Cancellation Of GST Registration

- By Legal Heirs

- By Registered Person

- By Proper Officer

By Registered Person: 29(1)

- Business Discontinued

- Amalgamation

- Demerger

- Transfer Of Business

- Change In Constitution of Business

- Otherwise, Disposal of Business

- No Longer Liable U/S 22 OR 24

- Intend To Opt-Out of Voluntary Registration U/S 25(3)

BY LEGAL HEIRS: 29(1)

| DEATH OF PROPRIETOR | Discontinuation | Amalgamation | Demerger |

| Death | Otherwise Disposal | Change in Constitution | |

| Transfer of business | Not Liable u/s 22/24 | Opt-out from Voluntary Registration |

SUO-MOTTO BY PROPER OFFICER: 29(2)

- Contravention of specified provisions by RP (Rule 21)

- Composition dealer has not furnished GSTR 4 within 3 months from the due date of such return

- Other than a Composite RP, has not furnished return(GSTR 3B) for such continuous tax period as may be prescribed

♦ Normal: For continuous 6 Months

♦ QRMP: For continuous 2 Tax Periods

- Voluntary RP has not commenced business within 6 months from the date of registration

- Registration has been obtained by means of fraud, wilful misstatement or suppression of fact

Liability of RP not affected due to cancellation: 29(3)

Liability of RP shall not get affected due to cancellation even if these are determined after effective date of Cancellation.

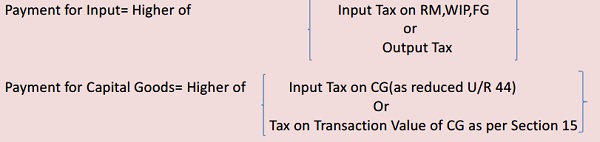

Payment on cancellation: 29(5)

Every RP whose registration is cancelled, shall pay an amount, by way of debit in E-Credit Ledger/ E-Cash Ledger

Transaction value as per section 15(1): a) Price actually paid/payable b) Supplier & recipient are unrelated c) Price is the sole consideration.

Rule 40(2): For Sec 18(6), ITC of CG shall be calculated @5%/Quarter or part thereof from the date of issue of invoice. [Benefit to RP]

Section 18(6): Where CG has been supplied by RP on which ITC has been taken, the RP shall pay

Rule 44: For ITC reversal on RM/WIP/FG or CG under section 18(4) or 29(5)

18(4):

- Regular to composition

- Taxable to Exempt

29(5):

- Registration cancellation

For RM/WIP/FG: Input tax credit to be reversed shall be calculated proportionately on the basis of the corresponding invoices on which credit had been availed(no need of utilisation as the amount in credit ledger will be reduced) by the registered taxable person on such inputs.

If Invoice is not available: Consider prevailing Market Rate as on the date of Opting in for Sec 10/Exemption date/Effective date of cancellation.

This calculation(market rate based) needs to be certified by CA/CMA.

For CG: ITC to be reversed shall be the ITC belonging to remaining useful life in months considering the total useful life of FIVE YEARS(60Months)

♦ Part of the month= 1month

Above calculations are to be done separately for CGST, IGST, SGST, UTGST.

Above reversals are to be shown in

- GST ITC-03 for section 18(4)

- GSTR 10 for section 29(5)

44(6): For Section 18(6) also, above method of ITC calculation is to be used.

Provided that where ITC amount>Tax on T.V, then that ITC will become Output Tax Liability and the same shall be furnished in GSTR 1.

Both Rule 44(6) & 40(2) cover Section 18(6), However, Rule 40(2) is more beneficial to RP and thus the same can be preferred

RULE 21: CANCELLATION BY PROPER OFFICER ON CONTRAVENTION

- Not conducting business from declared POB

- Fake supply

- Violates Section 171 and related rules (Involves in profiteering i.e. Retains benefit of reduction in tax rates and/or ITC)

- Violates Rule 10A of CGST Rules i.e Non-furnishing of bank account details after getting registration

- Avails ITC in violation of Section 16

- Outward supply in GSTR 1 for one or more tax periods > Details in 3B for said periods

- Violates the provisions of Rule 86B (Restriction on use of E-credit Ledger Balance)

- Normal Taxpayer fails to file GSTR 3B for continuous 6 Months

- QRMP Taxpayer fails to file GSTR 3B for continuous 2 Tax periods

M/S SHYAM SUNDAR SITA RAM TRADERS vs. STATE OF UP

Where action has been initiated u/s 74 against a RP, then the registration of such RP cannot be cancelled u/s 29(2) by P.O on the ground that said RP is non-existent and mere Bogus firm.

RULE 21A: SUSPENSION OF GST REGISTRATION

As per Section 29, When cancellation application is filed by RP or cancellation is initiated Suo-motto by proper officer, the proper officer is authorized to suspend registration during pendency of cancellation proceedings for such period and in such manner as prescribed in Rule 21A.

21A(1): Where RP has applied for cancellation under rule 20, the registration shall be deemed to be suspended from the date of submission of application or the date from which cancellation is sought, whichever is later, pending the completion of proceedings under rule 22.

21A(2): Where P.O has reasons to believe that the registration is liable to be cancelled under rule 21, he may suspend the registration from a date to be determined by him, pending the completion of proceedings under rule 22. [WITHOUT PROVIDING OOBH, however SCN for cancellation is required]

[suspension date decision to be taken by P.O and not by CCGST/CSGST]

21A(2A) Anomalies leading to cancellation of registration, detected on comparison of 3B with GSTR 1 or 3B with GSTR 2A/2B, registration shall be suspended and GST REG-31 shall be issued.

- SCN for Cancellation under Rule 21A(2A): GST REG-31

- Time to Reply: 30 Days

- Mode of communication: Portal and/or Email

21A(3):

- RP not to make any Taxable supply during suspension (Explanation: No Taxable supply means Not to Issue Tax Invoice and not to charge Tax)

♦ This means, during suspension period also, supply can be made using Bill of supply and that too @MRP otherwise RP has to bear Tax cost himself.

♦ And Later on revocation of suspension, Revised Invoices needs to be issued u/s 31(3)(f) within 30 days from the date of revocation.

- No need to file GSTR 3B for suspension period

- No refund to RP u/s 54 during suspension period where cancellation is initiated by P.O

- Deemed revocation of suspension upon completion of cancellation proceedings and effective date of revocation will be the date of suspension itself.

♦ Thus, where cancellation request is rejected: Returns for suspension period needs to be filed later on.

- Revocation of suspension by P.O during pendency of proceedings: If he deems fit

- Where the registration has been suspended by P.O due to non-filing of returns, and has not already been cancelled, the suspension shall be deemed to be revoked upon filing of all the pending returns

♦ This means, return filing option has to be provided in suspension period also where registration is suspended due to non-filing of returns.

- Where suspension is revoked, Section 31(3)(a) and section 40 shall apply w.r.t. supplies effected during suspension period.

♦ As of now, First Return u/s 40 is not applicable.

RULE 22- Cancellation of Registration

- SCN in Form GST REG-17 by P.O

- Reply to be given in 7 Days from the date of service of notice in Form GST REG-18

- Cancellation Order (effective from a date to be determined by P.O) in Form GST REG-19 within 30 Days

from the date of application by RP/legal heirs in GST REG-16 or the date of reply to SCN(GST REG-17) under Rule 22(1) or SCN under rule 21A(2A)

♦ Reply to SCN (REG 31) under Rule 21A(2A)- 30Days

♦ Reply to SCN (REG 17) under Rule 22(1)- 7Days

Drop Proceedings: GST REG-20

♦ Where reply to SCN REG31/REG17 is satisfactory

♦ Proceedings to be dropped even without reply where SCN REG-17 was issued u/r 22(1) due to Non-filing of returns as provided in section 29(2)(b)/(c), and all the returns have been filed along with payment of dues.

Section 30-Revocation of Cancellation of Registration:

30(1): RP can apply for revocation within 30 Days (within such period and in such manner and subject to such conditions & restrictions, as may be prescribed, by making amendment in Finance Bill, 2023 vide Clause 131A) from the date of service of cancellation order in GST REG-19 where cancellation has been initiated by P.O

Provided that, the above time limit can be extended by

♦ AC/JC by 30days

♦ Commissioner by further 30days

30(2): P.O can either accept/reject revocation application

♦ Order within prescribed time (Rule 23)

♦ OOBH before Rejection order

Rule 23 Prescribes

- Time limit for revocation application (At present, 30Days time limit has been prescribed in rule to align it with section 30, However, after Clause 131A of Finance Bill, the time limit specified in the section has been removed and rule has been given full authority w.r.t. specifying time limit. Thus, amendment can be expected in the rule to specify new time limit)

- Manner of Revocation Application

- Conditions & restrictions for revocation application (At present, Rule 23 only specifies conditions for applying for revocation, However, amendment is expected in the rule to specify restrictions as well)

Rule 23- Revocation of Cancellation

- Subject to Rule 10B [Aadhar Authentication], RP may make an application for revocation in Form GST REG-21 within 30Days from the date of service of cancellation order in REG-19

Where Registration is cancelled prospectively:

- File pending returns(till the cancellation order) along with dues before revocation application where registration is cancelled for non-filing

- File pending returns(from the date of cancellation order till the date of revocation order) within 30Days from revocation order

Where Registration is cancelled retrospectively:

- File pending returns (from the effective date of cancellation till the date of revocation order) within 30Days from revocation order

√ Revocation Acceptance order in GST REG-22 within 30Days from the date of receipt of application V’ Revocation Rejection order in GST REG-05

♦ Before issuing REG-05, P.O shall issue SCN in REG-23 (why revocation application not to be rejected)

♦ Reply by RP in REG-24 within 7 Working days from the date of service of REG-23

♦ P.O shall act on the Reply in REG-24 within 30Days from the date of reply

Revocation Application cannot be filed without Aadhar Authentication.

Author Bio