once— clause (h), (i) and (l) related to these clauses i.e.

[Possess or deal with goods liable to confiscation—which he knows or has reasons to believe]

[Receives or concerns himself in any way with the supply of services which contravene act/rules—which he knows or has reasons to believe]

Reduced from allowed once to not allowed at all— clause (b) i.e Fake supply.

Increased from not allowed at all to allowed once— where offences under this act are also offences under other law except offence specified under clause b of 132(1).

Clause 144 – Omission of proviso to section 12(8) of IGSTA, 2017

Section 12(8)

The place of supply of services by way of transportation of goods, including by mail or courier to,-

(a) A registered person, shall be the location of such person;

(b) A person other than a registered person, shall be the location at which such goods are handed over for their transportation.

Proviso: Provided that where the transportation of goods is to a place outside India, the place of supply shall be the place of destination of such goods.

Purpose of amendment

Before the circular 184/16/2022, it was a contentious issue whether ITC is available where supplier

and recipient are from India but place of supply is outside India due to proviso to 12(8) of IGSTA, 2017.

Another issue was that the state of the GST registered recipient was losing the GST revenue as the same does not accrue to it due to POS being ‘Outside India’.

Thus, to benefit the losing state— The amendment is proposed to bring POS back to India by omitting the proviso to 12(8) of IGSTA, 2017.

After the amendment, where both the supplier & the recipient are from India, the POS shall be

determined according to section 12(8) which makes

Location of recipient as the POS—If recipient is registered.

Otherwise, Location of supplier.

Circular 184/16/2022 clarified ITC admissibility

Attention is invited to sub-section (8) of section 12 of Integrated Goods and Services Tax Act, 2017 (hereinafter referred to as “IGST Act”) which provides for the place of supply of services by way of transportation of goods, including by mail or courier, where location of the supplier as well as the recipient of services is in India. As per clause (a) of the aforesaid sub-section, the place of supply of services by way of transportation of goods, including by mail or courier, to a registered person shall be the location of such registered person. However, the proviso to the aforesaid sub-section which was inserted vide the Integrated Goods and Services Tax (Amendment) Act, 2018 w.e.f. 01.02.2019 provides that where the transportation of goods is to a place outside India, the place of supply of the said service shall be the place of destination of such goods. In such cases, as the place of supply of services, as per the proviso to sub-section (8) of section 12 of IGST Act, is the concerned foreign destination and not the State where the recipient is registered under GST , doubts are being raised regarding the availability of input tax credit of the said services to the recipient located in India.

| S. No. | Issue | Clarification |

| 1 | POS where supplier & recipient in India and destination of goods is outside India? | In case of supply of services by way of transportation of goods, including by mail or courier, where the transportation of goods is to a place outside India, and where the supplier and recipient of the said supply of services are located in India, the place of supply is the concerned foreign destination where the goods are being transported, in accordance with the proviso to the sub-section (8) of section 12 o f IGST Act, which was inserted vide the Integrated Goods and Services Tax (Amendment) Act, 2018 w.e.f. 01.02.2019. |

| 2 | Whether the supply of services will be treated as inter-State supply or intra-State supply in Issue 1? | The aforesaid supply of services would be considered as inter-State supply in terms of sub-section (5) of section 7 of the IGST Act since the location of the supplier is in India and the place of supply is outside India. Therefore, integrated tax (IGST) would be chargeable on the said supply of services. |

| 3 | In Issue 1, whether the recipient of service of transportation of goods would be eligible to avail input tax credit in respect of the said input service of transportation of goods? | Section 16 of the CGST Act lays down the eligibility and conditions for taking input tax credit whereas, section 17 of the CGST Act provides for apportionment of credit and blocked credits under circumstances specified therein. The said provisions of law do not restrict availment of input tax credit by the recipient located in India if the place of supply of the said input service is outside India. Thus, the recipient of service of transportation of goods shall be eligible to avail input tax credit in respect of the IGST so charged by the supplier subject to fulfillment of other conditions. |

| 4 | What state code has to be mentioned by the supplier of the said service of transportation of goods, where the transportation of goods is to a place outside India, while reporting the said supply in FORM GSTR-1? | The supplier of service shall report place of supply of such service by selecting State code as ‘96-Foreign Country. |

–

Author Bio