Key Recommendations of CoE on Need for an Institutional Framework for Regulation and Development of Valuation Professionals in India

In August 2019, the Ministry of Finance (MoF) had constituted Committee of Experts (CoE) to examine the need for an institutional framework for regulation and development of valuation professionals in India. The said CoE had submitted a detailed report for consideration of the MoF on 2 April 2020.

In this article I have made an attempt to bring certain important recommendations made by the CoE which will guide the valuation profession in India the coming years.

1.0 The CoE had proposed an institutional framework that is the least disruptive, builds on existing institutional framework and is grounded on market realities, with zero gestation period. The proposed framework is, however, state-of-the-art, malleable to evolving environment, yet robust, which would serve the economy and the valuation profession in the days far ahead and engender a cadre of, not just valuation professionals, but most valuable professionals. The report of CoE is also accompanied by a draft of ‘Valuers Bill, 2020’.

2.0 The institutional framework is proposed keeping in mind 3 primary objectives asunder:

> Development and regulation of the valuation profession;

> Development and regulation of market for valuation services; and

> Protection of interest of the users of valuation services.

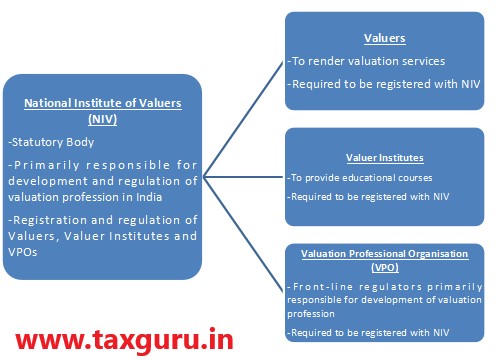

3.0 The proposed ecosystem should have 4 elements, diagrammatically depicted as under:

4.0 The framework should not be limited to valuations under the Companies Act, 2013 and the Insolvency and Bankruptcy Code, 2016 as are presently covered under the Valuation Rules. The framework should cover valuations under other laws in a phased manner in due course, depending on experience and the needs of the time.

5.0 The framework may enable valuation of all kinds of assets, to start with, the courses as well as registration of Valuers should be available for 3 asset classes, namely, Land & Building, Plant & Machinery, and Financial Assets. The framework should enable NIV to add / subtract an asset class to valuation profession as well as increase / decrease the scope of an asset class, with changing needs.

6.0 Educational courses for entering the valuation profession:

An individual may join the valuation profession on completing any of the courses:

> National Valuation Programme, a 4 year integrated full-time professional course, which includes an internship of one year, if he has passed class higher secondary examination;

> Graduate Valuation Programme, a 2 year full-time professional course on valuation, which includes an internship of one year, if he has a degree or equivalent qualification in any of the identified disciplines relevant for an asset class; or

> Limited Valuation Programme, a 400 hour professional course, if he does not have relevant qualification, but has been rendering valuation services as a Valuer for at least 5 years. The eligibility through this programme shall be available only for 2 years.

7.0 There should not be any lower or upper age limit for entry into the profession. Further, there should not be an upper age when a Valuer should cease practice.

8.0 Given that for most of the persons rendering valuation services, it is a part-time vocation, as an extension of their primary vocation / profession, it should not be mandatoryto require an individual to practise valuation profession exclusively in the initial years.

As the profession as well as the market for valuation services matures, it should be practised only as a full-time profession. The indicative time when valuation profession may required to be practised as full-time shall be when the pass-outs of National Valuation Programme join the profession. This would give reasonable time to existing practitioners to take a call whether they would practise valuation profession on full-time basis.

9.0 In order to avoid a situation of conflict of interests and to ensure that a Valuer devotes entire attention to the profession, he shall not be eligible to practise, while he is in employment.

10.0 The NIV should lay down valuation standards based on the recommendations of the Valuation Standards Committee. It shall be mandatory for Valuers to conduct valuation as per the valuation standards.

11.0 Transition and Implementation

> Valuers already registered with IBBI under the Valuation Rules should automatically become Valuers under the new framework subject to their consent.

> Registered valuer organisations recognised by the IBBI should automatically be transitioned as VPOs under the new framework.

> Until NIV is established, the IBBI may exercise the powers and discharge the functions of the NIV under the Valuers Act, in accordance with the provisions of that Act.

> Valuers engaged in valuation services should have a window of 2 years to become Valuers if they meet eligibility norms under the Valuation Rules and in the manner, provided therein.

> Valuers engaged in valuation services, but not having relevant educational qualifications, should have a window of 3 years to become Valuers subject to meeting other eligibility norms under the Valuation Rules and in the manner, provided therein, provided they undergo the limited valuation course.

The author is a Practicing Chartered Accountant, Registered Valuer (SFA), qualified CPA(USA), qualified Independent Director having experience spanning more than 10 years in Direct Taxation, FEMA, Valuation – Advisory, Compliance and Representation service. He can be reached at 9145687573, rvamolbongale@gmail.com

Author Bio