Introduction:

In investing terminology, the risk is often termed as getting a lower/negative return on investment. It is pertinent to note that even Bank Deposits have a risk of default by banks (i.e., in case of imposition or moratorium/closure of bank due to weak financial condition, depositors may be required to take a cut on their receivable amount). Though the possibility of this event is remote but not nil. This has happened in the case of the merger of South Indian Cooperative Bank with the Saraswat Bank.

Investing in Equity/Equity Oriented Mutual Funds is perceived as riskier since its returns are more volatile when compared to alternatives like Debt Funds and Bank Deposits. Debt mutual funds are considered to be relatively less volatile than equity mutual funds. While this may be true, especially over a long time, the probability of negative returns cannot be ruled out in the shorter term. This article elaborates about risk in debt mutual funds and then focuses on reasons for the same.

Risk in Debt Mutual Funds:

Debt Mutual Funds, unlike Bank Deposits, are not only prone to both risks related to interest receipts but also prone to market-related risks of the principal amount. i.e., Return on investment in Debt Mutual Funds depends upon the change in interest rates & change in principal value. This can be explained with the below example:

Suppose if an entity issued bonds of Rs.100 face value with a coupon rate of 10% and if the expected rate of return is 10%, then the bond will be trading at Rs. 100. If the expected return increases to 15%, then the bond price will fall to Rs. 67 to give the expected return of 15%. In the same way, if the expected return falls to 5%, then the bond price will increase to Rs. 200.

Though many factors cause a change in the expected rate, the effect of the same is the same as explained above. To summarise the above instances,

| Expected Rate | Bond Price | New Holder | Existing Holder |

| Decreases | Increases | Will buy the bond at premium☹ | Will enjoy capital appreciation😊 |

| Increases | Decreases | Will buy the bond at discount😊 | Will suffer capital loss☹ |

Volatility in Returns:

As explained above, return from Debt Funds varies on account of changes in both interest & principal amount. Average returns of various types of debt funds along with a comparison with an interest rate of Fixed Deposit with Bank (assumed as 6% constant) are tabulated below:

Average Returns of every calendar year are compared with that of FD returns and colored accordingly. Arrow marks evaluate the performance of the fund for that year with that of the entire period selected.

From the above diagram, one can conclude that Debt Mutual Funds hardly give returns exceeding FDs and hence not a preferred type of investment. But that is not the reality. There are various funds in each category that gave better returns than FDs continuously for many years. Investing after understanding the pros & cons of each fund will increase the chances of getting better returns.

Reasons for Above Risk:

– Increased supply in the market:

In the budget presented for FY22, The Government has announced that it will borrow Rs. 12 Lakh Crore in FY 21-22 & will borrow Rs. 80 Thousand Crore in remaining part of FY 20-21 (i.e., Feb-21 & Mar-21) to cover its fiscal deficit of 9.5% in FY22 & 6.8% in FY 21. This will increase the supply of bonds in the market. Since the available alternative investment stock market is giving better returns, investments are flowing into stocks and equity-linked schemes. Many fund managers have opined that the supply in this market is likely to be in excess for the next 4-5 years.

Further, some of the large corporates are considering issuing bonds as an alternative to borrowing for raising funds. The former one is beneficial since the interest cost is low when compared to bank loans. Credit Rating agency CRISIL has said that by FY25, the corporate bond market has the potential to double the market size to Rs.65-70 Lakh Crore (From Rs. 33 Lakh Crore in FY 20).

With increased supply & reduced demand, the value of the bonds has reduced and the required bond yield has increased accordingly. As explained above, increased required yield will reduce the bond price and hence existing holders will suffer a capital loss.

# This is the reason for negative bond yields in YTD 2021.

– Growing Commodity Prices:

Commodity prices are in a bullish trend for the past year. In the last 6 months, S&P GSCI (formerly the Goldman Sachs Commodity Index) rose by more than 30%. The below chart depicts the last one-year performance:

Though commodity prices and expected yields are not closely related, increased commodity prices will lead to inflation. To curb inflation, Central Banks then will be forced to increase the interest rates. Increased interest rates will lead to a decrease in the bond prices, the effect of the same is explained above.

– Investment in perpetual bonds:

Some of the mutual fund schemes (mainly long-term schemes) invest a portion of their funds in perpetual bonds. The coupon rate offered for these bonds is normally higher than normal bonds since they are very risky. As the name suggests, issuing entity pays interest on bonds perpetually but has no obligation to repay principal.

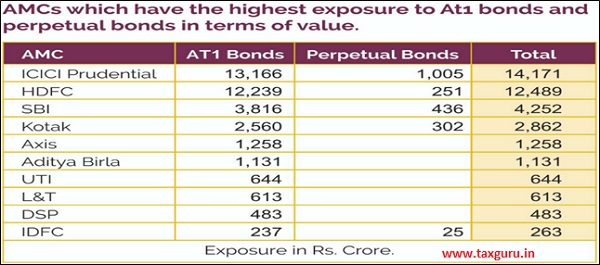

A popular category of bonds related to this category is AT-1 Bonds which are issued by banks to shore up its core capital base to comply with Basel-III norms. The risk with AT-1 bonds is that banks have a call option at the end of a specified period to buy them back (i.e., banks have an option to buy them back & not an obligation. Investors do not have any right to return the bonds to the bank and claim money) Understanding of key features of AT-1 bonds by all investors started after the Yes Bank writing off of Rs.8,415 Crore worth bonds.

SEBI has imposed has restricted holding of AT-1 bonds by Mutual Fund Schemes to 10%. But CRISIL has stated that 36 bonds across 13 fund houses have more than 10% exposure towards the same. Category wise break up of said funds is shown below:

Exposure to AT-1 bonds across various AMCs is summarized below:

– Risk of Side pocketing:

The term ‘Side Pocketing’ refers to the creation of a separate portfolio in lieu of troubled debt. Said troubled debt will be written down to zero and existing investors will get the benefit of participating in recovery proceeds of said troubled debt whereas fresh investors will not.

The term ‘Side Pocketing’ gained popularity when Franklin Templeton has written off investments worth Rs.2,074 Crore that it has made in Vodafone Idea through 6 funds owing SC verdict over AGR dues and degrading of its investments to below investment category (i.e., below BBB grade). FT has segregated those investments to another portfolio whereby existing investors will get recoveries from the same even after redeeming their investments in the main portfolio.

– Decrease in Credit Risk making investments illiquid:

Sovereign/AAA/AA+ rated (A+ for short-term instruments) are regularly traded in the market with good volume. Hence above instruments can be termed liquid instruments. Whenever an instrument’s rating is dropped to lower than the above ratings, it becomes a tough job for the MF entity to find a potential buyer for the same.

In this scenario of Covid outbreak and business slowdown, investing in credit mutual funds may turn risky and careful examination of the fund, underlying companies need to be ensured to avoid major capital loss.

As explained above, if the rating falls below BBB (investment category), writing off of the same needs to be done by the entity.

Conclusion:

This article does not discriminate/discourages investment in the debt market but it summarizes some key risks in this market that everyone should be aware of. Many fund managers advised investors to invest with short to medium time horizons and lower their expectations from the market. There are 17 types of funds in the debt mutual fund market based on duration and risk. One can plan for investing in funds after considering the above parameters.