“Uncover the world of Social Enterprises, Social Audit, and the Social Stock Exchange with our comprehensive 360-degree analysis. Understand the role of Social Auditors in Social Enterprises listed on the Social Stock Exchange. Learn about eligibility criteria, the emergence of the Social Stock Exchange in India, and the objectives it aims to achieve. Explore the criteria for identifying Social Enterprises, examples of listed organizations, and delve into the legal status of these entities. Discover the rights and advantages of Social Auditors in assessing the impact and efficacy of social development programs.”

Role of Social Auditor in Social Enterprises on the Social Stock Exchange

What is a Social Enterprise?

A social enterprise or social business is defined as a business with specific social objectives that serve as its primary purpose. A social enterprise can be a not-for-profit organization (NPO) or a for-profit social enterprise (FPE) that fulfills the eligibility conditions specified in SEBI ICDR Regulations or as specified by SEBI from time to time. Such enterprises are permitted to register or list their instruments.

Key Takeaways:

1. A social enterprise is a business with social objectives.

2. Maximizing profits is not the primary goal of a social enterprise, unlike a traditional business.

3. Social enterprises generate revenues through endeavors that fund their social causes, distinguishing them from charities.

4. Preference is given to job-seekers from at-risk communities in social enterprises.

5. Social enterprises often obtain funding by selling services and goods.

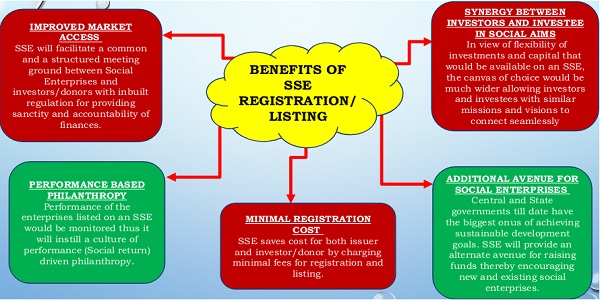

Social Stock Exchange (SSE)

The Social Stock Exchange segment on NSE provides social enterprises (including non-profit organizations and for-profit enterprises) engaged in eligible activities a unique opportunity to register and raise funds on a recognized exchange platform.

A social enterprise, whether an NPO or an FPE, fulfilling the eligibility conditions specified in SEBI ICDR Regulations or as specified by SEBI from time to time, is permitted to register or list its instruments.

Emergence of Social Stock Exchange in India

In the budget speech for FY 2019-20, Hon’ble Finance Minister Smt. Nirmala Sitharaman proposed the idea of an electronic fund-raising platform called the “Social Stock Exchange.” This platform, under the regulatory ambit of SEBI, aims to list social enterprises and voluntary organizations working towards social welfare objectives, allowing them to raise capital as equity, debt, or as units similar to a mutual fund.

Objectives of the Social Stock Exchange:

1. Create a regulated platform that brings together social enterprises and donors.

2. Facilitate funding and growth of social enterprises.

3. Establish an enabling mechanism to ensure robust standards of social impact and financial reporting.

Criteria for Identifying a Social Enterprise:

An entity can be identified as a social enterprise if it meets any of the following criteria:

1. Charitable trust registered under the Indian Trusts Act, 1882.

2. Charitable trust registered under the Public Trust Statute of the relevant state.

3. Charitable society registered under the Societies Registration Act, 1860 (21 of 1860).

4. Company incorporated under Section 8 of the Companies Act, 2013 (18 of 2013).

5. Any other entity as specified by SEBI.

Entities Ineligible for Registering or Raising Funds through the Stock Exchange:

An entity will not be eligible to register or raise funds through the stock exchange if:

1. Any of its promoters, promoter group, directors, or selling shareholders (in the case of for-profit social enterprises) or trustees are debarred from accessing the securities market by SEBI.

2. Any of the promoters, directors, or trustees of the social enterprise is a promoter or director of any other company or social enterprise that has been debarred from accessing the securities market by SEBI.

3. The social enterprise or any of its promoters, directors, or trustees is a willful defaulter or a fraudulent borrower.

4. Any of its promoters, directors, or trustees is a fugitive economic offender.

5. The social enterprise or any of its promoters, directors, or trustees has been debarred from carrying out its activities or raising funds by the Ministry of Home Affairs, any other ministry of the central government or state government, or charitable commissioner or any other statutory body.

EXAMPLES OF LISTED SOCIAL ENTERPRISE

| SR. NO | NAME OF ORGANISATION | DATE OF REGISTRATION WITH SSE |

| 1 | Gramalaya Trust | 05-Apr-2023 |

| 2 | SGBS Unnati Foundation | 05-Apr-2023 |

| 3 | Masoom Trust | 05-Apr-2023 |

| 4 | Opportunity Foundation Trust | 05-Apr-2023 |

| 5 | Possit Skill Organization | 19-Apr-2023 |

| 6 |

Development Management Foundation |

24-Apr-2023 |

| 7 | Krushi Vikas Va Gramin Prashikshan Sanstha | 28-Apr-2023 |

| 8 | Voice Society | 03-May-2023 |

| 9 | Mukti | 22-May-2023 |

| 10 | Ekalavya Foundation | 09-Jun-2023 |

SOCIAL ENTERPRISES: INSTRUMENTS & PROCESS OVERVIEW

Eligibility Criteria for Listing on SSE

To qualify for listing on the Social Stock Exchange (SSE), NPOs must meet the following eligibility criteria:

1. Social Intent and Impact: The primary goal of the NPO should be focused on social intent and impact, specifically addressing the needs of unattended and underprivileged populations or regions.

2. Engaged in Eligible Social Activities: The NPO should be involved in at least one of the 16 broad social activities listed by the board. These activities include eradicating hunger, poverty, malnutrition, and inequality, promoting healthcare, supporting education, employability, and livelihoods, ensuring gender equality and empowering women and LGBTQIA communities, as well as supporting social enterprise incubators.

3. Non-Profit Registration: The NPO should be registered as a non-profit entity, and its registration certificate should be valid for at least 12 months. There should be no ongoing scrutiny or notice by the Income Tax department.

4. Legal Entity: The NPO should be registered in India as a “charitable trust registered under the public trust statute of the relevant state,” or under the Societies Registration Act, 1860, or the Indian Trusts Act, 1882. Alternatively, it can be incorporated as a company under Section 8 of the Companies Act, 2013.

5. Minimum Age Requirement: The NPO should have a minimum age of 3 years from the date of registration.

6. Ownership Declaration: The NPO should declare whether it is government-owned or privately owned.

7. 80G Registration: The NPO should have 80G registration under the Income Tax Act, which grants tax exemption for donations made to the organization.

8. Financial Requirements: The NPO should have a minimum spending of Rs. 50 lakh in the previous fiscal year and a minimum funding of Rs. 10 lakh in the past financial year.

Meeting these eligibility criteria will allow NPOs to be considered for listing on the SSE, providing them with a recognized platform to raise funds and further their social objectives.

WHO IS SOCIAL AUDITOR IN INDIA?

”Social auditor” means an individual registered with a self-regulatory organization under the institute of chartered accountants of India or such other agency, as may be specified by the board, who has qualified a certification program conducted by national institute of securities market and holds a valid certificate; (As per Gazette Notification of SEBI dated 25th july,2022).

Social Audit Firm” means any entity which has employed Social Auditors and has a track record of minimum three years for conducting social impact assessment.

SOCIAL AUDITOR

|

ELIGIBILITY |

DISQUALIFICATION |

|

|

–

|

OBJECTIVES OF SOCIAL AUDIT |

ADVANTAGES OF SOCIAL AUDIT | RIGHTS OF SOCIAL AUDITOR |

| ♦ Assessing The Physical And Financial Gaps Between Needs And Resources Available For Local Development.

♦ Creating Awareness Among Beneficiaries And Providers Of Local Social And Productive Services. ♦ Increasing Efficacy And Effectiveness Of Local Development Programmes. ♦ Scrutiny Of Various Policy Decisions, Keeping In View Stakeholder Interests And Priorities, Particularly Of Rural Poor. ♦ Estimation Of The Opportunity Cost For Stakeholders Of Not Getting Timely Access To Public Services |

– Trains The Community On Participatory Local Planning.

– Encourages Local Democracy. – Encourages Community Participation. – Benefits Disadvantaged Groups. – Promotes Collective Decision Making And Sharing Responsibilities. – Develops Human Resources And Social Capital |

♦ Seek Clarifications From The Implementing Agency About Any Decision-making, Activity, Scheme, Income And Expenditure Incurred By The Agency;

♦ Consider And Scrutinize Existing Schemes And Local Activities Of The Agency; And ♦ Access Registers And Documents Relating To All Development Activities Undertaken By The Implementing Agency Or By Any Other Government Department. |