Why a 262-year-old listed travel company (i.e., Cox & Kings) with a value of 9000 Crores in FY 2017-18 went bankrupt for non-payment of just 200 Crores Loan in Oct 2019

Introduction:

Cox & Kings Ltd set up in 1758, is one of the longest established travel companies. Headquartered in India and the UK, the holiday and education travel group has subsidiaries in the United States, Canada, the United Kingdom, Netherlands, the United Arab Emirates, Japan, Singapore, Australia and New Zealand. Cox & Kings Ltd. has operations spread across 22 countries and 4 continents. Historically, Cox and Kings Ltd. has been an army agent, a travel agent, a printer and publisher. It has also worked as a news agent, cargo agent, ship-owner, banker, insurance agent, and dealer of several travel-related activities. Its core activities now include the sale of packaged holidays.

Financial Statement Analysis:

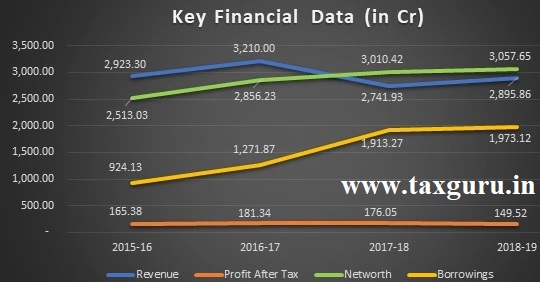

Cox & Kings was a financially sound company with stable revenue and profit and with constantly increasing networth and diversity in operations. Below image evidences the same:

With constant increase in operations and continuous expansion of business, increased borrowings are justified. Company was maintaining healthy profits with good dividend payout of 20% till FY 2017-18 which has led to belief that company is a financially sound company and company’s share was trading over Rs 200 till the end of the year 2018.

Below reasons has led to decrease in value of the company from 1.2 Billion Dollars (Around 9000 Crores) in FY 2017-18 to Rs 16.77 Crores Market Capitalization as on date.

Reasons behind fall of the Company:

1. Leverage Buyout:

Buyout means purchasing controlling stake in a company. Source of funds for companies going for buyout can be either their cashflows from existing businesses or funds raised by way of taking loan / issuing bonds. Latter one is referred as Leverage Buyout and often a risky one since bad performance of a acquired business can impact the holding company.

Below is the list of some of the companies acquired by Cox & Kings. These acquisitions led to increased debt and thereby huge finance cost on the company:

| Month | Name of the Company | Amount |

| Aug-09 | East India Travel Company | 22 Million Dollars |

| Jan-10 | Tempo Holidays | 25 Million Dollars |

| Sep-11 | Holiday Break | 323 Million Pounds |

| Oct-15 | LateRooms Ltd | 8.5 Million Pounds |

2. Unrelated Diversification:

Related diversification refers to a process where company expands into the product lines that are similar to those it currently offers. In vertical integration, company acquires business of its supplier / customer who are in same supply chain but at different levels so as to make the product available to customers at a low price and also enjoy high profits. In horizontal integration, company acquires business of its competitors thereby enjoying an increased stake and also to avail synergy benefits.

Cox & Kings has opted for aggressive risk-taking approach whereby acquiring various companies with debt funds and some of them are in business that is not related (education business and NBFCs etc.) to the main business of packaged holidays of the company.

Such acquisitions will have following impact:

- No / negligible synergy effect for current business

- Lack of focus on main business due to various unrelated businesses

- Lack of focus resulting loss of stake in core business to competitors thereby decreased cashflows from the same

- Increased debt and interest obligations on the company

3. Cash Crunch and Huge Debt Obligations:

Above mentioned above, leverage buyouts led to cash crunch as a result of increased debt obligations since acquired businesses could not perform as expected. This has resulted in company selling some of its business units for the purpose of raising funds for meeting debt obligations. Company has made sale of stake in following entities / business units:

| Period | Name of Entity / BU | Amount |

| Jun-14 | Camping division Holiday Break | 892 Crores |

| Dec-15 | Explore Worldwide Limited | 25.8 Million Pounds |

| Mar-16 | LateRooms | 20 Million Pounds |

| Mar-16 | Superbreak business | 9.25 Million Pounds |

| 2018 | Education Business | 4300 Cr |

Due to cash crunch in the company, it has stopped trips to New Zealand & Australia to cut costs in the company. Only part proceeds from sale of education business were used for meeting debt obligations and balance proceeds could not be traced in books. This has led to shareholders complaining on Company & Management to Ministry of Corporate Affairs (MCA) which was further referred to Serious Fraud Investigation Office (SFIO) by MCA.

4. Siphoning of funds and Fraudulent Financial Statements

Yes Bank, which has Rs 2267.22 Crores outstanding from the company has ordered for Forensic Audit from PWC since the company has defaulted in repayment of Rs 200 Crores in the month of June 2019 despite having Rs 723 Crores of Cash & Cash Equivalents and Rs 2,031 Crores Debtors as on 31st March 2019. This has unveiled siphoning of crores of rupees and fraudulent financial reporting happened in past 4 years (i.e., from 2015-19). Key points for consideration includes below points:

| * Transactions worth 21,000 Cr has in four years (2015-19) done mainly to siphon off funds; falsifying records * Most of the related party transactions of Cox & Kings were executed without “proper approvals” from its board and without any loan agreement. In financial year 2019 alone, Cox & Kings loaned Rs 589 crore to at least 11 related parties “without executing loan agreements |

|

| Gave loan of Rs. 1,100 crore to Alok Industries | It is a stressed firm that went bankrupt in 2017. When loan was given, CFO of Alok Industries was Sunil Khandelwal, who is also brother of Cox & Kings CFO Anil Khandelwal. |

| sales worth Rs 9,000 crore to over 160 customers who are bogus or do not exist |

* Between 2014 and 2019, the company made sales of Rs 5,278 crore to 147 bogus customers. Of these, at least 141 are not registered with the Goods and Services Tax (GST) department. At least six customers have listed the GST registration number for Cox and Kings as their own registration number. * Between 2016 and 2019, Cox & Kings made a substantial portion of its Rs 3,908 crore sales from 15 customers, who allegedly are non-existent. A physical verification of the addresses of these customers found that these were residential addresses and no travel agencies ever operated from these places * Ledgers of Cox & Kings have recorded collections of Rs 2,548 crore from these 15 customers, the money was not traced in its bank accounts as no actual funds were received by Cox & Kings.Between April 2014 and June 2015, Cox & Kings recorded sales of Rs 250-Rs 260 crore against each of these 15 customers. All these transactions were “curiously” recorded only on the last day of the month |

| Inflated balances of Cash & Cash Equivalents | For FY 2019, the company disclosed cash and bank balances of Rs 723 crore and Rs 1,830 crore on standalone and consolidated levels respectively. Despite this, the company kept on defaulting on loan repayment since June 2019, indicating that it had inflated its cash and bank balances, which led to manipulation of its financial statements. |

| Reduced Debt | For FY 2019, Cox & Kings reported the total debt of the company at Rs 2000 crore, whereas the standalone debt of the company was Rs 3600 crore. Apart from this, a credit card debt of Rs 750 crore was not disclosed to lenders, in violation of the disclosure norms. |

Comparison of amounts payable as per Audited Financial Statements for the period ended 31st March 2019 with information filed on 14th April 2020 with Liquidator upon bankruptcy has shown following discrepancy (Amount in Crores):

| Particulars | 31-Mar-19 | 14-Apr-20 | Difference |

| Financial Creditors | 1,985.84 | 5,901.32 | 3,915.48 |

| Operational Creditors & Workmen | 675.57 | 747.15 | 71.58 |

| 2,661.41 | 6,648.47 | 3,987.06 |

Difference of 71.58 Crores of due to Operational Creditors and Workmen is not a major difference since Financial information from 01st April 2019 is not made available by the company but difference of Rs 3,915 Crores reveals suppression of debt by the company.

Indicators of Mis-management and Fraud within the entity: Mis-management / Fraud within an entity can be evidenced by the fundamental and management analysis of the company. Following indicators might provide for the same:

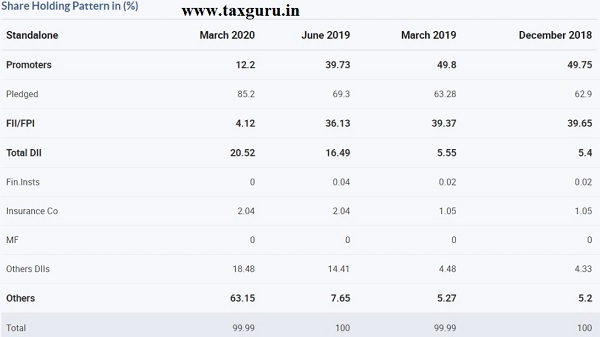

1. Decreased Promoter’s / FII’s Stake in the Company / Increased percentage of pledged shares by promoters:

Above indicator is key in assessing the future of the entity but a reasoned decrease in promoter’s stake (i.e., like a statutory requirement) should not be considered as negative sign for an entity. Below image describes share holding pattern of the company from Dec-18:

Further no investment by Mutual Funds also an indicator of high risk factor for a share.

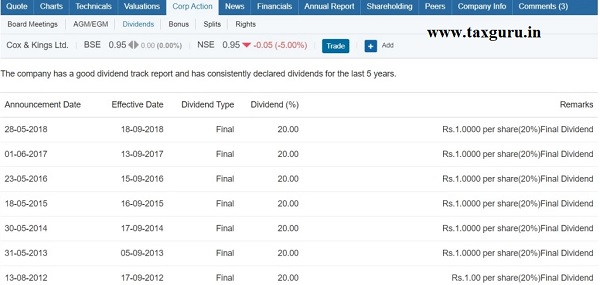

2. Stopped Dividend Payout without any reason:

A Company may stop declaring dividend owing to expansion of the business / cash crunch due to low / negative profits. But an unreasoned stoppage to dividend payout even when company is maintaining constant profits is an indicator of risk for a stock. Company has stopped declaration of dividend from May-18 despite having reasonable profits is evidenced by below picture.

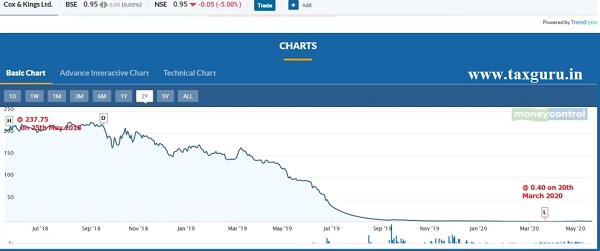

3. Correction of Share Price due to possible / probable news

For listed companies, any possible / probable negative news about the company can be evidenced by the correction (i.e., reduction) in share price. Below image evidences correction of share price from Rs 237.75 in May-18 to Rs 0.40 in Mar-20.

Takeaways from fall of Cox & Kings:

- Diversification is necessary for growth in the company but an unlevered buyout is always a safe option since the downside risk will not have major impact on core business

- Unrelated diversification is not always advisable unless the company is having a future plan of shifting into the other business / company is efficient in managing both the business and core business is earning sufficient cashflows for maintenance of group cashflows

- In expansion through unrelated diversification, entity should not reduce focus on core business since it is earning cash flows for maintenance of group. Any reduction in market stake will have an adverse impact since new businesses may not be able to generate independent cashflows and it may lead to closure of business

- Fraudulent Financial Reporting may look attractive in short-term for increasing value of the group but the same can lead to reduction in value of business and also civil and criminal action on both the company as well as management.

****

Disclaimer: The contents of this article are for information purposes only and do not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

The analysis shown are very correct. This is a sheer mis management case. The promotors have killed the company in such a short time. Promotors have not bothered to care for stakeholders and killed the company which was standing strong for such a long periods.

This is sheer fraud case as they have syphoned money, shown fake business and acquired businesses with getting kick back.

Promotors should be punished for the wrongdoing and being rude to stakeholders.

Regards

Ramesh Ghare