Background

The Goods and Services Tax constitutional amendment having been promulgated by the Govt of India, the rollout of the GST Bill will be a collective effort of the Central and State Governments, the tax payers and the IT platform provider i.e. GSTN, CBEC and State Tax Departments. Besides these main participants there are going to be other stakeholders e.g. Central and States tax authorities, RBI, the Banks, the tax professionals (tax return preparers, Chartered Accountants, Tax Advocates, STPs etc.), financial services providing companies like ERP companies and Tax Accounting Software Providers etc.

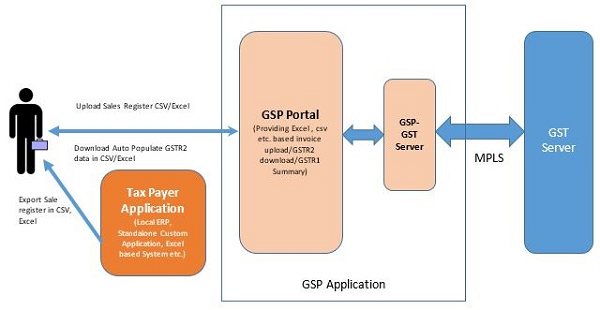

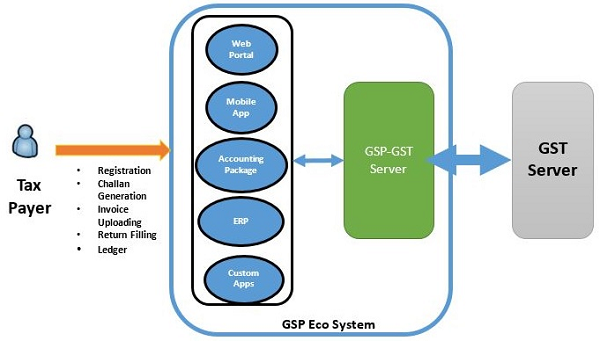

The GST System is going to have a G2B portal for taxpayers to access the GST Systems, however, that would not be the only way for interacting with the GST system as the taxpayer via his choice of third party applications, which will provide all user interfaces and convenience via desktop, mobile, other interfaces, will be able to interact with the GST system. The third party applications will connect with GST system via secure GST System APIs. All such applications are expected to be developed by third party service providers who have been given a generic name, GST Suvidha Provider or GSP. The GSPs are envisaged to provide innovative and convenient methods to taxpayers and other stakeholders in interacting with the GST Systems from registration of entity to uploading of invoice details to filing of returns. Thus there will be two sets of interactions, one between the App user and the GSP and the second between the GSP and the GST System. It is envisaged that App provider and GSP could be the same entity. Another version could where data in required format directly goes to GSP-GST Server. The diagram below gives the most generic case.

In the evolving environment of the new GST regime it is envisioned that the GST Suvidha Providers (GSP) concept is going to play a very important and strategic role. It is the endeavour of GSTN to build the GSP eco system, ensure its success by putting in place an open, transparent and participative framework for capable and motivated enterprises and entrepreneurs.

GST Compliance Requirement by the Taxpayer

The taxpayer under GST Regime will have to provide following information at regular intervals:

- Invoice data upload (B2B and large value B2C)

- Upload GSTR-1 (return containing supply data) which will be created based on invoice data and some other data provided by the taxpayer.

- Download data on inward supplies (receipts or purchase) in the form of Draft GSTR-2 from GST Portal created by the Portal based on GSTR-1 filed by corresponding suppliers.

- Do matching of purchases made and that downloaded from GST portal. Finalize the same based on his own purchase (inward supply data) and upload GSTR-2

- File GSTR-3 created by GST Portal based on GSTR-1 and 2 and other info and tax paid.

- Similarly there are other returns for other categories of taxpayers like casual taxpayer or composition taxpayers.

Concept

It is expected that the GSPs shall provide the tax payers with all services mentioned above in addition to maintaining their individual business ledgers (sales ledger and purchase ledger) and other value added services around the same. Another important service expected from GSPs is the automatic reconciliation of purchase made and entered in the purchase register and data downloaded in the form of GSTR-2 from the GST portal. In additional there will be sector-specific or trade specific needs which the GSPs are expected to fulfil. The conceptual diagram depicting the same is as given below.

While the GST System will have a G2B portal for taxpayers to access the GST System there will be a wide variety of tax payers (SME, Large Enterprise, Small retail vendor etc.) who will require different kind of facilities like converting their purchase/sales register data in GST compliant format, integration of their Accounting Packages/ERP with GST System. Similarly, the specific needs of an industry or trade could be met by GSP. In short, the GSP can help the taxpayers in GST compliance through their innovative solutions.

Design & Implementation Framework

Tax payer’s convenience will be a key in success of GST regime. The tax payer should have a choice to use third party applications which can provide varied interfaces on desktops, laptops and mobiles and can connect with GST System. The GSP developed apps will connect with the GST system via secure GST system APIs. Majority of GST system functionalities related to taxpayer’s GST compliance requirements shall be available to the GSP through APIs. GSPs may use GST APIs and enrich and enhance the tax payer’s experience. (The APIs of GST System are RESTful, json-based and stateless). GST System will not be available over the Internet for security reasons.

The production API end points can only be consumed via MPLS lines. All APIs will be accessed over HTTPS protocol. The benefits of API based integration are:

- Consumption across technologies and platforms (mobile, tablets, desktops, etc.) based on the individual requirements

- Automated upload and download of data

- Ability to adapt to changing taxation and other business rules and end user usage models.

- Integration with customer software (ERP, Accounting systems) that tax payers and others are already using for their day to day activities

Selection and On-boarding of GSPs

Any prospective applicant for GSP will need to meet a pre-qualification criteria for GSPs. The pre-qualification criteria are detailed later in this document.

GSPs who meet the pre-qualification criteria will sign a contract with GSTN to become an authorised GSP.

On signing of the contract, GSPs will get a unique license key for accessing the GST system. GSPs will be authenticated using this license key (Client id + Client Secret) provided by GSTN. GSP will have a provision to generate multiple License keys as per its need.

Who Can Become a GSP?

The organisations and entities who are expected to sign up as GSPs are visualised to be as under:

Registered companies in India in the IT / ITES / BFSI domain.

| Organization Type | Pre-qualification criteria | Supporting documents | |

| 1 | A company registered in India under the Indian Companies Act 1956 or 2013 meeting the pre-qualification criteria given in next column. | An IT / ITES / BFSI company having IT capability with the following parameters:

1. Financial Strength: a. Paid up / Raised capital of at least Rs. 5 crores and b. Average turnover of at least 10 Crores during last 3 financial years 2. Demonstration of capabilities: As given in 3. Technical Eligibility Criteria: As indicated in Table 2 below |

1. Letter of Intent by CMD/MD expressing interest to become GSP.

2. Letter of authority, authorizing the signatory to sign documents on behalf of the organization along with the attested specimen signatures (both initials and full) 3. Extract of AOA and MOA mentioning area of operation pertaining to IT / ITES / BFSI 4. Certificate of incorporation (In case of Partnership firms Registered Partnership deed) 5. Copy of Service Tax Number / TIN / PAN 6. Board Resolution for making GSP Application 7. Certified copy of letter of commencement of business issued by Ministry of Corporate Affairs (MCA)/ (In case of Partnership Firms, Registration Certificate from Registrar of Firms) |

| 2 | An undertaking owned and managed by Central / State Government (PSU) OR An Authority constituted under the Central / State Act/Special Purpose Organization constituted by Central/State govt. | As above | 1. Letter of Intent by Managing Director/Chief Managing Director of PSUs expressing interest to become a GSP

2. Letter of authority, authorizing the signatory to sign documents on behalf of the organization along with the attested specimen signatures (both initials and full) 3. Letter of establishment of PSU |

| 3 | Partnership registered under the India Partnership Act 1932 or under the Limited Liability Partnership Act, 2008 | As above | 1. Letter of Intent by the partners expressing interest to become GSP

2. Letter of authority, authorizing the signatory to sign documents on behalf of the organization along with the attested specimen signatures (both initials and full) 3. Registered Partnership deed. 4. Copy of Service Tax Number / TIN / PAN |

TABLE-1 : Demonstration of Technical Capability

Demonstrate, within 1 month of being offered the opportunity, a functioning model as a GSP with effective, efficient and useful tax payer oriented services to include at least (but not limited to):

| Sr No. | Suggested Test Activity | Evaluation Weight |

| i. | Invoice upload by tax payers | 10 |

| ii. | GST Return #1 and #2 preparation and filing | 10 |

| iii. | Reconciliation of downloaded GSTR2 with Purchase Register | 20 |

| iv. | Multiple GSTIN Ids mapped to a single user account | 5 |

| v. | Multiple roles mapped to single GSTIN | |

| vi. | E-sign / DSC integration for signing of returns | 10 |

| vii. | UI / UX | 15 |

| viii. | Mobile interface | 10 |

| ix. | Alert generation to tax payers | 5 |

| x. | Security design | 5 |

| 10 |

Note: The demonstration by the applicant GSP shall be evaluated basis the marks stated above. Minimum qualifying marks will 60 %.

TABLE-2: Technical Eligibility Criteria

| S.No. | Pre-Qualification Criteria | Supporting Documents |

| 1 | Backend infrastructure, such as servers, databases etc., required specifically for the purpose of GSP work shall be based in the territory of India, and | Declaration from the authorized signatory |

| 2 | IT Infrastructure owned or outsourced to carry out minimum of 1 Lakh GST transaction per month, and | Declaration from the authorized signatory, Submit IT Infrastructure details i.e. Server Details, Network Connectivity, Firewall Server, storage capacity, Disaster recovery plan etc. |

| 3 | Data Privacy policy to protect beneficiary privacy, and | Share the data privacy policy on organization’s website |

| 4 | Data security measures as per the IT Act. | Certification / Declaration from the authorized signatory |

Important Note:

1. The selected GSPs will be required to sign a contract between GSTN and the GSP and comply to the terms and conditions therein and also adhere to specifications given by GSTN from time to

2. The GSP will also give an affidavit (legal liability) undertaking that the data exchanged or sourced from GST System shall not be used for any financial product selling to tax payers directly or indirectly through subsidiaries/ parent companies. Violation of the same will not only lead to cancellation of license but other punitive action as per relevant laws.

√ GSPs can facilitate the tax payers in uploading invoices as well as filing of returns and act as a single stop shop for GST related services.

√ GSPs can customize products that address the needs of different segment of users.

√ Yes, the GSPs are free to charge the tax payers depending on the services they offer to the tax payers.

√ Agreements between tax payers and GSPs shall be decided by them exclusively. GSTN will not have any lien on them.

√ GSPs will need to conform to GST system technical interface and integration requirements.

√ Details of agreements with GSTN will be included in an agreement to be signed between GSPs and GSTN.

√ Yes, this would be left entirely to the GSPs. GSTN does not intend to have any restrictions on this. To be competitive, GSPs anyway would have to be pragmatic in their pricing.

Q:7 What are the legal compliance and fee involved to become a GSP?

Plase Visit: http://www.gstn.org/ecosystem/pdf/Agreement_GSP_legal_standard_draft.pdf

Q:8 What are the SLAs from STQC/third party auditors to validate the GSP services?

√ The GSP applications will have to go through STQC / authorized agency audit process. The compliance requirements will be to standards of security, business continuity and processes e.g. ITIL, ITSM, etc. The requirements of audit will be made available prior to the audit process so that applications can abide by the required standards during their development process. As an indicator, ISO 24001 standard compliance practices should be taken as reference.

Q:9 Will a taxpayer be allowed to be registered with multiple GSPs?

√ Yes, if the taxpayer desires so, it would be possible to choose a set of services from one GSP and the rest from other GSPs e.g. tax payer can choose one GSP for registration and another for returns filing.

Q:10 Is a data Centre in India must for a GSP?

Yes, For detail please visit here

While GSP may offer his services to tax payers from anywhere and any data center, while connecting to GST System, GSP will connect from an entity based in India only.

Q:11 How will Tax payers know the list of GSPs available to consume their services? Will GSTN have any strategy to help tax payers identify their GSPs?

√ The list of authorized GSPs and their services portfolio would be published on GST System Portal.

√ A communication strategy will be evolved where tax payers would continuously be updated on existing GSPs, de-listed GSPs or new enlisting GSPs.

Q:12 What benefits would a Tax payer see to consume the GSPs application, when GSTN provides the portal to perform all processes?

Currently GST System is providing one GSTIN, one userid. GSP can create innovative solution to solve this use case.

Q:13 Will taxpayers having multiple branches/locations and requirement to consolidate data and central approval (role of GSP to facilitate the same) be able to login from different sites or not?

Yes, GSP can provide such solutions to Tax payers.

Q:14 What will be the role of Tax return preparers (Tax professionals/TRP) in return generation and submission (and resultant work flow management)?

√ Tax return preparers (Tax professionals/TRP) are going to facilitate taxpayers in preparing and filing their monthly, quarterly and annual returns.

√ These Tax professionals/TRP may provide the facilities and services directly to tax payers by accessing the GST System.

√ Alternately, TRPs may also subscribe to services of GSP or Application Providers, subject to the terms and conditions prescribed by the GSPs or Application Providers. For example Application Provider would include “Tax Accounting Software Providers” or Companies provider Invoice generation/reconciliation as a service etc.

Q:15 What will be the flexibility for taxpayer to choose his ASP-GSP combination and on a dynamic basis Operational issues (Continuous upload, usage of OTP, requirement for multiple DSC users, Tokens etc.)?

√ The tax payer is free to choose his Application Providers and / or GSP irrespective and independent to the other.

Q:16 Will an agreement be signed between GSPs and GSTN?

Yes, an agreement will be signed between GSTN and the GSPs.

Q:17 Will the contents (SLAs) of agreement be discussed and deliberated with all potential GSPs?

Standardized SLAs will be built into the agreement to be met by the GSPs.

Q:18 What is the number of GSPs proposed to be boarded by GSTN?

The number is not fixed but is not expected to be too large. To start with, a handful of GSPs are expected to be on boarded by GSTN.

Source- http://www.gstn.org

GSTR 3B PDF Download

Can we maintain multiple GSP for same GSTN.

eg. out off 100 e-invoices can we generate 50 from from GSP-A and rest from GSP-B of same GSTN