“Wealth, the lamp unfailing, speeds to every land,

Dispersing darkness at its lord’s command.” –

Thirukural, Chapter 76, verse 753.

“Make money – there is no weapon sharper than it

to sever the pride of your foes.”

– Thirukural, Chapter 76, verse 759.

For more than three-fourths of known economic history, India has been the dominant economic power globally. Such dominance manifested by design. During much of India’s economic dominance, the economy relied on the invisible hand of the market for wealth creation with the support of the hand of trust. Specifically, the invisible hand of markets, as reflected in openness in economic transactions, was combined with the hand of trust by appealing to ethical and philosophical dimensions.

The Survey shows that contemporary evidence following the liberalization of the Indian economy support the economic model advocated in our traditional thinking. The exponential rise in India’s GDP and GDP per capita post liberalisation coincides with wealth generation in the stock market. Similarly, the evidence across various sectors of the economy illustrates the enormous benefits that accrue from enabling the invisible hand of the market. Indeed, the Survey shows clearly that sectors that were liberalized grew significantly faster than those that remain closed. The events in the financial sector during 2011-13 and the consequences that followed from the same illustrate the second pillar – the need for the hand of trust to support the invisible hand.

The Survey posits that India’s aspiration to become a $5 trillion economy depends critically on strengthening the invisible hand of markets together with the hand of trust that can support markets. The invisible hand needs to be strengthened by promoting pro-business policies to (i) provide equal opportunities for new entrants, enable fair competition and ease doing business, (ii) eliminate policies that undermine markets through government intervention even where it is not necessary, (iii) enable trade for job creation, and (iv) efficiently scale up the banking sector to be proportionate to the size of the Indian economy. Introducing the idea of “trust as a public good that gets enhanced with greater use”, the Survey suggests that policies must empower transparency and effective

enforcement using data and technology to enhance this public good.

IMPORTANCE OF WEALTH CREATION

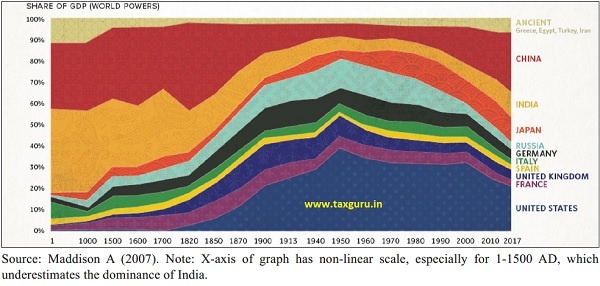

1.1 For more than three-fourths of known economic history, India has been the dominant economic power globally (Maddison, 2007). The country has historically been a major wealth creator and a significant contributor to world’s GDP as shown in Figure 1.

Figure 1: Global contribution to world’s GDP by major economies from 1 AD to 2003 AD

1.2 Economic dominance over such long periods manifests by design, and not by mere chance. In this context, the Survey notes that our age-old traditions have always commended wealth creation. While Kautilya’s Arthashastra is given as a canonical example, wealth creation as a worthy human pursuit is recognised by other traditional literature as well. The Thirukural, a treatise on enriching human life written in the form of couplets by Tamil saint and philosopher Thiruvalluvar, asserts in verses 753 of Chapter 76: “Wealth, the lamp unfailing, speeds to every land; Dispersing darkness at its lord’s command.” In verse 759 of the same chapter, which forms the second part of the Thirukural called Porul Paal or the essence of material wealth, Thiruvalluvar, declares: “Make money – there is no weapon sharper than it to sever the pride of your foes.” Needless to say, Thirukural advocates wealth creation through ethical means – an aspect that is discussed later in this chapter. Verse 754 in the same chapter avows: “(Wealth) yields righteousness and joy, the wealth acquired capably without causing any harm.”

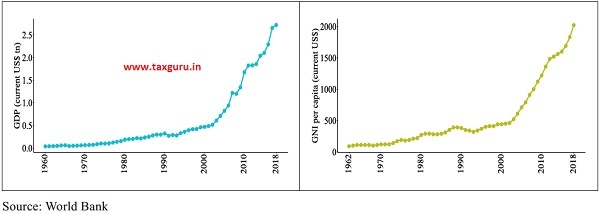

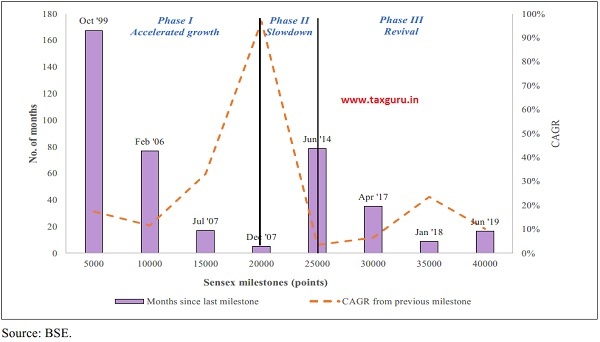

1.3 Despite such a “rich” tradition of emphasizing wealth creation, India deviated from this model for several decades after independence. However, India returned back to these roots post economic liberalisation in 1991. The exponential rise in India’s GDP and GDP (Figure 2a) per capita (Figure 2b) post liberalisation coincides with wealth generation in the stock market (Figure 3). Sensex has not only grown after 1991, but has grown at an accelerating pace. Whereas crossing the first incremental 5000 points took over 13 years from its inception in 1986, the time taken to achieve each incremental milestone has substantially reduced over the years. Note that the acceleration in the Sensex was not due to the base effect. In fact, the higher acceleration stemmed from higher cumulative annual growth rate (CAGR).

Figure 2a: India’s GDP (current US$ tn) Figure 2b: India’s GDP per capita

(1960-2018) (current US$) (1960-2018)

Figure 3: Incremental months taken for Sensex to cross each 5000-point milestone

Note: Time to cross each milestone is defined as the time elapsed between the first time the Sensex closed at the previous milestone and the first time it closed at the present milestone. Note that milestones are based on closing prices. Time elapsed is recorded as number of calendar days and converted to months assuming 30 days a month.

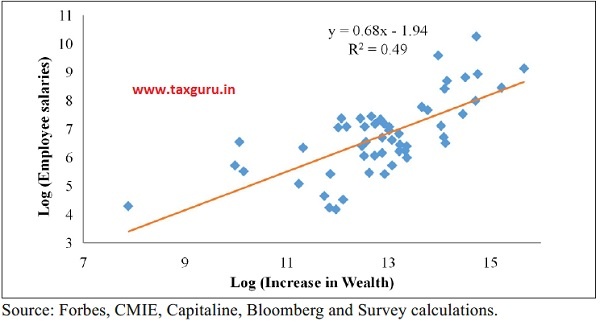

1.4 Yet, given India’s “tryst” with socialism, it is essential to emphasise its benefits in today’s milieu. To understand the benefits from wealth creation, we collate the companies created by top 100 wealthy entrepreneurs in the country as estimated by Forbes in March 2019. After excluding those with tainted wealth by applying several filters, we correlate the increase in the entrepreneur’s wealth over a decade (31-Mar-2009 to 31-Mar-2019) with the benefits that accrued to several other stakeholders including employees, suppliers, government, etc. Figure 4 shows that the wealth created by an entrepreneur correlates strongly with benefits that accrue to the employees working with the entrepreneur’s firms.

Figure 4: Wealth Creation and Salaries paid to Employees

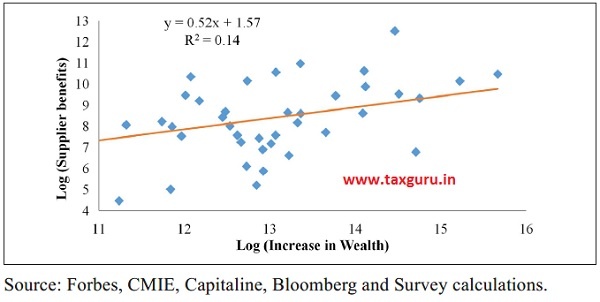

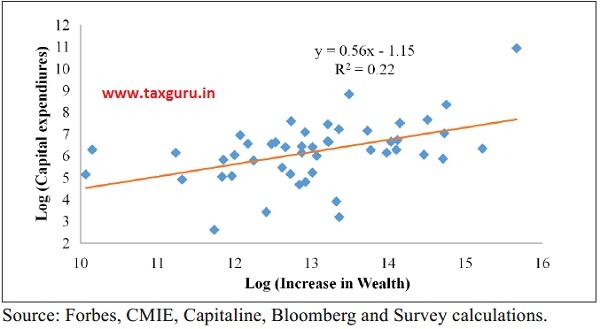

1.5 Figure 5 shows that the wealth created by an entrepreneur correlates strongly with raw materials procured by the entrepreneur’s firms, which proxies the benefits that suppliers reap by supplying raw materials to the entrepreneur’s firms. Similarly, Figure 6 shows that the wealth created by an entrepreneur correlates strongly with the capital expenditures made by the entrepreneur’s firms, which proxies the benefits that manufacturers of capital equipment reap by supplying such equipment to the entrepreneur’s firms.

Figure 5: Wealth Creation and Benefits reaped by Suppliers

Figure 6: Wealth Creation and Capital Expenditures

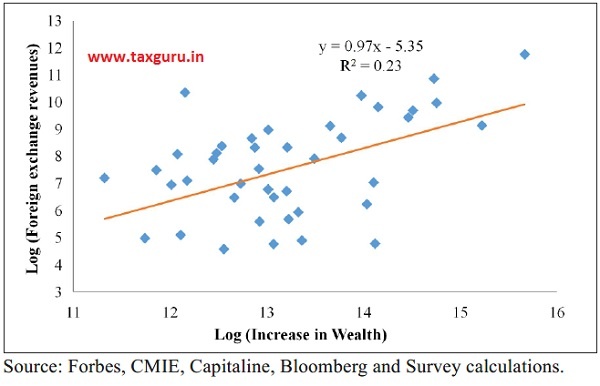

1.6 Revenues earned in foreign exchange enable macroeconomic stability by enabling the country to pay for its imports and keeping the current account deficit at manageable levels. Figure 7 shows that the wealth creation by entrepreneurs correlates strongly with the foreign exchange revenues earned by the entrepreneurs’ firms.

Figure 7: Wealth Creation and Foreign Exchange Revenues

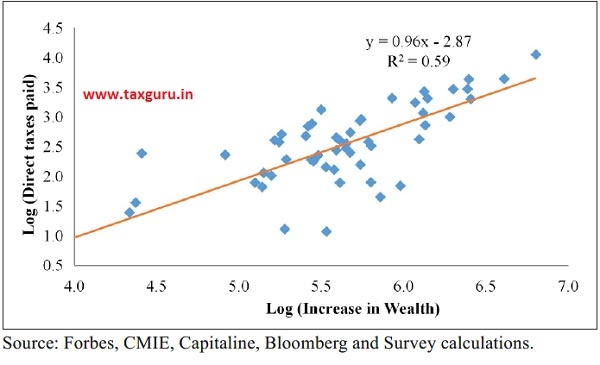

1.7 Finally, Figure 8 shows that the wealth created by an entrepreneur helps the country’s common citizens. Tax revenues enable Government spending on creating public goods and providing welfare benefits to the citizens. We correlate the wealth created by the entrepreneur with the direct taxes paid. Clearly, direct taxes underestimate the benefits accruing to the Government because it does not include the indirect taxes paid by the entrepreneur’s firms, the direct taxes paid by the employees or the suppliers. Yet, as a proxy for the benefits accruing to the citizens through spending of tax revenues by the Government, this figure captures the benefits accruing to the country’s common citizens. Therefore, the strong correlation of wealth creation by entrepreneurs to the taxes paid represents another important benefit to society from wealth creation.

Figure 8: Wealth Creation and Direct Tax Inflows

WEALTH CREATION THROUGH THE INVISIBLE HAND OF MARKETS

1.8 Wealth creation happens in an economy when the right policy choices are pursued. For instance, wealth creation and economic development in several advanced economies has been guided by Adam Smith’s philosophy of the invisible hand. Despite the dalliance with socialism – four decades is but an ephemeral period in a history of millennia – India has embraced the market model that represents our traditional legacy. However, scepticism about the benefits accruing from a market economy still persists. This is not an accident as our tryst with socialism for several decades’ makes most Indians believe that Indian economic thought conflicts with an economic model relying on the invisible hand of the market economy. However, this belief is far from the truth.

1.9 In fact, our traditional economic thinking has always emphasized enabling markets and eliminating obstacles to economic activity. As far as half-a-century back, Spengler (1971) wrote that Kautilya postulated the role of prices in an economy. Kautilya (p. 149) averred, “The root of wealth is economic activity and lack of it brings material distress. In the absence of fruitful economic activity, both current prosperity and future growth are in danger of destruction. A king can achieve the desired objectives and abundance of riches by undertaking productive economic activity (1.19)”. Kautilya advocates economic freedom by asking the King to “remove all obstructions to economic activity” (Sihag, 2016).

1.10 A key contributor to ancient India’s prosperity was internal and external trade. Two major highways Uttarapatha (the Northern Road) and Dakshinapatha (the Southern Road) and its subsidiary roads connected the sub-continent. Meanwhile, ports along India’s long coastline traded with Egypt, Rome, Greece, Persia and the Arabs to the west, and with China, Japan and South East Asia to the east (Sanyal, 2016). Much of this trade was carried out by large corporatized guilds akin to today’s multinationals and were funded by temple-banks. Thus, commerce and the pursuit of prosperity is an intrinsic part of Indian civilizational ethos.

1.11 Much before the time period that Maddison (2007) analyses, a stakeholders-model existed in India as is discernible in Arthashastra in which entrepreneurs, workers and consumers share prosperity (Deodhar, 2018). Arthashastra as a treatise on economic policy was deeply influential in the functioning of the economy until the 12th century (Olivelle, 2013). During much of India’s economic dominance, the economy relied on the invisible hand of the market.

1.12 As wealth creation happens by design, the overarching theme of Economic survey 2019-20 is wealth creation and the policy choices that enable the same. At its core, policies seek to maximize social welfare under a set of resource constraints. Resource constraints force policymakers to focus on efficiency, which more output to be produced from given resources such as land, human resources and capital, or, the same output for less resource use.

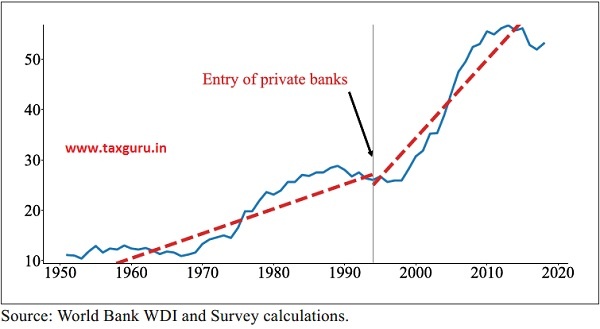

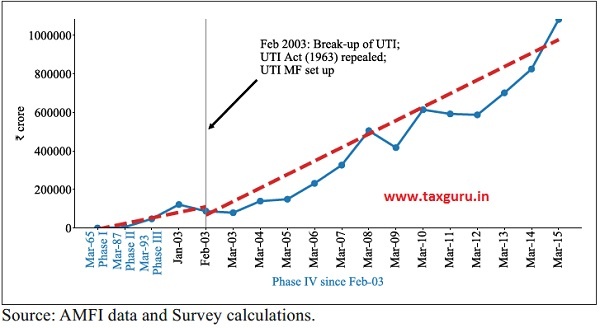

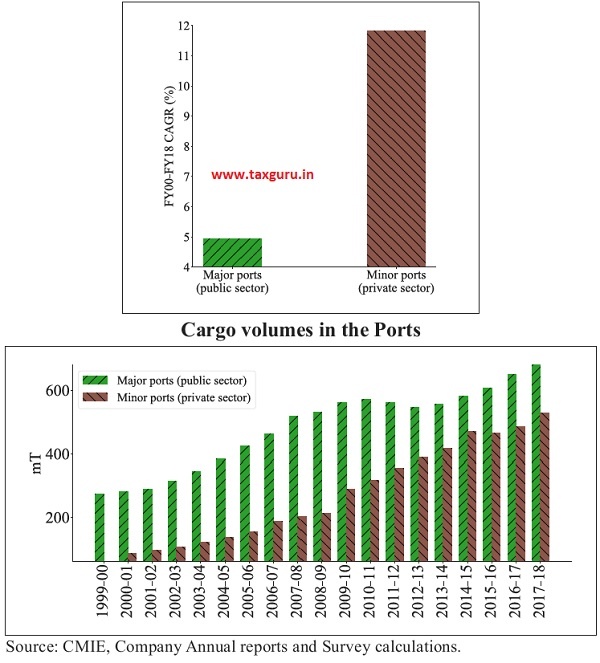

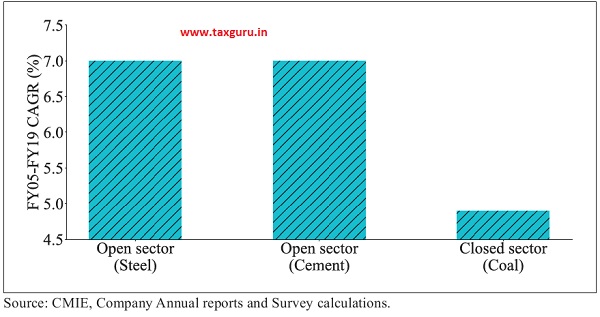

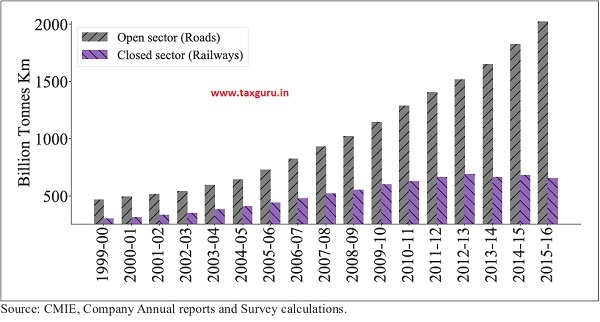

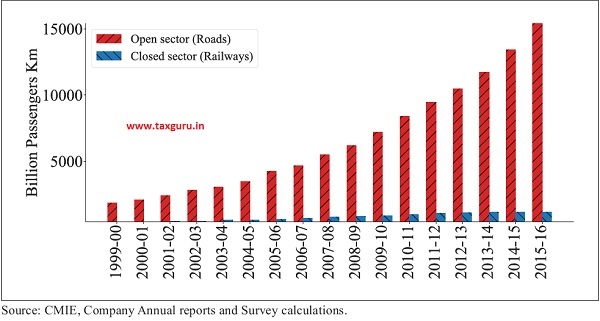

1.13 The evidence since 1991 shows that enabling the invisible hand of markets, i.e., increasing economic openness, has a huge impact in enhancing wealth both in the aggregate and within sectors. Indeed, the evidence presented below shows clearly that sectors that were liberalized grew significantly faster than those that remain closed. This is not surprising as the market economy is based on the principle that optimal allocation of resources occurs when citizens are able to exercise free choice in the products or services they want. Figure 9 shows how credit in the banking sector expanded at much higher rates after the sector was opened for competition through licenses granted to private sector banks. As competition expanded the banking choices available to citizens, the sector experienced strong growth. Figure 10 shows a similar effect in the mutual funds sector following its opening up to competition in 2003. In Figures 11-14, we examine growth in an open sector, which is defined as one where citizens can choose among many different producers, vis-à-vis a closed sector, where the citizen cannot exercise this choice. Figure 11 shows the growth in the cargo volumes in an open sector (small ports) versus a closed sector (large ports). Figure 12 shows the same for open sectors such as cement and steel versus a closed sector such as coal. Figures 13 and 14 show the growth in freight and passenger traffic in an open sector (roads) when compared to a closed sector (railways). Across Figures 11-14, we see that growth has been significantly greater in the open sector than in the closed sector. Figures 9-14 thus highlight the positive impact of enabling economic choice for citizens in the economy.

Figure 9: Increase in domestic credit to GDP after entry of private sector banks

Figure 10: Growth in mutual funds sector after opening up in 2003

Figure 11: Growth in the ports sector: open (minor ports) versus closed (major ports) Cumulative Annual Growth rates

Figure 12: Annual growth rates in open sectors (steel and cement) versus closed sector (coal)

Figure 13: Growth in freight traffic across open sector (roads) and closed sector (railways)

Figure 14: Growth in passenger traffic across open sector (roads) and closed sector (railways)

THE INSTRUMENTS FOR WEALTH CREATION

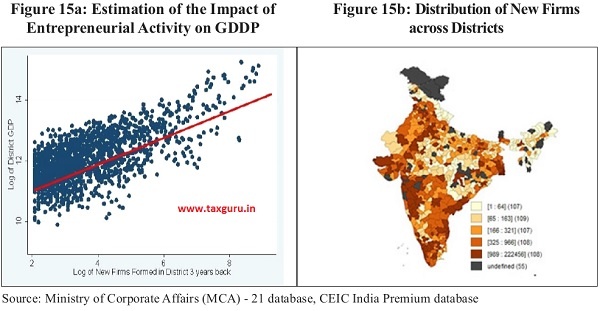

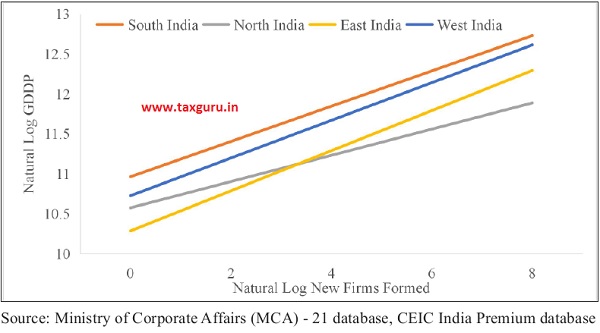

1.14 As argued above, enhancing efficiency is crucial for wealth creation. A key dimension of efficiency pertains to opportunity. Equal opportunity for new entrants is important because, as the survey shows in Chapter 2 (Entrepreneurship and Wealth Creation at the grassroots), a 10 per cent increase in new firms in a district yields a 1.8 per cent increase in Gross Domestic District Product (GDDP). This effect manifests consistently both across districts as shown in Figure 15a and across regions as shown in Figure 16. This impact of new firm creation on district-level GDP demonstrates that grassroots entrepreneurship is not just driven by necessity. Figure 15b, in fact, clearly demonstrates that, though the peninsular states dominate entry of new firms, enterpreneurship is dispersed across India and is not restricted just to a few metropolitan cities. The chapter shows using data from World Bank’s enterpreneurship data that new firm creation has gone up dramatically since 2014. While the number of new firms grew at a cumulative annual growth rate of 3.8 per cent from 2006-2014, the growth rate from 2014 to 2018 has been 12.2 per cent. As a result, from about 70,000 new firms created in 2014, the number has grown by about 80 per cent to about 1,24,000 new firms in 2018. Equal opportunity for new entrants in entrepreneurship enables efficient resource

Figure 16: Impact across regions of new firm creation on District level GDP after 3 years

allocation and utilization, facilitates job growth, promotes trade growth and consumer surplus through greater product variety, and increases the overall boundaries of economic activity.

1.15 A key dimension of opportunity pertains to that between new entrants and incumbents. While incumbents are likely to be powerful, influential, and have a voice that is heard in the corridors of power, new entrants are unlikely to possess these advantages. Yet, new entrants bring path-breaking ideas and innovation that not only help the economy directly but also indirectly by keeping the incumbents on their toes. Therefore, the vibrancy of economic opportunities is defined by the extent to which the economy enables fair competition, which corresponds to a “pro-business” economy. This is in contrast to the influence of incumbents in extracting rents from their incumbency and proximity to the corridors of power, which corresponds to “pro-crony” economy. It is crucial in this taxonomy to relate the term “pro-business” to correspond to an economy that enables fair competition for every economic participant. Given this backdrop, do new entrants have equal opportunity of wealth creation as the incumbents? Chapter 3 (Pro-business versus pro-crony) presents evidence on how efficient the Indian economy has been in terms of opportunity for new entrants against established players for wealth creation. Economic events since 1991 provide powerful evidence that supports providing equal opportunity for new entrants to unleash the power of competitive markets to generate wealth. India’s aspiration to become a $5 trillion economy depends critically on promoting pro-business policies that provide equal opportunities for new entrants. The Survey makes the case that the churn create by a healthy pro-business system generates greater wealth than a static pro-crony system. Note that the Survey contrasts two systems; the arguments are not directed at any individual or entity.

1.16 Greater wealth creation in a market economy enhances welfare for all citizens. Chapter 3 of the Survey presents evidence of wealth creation in the economy post-liberalisation. For instance, the Sensex reached the 5,000 mark for the first time in 1999 from its base of 100 points in 1978. It was less than 1,000 points in early 1991 when India moved to a market economy from a command economy. Since then, the market capitalization based index has seen unprecedented growth as shown in Figure 3. This unprecedented growth after 1999 can be divided into three phases. Phase I from 1999 to 2007 saw acceleration in the growth of the Sensex, with each successive 5000-point mark taking lesser and lesser time to achieve. Phase II from 2007 to 2014 saw a slowdown in the index’s growth. Phase III began in 2014 and saw a revival in response to structural reforms. Strikingly, in this phase, the Sensex jumped from the 30,000 mark to the 40,000 mark in just two years. As the CAGR shown in Figure 3 depict clearly, the acceleration in the Sensex was not due to the base effect. In fact, the higher acceleration stemmed from higher CAGR. Thus, there has been unprecedented wealth creation in the economy since 1991.

1.17 The freedom to choose is best expressed in an economy through the market where buyers and sellers come together and strike a bargain via a price mechanism. Where scarcity prevails and choice between one use of scarce resources and another must be made, the market offers the best mechanism to resolve the choice among competing opportunities. This principle is fundamental to a market economy. The command and control approach contends that the price of a good should be regulated. Our economy still has some of the regulatory relics of the pre-liberalisation era. The survey provides evidence in Chapter 4 (Undermining Markets: When Government Intervention Hurts More Than It Helps) that government intervention hurts more than it helps in the efficient functioning of markets. For instance, in the pharmaceutical industry, government regulated formulation prices increase more than unregulated formulations. Moreover, the supply of unregulated formulations is more than that of regulated formulations. Government interventions often times lead to unintended consequences such as price increases, when compared to markets that are unregulated. Unlike in command economies where prices are determined by the government, in a market economy, price of a good is determined by the interaction of the forces of supply and demand. The survey finds that unshackling the economic freedom for markets augments wealth creation.

1.18 Yet another dimension of efficiency concerns allocation of resources to ensure their optimal use. Since resources are limited, a nation has to make choices. For example, given its demographic dividend, should India focus on labour-intensive industries or on capital intensive industries? Chapter 5 (Creating Jobs and Growth by Specializing to Exports in Network Products) answers this question to lay out a clear-headed strategy for creating crores of jobs through our export policies. The survey finds that by integrating “Assemble in India for the world” into Make in India, India can create 4 crore well-paid jobs by 2025 and 8 crore by 2030. Our trade policy must be an enabler because growth in exports provides a much-needed pathway for job creation in India.

1.19 As discussed in Chapter 6 (Improving Ease of Doing Business in India), the ease of doing business has increased substantially in the last five years from reforms that provided greater economic freedom. India made a substantial leap forward in The World Bank’s Doing Business rankings from 142 in 2014 to 63 in 2019. The Doing Business 2020 report has recognized India as one of the ten economies that have improved the most.

1.20 Yet, the pace of reforms in enabling ease of doing business need to be enhanced so that India can be ranked within the top 50 economies on this metric. India continues to trail in parameters such as Ease of Starting Business, Registering Property, Paying Taxes, and Enforcing Contracts. Chapter 6 identifies the most crucial issues plaguing India’s performance beyond the approach taken by the World Bank’s surveys. It also demonstrates the specific points in the supply-chain of exports and imports that experience inordinate delays and blockages. Although, the Authorized Economic Operators Scheme has smoothed the process for registered electronics exporters/importers, much more needs to be done. A holistic assessment and a sustained effort to ease business regulations and provide an environment for businesses to flourish would be a key structural reform that would enable India to grow at a sustained rate of 8-10 per cent per annum. This requires a nuts-and-bolts approach of feedback loops, monitoring and continuous adjustment.

1.21 An efficient financial sector is extremely crucial for enhancing efficiency in the economy. Historically, in the last 50 years, the top-five economies have always been ably supported by their banks. The support of the U.S. Banking system in making the U.S. an economic superpower is well documented. Similarly, in the eighties during the heydays of the Japanese economy, Japan had 15 of the top 25 largest banks then. In recent times, as China has emerged as an economic superpower, it has been ably supported by its banks—the top four largest banks globally are all Chinese banks. The largest bank in the world—Industrial and Commercial Bank of China—is nearly two times as big as the 5th or 6th largest bank, which are Japanese and American banks respectively.

1.22 Chapter 7 (Golden Jubilee of Bank Nationalisation: Taking Stock) shows that India’s banking sector is disproportionately under-developed given the size of its economy. For instance, India has only one bank in the global top 100 – same as countries that are a fraction of its size: Finland (about 1/11th), Denmark (1/8th), Norway (1/7th), Austria (about 1/7th), and Belgium (about 1/6th). Countries like Sweden (1/6th) and Singapore (1/8th) have thrice the number of global banks as India. A large economy needs an efficient banking sector to support its growth. As PSBs account for 70 per cent of the market share in Indian banking, the onus of supporting the Indian economy and fostering its economic development falls on them. Yet, on every performance parameter, PSBs are inefficient compared to their peer groups. The chapter suggests some solutions that can make PSBs more efficient so that they are able to adeptly support the nation in creating wealth commensurate with a $5 trillion economy.

1.23 The shadow banking sector, which has grown significantly in India, accounts for a significant proportion of financial intermediation especially in those segments where the traditional banking sector is unable to penetrate. Chapter 8 (Financial Fragility in the NBFC Sector) constructs a diagnostic to track the health of the shadow banking sector and thereby monitor systemic risk in the financial sector.

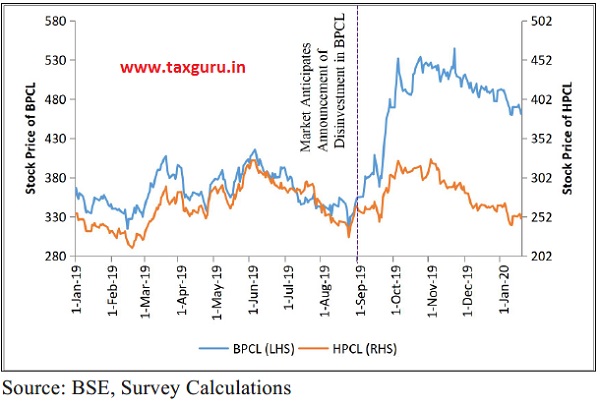

1.24 Chapter 9 (Privatization and Wealth Creation) uses the change in performance of Central Public Sector Enterprises (CPSEs) after privatization to show the significant efficiency gains that are obtained when the private sector runs businesses instead of the government. Figure 17 provides a compelling illustration using the announcement of the privatisation of Bharat Petroleum Corporation Limited (BPCL) by comparing to its peer Hindustan Petroleum Corporation Limited (HPCL). We focus on the difference in BPCL and HPCL prices from September 2019 onwards when the first news of BPCL’s privatization appeared.1 The comparison of BPCL with HPCL ensures that the effect of any broad movements in the stock market or in the oil industry is netted out. We note in Figure 17 that the stock prices of HPCL and BPCL moved synchronously till September. However, the divergence in their stock prices started post the announcement of BPCL’s disinvestment. The increase in the stock price of BPCL when compared to the change in the price of HPCL over the same period translates into an increase in the value of shareholders’

Figure 17: Comparison of Stock Prices of BPCL and HPCL

equity of BPCL of around ` 33,000 crore. As there was no reported change in the values of other stakeholders, including employees and lenders, during this time, the ` 33,000 crore increase translates into an unambiguous increase in the BPCL’s overall firm value, and thereby an increase in national wealth by the same amount.

1.25 The analysis in this chapter reveals that key financial indicators such as net worth, net profit and return on assets of the privatized CPSEs, on an average, have increased significantly in the post-privatization period compared to the peer firms. This improved performance holds true for each CPSE taken individually as well.

1.26 The ultimate measure of wealth in a country is the GDP of the country. As investors deciding to invest in an economy care for the country’s GDP growth, uncertainty about its magnitude can affect investment. Therefore, the recent debate about India’s GDP growth rates following the revision in India’s GDP estimation methodology in 2011 assumes significance, especially given the recent slowdown in the growth rate. Using careful statistical and econometric analysis that does justice to the importance of this issue, Chapter 10 (Is India’s GDP Growth Rate Overstated? No!) finds no evidence of misestimation of India’s GDP growth. Consistent with the hand of trust supporting the invisible hand, the Survey provides careful evidence that India’s GDP growth estimates can be trusted.

1.27 Wealth creation in the economy must ultimately enhance the livelihood of the common person by providing him/her greater purchasing power to buy goods and services. A plate of nutritious food for the common man – a Thali – is a basic item that every person encounters every day. Therefore, there cannot be a better way to communicate whether or not economic policies make the common man better off than quantifying what he/she pays for a Thali every day. Chapter 11 (Thalinomics: The Economics of a Plate of Food in India) constructs an index of Thali prices across around 80 centres in 25 States/UTs in India from April 2006 to March 2019. The survey presents evidence in using an elementary indicator of price stability—a Thali— that a nourishing plate of food has become more affordable for a common man now.

1.28 This chapter aims to relate economics to the common person. Through the chapter on the “Behavioural Economics of Nudge”, the Economic Survey 2018-19 made a humble attempt to understand humans as humans, not self-interested automatons, so that the common person can relate to his/her idiosyncrasies and use that easy prism to understand behavioural change as an instrument of economic policy. The Economic Survey 2019-20 continue this modest endeavour of relating economics to the common person using something that he or she encounters every day – a plate of food.

THE BREAKDOWN OF TRUST IN THE EARLY YEARS OF THIS MILLENNIUM

1.29 In a market economy too, there is need for state to ensure a moral hand to support the invisible hand. As Sandel (2012) argues, markets are liable to debase ethics in the pursuit of profits at all cost. Trust contributes positively to access of both formal and informal financing (Guiso et al., 2004). Ancient philosophers consider trust as an important element in a society and postulated2 that trust can be furthered by appealing to ethical and philosophical dimensions. Along these lines, the Survey introduces “trust as a public good that gets enhanced with greater use” (see Box 1). As Box 1 explains, philosophers such as Aristotle and Confucius (implicitly) viewed trust as a public good by explaining that “good laws make good citizens.”

1.30 In the contemporary context, Zingales (2011) and Sapienza and Zingales (2012) highlight that the Global Financial Crisis represented a glaring instance of the failure of trust in a market economy. Closer home, the events around 2011 paint a similar picture.

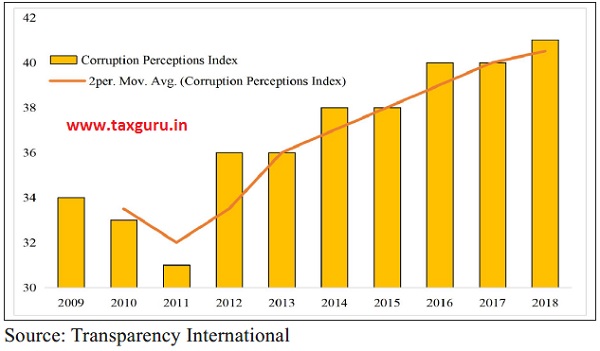

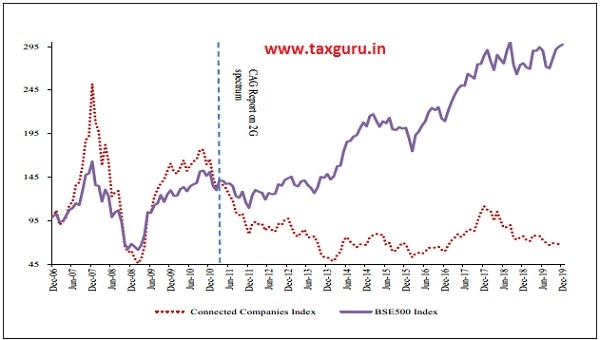

1.31 The corruption perception index, which Transparency International tracks across countries, shows India at its lowest point in recent years in 2011. Since 2013, India has improved significantly on this index (Figure 18). The phenomenon of trust deficit that developed in India during this period is also reflected in many other measures. As the survey shows in Chapter 4, prior to 2011, cronyism paid a firm and its shareholders. The index of “connected” firms – as defined and constructed by Ambit Capital consistently outperformed the BSE 500 index as shown in Figure 19. “Connected” firms however have consistantly underperformed the BSE 500 index post 2011. Chapter 3 also demonstrates how the discretionary allocation of natural resources before 2014 led to rent seeking by beneficiaries. In contrast, the competitive auction of natural resources after 2014 eliminated opportunities for such rent seeking.

Figure 18: Corruption Perceptions Index for India (low score = higher perceived corruption)

Figure 19: Investor wealth generated by “connected” firms before and after 2011

Source: Ambit Capital research, Capitaline, BSE

Note: 1) The connected companies index is an aggregate market cap index which has been rebased and is adjusted for demergers, 2) 70 companies with political dependence and connectivity as on Dec’06 as per Ambit analysts.

Box 1: Trust as a public good: Aristotle and Kautilya vs. Machiavelli

The Survey introduces the idea of “trust as a public good that gets enhanced with greater use”. Trust can be conceptualized as a public good with the characteristics of non-excludability i.e., the citizens can enjoy its benefits at no explicit financial cost. Trust also has the characteristics of non-rival consumption i.e., the marginal cost of supplying this public good to an extra citizen is zero. It is also non-rejectable i.e., collective supply for all citizens means that it cannot be rejected. Unlike other public goods, trust grows with repeated use and therefore takes time to build (Gambetta, 1998). Lack of trust represents an externality where decision makers are not responsible for some of the consequences of their actions.

Given the importance of trust in an economy, one might reasonably expect economic theory to address it, especially in the literature on transaction cost economics or incomplete contracts. However, this is not the case. Nobel laureate Oliver Williamson who specializes in transaction cost economics plainly states that there is no such thing as trust within economic activity: ‘It is redundant at best and can be misleading to use the term “trust” to describe commercial exchange for which cost-effective safeguards have been devised in support of more efficient exchange. Calculative trust is a contradiction in terms’ (Williamson, 1993, p. 463). Williamson does concede that there is a role of calculative co-operation based on incentives and governance structures: ‘Machiavellian grabbing is not implied if economic agents have a more far-sighted understanding of the economic relations of which they are a part than myopic Machiavellianism ascribes to them’ (Williamson, 1993, p. 474). He argues that calculative cooperation is more likely when agents have longer time horizons, which is also true for trust.

Equally, one would expect trust to be addressed in the incomplete contracts literature. The incomplete contracting paradigm was pioneered by Nobel laureate Oliver Hart with his co-authors Sanford Grossman, and John Moore. They argue that contracts cannot specify what is to be done in every possible contingency. So, it is reasonable to expect trust as a concept to be addressed in such a paradigm because economic agents will only risk entering into incomplete contracts if they trust their counterparts to adapt to unexpected outcomes in a manner that respects a fair division of economic returns. However, while the incomplete contracting literature analyses self-enforcing implicit contracts where myopic behaviour, i.e. opportunism, is restricted by concern for calculative, yet long-term, interest of either party (Baker et al. 1998).

In contrast to the transaction cost or incomplete contracting paradigm, individuals not only have material needs but also needs of self-esteem and self-actualization (Maslow, 1943). This view of humans relates directly to Benabou and Tirole (2006)’s schema, where people take actions to signal to themselves who they are. People’s self-esteem needs could inter alia stem from their intrinsic motivation to be “trustworthy.”

This contrast between modern economic theory’s view of people as “knaves” derives from the view of humans that Machiavelli and Hume present. Hume (1964) for instance posits: “Every man ought to be supposed to be a knave and to have no other end, in all his actions, then in his private interest. By this interest we must govern him, and, by means of it, make him, notwithstanding his insatiable avarice and ambition, cooperate to public good.” Economic policy today largely proceeds according to Hume’s maxim.

Yet, Aristotle’s view is in stark contrast to that of Hume or Machiavelli. Aristotle holds that “good laws make good citizens,” by inculcating habits and social virtue. Confucius advices government that “Guide them with government orders, regulate them with penalties, and the people will seek to evade the law and be without shame. Guide them with virtue, regulate them with ritual, and they will have a sense of shame and become upright.” People become “upright” when guided by “virtue” and regulated by “ritual” rather than by orders and penalties.

Kautilya is often presented as the Machiavelli of India. This is derived from a partial reading of the Arthashastra based on selectively quoting sections on spies and internal/external security. The Arthashastra literally means “The Treatise on Wealth” and it extensively discusses issues ranging from urban governance to tax administration and commerce. The book explicitly presents its intellectual framework right in the beginning by stating that good governance is based on the following branches of knowledge: Varta (economic policy), Dandaneeti (law and enforcement), Anvikshiki (philosophical and ethical framework) and Trayi (cultural context). The importance of Anvikshiki in Kautilya’s writings is often ignored but is critical to understanding his worldview. Interestingly this mirrors Adam Smith who did not just advocate the “invisible hand” but equally the importance of “mutual sympathy” (i.e. trust). The same idea is reflected in the writings of Friedrich Hayek, who advocated not only economic freedom but also a set of general rules and social norms that applies evenly to everyone.

Aristotle’s, Confucius’ and Kautilya’s notions may seem quaint in a 21st century worshipping self-interested greed. Yet, the events leading to and following the Global Financial Crisis clearly demonstrate that the intrinsic motivation to be “trustworthy” can generate trust as a public good while the intrinsic motivation of uninhibited greed can debase the same public good of trust. For instance, see Zingales (2011) and Sapienza and Zingales (2012) for the view that the Global Financial Crisis represented a glaring instance of the failure of trust in a market economy.

Figure 20: Proportion of Corporate Loan in Indian Non-Food Credit

Loan defaults

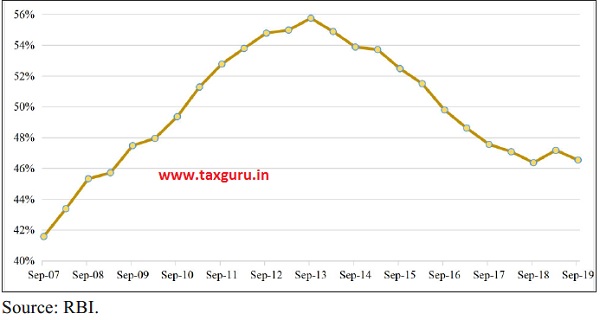

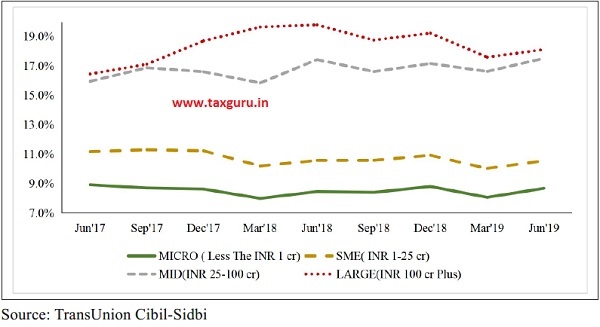

1.32 The Survey presents evidence in Chapter 3 of large corporations wilfully defaulting on their loans; further, such wilful defaults correlated with the use of related party transactions and the lack of disclosure on the same. This phenomenon of credit boom and bust manifested during the unprecedented and disproportionate growth in corporate credit between September 2007 and September 2013 as shown in Figure 20 and the subsequent decline following 2013. Figure 21 shows that the rates of default were the highest with larger loans (above `100 crores).

Audit failures

1.33 Just as farmers burning the stubble create negative externalities for all citizens through the contaminated air, when a corporate intentionally misreports financial information, it harms investors by creating

Figure 21: Non-Performing Asset (NPA) Rate by Size of the Loan

a negative externality of low trust for all domestic and international investors in the financials of firms in the economy. Lenders including other financial system intermediaries and economy at large suffer the negative externality created by the malpractices of a few.

1.34 Relatedly, when a corporate wilfully defaults on its loans, it harms its bank and creates negative externality to all other corporates as they get lesser supply of credit because of lack of trust. As can be seen from Figure 20, the proportion of corporate loans in non-food credit has fallen since September 2013 after showing a disproportionate increase for six years from September 2007. As discussed in the section on wilful defaulters in Chapter 3 of the Survey, due to the opportunistic behaviour of a few unscrupulous promoters, all other firms bear the cost through a higher credit spread stemming from the greater risk. The free-rider problem resulting in higher credit spread incentivises even more corporates to wilfully default on their loan obligations.

Figure 22: Accounting quality scores of large defaulters

Figure 23: Leading and Lagging Indicators disclosed in financial statements by large defaulters

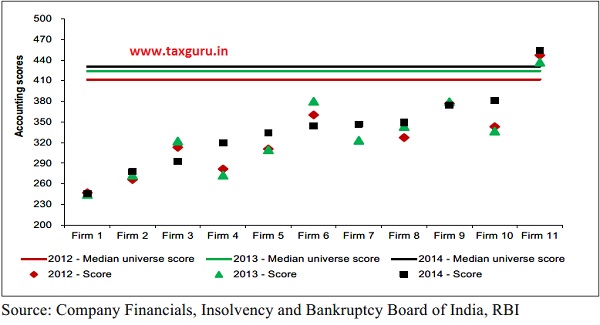

1.35 The common thread of opportunistic behaviour of a few unscrupulous promoters runs across both financial misreporting and wilful defaults. In June 2017, the Reserve Bank of India (RBI) identified twelve companies constituting 25 per cent of India’s total Non-Performing Assets (NPAs). As shown in Figure 22, the accounting quality of the large listed NPAs and a few wilful defaulters is much below the median accounting quality of other similar listed corporates in 2012, 2013 and 2014. Chapter 6 provides evidence that Public Sector Banks have a much greater proportion of NPAs as compared to New Private Sector Banks. In effect, wilful defaulters have siphoned off tax-payers money.

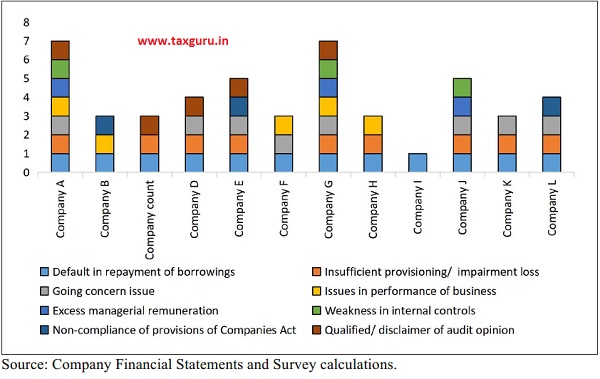

1.36 Similarly, there has been a market failure in the trust that auditors examine the accounting numbers of their clients reliably. The survey analysed the annual reports of the large listed NPAs and wilful defaulters to check if the auditors had purposely obfuscated material disclosures that are leading or lagging indicators of stress or impending default. These indicators should have been ideally flagged by the auditors. The leading indicators are shown in Table 1 and the lagging indicators in Table 2.

1.37 As can be seen from Figure 23, out of the twelve large defaulters, one of them had just one indicator disclosed with most others having three to four indicators disclosed of the eight leading and lagging indicators. Thus, a market failure of trust happened around 2011-13 due to a few large unscrupulous promoters. This created large Non-Performing Assets (NPAs) in the banking system, especially for Public Sector Banks (PSBs). The market failure of trust percolated to a couple of major Non-Banking Financial Companies (NBFCs). As investors in Liquid Debt Mutual Funds ran collectively to redeem their investments, it triggered panic across the entire gamut of NBFC-financiers, thereby causing a crisis in the NBFC sector. As mentioned above, Chapter 7 describes this phenomenon.

Table 1: Leading indicators of stress or impending default

| Leading Indicator | Description |

| Issues in performance of business |

|

| Weakness in internal controls |

|

| Non-compliance of provisions of Companies Act

|

|

| Qualified/Disclaimer of audit opinion |

|

| Excess managerial remuneration

|

|

Table 2: Lagging indicators of stress or impending default

| Lagging Indicator | Description |

| Default in repayment of borrowings |

|

| Insufficient provisioning/ impairment loss |

|

| Going concern issue |

|

Enabling Trust: Avoiding policies that crowd out intrinsic motivation

1.38 As in the case of the Global Financial Crisis, the events of 2011-13 and the consequences that have followed have created a trust deficit in the economy. This needs to be set right, even while acknowledging that trust takes time to rebuild. Our tradition celebrates wealth creators as auspicious elements of the economy. But, as Thiruvalluvar mentions clearly, it can happen only if wealth is made ethically.

“The just man’s wealth unwasting

shall endure,

And to his race a lasting joy ensure.”

– Thirukural, Chapter 12, verse 112.

1.39 Trust is the glue that has traditionally bound our economy and is an important ingredient in our recipe of economic well-being. Trust is a vital ingredient in the functioning of banking and financial markets as well. If there is high trust, economic activity can flourish despite the increased potential for opportunism. However, just because trust is functionally useful to an economy does not mean that it will necessarily arise. We need to identify the factors that underlie opportunistic behaviour and consider processes that facilitate trust creation since there has been a market failure of this public good around 2011-13 and the consequences that followed these events.

1.40 As Sandel (2012) postulates, good behaviour that stems purely from intrinsic motivation represents a crucial complement to the effective functioning of the market economy. In other words, the invisible hand of the market needs the supporting hand of trust. In this context, policy makers need to recognise that under-provisioning of public goods such as trust is often the result of lack of reward and recognition for good behaviour stemming purely from intrinsic motivation. When banks recognise corporates who pay their interest and principal in time in non-monetary ways, this enables the intrinsic motivation to get strengthened. Such gestures should not be accompanied by economic incentives such as greater credit limits or reduction in interest for award winners, otherwise the award-winning behaviour in the short-term may be perceived as ingratiation for better future credit availability i.e., future economic gains.

Reducing Information Asymmetry

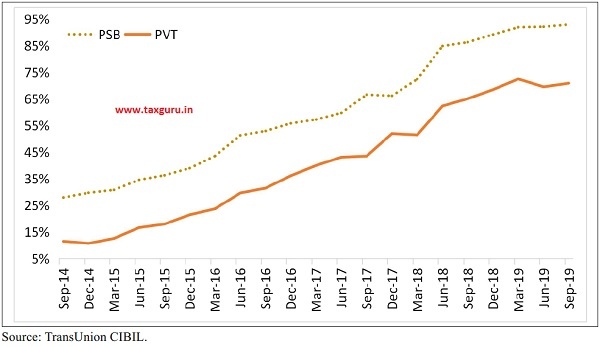

1.41 An important factorthatincreases the potential for opportunism in any economic exchange is information asymmetry. Such opportunism can be remedied increasingly through standardising enforcement systems and public databases. For instance, in the case of wilful defaults pre-2014, inability to access relevant borrower data was a key driver of information asymmetry. This aspect of access of credit information for corporate borrowers has improved considerably in the last five years. It can be argued that if the Indian economy had the data infrastructure such as CRILC (Central Repository of Information on large Corporates) during the in pre-2014 credit boom, the extent of systemic NPAs may have been lower. This information would have alerted lenders to limit exposures to corporates who have been tagged as NPA by another bank or NBFC. This information availability would have reduced NPAs in the entire banking system considerably because when a borrower defaults with one lender, other lenders can contractually tag their loan too as a default and therefore recall the loan. This is possible because all corporate loan documents have cross-default clauses. This would have limited incremental exposure of other banks who were not aware that at least one other financial institution had tagged a loan as an NPA. Such public databases remove information asymmetry considerably.

1.42 Figure 24 shows that the information sharing among lenders on NPAs was minimal as of 2014. While this information sharing was better among PSBs than NPBs, about a quarter of accounts that were declared as NPAs by other banks were classified as NPA in the bank’s account. This proportion has increased dramatically to reach 95 per cent in just a few years. This has decreased the potential for opportunism and should enable greater trust in lending activities of financial institutions.

1.43 A related issue is the tagging of default as wilful or genuine. In the banking sector, informational availability issues has been solved by shared databases and attribution problems between distressed defaulters and wilful defaulters have been solved by making the list of wilful defaulters public. Such naming and shaming of wilful defaulters has made such offenders subject to economic sanction in the form of downright unavailability of credit from the banking sector.

Enhancing quality of supervision

1.44 The government needs to support the hand of trust by being a good referee of the economy. The referee’s job is to not just report but also detect opportunistic behaviour if people are not playing by the rules. Like wilful defaults, malpractices such as financial mis-reporting and market manipulation needs to be detected early because these are termites that eat away investor’s faith in financial markets, diminishes portfolio investments and crowd-out important national investments.

It scares away scrupulous and law-abiding market participants. It is a scourge that drives away investments and therefore jobs in the economy. To fittingly celebrate wealth creators who make wealth ethically, it is of utmost importance that our financial markets are fair and transparent. In this, the state’s role as a competent referee cannot be overemphasized.

1.45 The U.S. Federal Trade Commission has one employee for every two listed firms, while the Competition Commission of India has one employee for every 38 listed firms. Securities and Exchange Commission (SEC) has almost one employee for each listed company. In contrast, SEBI has one employee for six listed companies. In fact, in key divisions such as Corporate Finance, SEC has more than fifteen times as many employees as SEBI. This resource deficit needs to be reduced to strengthen government’s role as a referee to ensure fair-play for all wealth creators.

1.46 SEC and FTC extensively use Artificial Intelligence and Machine Learning to track and flag market malpractices while none of our regulators do so. As a result of the limited resources at the regulators’ disposal, supervision of the market economy suffers badly thereby encouraging market malpractices. The economy cannot achieve the ambitious $5 trillion mark as long as it is plagued by market malpractices and suboptimal supervision. Therefore, significant enhancement in the quantity and quality of manpower in our regulators (CCI, RBI, SEBI, IBBI) together with significant investments in technology and analytics needs to be made. This would enhance the effectiveness of the hand of trust in supporting the invisible hand for greater wealth creation.

Figure 24: Proportion of Lenders Tagging an already tagged NPA (by Another Bank) as NPA in their books.

CHAPTER AT A GLANCE

> For more than three-fourths of known economic history, India has been the dominant economic power globally. Such dominance manifests by design; not happenstance. During much of India’s economic dominance, the economy relied on the invisible hand of the market for wealth creation with the support of the hand of trust. Specifically, the invisible hand of markets, as reflected in openness in economic transactions, was combined with the hand of trust that fostered intrinsic motivation by appealing to ethical and philosophical dimensions. As far as half-a-century back, Spengler (1971) reflected this fact by asserting that Kautilya’s Arthashastra postulates the role of prices in an economy.

> The Survey shows that contemporary evidence following the liberalization of the Indian economy supports both pillars of the economic model advocated in our traditional thinking. The exponential rise in India’s GDP and GDP per capita post liberalisation coincides with wealth generation in the stock market. Similarly, the evidence across various sectors of the economy illustrates the enormous benefits that accrue from enabling the invisible hand of the market. Indeed, the Survey shows clearly that sectors that were liberalized grew significantly faster than those that remain closed. The events in the financial sector during 2011-13 and the consequences that followed from the same illustrate the second pillar – the need for the hand of trust to support the invisible hand. In fact, following the Global Financial Crisis, an emerging branch of the economics literature now recognises the need for the hand of trust to complement the invisible hand.

> The survey posits that India’s aspiration to become a $5 trillion economy depends critically on strengthening the invisible hand of markets and supporting it with the hand of trust. The invisible hand needs to be strengthened by promoting pro-business policies to (i) provide equal opportunities for new entrants, enable fair competition and ease doing business, (ii) eliminate policies that unnecessarily undermine markets through government intervention, (iii) enable trade for job creation, and (iv) efficiently scale up the banking sector to be proportionate to the size of the Indian economy. Introducing the idea of “trust as a public good that gets enhanced with greater use”, the Survey suggests that policies must empower transparency and effective enforcement using data and technology to enhance this public good.

REFERENCES

Aristotle. 1962. Nicomachean Ethics. Translated by Martin Ostwald. Indianopolis: Bobbs-Merrill.

Baker, George, Robert Gibbons, and Kevin J. Murphy. “Relational Contracts and the Theory of the Firm.” The Quarterly Journal of Economics 117.1 (2002): 39-84.

Bénabou, Roland, and Jean Tirole. “Incentives and prosocial behavior.” American Economic Review 96.5 (2006): 1652-1678.

Coase, Ronald (1960), “The Problem of Social Cost”, Journal of Law and Economics, The University of Chicago Press, Vol. 3 (Oct., 1960): 1–44.

Confucius. 2007. The Analects of Confucius. Translated by Burton Watson. New York: Columbia University Press.

Deodhar, Satish (2018), “Indian Antecedents to Modern Economic Thought”, Working Paper, Indian Institute of Management Ahmedabad, No WP 2018-01-02.

Gambetta, D. (1988). “Can we trust trust?”. In Gambetta, D. (Ed.), Trust. Oxford: Blackwell, 213–38.

Gneezy, Uri and Aldo Rustichini. (2000a). “Pay Enough or Don’t Pay At All.” Quarterly Journal of Economics, 115(3): 791–810.

Gneezy, Uri and Aldo Rustichini. (2000b). “A Fine Is a Price.” Journal of Legal Studies, 29(1): 1–18.

Gneezy, Uri, Stephan Meier, and Pedro Rey-Biel (2011). “When and Why Incentives (Don’t) Work to Modify Behavior.” Journal of Economic Perspectives, Vol. 25, No. 4, 191–210.

Guiso, L., P. Sapienza, L. Zingales (2004), “The role of social capital in financial development”, American Economic Review, 94, pp. 526-556.

Hume, David. 1964. “David Hume: The Philosophical Works. Edited by Thomas Hill Green and Thomas Hodge Grose. 4 vols. Darmstadt: Scientia Verlag Aelen. Reprint of the 1882 London ed.

Maddison A (2007), Contours of the World Economy I-2030AD, Oxford University Press, ISBN 978-0199227204.

Maslow, A. H. (1943). A theory of human motivation. Psychological Review, 50(4), 370-96.

Meier, Stephan (2007a), “Do Subsidies Increase Charitable Giving in the Long Run? Matching Donations in a Field Experiment.” Journal of the European Economic Association, 5(6): 1203–22.

Meier, Stephan (2007b), “A Survey of Economic Theories and Field Evidence on Pro-Social Behavior.” In Economics and Psychology: A Promising New Cross-Disciplinary Field, ed. Bruno S. Frey and Alois Stutzer, 51–88. Cambridge: MIT Press.

Olivelle, Patrick (2013), King, Governance, and Law in Ancient India: Kauṭilya’s Arthaśāstra, Oxford UK: Oxford University Press, ISBN 978-0199891825.

Sandel, Michael J. (2012). What Money Can’t Buy: The Moral Limits of Markets. New York: Farrar, Straus and Giroux.

Sanyal, S. (2016). The Ocean of Churn. Penguin.

Sapienza, Paola, and Luigi Zingales. “A trust crisis.” International Review of Finance 12.2 (2012): 123-131.Shamasastry, R. “Kautilya’s Arthashastra (translated in English).” Sri Raghuvir Printing Press, Mysore (1956).

Shamasastry, R. “Kautilya’s Arthashastra (translated in english).” Sri Raghuvir Printng Press, Mysore (1956).

Sihag, Balbir S. “Kautilya’s Arthashastra: A Recognizable Source of the Wealth of Nations.” Theoretical Economics Letters 6.1 (2016): 59-67.

Spengler, J.J. 1971. “Indian Economic Thought,” Duke University Press. Durham.

The Road to Serfdom, Friedrich Hayek, University of Chicago 1944

Williamson, Oliver E. “Calculativeness, trust, and economic organization.” The Journal of Law and Economics 36.1, Part 2 (1993): 453-486.

Zingales, Luigi. “The role of trust in the 2008 financial crisis.” The Review of Austrian Economics 24.3 (2011): 235-249.

Notes:

1 https://www.livemint.com/market/mark-to-market/why-privatization-of-bpcl-will-be-a-good-thing-for-all-stakeholders-1568309050726.html

2 See Gneezy Rustichini (2000a, 2000b), Gneezy, Meier, and Rey-Biel (2011), Meier (2000a, 2000b) for economic research on intrinsic motivation.

Source-