The vision behind the Foreign Trade Policy continues to be focused on making India a significant participant in world trade and on enabling the country to assume a position of leadership in international trade. The Policy is issued once in Five Years and the Current Policy is for the period 2015 – 20, Mid Term Revision was made on 5th December’2017.

The revised FTP focuses on the goal of exploring new markets and new products as well as on increasing India’s share in the traditional markets and products, leveraging benefits of GST by exporters.

The FTP 2015-20 has 9 Chapters as depicted below.

Foreign Trade Policy : 9 Chapters

To help improve India’s export competitiveness and deepen engagements with new markets, in the Foreign Trade Policy 2015-20 and other schemes provided promotional measures to boost India’s exports with the objective to offset infrastructural inefficiencies and associated costs involved to provide exporters a level playing field and also neutralize incidences of Taxes and Duties.

Brief of the Advance Authorization Scheme under Chapter 4 of FTP shall be discussed here:

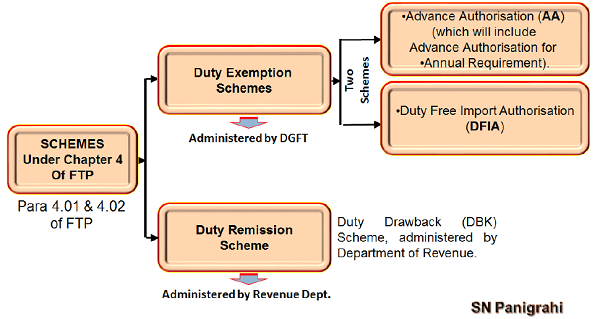

Chapter 4 : DUTY EXEMPTION / REMISSION SCHEMES

Objective:

Schemes under this Chapter enable duty free import of inputs for export production, including replenishment of inputs or duty remission.

Schemes

(a) Duty Exemption Schemes.

The Duty Exemption schemes consist of the following:

> Advance Authorisation (AA) (which will include Advance Authorisation for Annual Requirement).

> Duty Free Import Authorisation (DFIA).

(b) Duty Remission Scheme.

> Duty Drawback (DBK) Scheme, administered by Department of Revenue.

DUTY EXEMPTION / REMISSION

SCHEMES

Advance Authorisation

Advance Authorisation

As per 4.03 of FTP

(a) Advance Authorisation is issued to allow duty free import of input, which is physically incorporated in export product (making normal allowance for wastage). In addition, fuel, oil, catalyst which is consumed / utilized in the process of production of export product, may also be allowed.

(b) Advance Authorisation is issued for inputs in relation to resultant product, on the basis of SION (Standard Input ± Output Norms)

Advance Authorization Issued either to a Manufacturer Exporter or Merchant Exporter

As per para 4.05 of FTP, Advance Authorization is issued either to a manufacturer exporter or merchant exporter tied to a supporting manufacturer(s).

Validity Period for Import

Para 4.17 of FTP & Para 4.41 of HB

Validity period for import of Advance Authorisation shall be 12 months from the date of issue of Authorisation.

Export Obligation (EO) Period

Para 4.22 of FTP & Para 4.42 (a) & (e’) of HB

Period of 18 months for fulfilment of Export Obligation (EO) from the date of issue of authorization allowed.

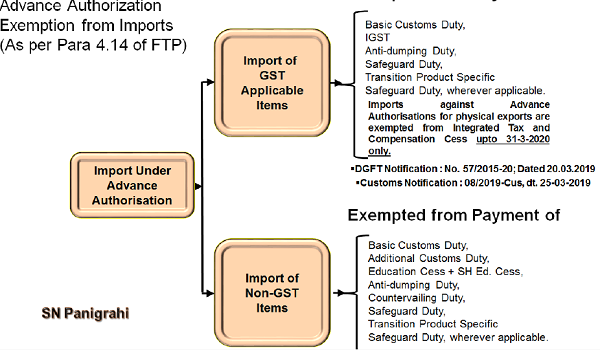

Details of Duties Exempted

As per Para 4.14 of FTP

Imports under Advance Authorization are exempted from payment of Basic Customs Duty, Additional Customs Duty, Education Cess, Anti-dumping Duty, Countervailing Duty, Safeguard Duty, Transition Product Specific Safeguard Duty, wherever applicable.

Import against supplies covered under paragraph 7.02 (c), (d) and (g) of FTP will not be exempted from payment of applicable Anti-dumping Duty, Countervailing Duty, Safeguard Duty and Transition Product Specific Safeguard Duty, if any.

However, imports under Advance Authorization for physical exports are also exempt from whole of the integrated tax and Compensation Cess leviable under sub-section (7) and sub-section (9) respectively, of section 3 of the Customs Tariff Act, 1975 (51 of 1975), as may be provided in the notification issued by Department of Revenue, and such imports shall be subject to pre-import condition. Imports against

Advance Authorizations for physical exports are exempted from Integrated Tax and Compensation Cess upto 31.03.2018 only. (However, further extended upto 31-03-2020 vide DGFT Notification No. 57/2015-20; Dated 20.03.2019 and Customs Notification : 08/2019-Cus, dt. 25-03-2019

Advance Authorization for Annual Requirement

Authorization holders who have been exporting for at least 2 years can get annual Advance Authorization.This gives them the flexibility to export any product throughout the year falling under an export product group using the duty exempted imports.However specific inputs have to be tallied with the resultant exports as per SION/ prescribed ad hoc norms.

Actual User Condition for Advance Authorisation

(i) Advance Authorisation and / or material imported under Advance Authorisation shall be subject to ‘Actual User’ condition. The same shall not be transferable even after completion of export obligation.

However, Authorisation holder will have option to dispose of product manufactured out of duty free input once export obligation is completed.

Domestic Sourcing of Inputs

As per Para 4.20 of FTP

(i) Holder of an Advance Authorisation / Duty Free Import Authorisation can procure inputs from indigenous supplier/ State Trading Enterprise/EOU/EHTP/BTP/STP in lieu of direct import.

Such procurement can be against Advance Release Order (ARO), or Invalidation Letter.

(ii) When domestic supplier intends to obtain duty free material for inputs through Advance Authorisation for supplying resultant product to another Advance Authorisation / DFIA / EPCG Authorisation, Regional Authority shall issue Invalidation Letter.

(iii) Regional Authority shall issue Advance Release Order if the domestic supplier intends to seek refund of duties exempted through Deemed Exports mechanism as per provisions under Chapter-7 of FTP.

(iv) Regional Authority may issue Advance Release Order or Invalidation Letter at the time of issue of Authorisation simultaneously or subsequently.

(v) Advance Authorisation holder under DTA can procure inputs from/SEZ units without obtaining Advance Release Order or Invalidation Letter.

Redemption & Export Obligation Discharge Certificate (EODC)

As per Para 4.47 of HB

On completion of exports and imports, the Authorisation holder shall submit online application in ANF-4F as in (a) (i) above.

In such cases, if EO has been fulfilled, the Regional Authority may issue EODC / Redemption Certificate to Authorisation holder and forward a copy to the Customs authority at the port of registration of Authorisation indicating the same details of proof of fulfilment of EO as stated in paragraph (a) above evidencing fulfilment of Export Obligation.

(ii) Copy of EODC will also be endorsed by Regional Authority to Customs at the Port of Registration by post till system of transmitting these through EDI under message exchange between DGFT and CBEC is introduced.

Disclaimer : The views and opinions; thoughts and assumptions; analysis and conclusions expressed in this article are those of the authors and do not necessarily reflect any legal standing.

Author : SN Panigrahi, GST Consultant, Practitioner, Corporate Trainer & Author Can be reached @ snpanigrahi1963@gmail.com

Author Bio

Sir we are falling under State Jurisdiction and we have required consumption certificate from GST for DGFT so kindly advise me form where i can get consumption certificate? and kindly guide me under which circular/ Notification to get consumption certificate from GST.

Get Chartered Accountant or Cost Accountant Certificate in APPENDIX -4H

REGISTER FOR ACCOUNTING THE CONSUMPTION AND STOCKS OF DUTY FREE IMPORTED OR DOMESTICALLY PROCURED RAW MATERIALS, COMPONENTS ETC. ALLOWED UNDER ADVANCE AUTHORISATION / DFIA

This Certificate is Mandatory for getting EODC

we are falling under State jurisdiction and we have to submit EODC to DGFT so where we will get consumption certificate? Please guide us

Dear Sir,

One party has received contract to supply to PAC.

Now they have taken A.A. to import raw material.

They have also taken Invalidation to procure locally for one item and advised to supply the item directly at PAC. In the PAC name of both suppliers are mentioned as main contractor and sub-contractor. But DGFT is not accepting since it is supply against invalidation. They are insisting for excise certification. Kindly advise.

We have AA and had it invalidated under 2 suppliers name , A &B to procure domestically.

Supplier A Invalidated license is still unused & we want to Import goods by canceling this invalidation.

Treid doing it online but negative result. Error saying first amend AA …. suggestions will be very much appreciated.

Dear Sir,

We were procure material against ARO from local market. Any condition to submit Intimation to Jurisdiction officer within time limit, if yes then how much time required.

We were import material under AA scheme in OCT-18 bur we were forgetting to show advance license detail in export shipping bill.

Now we will pay Custom Duty + Interest + IGST.

Can you guide please to how to get refund / credit of IGST Payment?

Sir,

We have imported material under AA on Adhoc Norms. Committee has sanction only 60% norms which we applied.Meanwhile , we already import total qty, which we applied. Now we have paid balance Cus. Duty/SWS/IGST alongwith interest.

Can u pl. guide us how we can avail the IGST credit of this under GST law. Pl. provide details of Noti./Sec./Rule etc. applicable for the eligibility or we have to apply for IGST cash refund?