Free enterprise has enabled the creative and the acquisitive urges of man to be given expression in a way which benefits all members of society. Let free enterprise fight back now, not for itself, but for all those who believe in freedom.

– Margaret Thatcher

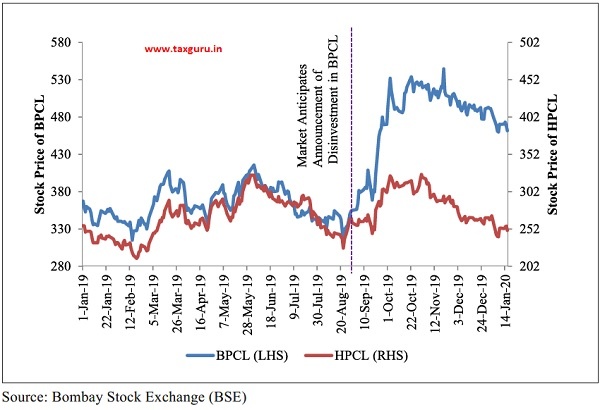

The recent approval of strategic disinvestment in Bharat Petroleum Corporation Limited (BPCL) led to an increase in value of shareholders’ equity of BPCL by Rs. 33,000 crore when compared to its peer Hindustan Petroleum Corporation Limited (HPCL)! This reflects an increase in the overall value from anticipated gains from consequent improvements in the efficiency of BPCL when compared to HPCL which will continue to be under Government control. This chapter, therefore, examines the realized efficiency gains from privatization in the Indian context. It analyses the before-after performance of 11 CPSEs that had undergone strategic disinvestment from 1999-2000 to 2003-04. To enable a careful comparison using a difference-in-difference methodology, these CPSEs are compared with their peers in the same industry group. The analysis shows that these privatized CPSEs, on an average, perform better post privatization than their peers in terms of their net worth, net profit, return on assets (ROA), return on equity (RoE), gross revenue, net profit margin, sales growth and gross profit per employee. More importantly, the ROA and net profit margin turned around from negative to positive surpassing that of the peer firms, which indicates that privatized CPSEs have been able to generate more wealth from the same resources. This improved performance holds true for each CPSE taken individually too. The analysis clearly affirms that privatization unlocks the potential of CPSEs to create wealth. The chapter, therefore, bolsters the case for aggressive disinvestment of CPSEs.

9.1 In November, 2019, India launched its biggest privatization drive in more than a decade. An “in-principle” approval was accorded to reduce Government of India’s paid-up share capital below 51 per cent in select Central Public Sector Enterprises (CPSEs). Among the selected CPSEs, strategic disinvestment of Government’s shareholding of 53.29 per cent in Bharat Petroleum Corporation Ltd (BPCL) was approved. Figure 1 shows the share price of BPCL when compared to its peer Hindustan Petroleum Corporation Limited (HPCL). The Survey focuses on the difference in BPCL and HPCL prices from September 2019 onwards when the first news of BPCL’s privatization appeared.1 The comparison of BPCL with HPCL ensures that the effect of any broad movements in the stock market or in the oil industry is netted out. Figure 1 shows that the stock prices of HPCL and BPCL moved synchronously till September. However, the divergence in their stock prices started post the announcement of BPCL’s disinvestment. The increase in the stock price of BPCL when compared to the change in the price of HPCL over the same period translates into an increase in the value of shareholders’ equity of BPCL of around ` 33,000 crore. As there was no reported change in the values of other stakeholders, including employees and lenders, during this time, the ` 33,000 crore increase translates into an unambiguous increase in the BPCL’s overall firm value, and thereby an increase in national wealth by the same amount.

Figure 1: Comparison of Stock Prices of BPCL and HPCL

9.2 As stock markets reflect the current value of future cash flows of a firm, the increase in value reflected anticipated gains from improvements in the efficiency of BPCL when compared to HPCL, which will continue to be under Government control. Strategic disinvestment is guided by the basic economic principle that Government should discontinue its engagement in manufacturing/ producing goods and services in sectors where competitive markets have come of age. Such entities would most likely perform better in the private hands due to various factors e.g. technology up-gradation and efficient management practices; and would thus create wealth and add to the economic growth of the country. Therefore, the increase in BPCL’s value when compared to HPCL reflects these anticipated gains. A large literature in financial economics spanning a large number of countries establishes very clearly that privatization brings in significant efficiency gains from the sources mentioned above (see Box 2). The experience of the UK under the leadership of Ms. Margaret Thatcher is particularly noteworthy in this context (see Box 1).

Box 1: UK Model of Privatization

The British privatization programme started in 1980 under the stewardship of then Prime Minister of United Kingdom (UK), Margaret Thatcher. In the initial phase (1979-81), the focus was on privatizing already profitable entities to raise revenues and thus reduce public-sector borrowing like in British Aerospace and Cable & Wireless. In the next phase (1982-86), focus shifted to privatizing core utilities and the government sold off Jaguar, British Telecom, the remainder of Cable & Wireless and British Aerospace, Britoil and British Gas. In the most aggressive phase (1987-91), British Steel, British Petroleum, Rolls Royce, British Airways, water and electricity were sold.

The dominant method was through an initial public offering (IPO) of all or a portion of company shares. British Aerospace was privatized in 1981 with an IPO of 52 per cent of its shares, with remaining shares unloaded in later years. The British Telecom (BT) IPO in 1984 was a mass share offering, and more than two million citizens participated in the largest share offering in world history to that date. The OECD (2003: 24) called the BT privatization “the harbinger of the launch of large-scale privatizations” internationally. In subsequent years, the British government proceeded with large public share offerings in British Gas, British Steel, electric utilities, and other companies. A second privatization method is a direct sale or trade sale, which involves the sale of a company to an existing private company through negotiations or competitive bidding. For example, the British government sold Rover automobiles and Royal Ordnance to British Aerospace. Other privatizations through direct sale included British Shipbuilders, Sealink Ferries, and The Tote. A third privatization method is an employee or management buyout. Britain’s National Freight Corporation was sold to company employees in 1982, and London’s bus services were sold to company managers and employees in 1994.

In most cases, British privatizations went hand-in-hand with reforms of regulatory structures. The government understood that privatization should be combined with open competition when possible. British Telecom, for example, was split from the post office and set up as an arms-length government corporation before shares were sold to the public. Then, over time, the government opened BT up to competition. The British government opened up intercity bus services to competition beginning in 1980. That move was followed by the privatization of state-owned bus lines, such as National Express. Numerous British seaports were privatized during the 1980s, and the government also reformed labour union laws that had stifled performance in the industry. Florio (2004) in his extensive research on UK privatization has found that the divestiture benefited shareholders and employee (especially managers), small impact on firms and other employees. Sector specific studies (Affuso, Angeriz, & Pollitt, 2009) found that privatization in train companies in UK was associated with increased efficiency. Parker (2004) found that the privatization facilitated creation of competitive market.

Box 2: Evidence on the Benefits of Privatization

Brown et al. (2015) found that the average privatization effects are estimated to be significantly positive, about 5-12 per cent, but these vary across countries and time periods. There is evidence of significant positive impacts for better quality firms and in better macroeconomic and institutional environments. Chibber and Gupta (2017) showed that disinvestment has a very strong positive effect on labour productivity and overall efficiency of PSUs in India. O’ Toole et al. (2016) in their study from Vietnam find that privatization improves capital allocation and economic efficiency. Chen et al. (2008) showed that there is a significant improvement in performance of Chinese companies after transfer of ownership control, largely due to cost reductions but only when the new owner is a non-state entity.

Subramanian, K. and Megginson, W (2018) found that stringent employment protection laws (EPL) are a deterrent to privatization, and the effect of EPL on privatization is disproportionately greater in industries with higher relocation rates and in less productive industries. Megginson and Netter (2001), Boardman and Vining (1989), La Porta and Lopez de Silanes (1999) found that in the post-privatization period, firms show significantly higher profitability, higher efficiency, generally higher investment levels, higher output, higher dividends, and lower leverage post privatization. According to Gupta (2005), both the levels and growth rates of profitability, labour productivity, and investment spending improve significantly following partial privatization. Majumdar (1996) documented that efficiency levels are significantly higher than state owned enterprises which show efficiency only during efficiency drives only to decline afterwards based on a study of Indian firms over the period 1973-89.

Borisova and Megginson (2010) indicated that on an average across firms, a one percentage point decrease in government ownership is associated with an increase in the credit spread, used as a proxy for the cost of debt, by three-quarters of a basis point. According to Li et al. (2016), profitability of newly privatized companies increases significantly (by 2-3 percentage points) after adjusting for negative listing effect. Capital spending and sales growth also improve significantly based on triple difference-in-difference tests. Wolf and Pollitt (2008) showed that privatization is associated with significant and comprehensive performance improvements over 7-year period (−3 to +3 years). Oum et al. (2006) provides strong evidence that airports with majority government ownership and those with multi-level government ownership are significantly less efficient than those with private majority ownership. Increased customer satisfaction comes in form of reduction in tariffs, increased data usage etc. in the telecommunication sector; increased penetration of banking services in the rural areas; and reduced air-fares comparable to high-end consumers in the railways.

9.3 To examine the efficiency gains from privatization and whether the purported benefits of privatization have indeed manifested in the Indian context, this chapter analyses the before-after performance of 11 CPSEs that had undergone strategic disinvestment from 1999-2000 to 2003-04. To provide a historical context for the current disinvestment drive, Box 3 summarizes the evolution of disinvestment policy in India.

Box 3: Evolution of Disinvestment Policy in India

The liberalization reforms undertaken in 1991 ushered in an increased demand for privatization/ disinvestment of PSUs. In the initial phase, this was done through the sale of minority stake in bundles through auction. This was followed by separate sale for each company in the following years, a method popularly adopted till 1999-2000. India adopted strategic sale as a policy measure in 1999-2000 with sale of substantial portion of Government shareholding in identified Central PSEs (CPSEs) up to 50 per cent or more, along with transfer of management control. This was started with the sale of 74 per cent of the Government’s equity in Modern Food Industries Limited (MFIL). Thereafter, 12 PSUs (including four subsidiaries of PSUs), and 17 hotels of Indian Tourism Development Corporation (ITDC) were sold to private investors along with transfer of management control by the Government.

In addition, 33.58 per cent shareholding of Indo Bright Petroleum (IBP) strategically sold to Indian Oil Corporation (IOC). IBP, however, remained a PSU after this strategic sale, since IOC held 53.58 per cent of its paid-up equity. Another major shift in disinvestment policy was made in 2004-05 when it was decided that the government may “dilute its equity and raise resources to meet the social needs of the people”, a distinct departure from strategic sales.

Strategic Sales have got a renewed push after 2014. During 2016-17 to 2018-19, on average, strategic sales accounted for around 28.2 per cent of total proceeds from disinvestment. Department of Investment and Public Asset Management (DIPAM) has laid down comprehensive guidelines on “Capital Restructuring of CPSEs” in May, 2016 by addressing various aspects, such as, payment of dividend, buyback of shares, issues of bonus shares and splitting of shares. The Government has been following an active policy on disinvestment in CPSEs through the various modes:

i. Disinvestment through minority stake sale in listed CPSEs to achieve minimum public shareholding norms of 25 per cent. While pursuing disinvestment of CPSEs, the Government will retain majority shareholding, i.e., at least 51 per cent and management control of the Public Sector Undertakings;

ii. Listing of CPSEs to facilitate people’s ownership and improve the efficiency of companies through accountability to its stake holders – As many as 57 PSUs are now listed with total market capitalisation of over ` 13 lakh crore.

iii. Strategic Disinvestment;

iv. Buy-back of shares by large PSUs having huge surplus;

v. Merger and acquisitions among PSUs in the same sector;

vi. Launch of exchange traded funds (ETFs) – an equity instrument that tracks a particular index. The CPSE ETF is made up of equity investments in India’s major public sector companies like ONGC, REC, Coal India, Container Corp, Oil India, Power Finance, GAIL, BEL, EIL, Indian Oil and NTPC; and

vii. Monetization of select assets of CPSEs to improve their balance sheet/reduce their debts and to meet part of their capital expenditure requirements.

NITI Aayog has been mandated to identify PSUs for strategic disinvestment. For this purpose, NITI Aayog has classified PSUs into “high priority” and “low priority”, based on (a) National Security (b) Sovereign functions at arm’s length, and (c) Market Imperfections and Public Purpose. The PSUs falling under “low priority” are covered for strategic disinvestment. To facilitate quick decision making, powers to decide the following have been delegated to an Alternative Mechanism in all the cases of Strategic Disinvestment of CPSEs where Cabinet Committee on Economic Affairs (CCEA) has given ‘in principle’ approval for strategic disinvestment:

(i) The quantum of shares to be transacted, mode of sale and final pricing of the transaction or lay down the principles/ guidelines for such pricing; and the selection of strategic partner/ buyer; terms and conditions of sale; and

(ii) To decide on the proposals of Core Group of Disinvestment (CGD) with regard the timing, price, terms & conditions of sale, and any other related issue to the transaction.

On November 20, 2019, the government announced that full management control will be ceded to buyers of Bharat Petroleum Corporation Ltd. (BPCL), Shipping Corporation of India (SCI) and Container Corporation of India Ltd (CONCOR). On January 8, 2020, strategic disinvestment was approved for Minerals & Metals Trading Corporation Limited (MMTC), National Mineral Development Corporation (NMDC), MECON and Bharat Heavy Electricals Ltd. (BHEL).

IMPACT OF PRIVATIZATION: A FIRM LEVEL ANALYSIS

9.4 To assess the impact of strategic disinvestment/privatization on performance of select CPSEs before and after privatization, 11 CPSEs are studied, that had undergone strategic disinvestment from 1999-2000 to 2003-04 for which data is available both before and after privatization.2 To enable careful comparison using a difference-indifference methodology, these CPSEs have been compared with their peers in the same industry group (Table 1). Box 4 gives an explanation of the difference-in-difference methodology.

Table 1: List of Selected CPSEs and Peers

| Industry Group | Privatized CPSE | Peers |

| Metals Non Ferrous | Hindustan Zinc | Tinplate Co. Of India, Hindustan Copper, Vedanta |

| Aluminium& Aluminium Products | Bharat Aluminium Company Ltd. (BALCO) | NALCO, Hindalco, PG Foils |

| Computers, peripherals & storage devices | Computer Management Corporation Ltd. (CMC) | Moserbear, Zenith Computers, Izmo Limited |

| Automobile | Maruti Suzuki | Ashok Leyland Ltd, Tata Motors.,Mahindra & Mahindra Ltd |

| Petrochemicals

|

Indian Petrochemicals Corporation Ltd. (IPCL) | Chemplast Sanmar, Bhansali Engineering Polymers, Ineos Styrolution India Ltd |

| Telecommunication Services | Tata Communications | Tata Teleservices, MTNL, GTL infra |

| Heavy Engineering | Lagan Engineering | Gujarat Toolroom, Gujarat Textronics, Integra Engineering India Ltd. |

| Medium & Light Engineering | Jessop &Co. | Elgi Ultra, Disa India, Alfa Laval, Filtron Engineers |

| Bakery Products

|

Modern Food India Ltd. (MFIL) | Britannia |

| Wires and Cables

|

Hindustan Teleprinters (HTL) | Anamika Conductors, Delton Cables, Fort Gloster Ltd |

| Chemicals and Fertilizers | Paradeep Phosphates

|

GSFC, Fertilizers & Chemicals- Travancore, Godavari Chemicals and Fertilizers |

| Total | 11 | 32 |

Source: Survey calculations based on data from CMIE Prowess

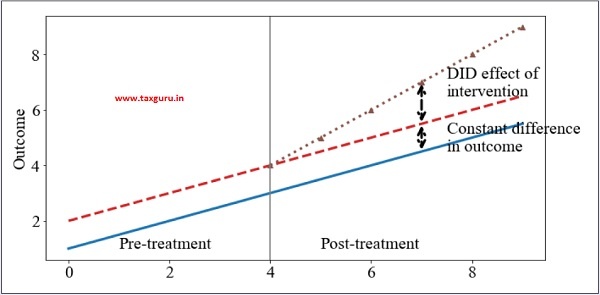

Box 4: Difference-in-Differences Methodology

Difference-in-differences (DiD) is a statistical technique used to estimate the effect of a specific intervention or treatment (such as a passage of law, enactment of policy, or large-scale program implementation). The technique compares the changes in outcomes over time between a population that is affected by the specific intervention (the treatment group) and a population that is not (the control group). DiD is typically used to mitigate the possibility of any extraneous factors affecting the estimated impact of an intervention. This is accomplished by differencing the estimated impact of the treatment on the outcome in the treatment group as compared to the control group.

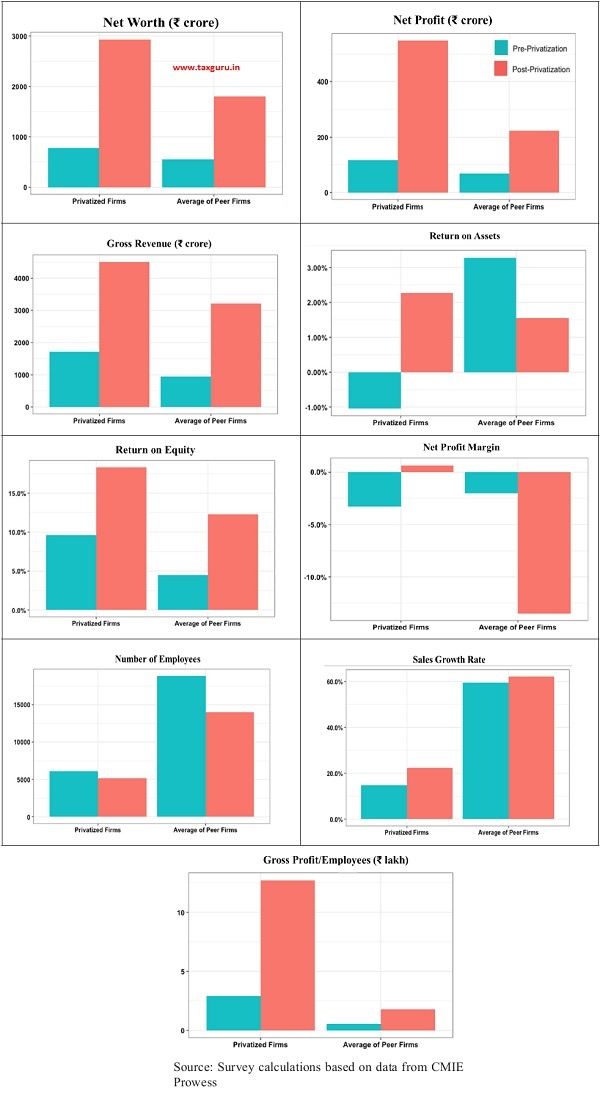

9.5 Figure 2 shows the average performance of these CPSEs using various financial indicators as compared to their peers for ten years before and after the year of privatization of the specific CPSE.3 It is clear from Figure 2 that the performance of privatized firms, after

controlling for other confounding factors using the difference in performance of peer firms over the same period, improves significantly following privatization.

Figure 2: Comparison of Financial Indicators of Privatized Firms vis-à-vis Peers

9.6 The differences for each metric are described in detail below.

i) Net worth: The net worth of a company is what it owes its equity shareholders. This consists of equity capital put in by shareholders, profits generated and retained as reserves by the company. On an average, the net worth of privatized firms increased from `700 crore before privatization to ` 2992 crore after privatization, signalling significant improvement in financial health and increased wealth creation for the shareholders (Table 2). Difference in difference (DiD) analysis attributes an increase of ` 1040.38 crore in net worth due to privatization.

Table 2: Net Worth (` Crore)

| Name of privatized CPSE | Pre average | Post average | Post minus Pre |

| 1 BALCO | 656.25 | 1921.60 | 1265.35 |

| 2 CMC | 35.28 | 275.41 | 240.13 |

| 3 Maruti | 1426.02 | 8191.98 | 6765.96 |

| 4 Jessop | -212.07 | 77.19 | 289.26 |

| 5 Lagan Engineering | 5.15 | 6.30 | 1.15 |

| 6 IPCL | 2258.52 | 3106.69 | 848.17 |

| 7 HTL | 33.35 | -145.98 | -179.33 |

| 8 Hindustan Zinc | 818.06 | 12874.57 | 12056.51 |

| 9 Modern Food India | 10.63 | -79.34 | -89.97 |

| 10 Paradeep Phosphates | -3.98 | 214.12 | 218.1 |

| 11 Tata Communications | 2683.82 | 6468.49 | 3784.67 |

| 12 Combined average of all privatized firms | 701.00 | 2991.91 | 2290.91 |

| 13 Combined average of peer firms | 551.61 | 1802.14 | 1250.53 |

| 14 Privatized firm minus peer firms | 149.39 | 1189.77 | DiD = 1040.38 |

Source: Survey calculations based on data from CMIE Prowess

ii) Net Profit: This is the net profit of the company after tax. An increase in net profit indicates greater realizations from the company after incurring all the operational expenses. On an average, the net profit of privatized firms increased from Rs. 100 crore before privatization to Rs. 555 after privatization compared to the peer firms (Table 3 below). DiD analysis attributes an increase of Rs. 300.27 crore in net profit due to privatization.

Table 3: Net Profit (Rs. Crore)

| Name of privatized CPSE | Pre average | Post average | Post minus Pre |

| 1 BALCO | 45.47 | 348.94 | 303.47 |

| 2 CMC | 6.77 | 73.22 | 66.45 |

| 3 Maruti | 205.28 | 1321.99 | 1116.71 |

| 4 Jessop | -36.44 | 7.87 | 44.31 |

| 5 Lagan Engineering | -0.49 | 0.18 | 0.67 |

| 6 IPCL | 238.48 | 606.42 | 367.94 |

| 7 HTL | 3.16 | -43.84 | -47 |

| 8 Hindustan Zinc | 72.47 | 3237.04 | 3164.57 |

| 9 Modern Food India | -1.2 | -18.4 | -17.2 |

| 10 Paradeep Phosphates | -53.93 | 114.83 | 168.76 |

| 11 Tata Communications | 620.34 | 452.25 | -168.09 |

| 12 Combined average of all privatized firms | 100 | 554.6 | 454.6 |

| 13 Combined average of peer firms | 68.51 | 222.84 | 154.33 |

| 14 Privatized firm minus peer firms | 31.49 | 331.76 | DiD=300.27 |

(iii) Gross Revenue: On an average, the gross revenue of privatized firms increased from ` 1560 crore to before privatization to ` 4653 crore after privatization, signalling increase in income from sales of goods and other nonfinancial activities (Table 4). DiD analysis attributes an increase of ` 65 crore in gross revenue due to privatization.

(iv) Return on assets (ROA): ROA captures the ratio of profits after taxes (PAT) to the total average assets of the company, expressed in percentage terms. On an average, ROA for the privatized firms have turned around from (-)1.04 per cent to 2.27 per cent surpassing the peer firms which indicates that privatized firms have been able to use their resources more productively (Table 5). DiD analysis attributes an increase of 5.04 per cent in ROA due to privatization.

Table 4: Gross Revenue (Rs. Crore)

| Name of privatized CPSE | Pre average | Post average | Post minus Pre |

| 1 BALCO | 747.84 | 2858.48 | 2110.64 |

| 2 CMC | 261.55 | 792.88 | 531.33 |

| 3 Maruti | 6013.28 | 22958.8 | 16945.52 |

| 4 Jessop | 79.76 | 178.33 | 98.57 |

| 5 Lagan Engineering | 6.52 | 12.87 | 6.35 |

| 6 IPCL | 3791.56 | 9341.25 | 5549.69 |

| 7 HTL | 141.21 | 126.89 | -14.32 |

| 8 Hindustan Zinc | 999.16 | 7923.77 | 6924.61 |

| 9 Modern Food India | 77.21 | 192.6 | 115.39 |

| 10 Paradeep Phosphates | 824.52 | 2692.56 | 1868.04 |

| 11 Tata Communications | 4219.51 | 4106.69 | -112.82 |

| 12 Combined average of all privatized firms | 1560.19 | 4653.19 | 3093 |

| 13 Combined average of peer firms | 945.42 | 3210.77 | 2265.35 |

| 14 Privatized firm minus peer firms | 614.77 | 1442.42 | DiD=827.65 |

Source: Survey calculations based on data from CMIE Prowess

Table 5: Return on Assets (per cent)

| Name of privatized CPSE | Pre average | Post average | Post minus Pre |

| 1 BALCO | 4.62 | 6.84 | 2.22 |

| 2 CMC | -0.89 | 8.7 | 9.59 |

| 3 Maruti | 8.24 | 10.29 | 2.05 |

| 4 Jessop | -35.95 | 4.34 | 40.29 |

| 5 Lagan Engineering | -2.19 | 0.78 | 2.97 |

| 6 IPCL | 4.34 | 6.74 | 2.4 |

| 7 HTL | -3.12 | -24.17 | -21.05 |

| 8 Hindustan Zinc | 5.29 | 26.7 | 21.41 |

| 9 Modern Food India | 3.35 | -39.5 | -42.85 |

| 10 Paradeep Phosphates | -8.78 | 2.57 | 11.35 |

| 11 Tata Communications | 13.4 | 4.03 | -9.37 |

| 12 Combined average of all privatized firms | -1.04 | 2.27 | 3.31 |

| 13 Combined average of peer firms | 3.28 | 1.55 | -1.73 |

| 14 Privatized firm minus peer firms | -4.32 | 0.72 | DiD=5.04 |

Source: Survey calculations based on data from CMIE Prowess

v) Return on equity (ROE): Return on equity (ROE) is profit after tax (PAT) as percentage of average net worth. On an average, the ROE of privatized firms increased from 9.6 per cent before privatization to 18.3 per cent after privatization, reflecting increase in firm’s efficiency at generating profits from every unit of shareholders’ equity. For the average peer group, the increase in ROE over pre privatization period was 7.8 per cent (Table 6). DiD analysis attributes an increase of 0.89 per cent in ROE due to privatization.

Table 6: Return on Equity (per cent)

| Name of privatized CPSE | Pre average | Post average | Post minus Pre |

| 1 BALCO | 6.1 | 16.9 | 10.8 |

| 2 CMC | 11.2 | 26.6 | 15.4 |

| 3 Maruti | 19 | 16.6 | -2.4 |

| 4 Jessop | 5 | 12.9 | 7.9 |

| 5 Lagan Engineering | -4.5 | 1.4 | 5.9 |

| 6 IPCL | 11.2 | 17.9 | 6.7 |

| 7 HTL | 9.8 | 2.3 | -7.5 |

| 8 Hindustan Zinc | 9.2 | 28.8 | 19.6 |

| 9 Modern Food India | 11.4 | 27.8 | 16.4 |

| 10 Paradeep Phosphates | 3.5 | -0.1 | -3.6 |

| 11 Tata Communications | -44.8 | 7.3 | 52.1 |

| 12 Combined average of all privatized firms | 9.6 | 18.3 | 8.7 |

| 13 Combined average of peer firms | 4.5 | 12.31 | 7.81 |

| 14 Privatized firm minus peer firms | 5.1 | 5.99 | DiD=0.89 |

Source: Survey calculations based on data from CMIE Prowess

vi) Net profit margin: Net profit margin of a company is PAT as percentage of total income. On an average, the net profit margin of privatized firms increased from (-3.24) per cent before privatization to 0.65 per cent after privatization, reflecting that out of a rupee that is generated as income, the share of after-tax profit in the income increases. For the average peer group, the net profit margin has fallen to (-13.4) per cent in the post privatization period from (-2.03) per cent in the pre privatization period (Table 7). DiD analysis attributes an increase of 15.26 per cent in net profit margin due to privatization.

Table 7: Net profit margin (per cent)

| Name of privatized CPSE | Pre average | Post average | Post minus Pre |

| 1 BALCO | 5.8 | 10.1 | 4.3 |

| 2 CMC | 1.9 | 9.1 | 7.2 |

| 3 Maruti | 6.5 | 34.3 | 27.8 |

| 4 Jessop | 2.9 | -66.9 | -69.8 |

| 5 Lagan Engineering | 6.7 | 5.9 | -0.8 |

| 6 IPCL | -65 | 5.8 | 70.8 |

| 7 HTL | -3.1 | -0.2 | 2.9 |

| 8 Hindustan Zinc | 3.7 | 5.9 | 2.2 |

| 9 Modern Food India | -2.1 | -9.8 | -7.7 |

| 10 Paradeep Phosphates | -6.6 | 1.8 | 8.4 |

| 11 Tata Communications | 13.7 | 11.1 | -2.6 |

| 12 Combined average of all privatized firms | -3.24 | 0.65 | 3.89 |

| 13 Combined average of peer firms | -2.03 | -13.4 | -11.37 |

| 14 Privatized firm minus peer firms | -1.21 | 14.05 | DiD= 15.26 |

Source: Survey calculations based on data from CMIE Prowess

(vii) Sales growth: On an average, growth rate of sales of privatized firms increased from 14.7 per cent before privatization to 22.3 per cent after privatization (Table 8). DiD analysis attributes 4.9 per cent increase in sales growth due to privatization.

(viii) Gross profit per employee: Figure 2 shows that on average, the number of employees has declined for both set of firms, but the reduction is lesser in magnitude as compared to its peers. Gross profit per employee has been estimated for only 8 out of the selected eleven CPSEs as per the availability of relevant data. DiD analysis attributes an increase of ` 21.34 lakh in gross profit per employee due to privatization (Table 9).

Table 8: Sales growth y-o-y (per cent)

| Name of privatized CPSE | Pre average | Post average | Post minus Pre |

| 1 BALCO | 7.87 | 22.25 | 14.38 |

| 2 CMC | 20.19 | 4.66 | -15.53 |

| 3 Maruti | 20.26 | 16.18 | -4.08 |

| 4 Jessop | -2.45 | 17.26 | 19.71 |

| 5 Lagan Engineering | 0.22 | 17.05 | 16.83 |

| 6 IPCL | 14.33 | 23.90 | 9.58 |

| 7 HTL | 19.29 | 82.10 | 62.81 |

| 8 Hindustan Zinc | 10.44 | 28.34 | 17.90 |

| 9 Modern Food India | 18.36 | 4.02 | -14.34 |

| 10 Paradeep Phosphates | 6.41 | 32.39 | 25.99 |

| 11 Tata Communications | 46.58 | -2.94 | -49.52 |

| 12 Combined average of all privatized firms | 14.68 | 22.29 | 7.61 |

| 13 Combined average of peer firms | 59.37 | 62.09 | 2.72 |

| 14 Privatized firm minus peer firms | -44.69 | -39.80 | DiD =4.89 |

Table 9: Gross profit/employee (Rs. lakh)

| Name of privatized CPSE | Pre average | Post average | Post minus Pre |

| 1 BALCO | 0.46 | 10.87 | 10.42 |

| 2 CMC | 0.17 | 1.49 | 1.32 |

| 3 Maruti | 4.75 | 21.01 | 16.26 |

| 4 Jessop | -1.06 | 0.77 | 1.82 |

| 5 IPCL | 1.89 | 4.14 | 2.26 |

| 6 Hindustan Zinc | 0.26 | 166.66 | 166.40 |

| 7 Paradeep Phosphates | -6.02 | -14.96 | -8.94 |

| 8 Tata Communications | 22.28 | 13.42 | -8.85 |

| 9 Combined average of all privatized firms | 2.84 | 25.43 | 22.58 |

| 10 Combined average of peer firms | 0.54 | 1.78 | 1.24 |

| 11 Privatized firm minus peer firms | 2.30 | 23.65 | DiD= 21.34 |

Source: Survey calculations based on data from CMIE Prowess

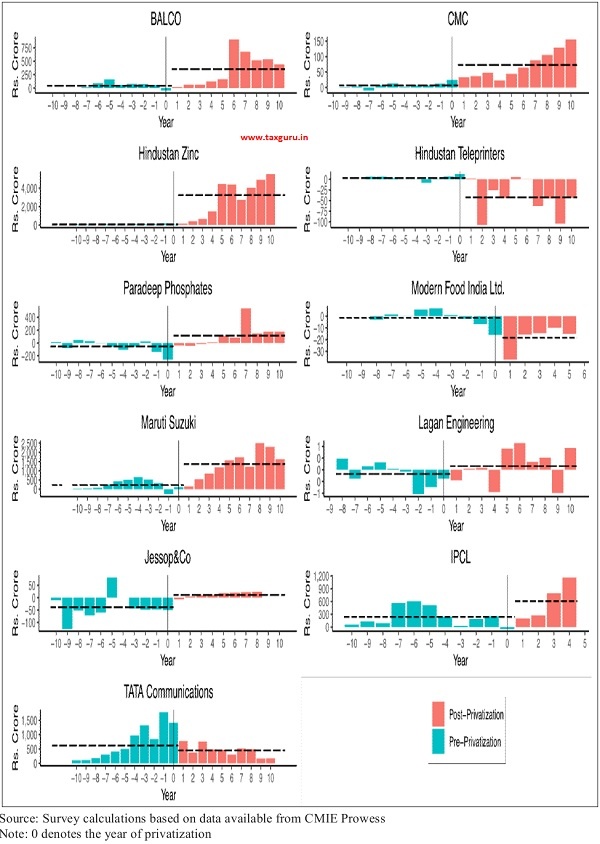

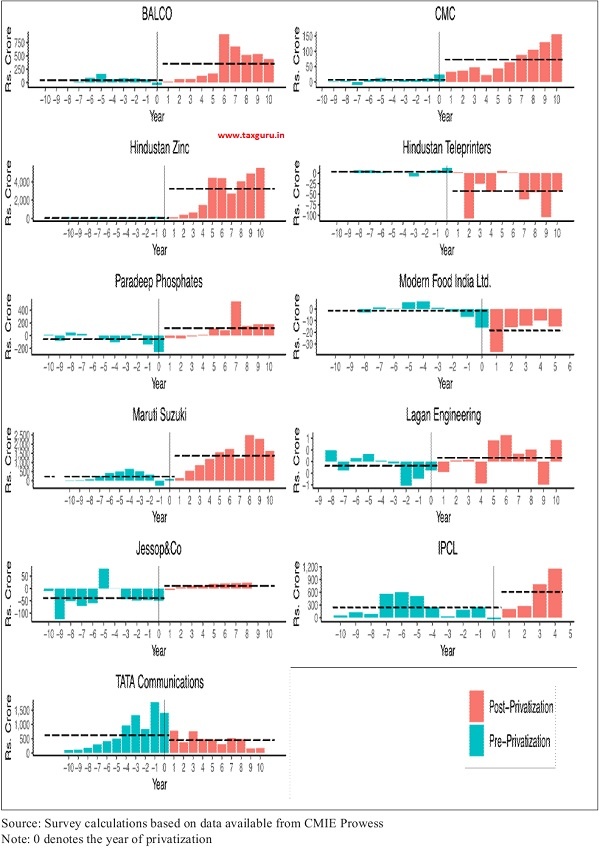

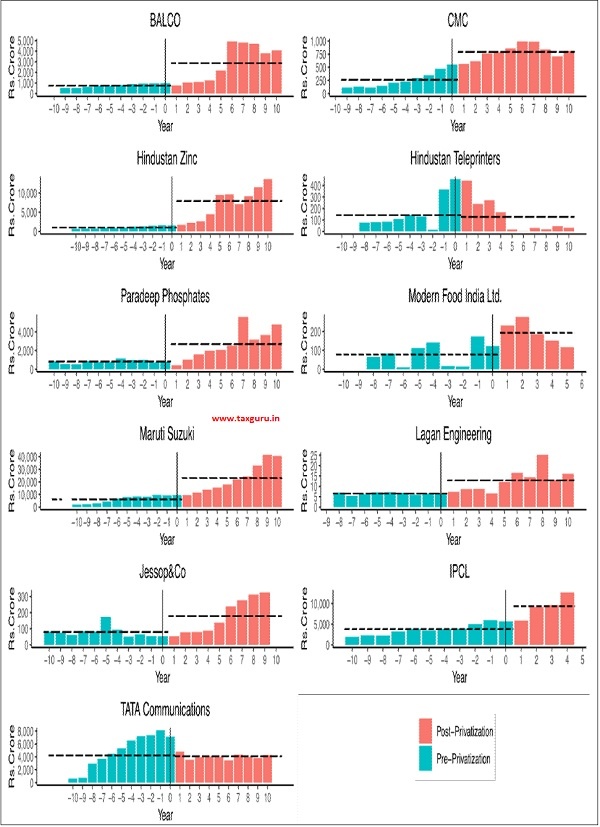

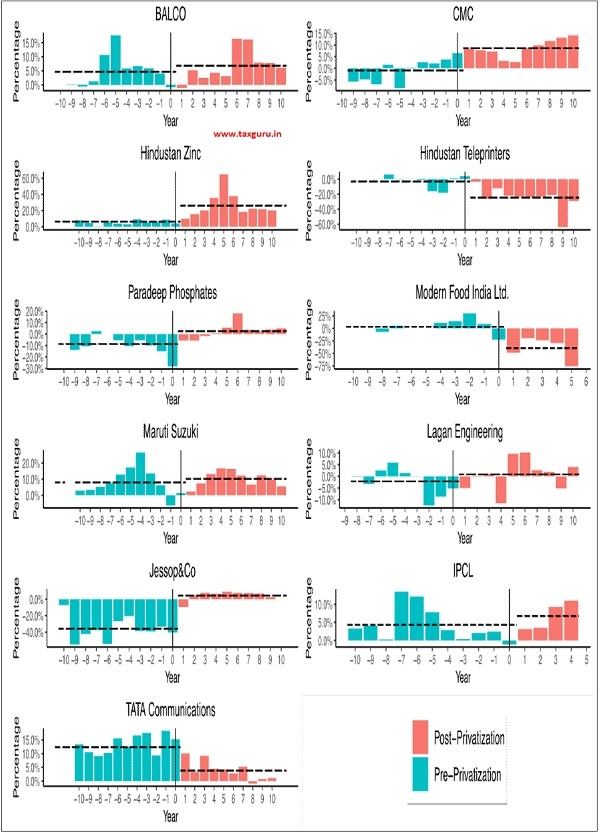

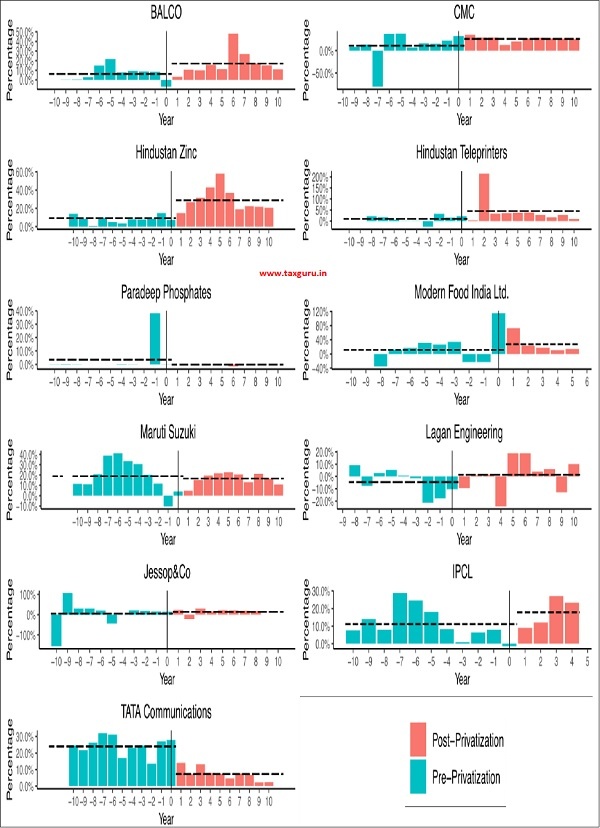

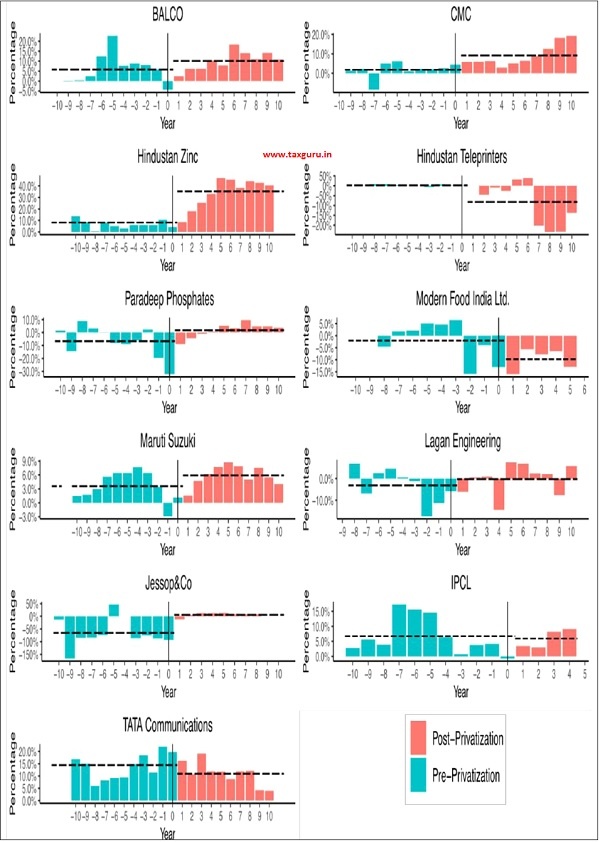

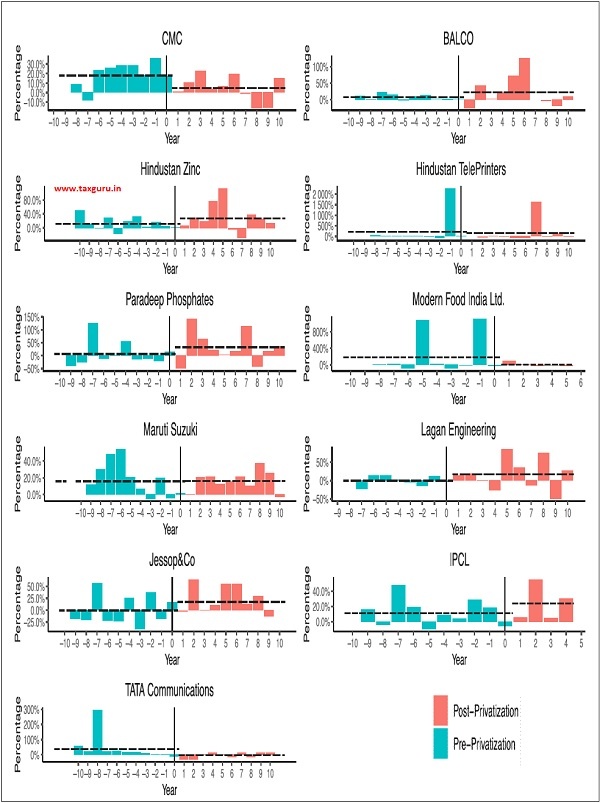

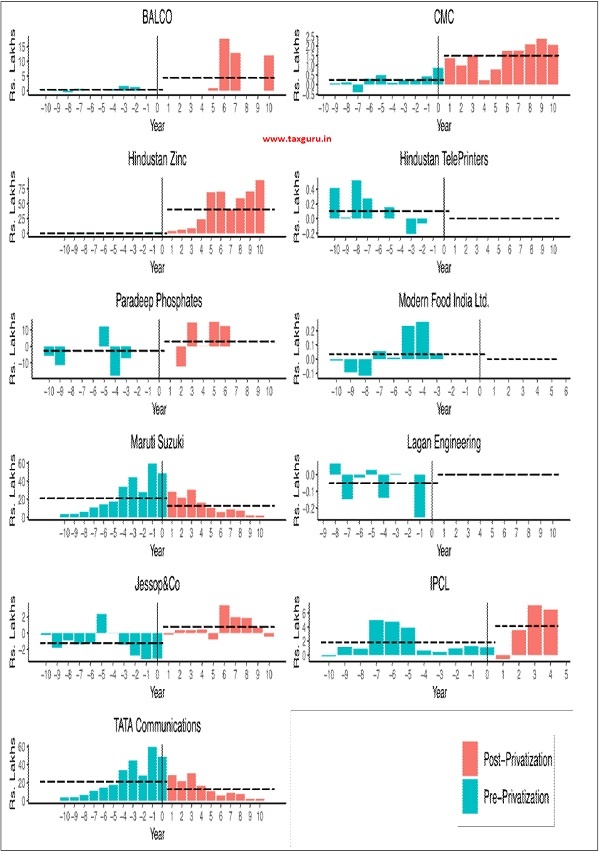

9.7 The Survey also examines the change in performance for each individual CPSE. Figures 3 to 10 show the movement in these major financial indicators for each of the firm ten years before and after the year of strategic disinvestment/privatization. Taken individually, each privatized CPSE witnessed improvement in net worth, net profit, gross revenue, net profit margin, sales growth in the post privatization period compared to pre privatization period (except for Hindustan Teleprinters, MFIL and Tata Communications in the case of few indicators).

Figure 3: Net worth of privatized firms (pre and post privatization)

Figure 4: Net Profit of privatized firms (pre and post privatization)

Figure 5: Gross Revenue of privatized firms (pre and post privatization)

Source: Survey calculations based on data available from CMIE Prowess

Note: 0 denotes the year of privatization

Figure 6: Return on Assets (ROA) of privatized firms (pre and post privatization)

Source: Survey calculations based on data available from CMIE Prowess

Note: 0 denotes the year of privatization

Figure 7: Return on Equity (ROE) of privatized firms (pre and post privatization)

Source: Survey calculations based on data available from CMIE Prowess

Note: 0 denotes the year of privatization

Figure 8: Net Profit Margin of privatized firms (pre and post privatization)

Source: Survey calculations based on data available from CMIE Prowess

Note: 0 denotes the year of privatization

Figure 9: Sales growth of privatized firms (pre and post privatization)

Source: Survey calculations based on data available from CMIE Prowess

Note: 0 denotes the year of privatization

Figure 10: Gross Profit per Employee of privatized firms (pre and post privatization)

Source: Survey calculations based on data available from CMIE Prowess

Note: 0 denotes the year of privatization

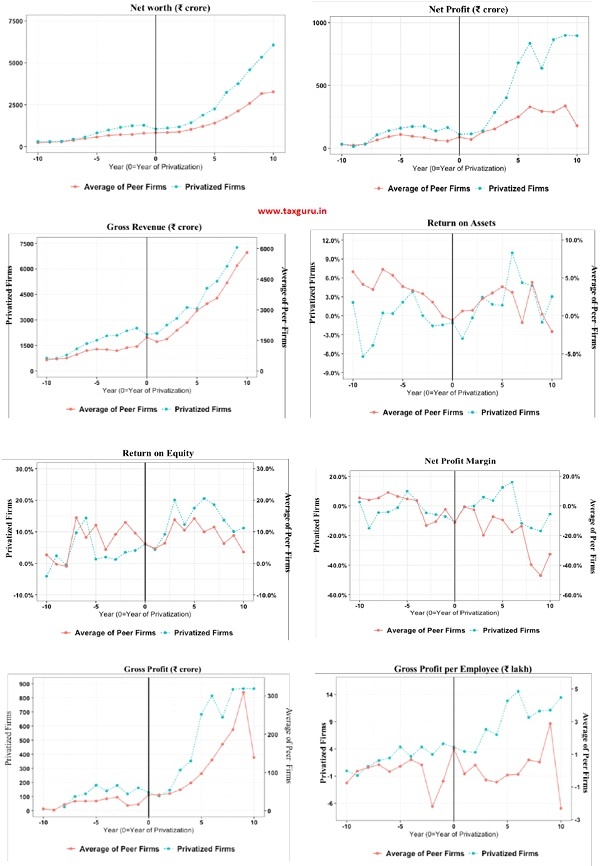

9.8 Figure 11 below shows the trend in the performance of the privatized CPSEs, on an average, as compared to their peers over the period of ten years before and after the year of privatization of the specific CPSE. The trend thereby enables us to understand the dynamic aspects of the change in performance of the privatized firms after privatization when compared to its peer firms. The trends confirm that the performance of the privatized CPSE and its peers is quite similar till the year of privatization. However, post privatization, the performance of the privatized entity improves significantly when compared to the change in the peers’ performance over the same time period.

Figure 11: Trend in Performance of privatized firms vs. Peers

Source: Survey calculations based on data available from CMIE Prowess

Way Forward

9.9 The analysis in this chapter clearly affirms that disinvestment improves firm performance and overall productivity, and unlocks their potential to create wealth. This would have a multiplier effect on other sectors of the economy. Aggressive disinvestment, preferably through the route of strategic sale, should be utilized to bring in higher profitability, promote efficiency, increase competitiveness and to promote professionalism in management in CPSEs. The focus of the strategic disinvestment needs to be to exit from non-strategic business and directed towards optimizing economic potential of these CPSEs. This would, in turn, unlock capital for use elsewhere, especially in public infrastructure like roads, power transmission lines, sewage systems, irrigation systems, railways and urban infrastructure. It is encouraging that the enabling provisions by DIPAM are already in place (as detailed in Box 3 earlier). The Cabinet has ‘in-principle’ approved the disinvestment in various CPSEs (as detailed in Annex to the chapter). These need to be taken up aggressively to facilitate creation of fiscal space and improve the efficient allocation of public resources.

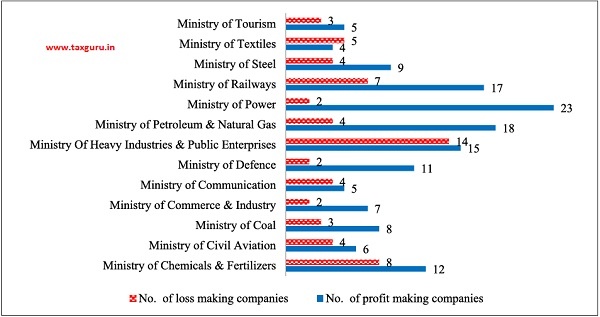

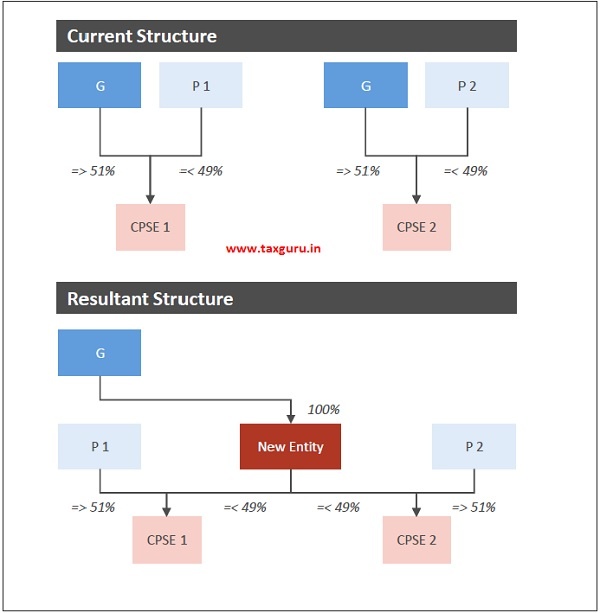

9.10 There are about 264 CPSEs under 38 different Ministries/Departments. Of these, 13 Ministries/Departments have around 10 CPSEs each under its jurisdiction. It is evident from Figure 11 that many of the CPSEs are profitable. However, CPSEs have generally underperformed the market as is evident from the average return of only 4 per cent of BSE CPSE Index against the 38 per cent return of BSE SENSEX during the period 2014-2019. The aim of any privatization or disinvestment programme should, therefore, be the maximisation of the Government’s equity stake value. The learning from the experience of Temasek Holdings Company in Singapore may be useful in this context (Box 4). The Government can transfer its stake in the listed CPSEs to a separate corporate entity (Figure 12). This entity would be managed by an independent board and would be mandated to divest the Government stake in these CPSEs over a period of time. This will lend professionalism and autonomy to the disinvestment programme which, in turn, would improve the economic performance of the CPSEs.

Figure 11: No. of CPSEs under various Ministries which are profitable

Source: Department of Public Enterprises

Figure 12: Proposed Structure for Corporatization of Disinvestment

Box 4: Temasek Holdings Ltd – Privatization Model of Singapore

Temasek Holdings was incorporated by Government of Singapore on 25 June 1974, as a private commercial entity, to hold and manage its investments in its government-linked companies (GLCs). Temasek Holdings is wholly owned by the Ministry for Finance and operates under the provisions of the Singapore Companies Act. Temasek’s board comprises 13 members—mostly non-executive and independent business leaders from the private sector. The company has since expanded its operations to cover key areas of business in sectors such as telecommunications, media, financial services, energy, infrastructure, engineering, pharmaceuticals and the bio-sciences.

Many of the original investments that Temasek managed included national treasures such as shipping firms (NOL, Keppel, Sembawang), a bank (DBS Bank), and systems engineering conglomerates (Singapore Technologies, Singapore Telecom). Temasek has retained strategically important investments, including its original stakes in all of these GLCs. Since March 2002, Temasek began diversifying its portfolio outside of Singapore such that a third of its investments are in developed markets, a third in developing countries and a third in Singapore. Some of the company’s major investments in foreign companies include Standard Chartered, ICICI Bank (India), Bank Danamon (Indonesia), Telekom Malaysia and ShinCorp (Thailand). Temasek’s investments in local companies include Singapore Airlines, Singtel, DBS Bank, SMRT, ST Engineering, MediaCorp and Singapore Power.

It manages a net portfolio of over US$230 billion as on 31st March 2019 – around fourfold jump from US$66 billion in 2004. Its compounded annualised total shareholder return since inception in 1974 is 15 per cent in Singapore dollar terms.

CHAPTER AT A GLANCE

> Approval for strategic disinvestment of Government’s shareholding of 53.29 per cent in Bharat Petroleum Corporation Limited (BPCL) led to an increase of around ` 33,000 crore in the value of shareholders’ equity of BPCL when compared to Hindusta Petroleum Corporation Limited (HPCL). This translates into an unambiguous increase in the BPCL’s overall firm value, and thereby an increase in national wealth by the same amount.

> A comparative analysis of the before-after performance of 11 CPSEs that had undergone strategic disinvestment from 1999-2000 to 2003-04 reveals that net worth, net profit, return on assets (ROA), return on equity (ROE), gross revenue, net profit margin, sales growth and gross profit per employee of the privatized CPSEs, on an average, have improved significantly in the post privatization period compared to the peer firms.

> The ROA and net profit margin turned around from negative to positive surpassing that of the peer firms which indicates that privatized CPSEs have been able to generate more wealth from the same resources.

> The analysis clearly affirms that disinvestment (through the strategic sale) of CPSEs unlocks their potential of these enterprises to create wealth evinced by the improved performance after privatization.

> Aggressive disinvestment should be undertaken to bring in higher profitability, promote efficiency, increase competitiveness and to promote professionalism in management in the selected CPSEs for which the Cabinet has given in-principle approval.

REFERENCES

Affuso, L., A. Angeriz, and M. Pollitt. 2009. “The impact of privatization on the efficiency of train operation in Britain”. CGR Working Paper No. 28. Centre for Globalization Research School of Business and Management. Queen Mary University of London.

Berkman, Henk, Rebel A. Cole, and Jiang Lawrence Fu. 2012. “Improving Corporate Governance Where the State is the Controlling Block Holder: Evidence from China”. SSRN Electronic Journal.

Borisova, Ginka, and William L. Megginson. 2011. “Does Government Ownership affect the Cost of Debt? Evidence from Privatization”. Review of Financial Studies 24 (8): 2693-2737.

Boubakri, Narjess, Sadok El Ghoul, Omrane Guedhami, and William L. Megginson. 2018. “The Market Value of Government Ownership”. Journal of Corporate Finance 50: 44-65.

Brown, David J., John S. Earle, and Almos Telegdy. 2015. “Where Does Privatization Work? Understanding The Heterogeneity in Estimated Firm Performance Effects”. Journal of Corporate Finance 41: 329-362.

Brown, J. David, John S. Earle, and Almos Telegdy. 2006. “The Productivity Effects of Privatization: Longitudinal Estimates from Hungary, Romania, Russia, And Ukraine”. Journal of Political Economy 114 (1): 61-99.

Chen, Gongmeng, Michael Firth, Yu Xin, and Liping Xu. 2008. “Control Transfers, Privatization, And Corporate Performance: Efficiency Gains in China’s Listed Companies”. Journal of Financial and Quantitative Analysis 43 (1): 161-190.

Choi, Seung-Doo, Inmoo Lee, and William Megginson. 2010. “Do Privatization IPOs Outperform in The Long Run?”. Financial Management 39 (1): 153-185.

Conway, Paul, and Richard Herd. 2009. “How Competitive Is Product Market Regulation in India?”. OECD Journal: Economic Studies 2009 (1): 1-25.

Dinc, I. Serdar, and Nandini Gupta. 2011. “The Decision to Privatize: Finance and Politics”. The Journal of Finance 66 (1): 241-269.

Florio, Massimo. The great divestiture: Evaluating the welfare impact of the British privatizations, 1979-1997. MIT press. 2004.

Gan, Jie, Yan Guo, and Chenggang Xu. 2014. “Decentralized Privatization and Change of Control Rights in China”. The Review of Financial Studies 31 (10): 3854-3894.

Ghosh, Saibal. 2011. “R&D in Public Enterprises”. Science, Technology and Society 16 (2): 177-190.

Gupta, Nandini. 2005. “Partial Privatization and Firm Performance”. The Journal of Finance 60 (2): 987-1015.

Li, Bo, William L. Megginson, Zhe Shen, and Qian Sun. 2016. “Do Share Issue Privatizations Really Improve Firm Performance in China?”. SSRN Electronic Journal.

Makhija, Anil K. “Privatization in India.” Economic and Political Weekly 41, no. 20 (2006): 1947-951.

Megginson, William L, and Jeffry M Netter. 2001. “From State to Market: A Survey of Empirical Studies On Privatization”. Journal of Economic Literature 39 (2): 321-389.

Megginson, William L. 2007. “Introduction to The Special Issue On Privatization”. International Review of Financial Analysis 16 (4): 301-303.

Megginson, William L. 2017. “Privatization, State Capitalism, And State Ownership of Business in The 21St Century”. Foundations and Trends® In Finance 11 (1-2): 1-153.

Megginson, William L., Robert C. Nash, Jeffry M. Netter, and Annette B. POULSEN. 2004. “The Choice of Private Versus Public Capital Markets: Evidence from Privatizations”. The Journal of Finance 59 (6): 2835-2870.

Megginson, William. 2010. “Privatization and Finance”. Annual Review of Financial Economics 2 (1): 145-174.

Meher, Kishor & Samiran, Jana. (2012). Bottom line of Divested PSE’s in Post Privatization Scenario. 4D International Journal of Management & Science. III.

Ministry of Finance, Department of Disinvestment, Government of India. 2007.

Dipam.Gov.In. https://dipam.gov.in/sites/ default/files/white_paper.pdf.

Muhlenkamp, Holger. 2013. “From state to market revisited: a reassessment of the empirical evidence on the efficiency of public (and privately-owned) enterprises”. Annals of Public and Cooperative Economics 86 (4): 535-557.

OECD. 2008. “Improving Product Market Regulation in India”. OECD Economics Department Working Papers.

O’Toole, Conor M., Edgar L.W. Morgenroth, and Thuy T. Ha. 2016. “Investment Efficiency, State-Owned Enterprises and Privatization: Evidence from Viet Nam in Transition”. Journal of Corporate Finance 37: 93-108.

Oum, Tae H., Nicole Adler, and Chunyan Yu. 2006. “Privatization, Corporatization, Ownership Forms and Their Effects On the Performance of the World’s Major Airports”. Journal of Air Transport Management 12 (3): 109-121.

Parker, David. 2004. “The UK’s Privatization Experiment: The Passage of Time Permits A Sober Assessment”. Cesifo Working Paper No. 1126.

Stiglitz, Joseph E. Privatization: Successes and Failures. Edited by Roland Gerard. Columbia University Press, 2008.

Subramanian, Krishnamurthy, and William L. Megginson. 2018. “Employment Protection Laws and Privatization”. SSRN Electronic Journal.

Tran, Ngo My, Walter Nonneman, and Ann Jorissen. 2015. “Privatization of Vietnamese Firms and Its Effects On Firm Performance”. Asian Economic and Financial Review 5 (2): 202-217.

Wolf, Christian O. H., and Michael G. Pollitt. 2008. “Privatizing National Oil Companies: Assessing The Impact On Firm Performance”. SSRN Electronic Journal.

List of CPSE that have received ‘in-principle’ approval of Cabinet Committee on Economic Affairs (CCEA) for strategic disinvestment

| SL. No | Name of CPSE | Date of CCEA approval |

| ONGOING | ||

| 1 | Nagarnar Steel Plant of NMDC | 27.10.2016 |

| 2 | Alloy Steel Plant, Durgapur; Salem Steel Plant; Bhadrwati units of SAIL: |

27.10.2016 |

| 3 | Ferro Scrap Nigam Ltd (Subsidiary) | 27.10.2016 |

| 4 | Central Electronics Ltd. | 27.10.2016 |

| 5 | Bharat Earth Movers Ltd. (BEML) | 27.10.2016 |

| 6 | Cement Corporation of India Ltd. | 27.10.2016 |

| 7 | Bridge & Roof Co. India Ltd. | 27.10.2016 |

| 8 | Engineering Projects (India) Ltd. | 27.10.2016 |

| 9 | Scooters India Ltd | 27.10.2016 |

| 10 | Bharat Pumps & Compressors Ltd. | 27.10.2016 |

| 11 | Hindustan Newsprint Ltd. (Subsidiary) | 27.10.2016 |

| 12 | Hindustan Fluorocarbons Ltd. (Subsidiary) | 27.10.2016 |

| 13 | Pawan Hans Ltd. | 27.10.2016 |

| 14 | Projects Development India Ltd. | 27.10.2016 |

| 15 | Hindustan Prefab Ltd. (HPL) | 27.10.2016 |

| 16 | Hindustan Antibiotics Ltd. | 28.12.2016 |

| 17 | Bengal Chemicals and Pharmaceuticals Limited (BCPL) | 28.12.2016 |

| 17 | Air India and its subsidiaries | 28.06.2017 |

| 19 | India Medicines & Pharmaceuticals Corporation Ltd. (IMPCL) | 01.11.2017 |

| 20 | Karnataka Antibiotics and Pharmaceuticals Ltd. | 01.11.2017 |

| 21 | HLL Lifecare | 01.11.2017 |

| 22 | Kamarajar Port Limited | 28.02.2019 |

| 23 | Shipping Corporation of India (SCI) | 20.11.2019 |

| 24 | (a) Bharat Petroleum Corporation Ltd (except Numaligarh Refinery Limited) (b) BPCL stake in Numaligarh Refinery Limited to a CPSE strategic buyer | 20.11.2019 |

| 25 | Container Corporation of India Ltd. (CONCOR) | 20.11.2019 |

| 26 | THDC India Limited (THDCIL) | 20.11.2019 |

| 27 | North Eastern Electric Power Corp. Ltd. (NEEPCO) | 20.11.2019 |

| 28 | Neelanchal Ispat Nigam Ltd (NINL) | 08.01.2020 |

|

TRANSACTION COMPLETED |

||

| 29 | Hindustan Petroleum Corporation Limited | 19.07.2017 |

| 30 | Rural Electrification Corporation Limited | 06.12.2018 |

| 31 | Hospital Services Consultancy Corporation Limited (HSCC) | 27.10.2016 |

| 32 | National Projects Construction Corporation Limited (NPCC) | 27.10.2016 |

| 33 | Dredging Corporation of India Limited | 01.11.2017 |

Notes:

1 https://www.livemint.com/market/mark-to-market/why-privatization-of-bpcl-will-be-a-good-thing-for-all-stakeholders-1568309050726.

2 Of the 30 CPSEs that were privatised from 1999-2000 to 2003-04, 18 were subsidiaries of India Tourism Development Corporation (ITDC) and 1 was a subsidiary of Hotel Corporation of India (HCI). For the purpose of our analysis, we require information on all financial performance indicators of each disinvested company over a period of 10 years pre and post privatization. However, in the case of disinvested subsidiaries of ITDC (18) and HCI (1), the financial statements are subsumed in the consolidated financial statements of the parent companies. Post disinvestment, these subsidiaries are attached to buyer companies and the financial statements are again presented as consolidated statements of the new parent companies. Due to this challenge, these subsidiaries could not be included in our analysis. Indo Bright Petroleum (IBP) Private Ltd. was merged with Indian Oil Corp (IOC), which is a government enterprise and hence is not considered for the analysis.

3 Given data limitations, the financial data of MFIL and IPCL have been taken for less than 10 years after their disinvestment.

Note: The Government has already strategically sold its stake in 5 CPSEs namely Hindustan Petroleum Corporation Limited (HPCL) (to Indian Oil Corporation (IOC)), Rural Electrification Corporation Limited (REC) (to Power Finance Corporation (PFC)), Dredging Corporation of India Limited (DCIL) (to a consortium of four ports), Hospital Services Consultancy Corporation Limited (HSCC) (to NBCC) & National Projects Construction Corporation Limited (NPCC) (to WAPCOS) in last two years resulting in a yield of Rs. 52,869 crore.

Source: Department of Investment and Public Asset Management (DIPAM) and Press Information Bureau (PIB)