The Economic Survey 2015-16 had predicted the Indian economy to register the GDP growth rate in the range of 7 to 7.75 per cent in the year 2016-17. The economy was indeed treading along that path and clocked 7.2 per cent in the first half of the current financial year, as per the estimates released by the Central Statistics Office (CSO). However, consequent upon the radical measures initiated in November 2016 in the form of demonetisation of Rs. 1000 and Rs. 500 currency notes, the Indian economy is likely to experience a slowdown in the growth rate that could be lower than the first advance estimates of CSO. The first advance estimates released in early January 2017 were arrived at mainly based on data prior to demonetisation and largely reflect the economic situation prevailing in the first seven to eight months of the financial year. Even the likely reduction in the rate of real GDP growth of 1/4 percentage points to 1/2 percentage points relative to the baseline of about 7 per cent still makes India’s growth noteworthy given the weak and unsettled global economy which posted a growth rate of a little over 3 per cent in 2016. That India managed to achieve this high growth in the aftermath of demonetisation and amidst the global slowdown, along with a macro-economic environment of relatively lower inflation (unlike a generally higher inflation in the previous episodes of high growth), moderate current account deficit coupled with broadly stable rupee-dollar exchange rate and the economy treading decisively on the fiscal consolidation path, makes it quite creditable. Most external debt indicators also point towards an improvement as at end September 2016.

However, challenges abound. The investment to GDP ratio has not only been lower than the desirable levels but has been consistently declining over the last few years. This trend needs to be reversed at the earliest in order to realise higher and lasting economic growth. Similarly, the savings rate will have to be raised, so that investment can be financed without resorting to high dose of external financing. After remaining fairly stable for much of the last twojears, international prices of crude oil have started to trend up. This along with rise in the prices of other commodities like coal, etc. could exert inflationary pressure and have the potential to adversely impact the trade and fiscal balances. The outlook for the next financial year suggests that growth is set to recover, as the currency in circulation returns to normal levels and taking into account the significant reform measures initiated by the government.

I. INTRODUCTION

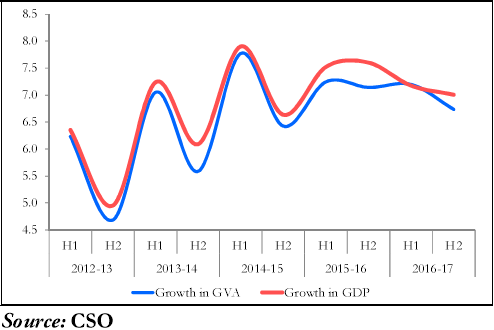

8.1 As per the first Advance Estimates (AE) released by the CSO, the Indian economy is estimated to register a GDP growth rate of 7.1 per cent in 2016-17. (There is a likelihood of this growth being revised downwards in the subsequent revisions carried out by the CSO). The growth in the second half of 2016-17 works out to 7.0 per cent as against 7.2 per cent in the first half (Figure 1). The first AE released by CSO in early January 2017 were arrived at based on data mainly up to October and in some cases up to November 2016 and hence largely mirror the economic situation during the first seven to eight months of the financial year.

Figure 1. Growth in GDP and GVA at constant prices (per cent)

8.2 As per the first AE, the growth rate of gross value added (GVA) at constant basic prices for 2016-17 is placed at 7.0 per cent, as against 7.2 per cent in 2015-16. The growth in the second half of 2016-17 is estimated at 6.7 per cent as against 7.2 per cent in the first half (Figure 1). The sector-wise details are presented in the Table 1.

8.3 At the sectoral level, growth of agriculture & allied sectors improved significantly in 2016-17, following the normal monsoon in the current year which was preceded by sub-par monsoon rainfall in 2014-15 and 2015-16. Higher growth in agriculture sector in 2016-17 is not surprising; rabi sowing so far and the first advance estimates of the kharif crop production for the year attest to this. After achieving a real growth of 7.4 per cent in terms of value added in 2015-16, the growth in industrial sector, comprising mining & quarrying, manufacturing, electricity, gas & water supply, and construction sectors moderated in 2016-17. This is in tandem with the moderation in manufacturing, mostly on account of a steep contraction in capital goods, and consumer non-durable segments

Table 1. Growth Rate of GVA at Basic Prices for Different Sectors (per cent)

| Sector | 2012-13a | 2013-14a | 2014-15b | 2015-16c | 2016-17d | 2016-17 | |

| H1 | H2 | ||||||

| Agriculture, forestry & fishing | 1.5 | 4.2 | -0.2 | 1.2 | 4.1 | 2.5 | 5.2 |

| Industry | 3.6 | 5.0 | 5.9 | 7.4 | 5.2 | 5.6 | 4.9 |

| Mining & quarrying | -0.5 | 3.0 | 10.8 | 7.4 | -1.8 | -0.9 | -2.6 |

| Manufacturing | 6.0 | 5.6 | 5.5 | 9.3 | 7.4 | 8.1 | 6.7 |

| Electricity, gas, water supply, etc | 2.8 | 4.7 | 8.0 | 6.6 | 6.5 | 6.4 | 6.6 |

| Construction | 0.6 | 4.6 | 4.4 | 3.9 | 2.9 | 2.5 | 3.4 |

| Services | 8.1 | 7.8 | 10.3 | 8.9 | 8.8 | 9.2 | 8.4 |

| Trade, hotel, transport, storage | 9.7 | 7.8 | 9.8 | 9.0 | 6.0 | 7.6 | 4.5 |

| Financial, real estate & professional services | 9.5 | 10.1 | 10.6 | 10.3 | 9.0 | 8.8 | 9.2 |

| Public administration, defence, etc. | 4.1 | 4.5 | 10.7 | 6.6 | 12.8 | 12.4 | 13.2 |

| GVA at basic prices | 5.4 | 6.3 | 7.1 | 7.2 | 7.0 | 7.2 | 6.7 |

Source: CSO

Note: a=second revised estimate; b=first revised estimate c=provisional estimate; d= first advance estimate

of Index of Industrial Production (IIP). The contraction in mining and quarrying largely reflects slowdown in the production of crude oil and natural gas. However, the performance of industrial sector in terms of value added continued to be at variance with its achievements based on IIP. As in the previous years, the service sector continued to be the dominant contributor to the overall growth of the economy, led by a significant pick-up in public administration, defence & other services, that were boosted by the payouts of the Seventh Pay Commission. Consequently, the growth in services in 2016-17 is estimated to be close to what it was in 2015-16 (Table 1).

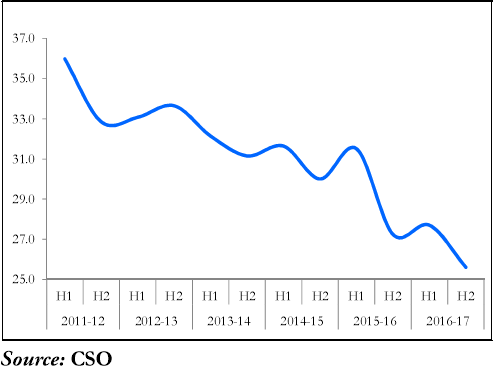

8.4 Fixed investment (gross fixed capital formation(GFCF)) to GDP ratio (at current prices) is estimated to be 26.6 per cent in 2016-17, vis-à-vis 29.3 per cent in 2015-16. The growth in fixed investment at constant prices declined from 3.9 per cent in 2015- 16 to (-) 0.2 per cent in 2016-17. Fixed investment rate has been declining since 2011-12 (Figure 2) and this trend has to be reversed for medium to long term growth prospects. Being aware of the need to boost investment and growth, Government, in co-ordination with the Reserve Bank of India and other stakeholders, has taken a number of steps to improve the ease of doing business and to improve the balance sheet positions of banks and firms.

8.5 It is the 23.8 per cent growth in government final consumption expenditure that is the major driver of GDP growth in the current year from the demand side (Table 2). Private consumption is also projected to grow at a reasonable pace during the year. With plummeting imports of gold, silver and other bullion, acquisition of valuables by households is expected to contract in the current year. Steeper contraction in imports, compared to exports, during the first half of 2016-17 led to a sharp decline in trade deficit. Despite slowing services exports, the decline in merchandise trade deficit helped improve the position of net exports of goods and non-factor services in the national accounts.

Figure 2. GFCF as percentage of GDP

Table 2. Growth Rate of GDP at constant Prices and its components (per cent)

| Component | 2012-13a | 2013-14a | 2014-15b | 2015-16c | 2016-17d | 2016-17 | |

| H1 | H2 | ||||||

| Government final consumption | 0.5 | 0.4 | 12.8 | 2.2 | 23.8 | 16.9 | 32.4 |

| Private final consumption | 5.3 | 6.8 | 6.2 | 7.4 | 6.5 | 7.1 | 6.0 |

| Gross fixed capital formation | 4.9 | 3.4 | 4.9 | 3.9 | -0.2 | -4.4 | 4.2 |

| Change in stocks | -3.8 | -18.6 | 20.3 | 5.5 | 5.2 | 5.9 | 4.6 |

| Valuables | 2.6 | -42.2 | 15.4 | 0.3 | -33.5 | -47.9 | -19.3 |

| Exports of goods and services | 6.7 | 7.8 | 1.7 | -5.2 | 2.2 | 1.7 | 2.6 |

| Imports of goods and services | 6.0 | -8.2 | 0.8 | -2.8 | -3.8 | -7.5 | -0.1 |

| GDP | 5.6 | 6.6 | 7.2 | 7.6 | 7.1 | 7.2 | 7.0 |

II. FISCAL DEVELOPMENTS

8.6 Budget 2016-17 reaffirmed Government’s commitment to continue with fiscal consolidation and projected fiscal deficit at 3.5 per cent of GDP for the year, down from 3.9 per cent in 2015-1 6. Consolidation was sought to be achieved through a 11.9 per cent increase in the gross tax revenue (over 2015-16 PA) and significant strides in non-tax revenue and non-debt capital receipts, despite upside compulsions on the expenditure side necessitated primarily by higher pay-outs on account of the implementation of the recommendations of the Seventh Pay Commission.

8.7 The buoyancy of non-debt receipts of the Union Government, consisting of net tax revenue, non-tax revenue and non-debt capital receipts during April-November 2016 supported fiscal rectitude (Table 3). The growth in non-debt receipts at 25.8 per cent during April-November 2016 surpassed the budgeted growth rate of 16.4 per cent for the full year (over 2015-16 PA).

8.8 On the whole, tax collections, especially union excise duties and service tax, have been buoyant in the current year till November 2016 (Figure 3). Despite the possible short-term spill-over effects of the cancellation of the legal tender character of

Table 3. Non-debt receipts of the Union Government

| April-November (as per cent of BE) |

Growth in April-November (per cent) |

|||

| 2015-16 | 2016-17 | 2015-16 | 2016-17 | |

| Gross tax revenue | 53.0 | 57.2 | 20.8 | 21.5 |

| Tax (net to Centre) | 50.5 | 58.9 | 12.5 | 33.6 |

| Non tax revenue | 78.1 | 54.2 | 34.9 | 1.0 |

| Non-debt capital receipts | 25.8 | 48.5 | 180.3 | 57.1 |

| Total non-debt receipts | 53.9 | 57.4 | 20.0 | 25.8 |

Source: CGA

Note: BE-Budget Estimates

Figure 3. Growth in Central taxes (per cent)

Note: PA: Provisional Actuals

high value notes, indirect taxes grew by 36.4 per cent during the month of November 2016. The tax measures on additional resource mobilization have primarily helped this buoyancy thus far.

8.9 An average of about 34.5 per cent of the gross tax collections was realized during the fourth quarter during the five-year period, 2011-12 to 2015-16. This indicates that the achievement of the budget estimates of tax collections in the current year will depend significantly on the dynamics of economic activity and tax collections during the last quarter. In the last quater of the current year, the pace of economic activity can be affected by the demonetisation of the high domination currency and the response to the gradual re-monetization.

8.10 The realization of the gross tax revenue during April-November 2016 as ratio of the budget estimates for 2016-17 was much higher than the corresponding figure in the previous year (Table 3). Devolution to States and Union Territories during April-November 2016 also kept pace with the tax collections (Figure 4). The net resources transferred, including tax devolution, nonplan grants and Central assistance during April-November 2016 was 58 per cent of the budget estimates for the full year and a notch below the corresponding accomplishments in the previous year.