The ‘Other Indias’: Two Analytical Narratives (Redistributive and Natural Resources) on States’ Development

“Please understand, Your Excellency that India is two countries: an India of Light, and an India of Darkness. The ocean brings light to my country. Every place on the map of India near the ocean is well-off. But the river brings darkness to India.”

– “The White Tiger” by Aravind Adiga

This chapter examines whether the pathologies associated with foreign aid and natural resources internationally also afflict the Indian states. It calculates redistributive resource transfers (RRT) from the Centre and revenue from natural resources for Indian states. There is no evidence of a positive relationship between these transfers and various state outcomes, including per capita consumption, GDP growth, development of manufacturing, own tax revenue effort, and institutional quality. In the case of RRT, there is even suggestive evidence of a negative relationship. The question is whether RRT can be tied more strictly to fiscal and governance efforts on the part of the states as provided for by the Thirteenth Finance Commission. Another idea that merits discussion is providing a universal basic income (UBI) directly to households in states receiving large RRT and reliant on natural resource revenues.

I. INTRODUCTION

13.1 The Indian growth take-off since 1980 is associated with Peninsular India, the states that the narrator in “The White Tiger” astutely associates with better geography– being close to the ocean–which development experience has long confirmed as conferring special advantages (Sachs and Warner [1997]). These states—Gujarat, Maharashtra, Tamil Nadu, Karnataka, Kerala, and Andhra Pradesh—have indeed grown faster and advanced more rapidly economically.

13.2 As a result, they have also been a greater focus of policy and research attention in comparison to other states- the so called ‘Other Indias’. These states include not just hinterland India (the India of rivers) but also the India of forests, of natural resources, and of ‘Special Category’ status1. This chapter is devoted to those states that have not been at the mainstream of India’s development narrative. But the analysis is conducted through the lens of broader development experience.

13.3 Successful Peninsular India has offered three interesting and different models of development: the traditional East Asian mode of escape from development based on manufacturing (Gujarat and Tamil Nadu); the remittance-reliant mode of development exemplified by Kerala; and the distinctive, “Precocious India” model based on specializing in skilled services (Karnataka, Andhra Pradesh and Tamil Nadu studied by Kochhar et. al. [2006]).

13.4 Other states have been relatively less successful, and perhaps because of that have received less attention. But they are interesting in their own right because they have conformed to other models of development. This chapter studies two such models of development: those based on “aid” or special status, and those based on natural resources. The definition of natural resources includes coal, onshore oil and natural gas, major and minor minerals but excludes forest cover. Large forest covers can also lead to a “forest curse” but is not analysed in this chapter.

13.5 The “aid” model is most applicable to the erstwhile ‘Special Category’ states that includes North-eastern states and Jammu and Kashmir; the natural resources model to Jharkhand, Chhattisgarh, Odisha, Gujarat and Rajasthan. This chapter examines in an analytical manner the experience of these states.

II. IMPACT OF REDISTRIBUTIVE RESOURCES

13.6 At the time of India’s independence, most economists held a straightforward view of development. According to this view, developing countries were poor because they lacked capital. And they were unable to overcome this problem themselves, because their people were too poor to save. So the key to development, the only way to solve the conundrum, was foreign aid. There was only one possible exception to this rule. Countries with vast amounts of mineral resources mine and sell them, allowing the proceeds to be invested in physical or human capital. But all others were doomed to rely on aid.

13.7 India was never completely convinced of this paradigm. For many years, it accepted aid, but tried to rely on its resources as much as possible, with the aim of winding down its aid dependence as quickly as possible. This strategy has proved successful, and over time many international economists, starting with Easterly (2003) and Rajan and Subramanian (2007) have begun to realise the virtues of this approach. One reason for the change of heart is that research has found it difficult to identify a robust positive relationship between aid and growth.

13.8 Why so? Several theories have been advanced. One hypothesis is that aid perpetuates resource dependency, in the sense that since revenues flow in from outside, recipient countries may fail to develop their own tax bases or their institutions more generally. And it is institutions, tax revenues, and incentives that have been found to be critical for growth, much more than overall resource availability. Many economists, including Brautigam and Knack (2004), Azam, Devarajan, and O’Connell (1997), and Adam and O’Connell (1999) document such effects.

13.9 Another potential downside of aid is that it could trigger “Dutch disease”, named after the impact that discovery of natural gas in the North Sea had on the domestic economy in the Netherlands. This windfall caused the real exchange rate to appreciate as the extra income was spent domestically, pushing up the price of nontradeables, such as services geared to the local economy. The higher prices for services then eroded profitability in export and import-competing industries, de-industrialising the economy, with the share of manufacturing in the economy falling (Corden and Neary [1982]). Similar effects have occurred in Canada, Australia, Russia, and Africa.

13.10 Despite these international examples and the lessons of India’s own experience with foreign aid, when it comes to development within India, the country has followed the path prescribed by the first development economists. It has provided extensive transfers to certain poorer states in an attempt to spur their development. Has this strategy succeeded where others have failed? Could it be that the original development consensus was actually correct? If not, what are the alternatives?

13.11 This section examines the record of Indian states, to try to find an answer – in part so that it can inform the process of reforming the architecture of fund disbursal by the Centre.

III. REDISTRIBUTIVE RESOURCE TRANSFERS: EVIDENCE FROM INDIAN STATES

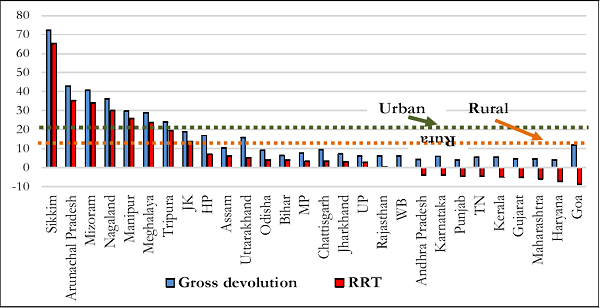

13.12 The first task is to define a concept akin to “aid” in the Indian internal context. State governments up to now have received funds from the Centre via different channels: (i) a share of central taxes, as stipulated by Finance Commissions; (ii) plan and non-plan grants; and (iii) plan and non-plan loans and advances. These funds constitute “gross devolution to states” and the entire amount is not “aid”.2

13.13 Gross devolution entails a strong redistributive element. Certain state-specific characteristics (captured in the ‘Special Category’ status) have determined whether some states are more dependent on such transfers, and particularly concessional assistance (grants). The ‘Special Category’ states have been heavily dependent on such flows for their developmental needs vis-à-vis other states. However, redistributed resources from the Centre differ from traditional “aid” in two important aspects. First, these are intra-country transfers and do not augment overall national disposable income like foreign aid does; second, the donor-recipient relationship is also very different because states benefiting from transfers are part of national governance structures that determine them. The objective of the chapter is not to argue for the replacement of such transfers, but to examine their effects. The perspective utilized in this chapter does recognize that transfer of resources to states are done to avert regional inequalities and correct fiscal imbalances and are therefore extremely crucial.

13.14 In this light, this chapter utilizes the concept of ‘Redistributive Resource Transfers’ (RRT). RRT to a state is defined as gross devolution3 to the state adjusted for the respective state’s share in aggregate gross domestic product (definition D1). Thus RRT is not identical to gross devolution. This adjustment is made to ensure that only the portion of resources devolved to the states

Figure 1. Gross Devolution & RRT per capita (Rs. thousand, annual 2015)

over and above their contribution to Gross Domestic Product is included as RRT. An alternative definition (gross devolution net of the amount the state would have received as per its contribution in the country-wide fiscal effort measured by the state’s share in aggregate own tax revenue) is also considered to check whether results obtained using the first definition are robust or not.

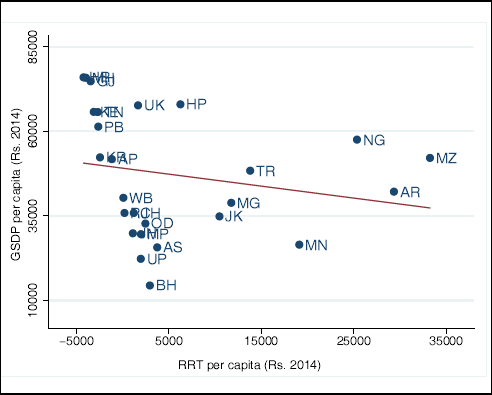

Figure 3a. Per-capita GSDP and per-capita RRT*

13.15 The definition of RRT excludes the impact such transfers have on expenditures undertaken by state governments. It is also essential to note that any redistribution that might occur directly by the Centre’s spending is also excluded4. Thus, RRT is one specific measure of transfers, and is not a definitive metric of redistribution. Gross devolution and RRT as share of GSDP for various states is plotted in the Appendix.

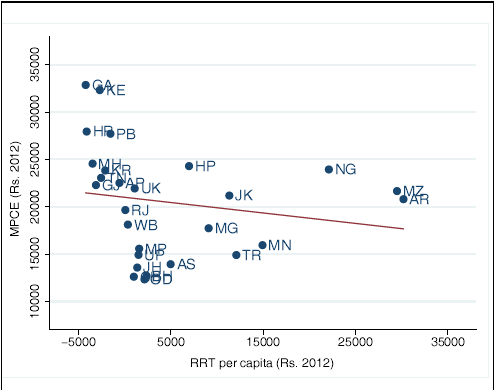

Figure 3b. Per-capita Consumption (MPCE) and per-capita RRT

*: Robust to outliers. Chart 2a excludes Goa and Sikkim. Downward slope in chart 3b is preserved if Goa is excluded.