Discussion Paper No. 1/2020-DEA

Risk Vs Uncertainty: Supervision, Governance & Skin-in-the-Game

By

Sanjeev Sanyal

Principal Economic Adviser

February 2020

Government of India

Ministry of Finance

Department of Economic Affairs

Economic Division

www.finmin.nic.in

Disclaimer and Acknowledgements

The views expressed in this paper are those of the author and do not necessarily reflect the views of the Ministry of Finance or Government of India.

The author is grateful to Mr. Atanu Chakraborty, Secretary (Economic Affairs) and Dr. K.V. Subramanian, Chief Economic Adviser, for their encouragement and inputs. He would also like to thank Ms. Arpitha Bykere, Ms. Mahima and Ms. Aakanksha Arora for their contribution in preparing this paper. The author takes full responsibility of any remaining errors and omissions.

SUMMARY

The concept of Risk is distinct from the concept of Uncertainty. The former relates to that which can be predicted, measured or quantified whereas the latter relates to “unknown unknowns” and “known unknowables” where outcomes and probability distributions cannot be meaningfully defined. This paper makes the case that the well-engrained policy frameworks used to deal with Risk are fundamentally different from the policy toolkits required to deal with Uncertainty. At the very least, they cannot substitute for each other and attempts to do so have negative unintended consequences. Moreover, given the fuzziness of Uncertainty, it highlights the importance of systemic Trust. This paper primarily uses the financial sector to illustrate this issue, but the approach is widely applicable to the whole range of policymaking from taxation to urban planning.

The use of ever more heavy regulations and Basel-type capital requirements to tackle Risk have not only led to better capitalized banks, but also to the growth of shadow banking that is outside the heavily regulated arena. The use of prescriptive risk weights for bank assets, moreover, means that there is no genetic diversity in how the banking system manages risk. When faced with the unpredictable shocks of an uncertain world, the lack of genetic diversity is a possible threat to the stability of the global financial system. Similarly, the assessment of risk is being effectively outsourced to rating agencies despite their mixed record on providing advance warnings. The current approach focuses exclusively on fixing the internal incentive structures of the rating agencies. However, this presupposes the ability of rating agencies to deal with Uncertainty when the best they can do is quantify Risk. In view of the inherent unpredictability of Uncertainty, this paper argues that the better response would be to invest in active supervision rather than ever more stringent regulation. Simple systems that are transparent and flexible, and those that embed “skin-in-the-game” and institutionalize corporate governance, are far better for dealing with Uncertainty.

A related secondary theme that is also explored here is the need to create rules and regulations that focus on supporting the “compliant” rather than penalizing the “non-compliant”. The approach of creating rules that encompass every possible deviation leads to unnecessary opacity and complexity that burden the majority that comply. The exclusive focus on “round-tripping”, for instance, has meant that India has not been able to develop a globally competitive fund management and financial services sector. A simple, transparent system that presumes compliance, backed up by better supervision and legal enforcement, would be far better.

Finally, the paper argues that in an Uncertain world where contracts, regulations and laws are inherently incomplete, no amount of ex-ante protective walls can prevent things from going wrong. This is why ex-post recovery and resolution must be an important part of a policy toolkit to deal with Uncertainty.

“But Uncertainty must be taken in a sense radically distinct from the familiar notion of Risk, from which it has never been properly separated.” –

Frank H. Knight

INTRODUCTION

Economic policy-making must be able to deal with a world that faces both Risk and Uncertainty. The two are fundamentally different. Risk can be measured and quantified – the possible set of future events and their potential impacts can be quantified within a probability distribution. Policy measures, regulations and contracts can be put in place to specifically deal with these Risks (economists will recognize this as an “Arrow-Debreu” world). In contrast, Uncertainty cannot be predicted or quantified in a meaningful way since that the probability of future events and their possible impact are unknown (Knight, 1921). In complex interconnected systems such as the economy and the financial sector, Uncertainty implies unpredictable shocks, and equally unpredictable responses of economic agents to those shocks, that can lead down multiple non-linear pathways, feedback loops, and unintended consequences. Uncertainty includes: (i) the “unknown unknowns” – the economic, financial, technological, policy, geopolitical, political and “Black Swan” events, which lead to contagion, structural breaks and systemic shifts; and (ii) the “known unknowables” – factors that cannot be entirely resolved due to inherent information gaps and asymmetries among market participants1. This paper argues that the policy prescriptions to deal with Uncertainty are intrinsically different from the policy frameworks used to manage Risk. Policymakers often try to employ the same regulatory approach to tackle both Risk and Uncertainty. This is a slippery slope since the large range of possible outcomes in an Uncertain world lead to a proliferation of regulations that ironically get in the way of the flexibility and transparency needed to deal with unpredictable situations. Moreover, it leads to an excessive focus on controlling every “non-compliant” rather than encouraging the “complaint”. This leads to policy outcomes that discourage good behaviour by increasing the cost of compliance. This point is applicable across all forms of policy-making but this paper illustrates it using the financial system.

Basel Banking Regulatory Reforms

The bank failures in the 1970s and Latin American debt crisis in the 1980s led the Basel Committee comprising of the G10 countries to adopt international-standards for “minimum” risk-based regulatory capital adequacy, the Capital-to-Risk Weighted Assets Ratio2 (CRAR), for banks in 1988. Now known as Basel I, it aimed to align banks’ regulatory capital requirements to the credit risk on their balance sheets (Table 1). Over time, the Basel Committee refined this framework, including under Basel II in 2004, to also account for market risk and operational risk on bank balance sheets.

Table 1: Evolution of Basel Framework

| Regulatory Norms | Basel I | Basel II | Basel III |

| Total Regulatory Capital (CRAR + Capital Conservation Buffer) (per cent of risk-weighted assets) | 8% | 8% | 10.5% |

| 1.1. Capital to Risk-Weighted Asset Ratio (CRAR) # | 8% | 8% | 8% |

| 1.1.1.Tier 1 Capital Ratio | 4%* | 4% | 6% |

| 1.1.1.1. Common Equity | 2% | 4.5% | |

| 1.1.2.Tier 2/Tier 3 Capital | 4% | 4% | 2% |

| Capital Conservation Buffer (Comprised of Common Equity) | 2.5% | ||

| Counter-Cyclical Capital Buffer (Comprised of Common Equity) (per cent of risk-weighted assets) | 0-2.5% | ||

| Leverage Ratio @ (Tier 1 Capital as a per cent of on- & off-balance sheet assets) | 3% | ||

| Liquidity Framework | Net Stable Funding Ratio for 1 year; Liquidity Coverage Ratio of 100% ** | ||

| Large Exposures Framework (per cent of Tier 1 capital) |

25% | ||

| 6. Systemically-Important Banks | Additional capital and supervisory requirements | ||

| 7. Risk Management | Credit risk, market risk | Credit risk, market risk, operational risk | Focus on counter party risk, credit value adjustment; increased risk sensitivity for certain exposures |

Source: Basel Committee on Banking Supervision, BIS. Note: *Comprised of Core capital. #See footnote 2. @See footnote 3. **See footnote 4.

The Global Financial Crisis 2007-08, however, highlighted the inability of financial institutions to withstand a system-wide credit/liquidity event. The Basel Committee responded by introducing more stringent norms on the quantity and quality of capital requirements under Basel III in 2010. Basel III added an additional layer of Common Equity called the Capital Conservation Buffer; introduced a leverage ratio3 and two liquidity ratios4 to enhance loss-absorbing capital and reduce liquidity and maturity mismatches, respectively; and imposed “macro-prudential norms” including a Counter-Cyclical Capital Buffer to balance out credit cycles, and additional requirements on systemically important banks (Table 1).

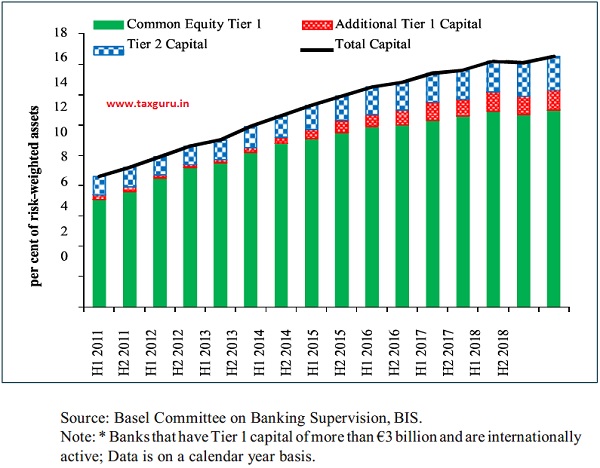

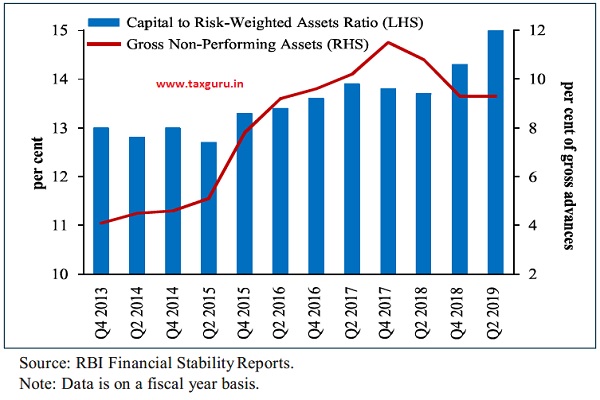

It is fair to say that the implementation of Basel III norms has helped banks globally to become better capitalized, in particular by increasing Common Equity capital requirements, and has reinforced the focus on risk management (Figure 1). In India, the RBI rolled-out Basel III regulations in a phased manner starting 2013, with the CRAR and leverage ratio requirements and the risk weights assigned to some asset classes set somewhat higher than those prescribed under Basel III (Table 2).This along with the introduction of the Insolvency and Bankruptcy Code, 2016 (IBC) and more stringent asset quality recognition have helped strengthen the Indian banking system compared to a few years ago (Figure 2).

Figure 1: Capital as a Per Cent of Risk-Weighted Assets for Global Internationally-Active Banks*

Table 2: Capital Requirements and Assignment of Risk Weights under Basel III and RBI Regulations

| Regulatory Norms | Basel III Norms | RBI Norms |

| 1. Regulatory Capital (per cent of risk-weighted assets) | ||

| 1.1. Capital to risk-weighted asset ratio (CRAR) | 8.0 | 9.0 |

| 1.1.1. Tier 1 Capital | 6.0 | 7.0 |

| Common Equity Tier 1 | 4.5 | 5.5 |

| Additional Tier 1 Capital | 1.5 | 1.5 |

| 1.1.2. Tier 2 Capital | 2.0 | 2.0 |

| 1.2. Capital Conservation Buffer (comprised of Common Equity) | 2.5 | 2.5 |

| Total Capital (CRAR + Capital Conservation Buffer) | 10.5 | 11.5 |

| 2. Leverage Ratio (Tier 1 Capital as a per cent of on- & off- balance sheet assets) | ||

| Minimum Levarage Ratio | 3.0 | 3.5 |

| 3. Large Exposures Framework (per cent of Tier 1 capital) | ||

| Bank exposure to a single counterparty | 25.0 | 20.0* |

| Bank exposure to a group of connected counterparties | 25.0 | 25.0 |

–

| Risk weights for long-Term exposure to corporates based on external credit ratings (percent) | Basel III Norms | RBI Norms |

| AAA | 20 | 20 |

| AA | 20 | 30 |

| A | 50 | 50 |

| BBB | 75 | 100 |

| BB & below | 100 | 150 |

| Below BB | 150 | 150 |

| Unrated | 100 (85 if SME) | 100 |

Source: Basel Committee on Banking Supervision, BIS, RBI.

Note: *Note: 25 per cent only in exceptional cases as allowed by a bank’s Board.

Figure 2: Regulatory Capital Adequacy and Asset Quality of Indian Banks

Nonetheless, note that the increasingly stringent Basel norms over the past four decades have continued to focus on addressing Risks and “known unknowns” in the financial system. While increased Bank capitalization is good even from an Uncertainty perspective, this particular approach is oriented to a deterministic view of Risk.

The Problem with Prescriptive Risk Weights

The Basel approach implicitly assumes that banks are primarily exposed to outcomes that are known and have a quantifiable probability distribution. The Basel norms and national regulators prescribe risk weights for bank asset classes and corresponding credit ratings based on which banks calculate the regulatory capital requirements as a share of risk-weighted assets. Over the years, regulators have made these risk-weights more granular and have increased the risk sensitivity of bank balance sheets to credit risk and operational risk (Table 3).

However, economies and financial systems are complex systems buffeted by unpredictable shocks and unknown impacts. While the regulatory models of banks and

Table 3: Evolution of Risk Weights Assigned to Bank Exposures under Basel Norms

| Credit Ratings | Risk Weights Assigned to Sovereign Debt (per cent) | Risk Weights Assigned to Long-Term Exposurto Banks (per cent) | |||

| Basel I | Basel II & III | Basel I | Basel II | Basel III | |

| AAA AA- | 0 | 20 | 20 | ||

| A+ to A- | 20 | 50 | 30 | ||

| BBB+ to BBB- | 50 | 50 | 50 | ||

| BB+ to B- | 100 | 100 | 100 | ||

| Below B- | 150 | 150 | 150 | ||

| Unrated | 100 | 50 | 30-150 based on Grade |

||

| OECD** Countries | 0 | 20 | |||

| Non-OECD Countries | 100 | 100 | |||

–

| Credit Rating | Risk Weights Assigned to Corporates | ||

| Basel I | Basel II | Basel III | |

| AAA AA- | 20 | 20 | |

| A+ to A- | 50 | 50 | |

| BBB+ to BBB- | 100 | 75 | |

| BB+ to BB- | 100 | 100 | |

| Below BB- | 150 | 150 | |

| Unrated | 100 | 100 (85 for SMEs) | |

| OECD Countries | 100 | ||

| Non-OECD Countries | 100 | ||

Source: Basel Committee on Banking Supervision, BIS.

Note: *Under Basel II and Basel III, national supervisors have discretion to set a lower risk weight for exposures denominated and funded in the local currency of the corresponding sovereign. **Organisation for Economic Co-operation and Development.

regulators aim to account for and estimate Risk, even the most sophisticated models will fail to predict Uncertain events – the “unknown unknowns” and “known unknowables”. This makes it challenging to assess the impact of such Uncertainty on bank balance sheets and therefore precisely measure the “true” riskiness of assets and assign them suitable risk weights. Hence, a risk weight-based approach to determine bank capital requirements may be misleading when dealing with Uncertainty. Local currency government debt, for instance, is assigned zero risk weight but the recent Greek sovereign debt crisis showed that this is an incorrect assumption. This is not to argue that banks should not be encouraged to hold more capital, but to point out that an excessively prescriptive Risk-oriented system may embed a fundamental flaw.

In addition, a “one size fits all” regulatory approach to measure risk and assign risk weights implies reduced “genetic diversity” in the financial system as banks and regulators around the world fine-tune business models to assess and manage risk in an identical manner5. If a “Black Swan” shock unanticipated by Basel models hits the global financial system, all homogenous parts of the global financial system would be vulnerable in the same manner (Haldane and May, 2011).

The use of banks’ internal models and Basel’s standardized approach model illustrates the trade-off between Risk and Uncertainty approaches. Basel III norms limited the use of banks’ internal models since such models were prone to gaming by banks to minimize risk weights and therefore capital requirements. Aiming to reduce the “non-compliants” in the system, Basel III instead introduced a standardized approach model to assess and manage risk. This may have partly reduced gaming but it also clearly reduced genetic diversity of the banks. Meanwhile, the discretion to determine total risk-weighted assets on the balance sheet allows some banks to continue gaming the rules to underestimate capital requirements. For instance, banks can “optimize” the standardized approach model by adjusting their portfolio towards assets that entail lower risk weights in order to arbitrage regulatory capital. The Euro Area sovereign debt crisis showed the danger of banks adjusting their portfolio towards sovereign debt that enjoys zero risk weight (Acharya and Steffen, 2013).

Given the problem of genetic diversity, the policy approach for managing Risk would be ineffective for managing Uncertainty. Empirical evidence based on past crises suggest that growing assets and complexity of bank balance sheets may require simpler non-risk weight based regulatory rules, such as the leverage ratio, instead of the ever more complex risk-weight based rules to insure against “Knightian Uncertainty” (Haldane and Madouros, 2012; Aikman, Haldane, Hinterschweiger and Kapadia, 2018). In fact, studies suggest that a simple leverage ratio based on Common Equity, instead of Total Tier 1 Capital, could be more effective in preserving bank solvency during shocks. This is especially likely when banks tend to hold weaker forms of capital such as hybrid debt capital instruments and subordinated debt (World Bank’s Bank Regulation and Supervision Survey, 2019).

Can Credit Ratings be Made Reliable?

Another illustration of the difference between the Risk and Uncertainty approaches is the importance given to risk assessments by credit rating agencies (CRAs) for calculating risk weights prescribed by Basel/national supervisors for bank regulatory capital requirements. The Basel approach hardwires risk weights to the ratings assigned by CRAs, even though the track record of CRAs is far from exemplary. Many regulators recognise the problem but it is mostly seen as a matter of fixing the internal incentive structures of the CRAs – particularly the conflict of interest in the CRA’s “issuer-pay” model, where debt issuing firms have incentives to shop for favourable credit ratings.

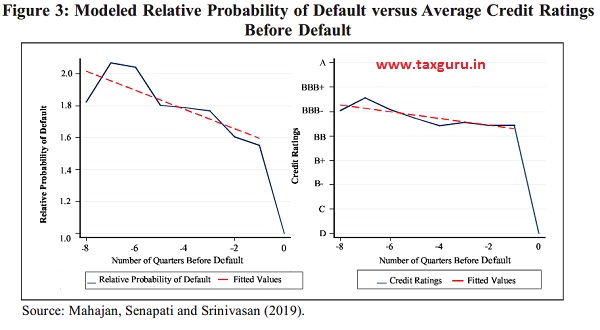

The criticism around the incentives of CRAs both in India and globally has focused on their repeated failure to predict and measure Risk, i.e., the delay in recognizing credit quality deterioration in firms and downgrading them despite negative publicly available information on such firms. This is a valid concern. For instance, some CRAs in India continued to assign ‘Investment Grade’ ratings to a number of firms until a few days before these firms filed for bankruptcy. Mahajan, Senapati and Srinivasan’s (2019) corporate default model for a set of publicly traded firms in India shows that the firms were in distress several quarters prior to default as indicated by the relative probability of default, whereas the ratings were sharply downgraded to default status in the same quarter as the default happened (Figure 3). Hence, this is a systematic failure to correctly flag a measurable deviation.

As Goodhart’s Law (1975) suggests, when a measure becomes the target, it is no longer a good measure since market participants change their behaviour to meet the target, i.e., investors optimize ratings since it is a measure of default on their portfolio, and banks optimize ratings since it is a measure of capital requirements and bank solvency. There are incentives for all major users/providers of credit ratings to seek inflated ratings. Thus, there is a necessary debate on how to reinstate trust by addressing the incentive conflicts in both the current “issuer-pay” model and the “subscriber-pay” model, which was in place until the 1970s, and had led institutional investors to seek favourable ratings to cater to their portfolio.

The problem, however, is that fixing the incentive alignment problem alone does not improve the ability of CRAs to deal with Uncertainty. Trying to get CRAs to use credit rating models to quantify “unknown unknowns” is an example of what Friedrich von Hayek (1974) termed as the “pretence of knowledge”. Before Basel norms gave it a regulatory sanction, credit ratings were used merely as educated opinions of third-parties. They provided additional information but did not substitute for the active judgment of the financier. Rather than hardwire risk weights on outsourced opinion, there may be a case for enhancing real time transparency. In this regard, note that the Securities and Exchange Board of India (SEBI) has implemented several measures since November 2018 to enhance disclosures by CRAs and corporates. This includes disclosure to the stock exchange about any default on loan interest or principal payments beyond 30 days; disclosure of liquidity indicators, average one-year rating transition rates for long-term instruments, inter-linkages of subsidiaries; and explanation of the broad operating and/ or financial performance levels that could trigger a rating change. Improved real-time transparency is perhaps more important from an Uncertainty perspective than the opinion of a CRA.

Risk Shifting and Shadow Banking

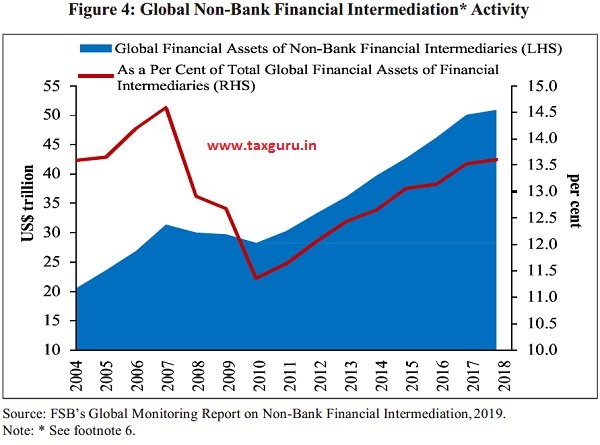

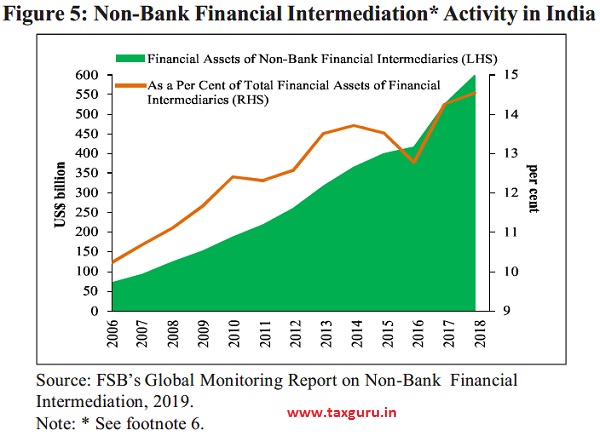

One of the unintended consequences of ever increasing bank regulations is that it shifts market activity to “shadow banks” (also called “non-bank financial intermediaries”) where the scope for regulatory arbitrage is higher, especially as banks become more averse to lend to high risk borrowers and/ or small borrowers (Gandhi, 2014). This phenomenon has been witnessed in various forms in India and globally. According to the Financial Stability Board (FSB), after having shrunk following the Global Financial Crisis, the size of the non-bank financial intermediation sector6globally has increased steadily in the recent years, nearly doubling from US$ 28.3 trillion in 2010 to US$ 50.9 trillion in 2018 (Figure 4).

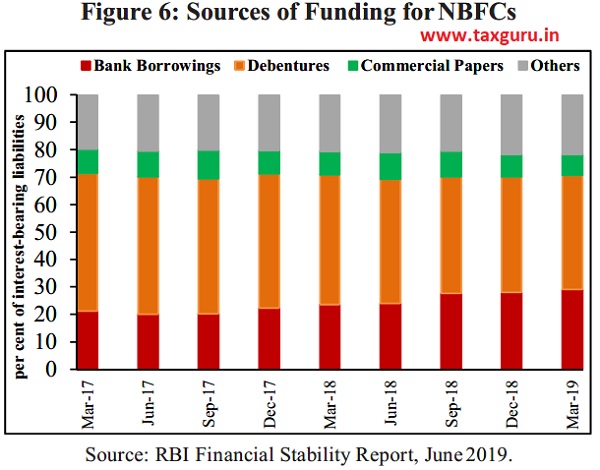

The FSB’s measure shows that the size of the non-bank financial intermediation sector involved in credit intermediation in India has increased markedly over the past decade, driven by the rapid growth of the Non-Banking Financial Companies (NBFCs) (Figure 5). Moreover, as also witnessed globally, banks continue to have strong linkages with the shadow banking system and therefore high indirect exposure to high-risk customers. For instance, the share of bank borrowings in NBFCs’ funding has increased from 21.2 per cent in March 2017 to 29.2 per cent as of March 2019 as banks compensated for reduced capital market access for NBFCs (Figure 6). In addition, the top 10 NBFCs (out of a total 9,659 NBFCs) accounted for more than 50 per cent of the total bank lending to NBFCs as of March 2019.

As can be seen, increasing regulation in one part of the financial system has shifted Risk to the less-regulated, less- transparent part of the financial system. The RBI is currently in the process of improving supervision, including risk management and governance, at NBFCs, and harmonising the regulations for Housing Finance Companies (HFCs) with the NBFC regulations. However, in a complex and interconnected financial system, imposing stringent bank- type regulations on NBFCs could either shut off capital to a significant part of the economy or shift systemic risk to yet another part of the financial system. In such a case, only a nuanced regulatory trade-off with active and flexible supervision can be made to work (Admati and Hellwig, 2019).

Regulation versus Supervision

Just like Risk and Uncertainty are often treated the same, there is a common tendency to treat “regulation” and “supervision” as broadly the same or even as substitutes. Regulation refers to the minimum standards, rules and policy frameworks put in place for institutions to operate in a sector. In contrast, supervision is not merely about ensuring compliance and enforcement of regulatory rules but also about actively monitoring the sector, with supervisors exercising flexibility and discretion to manage and respond to shocks on a real-time basis.

Since regulation is a more mechanical, top-down approach, it often becomes the default response of policymakers. As the extensive academic literature on incomplete contracts shows, under conditions of Uncertainty, it is very difficult to create regulations for every possible state-of-the- world. It is also very difficult to account for every non-compliant. The compliant tends to comply in similar ways, but the non-compliant can deviate in a myriad ways. It is then a slippery slope towards a regulatory framework that throttles the compliant with endless box-ticking and excessive requirements. It would be far better, therefore, to have a simpler regulatory framework supplemented by active and efficient supervision. The problem is that supervision demands active monitoring and accountability from the government department or regulatory body. This creates a perverse incentive to keep adding more top-down regulations regardless of their effectiveness.

The tax treatment of India’s fund management and financial services sector provides a good illustration of the above problem. With the aim of developing the fund management industry, Section 9A of the Income Tax Act (1961) provides a tax exemption to foreign portfolio investors in order to encourage them to locate their fund managers in India. However, the foreign fund must satisfy 17 eligibility conditions. These stringent conditions are focused on preventing round-tripping and money laundering, even though regulators have several money laundering and foreign exchange management related laws in place to counter round-tripping. The Commerce Ministry’s Report of the High-Level Advisory Group (2019) noted that such stringent financial services regulations have caused several India-related financial services to be rendered from offshore financial centres. The report pointed out that “the baggage of round tripping cannot be used to stifle the financial services sector any more than using the risk of a traffic accident to stop construction of a key highway”, especially as emerging technologies, global Know Your Customer (KYC) norms, and tax information sharing under OECD’s Common Reporting Standard now offer better tools to track international money trails. Institutionalized distrust is again the problem.

The regulation versus supervision trade- off requires a mindset change such that the first order of policy should be to ensure that legitimate entities, i.e., the “compliants”, can carry out business activity without any encumbrance. This requires simpler regulations combined with greater emphasis on supervision to detect improper activity, determine the extent of the problem, and penalize the “non-compliants”. This applies to all fields of policymaking and concerned ministries and regulators need to invest in supervisory capacity.

Ensuring Skin-in-the-Game

One of the aspects of Uncertainty is related to the “known unknowables”, such as moral hazard, irresponsible behavior, excessive and inefficient risk-taking, and distorted incentive structures, that may apply to senior management, key employees or shareholders of a firm. The problem arises because the actions of such key market players and decision-makers are sometimes not directly observable, and given the inherent uncertainty of outcomes, it is not easy to hold them accountable. One way to circumvent this problem is to ensure that key managers, employees and shareholders have “skin-in-the-game”.

One area that has attracted a lot of attention since the Global Financial Crisis is compensation reform of key personnel in financial institutions relating to variable compensation, malus clauses, claw-backs provisions and delayed encashment in order to reduce excessive risk-taking and risk-shifting. The FSB’s Principles and Standards for Sound Compensation Practices with regard to compensation structure, governance and disclosure aims to align compensation at banks with prudent risk-taking and longterm profitability. In line with these best practices, India has begun implementing compensation reforms at the supervisory and bank level (Table 4). In November 2019, the RBI revised compensation guidelines for CEOs, whole-time directors, “material risk takers” and control-function staff at private and foreign banks with effect from April 2020, with specifications on minimum and deferral of variable pay and malus and clawback arrangements. The basic idea here is that compensation packages contain enough “skin-in-the-game” in order to align the personal interests of key personnel with that of the institution and the wider system. It should be noted, however, that there is a trade-off. If decision-makers are made to pay too large a price for negative outcomes, they will turn systematically risk-averse leading to a decline in innovation and investment.

Table 4: Implementation of FSB’s Compensation Principles for Financial Institutions in India and Other Major Jurisdictions

| Compensation Policies | India | USA | UK | Singapore |

| Supervisors discuss compensation policies with banks’ non-executive board members, senior executives and | No | Yes | Yes | Yes |

| Remuneration Committees | ||||

| Supervisory requirements/expectations on control functions to be involved in compensation for senior executives and certain MRTs* | Yes | Yes | Yes | Yes |

| Supervisory requirements/expectations on no. of years of compensation deferral for senior executives and other | Yes | Yes | Yes | Yes |

| MRTs | ||||

| Banks link senior executive compensation to risk appetite frameworks | Yes | Yes | Yes | Yes |

| Banks link compensation to non-financial risks taken and “what” and “how” business is conducted to achieve performance | No | Yes | Yes | Yes |

| Banks apply gateways to not award variable compensation to senior executives and other MRTs due to misconduct/poor performance | No | Yes | Yes | Yes |

| For significant banks, compensation policies (incl. on governance, risk alignment) are timely, clearly, comprehensively and publicly disclosed | Some banks | All banks | All banks | All banks |

| For significant banks, Boards and/or Board Committee are actively involved in monitoring and reviewing Banks’ compensation system | All banks | All banks | All banks | All banks |

| Significant banks regularly review compensation and risk outcomes for consistency with the underlying compensation system | All banks | All banks | All banks | All banks |

Corporate Governance and Values

There is a need to revisit a gamut of old-fashioned solutions for some of the Uncertainty arising from “known unknowables” of management behaviour: corporate governance, internal controls, reporting and oversight, accountability, corporate values and ethics (Table 5).

The Board of Directors, especially non-executive independent directors, are a firm’s first line of defence. The Board’s expertise, composition, ratio of independent directors and sufficient engagement with the management are imperative here. It is also necessary to attract talent to Boards by providing appropriate incentives. While more stringent regulation of Directorships is also needed, just using the stick may not work as it will merely discourage good quality people from participating in the Board.

Table 5: Banking Sector Corporate Governance in India and Other Major Jurisdictions

| Supervision of Bank Governance and Audit | India | Singapore | UK | USA |

| I. Has the supervisor introduced changes to bank governance framework after the 2007-09 crisis? | ||||

| a. New requirements on executive compensation | √ | √ | √ | |

| b. Independence of the Board | √ | √ | √ | |

| c. Chief risk officer direct reporting line to the Board/Board Committee | √ | √ | √ | √ |

| d. Existence of a Board risk committee | √ | √ | √ | |

| II. Does the supervisor exercise approval authority for appointment of: | ||||

|

a. Board directors |

√ | √ | √ | √ |

|

b. Senior bank management |

√ | √ | √ | |

| III. Can the banking supervisor agency: | ||||

| Blacklist unfit/not proper shareholders, board members, senior management from holding any position/stake in any bank | √ | √ | ||

| Remove board members and senior management from banks who are found to be unfit/not proper | √ | √ | √ | √ |

| Require banks to obtain supervisors’ approval/no-objection for appointment of key staff (e.g., chief risk officer, chief operating officer, chief financial officer) | √ | √ | √ | |

| IV. Do supervisors receive a copy of: | ||||

|

a. The auditor’s report on financial statements |

√ | √ | √ | |

|

b. The auditor’s letter to bank management |

√ | √ | ||

|

c. Other communication to the Audit Committee |

√ | √ | ||

| V. Can the bank supervisor: | ||||

| a. Remove a bank’s external auditor | √ | √ | √ | √ |

| b. Prosecute a bank’s external auditor for negligence, fraud or collusion | √ | |||

| c. Blacklist a bank’s external auditor from performing future bank audits | √ | √ | √ | |

| VI. Does the external auditor have to: | ||||

|

a. Obtain a professional certification or pass a specific exam to qualify |

√ | √ | √ | |

|

b. Register with an appropriate public and/or professional body |

√ | √ | √ | |

|

c. Have a minimum required bank auditing experience |

√ | |||

|

d. Be approved/reviewed by supervisor |

√ | |||

| VII. Are there mandatory rotation requirements (i.e. limits on no. of consecutive years audited) in place for: | ||||

|

a. Lead auditor (engagement/concurring partner) |

√ | |||

|

b. Auditing firm |

√ | √ | √ | |

| VIII. Are auditors required to promptly inform banking supervisors when they intend to issue qualified opinions on the accounts, and when they identify information that could affect the safety/soundness of a bank? | √ | √ |

Source: World Bank’s Bank Regulation and Supervision Survey, October 2019 based on survey of relevant regulatory/supervisory agency in each jurisdiction conducted during 2017-19.

How well the Board represents the shareholders’ interests depends on whether the Board has a sound understanding of the “inner workings” of the bank (Mehran, 2011). An alert Board would be capable of ensuring proactive rather than reactive and post-facto governance and supervision. It is key to strengthen the ex-ante, forward-looking risk-management culture among the Board and management for timely identification and mitigation of risks, and to institutionalize risk culture. The Board should be able to ask questions and challenge the senior management’s actions, especially during the good times, demand adequate information from the management, and ensure effective internal controls. However, in the long term, what may matter are the most old-fashioned ideas – corporate values and culture (Chakrabarty, 2013). Sound corporate governance and compliance culture at the bank level would also help supervisors relay more on bank’s internal processes, making supervision more efficient (Jain, 2019).

Ex-post Resolution and Contract Enforcement

The above discussion relates to ex-ante ways of dealing with Uncertainty. However, in an uncertain world with unpredictable outcomes, things could go inevitably wrong even with the best regulation, supervision and management in place. As Grossman and Hart’s (1986) work on “incomplete contracts” shows, contracts are contingent on future states and it is not possible to write complete contracts, and by extension regulations, for every future state. Thus, adding ex-ante complexity to contracts and regulations, or ex-ante risk analysis and management cannot resolve this issue. The resilience of an institution, system or even a policy framework depends on the efficiency of recovery after things have gone wrong. This is where ex-post resolution and contract enforcement become critical.

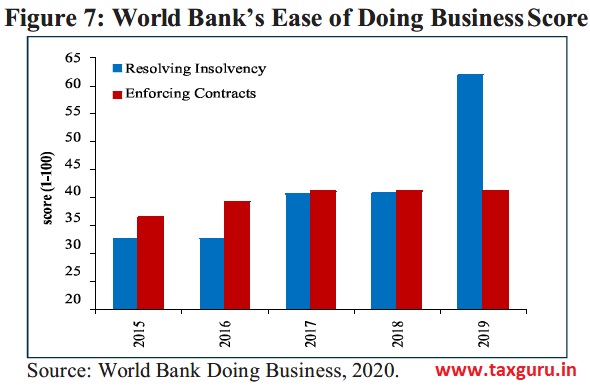

India has made some progress with resolution in recent years with the introduction of the Insolvency and Bankruptcy Code, 2016 (IBC). Economic Survey 2019-20, Volume II contains an update on how things have progressed in the insolvency space. However, dispute resolution and contract enforcement remain areas of concern. Following the introduction of IBC in 2016, India’s score in the World Bank’s Doing Business indicators for resolving insolvency has jumped, with the country ranking rising to the 52nd position (Figure 7). However, India’s score for contract enforcement remains low and the country ranking remains at 163 out of 190 countries. The Economic Survey 2018-19 had highlighted some of the problems with India’s legal system and future Economic Surveys will almost certainly return to these issue.

CONCLUSION

The world of Uncertainty is fundamentally different from the world of Risk, and therefore, it requires policy tools that are also significantly different. However, the default policy response tends to be dominated by the Risk-based approach. The financial system provides a good illustration of the conflicts between the two approaches: supervision versus regulation, the reliability of credit ratings, risk shifting, the danger of prescriptive risk weights, genetic diversity and so on. The above discussion shows how there is not only a difference between the two views but there is a trade-off that is not always appreciated.

Since regulation is a more mechanical, top-down approach, it often becomes the default response of policymakers. As the extensive academic literature on incomplete contracts shows, under conditions of Uncertainty, it is very difficult to create regulations for every possible state-of-the-world. It is also very difficult to account for every noncompliant. It would be far better, therefore, to have a simpler regulatory framework supplemented by active and efficient supervision. The problem is that supervision demands active monitoring and accountability from the government department or regulatory body. This creates a perverse incentive to keep adding more top-down regulations regardless of their effectiveness.

Irrespective of the quality of regulations and supervision, the fuzziness of a world of Uncertainty further requires systemic trust. This implies revitalizing old-fashioned responses such as corporate governance, transparency, ethics and skin-in-the- game. Moreover, there should be a greater acceptance of the likelihood that things will go wrong. No amount of ex-ante planning and rule-making can compensate for efficient ex-post resolution and contract enforcement.

REFERENCES

Aikman, David, Andrew G Haldane, Marc Hinterschweiger and Sujit Kapadia, “Rethinking financial stability,” Bank of England Staff Working Paper No. 712, 2018.

Acharya, Viral V. and Sascha Steffen, “The “Greatest” Carry Trade Ever? Understanding Eurozone Bank Risks,” NBER Working Paper No. 19039, 2013.

Admati, Anat R. and Martin F. Hellwig, “The Parade of the Bankers’ New Clothes Continues: 34 Flawed Claims Debunked,” Stanford University Graduate School of Business Working Paper No. 3032, 2019.

Anginer, Deniz, Ata Can Bertay, Robert J. Cull, Asli Demirguc-Kunt and Davide Salvatore Mare, “Bank Regulation and Supervision Ten Years after the Global Financial Crisis,” Policy Research Working Paper No. WPS 9044, World Bank Group, 2019.

Chakrabarty, K.C., “Strengthening the Banking Supervision through Risk Based Approach: Laying the Stepping Stones,” Speech at Inaugural Session of CAFRAL’s Conference of Non-Executive Directors on the Boards of Commercial Banks, Reserve Bank of India, 2013.

Gandhi, R., “Designing Banking Regulation in Aspiring Economies: The Challenge,” Speech at 41st Annual Convention of the Department of Business Economics, University of Delhi, Reserve Bank of India, 2014.

Goodhart, C.A.E., “Problems of Monetary Management: The UK Experience,” Papers in Monetary Economics, Volume I, Reserve Bank of Australia, 1975a.

Greenwood, Robin, Samuel G. Hanson, Jeremy C. Stein and Adi Sunderam, “Strengthening and Streamlining Bank Capital Regulation,” Brookings Papers on Economic Activity, BPEA Conference Drafts, 2017.

Grossman, Sanford J. and Oliver D. Hart, “The Costs and Benefits of Ownership: A Theory of Vertical and Lateral Integration,” Journal of Political Economy Vol. 94(4), University of Chicago Press, 1986.

Haldane, Andrew G. and Vasileios Madouros, “The dog and the frisbee,” Proceedings – Economic Policy Symposium – Jackson Hole, Pages 109-159, 2012.

Haldane, Andrew G. and Robert M. May, “Systemic risk in banking ecosystems,” Nature, Vol. 469, No. 7330, 2011.

Hayek, Friedrich August von, “The Pretence of Knowledge,” Prize Lecture to the memory of Alfred Nobel, NobelPrize.org, Nobel Media AB 2020, 1974.

Jain, M. K., “Regulatory and Supervisory Expectations on Compliance Function in Banks,” Financial Institution Benchmarking and Calibration (FIBAC) IBA and FICCI Annual Global Banking Conference, Reserve Bank of India, 2019.

Knight, Frank H., “Risk, Uncertainty and Profit,” University of Illinois at Urbana-Champaign’s Academy for Entrepreneurial Leadership Historical Research Reference in Entrepreneurship, 1921.

Mahajan, Kriti, Manjusha Senapati and Anand Srinivasan, “Stress testing of firm level credit risk,” Working Paper, CAFRAL, 2019.

Mehran, Hamid, Alan Morrison and Joel Shapiro, “Corporate governance and banks: what have we learned from the financial crisis?,” Federal Reserve Bank of New York Staff Reports No. 502, 2011.

Report of the High-Level Advisory Group, Commerce Ministry, Government of India, 2019.

Sanyal, Sanjeev, “Beyond Risk: Policy making for an Uncertain World,” Indian Institute of Banking and Finance (IIBF) 10th R.K. Talwar Memorial Lecture, 2019.

Notes :

1 See Indian Institute of Banking and Finance (IIBF) 10th R.K. Talwar Memorial Lecture “Beyond Risk: Policy making for an Uncertain World”, Sanjeev Sanyal, November 2019.

2 Capital-to-Risk Weighted Assets Ratio (CRAR) is a bank’s regulatory capital as a per cent of its risk-weighted assets, where regulatory capital includes Tier 1 Capital (Common Equity + Additional Tier 1 Capital) and Tier 2 Capital. Common Equity includes common shares, retained earnings and other comprehensive income and disclosed reserves; Additional Tier 1 Capital includes capital instruments with no fixed maturity; and Tier 2 Capital includes subordinated debt and general loan-loss reserves.

3 Leverage Ratio is a bank’s Tier 1 Capital as a per cent of its on- and off-balance sheet assets including derivatives, repos and other securities financing transactions, irrespective of risk weighting.

4 Net Stable Funding Ratio is the amount of available stable funding relative to the amount of required stable funding for a Bank, where available stable funding is a bank’s capital and liabilities expected to be reliable over a 1-year time horizon, and required stable funding is a function of a bank’s liquidity characteristics and residual maturities of the on- and off-balance sheet assets. Liquidity Coverage Ratio is the value of a bank’s stock of high-quality liquid assets relative to the total net cash outflows over 30 calendar days under stressed conditions.

5 See Indian Institute of Banking and Finance (IIBF) 10th R.K. Talwar Memorial Lecture “Beyond Risk: Policy making for an Uncertain World”, Sanjeev Sanyal, November 2019.

6 Includes non-bank financial institutions involved in credit intermediation that may pose bank-like financial stability risks (i.e., maturity/ liquidity transformation, leverage, imperfect credit risk transfer) and/or regulatory arbitrage. These include activities related to Money Market Funds, fixed income funds, mixed funds, credit hedge funds, real estate funds, finance companies, leasing/factoring companies, consumer credit companies, broker-dealers, securities finance companies, credit insurance companies, financial guarantors, monolines, securitisation vehicles, structured finance vehicles, asset-backed securities.