Article explains about Non- Banking Financial Company (NBFC), Importance of NBFC in Indian Economy, Principal Business activities (Financials Activities) of NBFC’s recognized but not limited, Restricted Activities: Activities that are exclusively restricted to be carried on by the NBFC’s, Difference between NBFC & Bank, Requirement to establish business of Non- Banking Financial Services, Types of NBFC’s, NBFC Registered with RBI , Procedures of Registration of NBFC, Foreign Direct Investment (FDI) in NBFC and Opportunity for NBFC’s.

Page Contents

- 1. Non- Banking Financial Company (NBFC)

- 2. Importance of NBFC in Indian Economy

- 3. Principal Business activities (Financials Activities) of NBFC’s recognized but not limited

- 4. Restricted Activities: Activities that are exclusively restricted to be carried on by the NBFC’s

- 5. Difference between NBFC & Bank

- 6. Requirement to establish business of Non- Banking Financial Services

- 7. Types of NBFC’s

- 8. NBFC Registered with RBI

- 9. Procedures of Registration of NBFC

- 10. Foreign Direct Investment (FDI) in NBFC

- 11. Opportunity for NBFC’s

1. Non- Banking Financial Company (NBFC)

Non-Banking Financial Company (NBFC) is a company registered under the Companies Act and engaged in the business of financial services including that of financial institutions. NBFC’s are not Banks but engaged in the business akin to that of banks. Due to simplified sanction procedures, customer oriented financial activity, attractive rate of return on deposits, flexibility and timeliness in meeting the credit needs of specified sectors, NBFC has gained the popularity in Indian economy.

2. Importance of NBFC in Indian Economy

India being a developing economy requires easy access to financial support and services. Financial support and services being offered by traditional banks have long procedural gap between the requirement and availability. In this scenario, NBFC’s are playing crucial role to support the Individuals and businesses for its requirement to personal loans, working capital loans, shared investments and other finance requirement. NBFC’s with the help of technology are addressing the issue of procedural gap and time taken for financial supports. NBFC’s with help of Fin Tech is requirement of the days in the India economy.

3. Principal Business activities (Financials Activities) of NBFC’s recognized but not limited

– Business of extending Loans and advances

– Acquisition of Shares, stocks, bonds, debentures and other marketable securities

– Leasing

– Hire Purchase

– Chit Business

– Insurance Business

4. Restricted Activities: Activities that are exclusively restricted to be carried on by the NBFC’s

– Agricultural Operations

– Industrial Activity

– Purchase and sale of any goods (Other than Securities)

– Providing of any services

– Sale Purchase construction of Immovable Property

5. Difference between NBFC & Bank

NBFCs perform functions similar to that of banks but there are a few differences-

– NBFC Provides Banking services to People without holding a Bank license,

– An NBFC cannot accept Demand Deposits,

– An NBFC is not a part of the payment and settlement system and as such as

– An NBFC cannot issue Cheques drawn on itself, and

– Deposit insurance facility of the Deposit Insurance and Credit Guarantee Corporation is not available for NBFC depositors, unlike banks,

– An NBFC is not required to maintain Reserve Ratios (CRR, SLR etc.)

– An NBFC cannot indulge Primarily in Agricultural, Industrial Activity, Sale-Purchase, Construction of Immovable Property

– Foreign Investment allowed up to 100 %

– An NBFC companies working in Financial Body and Money handling

6. Requirement to establish business of Non- Banking Financial Services

A Company cannot commence or carry on Business of Financial Institution without obtaining certificate of registration from Reserve Bank of India. It requires to fulfill minimum criteria of Net owned fund of Rs. 200 lacs for registration of a Company as Non -Banking Financial Company.

Minimum criteria for Licensing of NBFC’s:

i. It should be a Company Incorporated under the Companies Act, 2013 or previous Acts.

ii. It should have a Net owned fund of Rs. 200 Lacs

Registration and regulations of NBFC’s are done by the Reserve Bank of India. All Activities and transactions of NBFC’s are supervised and controlled by the Reserve Bank of India through its Acts, regulations, prudential norms and guidelines.

However certain categories of NBFC’s are exempted from Registration with RBI avoid implications of dual regulations:

| S. No. | Types of NBFC’s Exempted from Registration with RBI | Regulators of Those Companies |

| 1. | Merchant Banking Company/ Venture Capital Fund Companies/Stock Broking Companies | Securities and Exchange Board of India |

| 2. | Insurance Companies | Insurance Regulatory and Development Authority of India. |

| 3. | Housing Finance Companies | National Housing Bank |

| 4. | Nidhi Companies | Ministry of Corporate Affairs |

| 5. | Chit Fund Companies | State Governments |

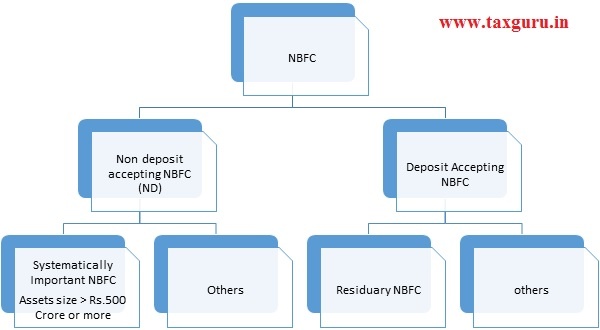

7. Types of NBFC’s

All NBFC’s Registered with RBI are classified in following two categories.

i. Deposit Taking NBFC’s

ii. Non Deposit taking NBFC (the word ND suffixed to the Name of NBFC in this categories)

Further NBFC’s whose assets size is of Rs. 500 Crore or more are categorized as systematically Important NBFC’s. They are classified so because they can have bearing on the financial stability of the country.

8. NBFC Registered with RBI

8. NBFC Registered with RBI

| S. No. | Types of NBFC | Principal Business Activities | Minimum Criteria to be Recognized |

| 1 | Assets Finance Company | Financing Real and physical Assets supporting economic activity. | a) Finance in Real and physical assets should be 60% or more of its total assets size.

b) Income arising from finance in real and physical assets should be 60% or more of its total Income. |

| 2 | Investment Company | Acquisition of Shares and securities of other company | |

| 3 | Loan Company | To make Loan and advances for working capital of the Business (Not for Physical or real assets) | |

| 4 | Infrastructure Finance Company | To make available infrastructure loans | a) Minimum Net owned fund Rs. 300 Crore, and

b) Minimum Credit Rating of ‘A”, and c) Infrastructure Loan Constitute 75% or more of its total assets, and d) Minimum CRAR 15% |

| 5 | Core Investment Company (CIC)

NBFC-CIC-ND |

Investment in Shares , securities or Loans in a Group Companies. | a) 90% of total assets in the form of Investment in shares and securities of group companies.

b) Minimum 60% of the Investment should be in the form of Equity or instruments convertible into Equity. |

| 6 | Infrastructure Debt Finance Company

(IDF) NBFC-ND |

To Facilitate the flow of Long Terms Debt in Infrastructure Projects | To be Sponsored only by Infrastructure Finance Company |

| 7 | Micro Finance Institutions

NBFC-MFI-ND |

To make finance in the form of Loan and advances to lower Income group people | a) Minimum 85% of its total assets constitute in the form of Microfinance.

b) Loan given to people having annual income of Rs. 100,00 and Rs. 160,000 in rural and urban area respectively. c) Loan Amount should not exceed Rs. 100,000 and payment tenure should not be less than 24 months. d) No collateral for such Loan. e)Loan repayment schedule should be weekly fortnightly or monthly at the choice of borrower. |

| 8 | Factor- NBFC-ND | Principal Business of Factoring-acquisition of Receivables by way of assignment of such receivables or financing | a) Factoring Business constitute 50% or more of its Total Assets.

b) Income From Factoring Business should be 50% or more of total gross revenue. |

| 9 | Mortgage Guarantee Company | Business of Mortgage Guarantee | a) Net owned fund of Rs. 100 crore

b) 90% of the business and gross income is from mortgage guarantee. |

| 10 | Non- Operative Financial Holding Company | Financial Holding Company through which the promoters hold the NBFC and other finance company. |

9. Procedures of Registration of NBFC

i. Incorporation of a Company: First step towards registration of NBFC is to Incorporate a company under the Companies Act, 2013 or in case of an existing company, incorporated under any previous Companies Act. It can be a private limited company or a public limited company.

ii. Drafting of MOA and AOA: The Memorandum of Association of the new company or the existing one should be drafted in such a way as it should explicitly depict the main object as financial business.

iii. Fulfilment of the Requirement of the Net owned Fund: A company to be registered as NBFC with RBI should have minimum net owned fund of Rs. 200 Lakh. In case of new company, it requires to Incorporate the company with minimum paid up capital of Rs. 200 lakhs and the amount should be deposited in the bank. In case of existing company, it should be calculated as per RBI definition of Net owned fund.

iv. Complying with other requirements: Other requirements to be fulfilled for registration need to be checked and complied with such as maintenance of CIBIL Record, Compliance with the directorship requirement, obtaining declaration from Board of directors, getting certificate from auditor of the company, furnishing of audited financials in case of existing company.

v. Submission of Application: After the arrangement of documents and compliance requirement application need to be submitted online (electronically) and a physical copy of application along with supporting documents need to be submitted with regional office of RBI. Once the acknowledgement number of submitted application is obtained, the status of the approval can be checked at website of the Reserve Bank of India.

vi. Obtaining Registration Certificate: After the submission of the application and supporting documents it will take 2-3 month to get the licence from RBI to carry on the business of NBFC.

10. Foreign Direct Investment (FDI) in NBFC

The Government has allowed 100% FDI in Non- Banking Financial services through automatic route without any capitalization norms and limited ambit of activities. Now, the NBFC’s which are governed by financial regulators like, RBI, SEBI, IRDA, National Housing Bank or any other regulator as notified by the Government are eligible to receive 100% FDI under automatic route.

FDI in Non- Banking Financial activities which are not regulated by any financial sector regulatory body would be allowed with prior Government approval subject to condition of minimum capitalization as prescribed by the Government.

11. Opportunity for NBFC’s

Large segment of people in India are undercapitalized even being capable to generate the throughput. They don’t have access to capital market or are being declined by the traditional banking system due to assessment of credibility. Low Income –households and informal MSME Enterprises are far away from to the access financial support and services as they require due to lack of data and financials history of the segment. Retail and MSME segments are striving for its capital requirement to increase their length of operation. With right strategy, robust business model and strong governance and risk management, NBFC’s can grab the opportunity of fairly large segment of economy.

About the Author

Author is CA. Shambhu Thakur, Manager at Neeraj Bhagat & Co., Chartered Accountants. He has been taking care of Accounting and Taxation Compliance of domestic as well as multinational Companies operating in India since last 5 years. He has exposure in maintenance of Accounts as per requirement of the business and Industry catering to applicable laws and regulations.

Author is CA. Shambhu Thakur, Manager at Neeraj Bhagat & Co., Chartered Accountants. He has been taking care of Accounting and Taxation Compliance of domestic as well as multinational Companies operating in India since last 5 years. He has exposure in maintenance of Accounts as per requirement of the business and Industry catering to applicable laws and regulations.