NFRA Consultative Paper on Statutory Audit and Auditing Standards for Micro, Small and Medium Companies (MSMCs) – Comments of AICAS

16th November 2021

To,

Secretary,

National Financial Reporting Authority

7th-8th Floor, Hindustan Times House

18-20, Kasturba Gandhi Marg, New Delhi -110001

Sub: Comments and Response in respect of NFRA Consultation Paper on Statutory Audit & Auditing Standards for MSMCs

Respected Sir,

We have been working over the last one month to seek views from members of society and other interest groups.

We have compiled all the comments and response in the ensuing pages. We request you to kindly consider them.

We are also enclosing a presentation prepared by us further substantiating our views and comments. We further request you an opportunity of being heard in person by the Board of National Financial Reporting Authority (NFRA) so that we can explain the vitality of the issues and concerns involved including the devastating impact on the country and economy in absence of widespread and strong Audit Mechanism across corporate sector.

Thanking you,

For All India Chartered Accountants Society (Regd.)

Vaibhav Jain

General Secretary

Mobile: +91 9711310004

Email: aicas.cfo@gmail.com

NFRA Consultative Paper: Comments

1. Background

- NFRA was constituted on 1st October 2018 (Section 132 – Companies Act, 2013)

- NFRA constituted to

i. Make recommendation to government on Accounting and Auditing Policies and Standards.

ii. Monitor and enforce compliance- exceptional cases identified or referred by Government

iii. Oversee the quality of service by Chartered Accountants.

iv. NFRA to recommend only on policies and standards as Institute of Chartered Accountants of India

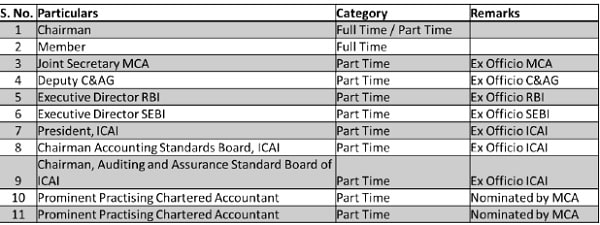

- Constitution of NFRA Board

- 4 More Nominees can be appointed by Government of India (2 Full Time and 2 Part Time)

- We Recommend

- NFRA Chairman can be Part Time in terms of Companies Act (CA with a Minimum Audit Experience of more than 25 years)

- It is important to ensure that only CAs with Audit experience of more than 10 years should be considered for nomination for any part-time or full-time members role in NFRA, except Ex-Officio Members.

2. NFRA Issued a consultative paper to seek public comments on NFRA recommendations:

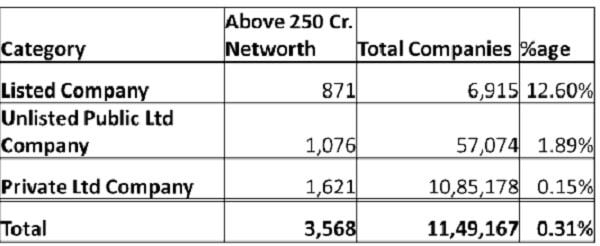

- Proposal to exempt mandatory statutory audit of companies below net worth of Rs 250 crores

- Exempting 99.69% companies from Audit

a) Only 3,568 companies to be subject to Audit

b) Only 871 listed companies.

- Proposal to exempt compliance

a) of Accounting Standards

b) of Auditing Standards

3. Basis of NFRA Conclusions:

NFRA Conclusion is based on premise

- The Chartered Accountants are charging very low audit fee currently.

- The audits presently conducted are only a Sham

- Compliance of accounting and auditing requirements are unnecessary burden

The Audit fee figures quoted by the Consultative paper is based on wrong information as full details of Audit fee is disclosed in all financial statements Notes and may not be available in MCA Data.

There is no basis for NFRA consultative paper to conclude that audits being currently conducted are sham, on the false presumption that Auditors cannot undertake audit in terms of current standards because of low fee. This is an absurd and defamatory allegation and presumption. Do the paper writer mean that all big audit firms who charged large fee are only properly conducted audits. This is a lack of even basic understanding of Indian professional culture for thousands of years that “Professional Fee is only an Honorarium and once an assignment is accepted it is to be delivered with world class standards- Former PM Hon’ble Late Shri Atal Bihari ji Vajpayee on the occasion of Golden Jubilee of ICAI”

The NFRA paper also undermine the commitment of pure Indian CA firms, who stand committed to Truth, Fairness, effectiveness, efficiency, ethics, transparency, Indian values, transparency, Honesty, independence, and Indian culture.

We have included herein the detailed analysis of why audit, accounting standards, auditing standards are important for all Companies and even non-Corporate. Those who are answerable to independent audit, sometime wish to reject the requirement with vested interest and lack of full understanding of Indian economic environment.

No Industry body or Chamber of Commerce or trade body has demanded or even suggested that audit is not required. The value addition to audit clients by Auditor is many times of the cost.

4. Consultative paper is unauthorised: The Consultative paper circulated in the name of National Financial reporting authority is unauthorised. The statement is supported by the following facts: –

a) Ultra Vires of Powers Delegated to NFRA by Companies Act, 2013: The Companies Act, 2013 under Section 132 has created NFRA for matters related accounting and auditing standards under this Act. No Role has been assigned to NFRA to determine or even suggest whether an Audit should be conducted or not.

b) Breach of Corporate Governance by NFRA: The Consultative Paper has been issued without circulation or knowledge or approval of the NFRA Board. This is a clear case of breach of Corporate Governance by NFRA concerned officials. No agenda or note in this regard was circulated to 11 members of NFRA nor this matter was ever listed for consideration in any meeting of NFRA. The subject matter is completely unauthorised by NFRA as it was never discussed in any meeting of NFRA.

5. Misuse of Section 132 (2) (a): The Consultative Paper has been issued referring the powers conferred upon NFRA under Section 132 (2) (a). The said Section only mandates NFRA to make recommendations to the Central Government on Formulation and laying down of Accounting and Auditing Policies and Standards. No action can be initiated by NFRA in terms of section 132(2)(a) (as cited by the consultation paper) for recommending removal of audit requirements under the Act.

6. Proposed Exemption from Audit: The proposed exemption from the statutory audit to Companies with net worth up to Rs 250 crore will harm Indian economy and businesses substantially. The statutory audit by an independent Chartered Accountant firm provides a professional assurance that:

- Internal operational Control exist – ensure efficiency and efficacy of management

- Internal financial control is adequate

- Financial statements are credible

- The financial statements are free from material misstatement due to fraud or error

- No personal expenses are debited in the Profit and loss account

- Capital expenditures are not charged to revenue or vice versa

- No unsupported and unrelated expenses are charged to Profit and loss account

- The generally accepted Accounting Principles (GAAP) and mandatory accounting standards are followed in letter and sprit

- Disclosure of diversion of funds

- Disclosure of misuse of funds

- All transactions in the bank or otherwise undertaken by the Company are properly accounted for as per Generally accepted accounting Principles

- suspicious transactions are identified

- Money laundering is detected and reported

- Public deposits are properly monitored

- Check on fraud or mismanagement of funds at various levels of management

- The books of accounts and GST returns, invoices, credit notes and input utilised are all in accordance with the GST law in force and there is a proper reconciliation of the GST supplies and turnover and other transactions in the Company.

- All fixed assets and Current assets are verified by auditors.

- The immoveable properties of the Company are registered in the name of the Company

- Loans given by the Company are in the interest of the company and are interest bearing and are being properly approved and monitored

- Secured and unsecured loans received or given are examined in detail with supporting agreements, documents, and underlying transactions.

- Proper provision and payment of Income Tax is made by a Company

- Minority investor interest, bank stipulations, shareholders resolutions, Board instructions are followed as per corporate Governance standards.

- All legal requirements having implication on true and fairness of financial statements are examined so as to ensure that the Company is not subjected to material non compliances.

7. Risk of Unaudited Financials: In the absence of Audit, even in a small net worth company, the Company vehicle with a limited liability, may be massively misused:

- Lack of Corporate Governance

- Financial statements may be drawn without books of accounts

- Non-compliance of Generally Accepted Accounting Principles and basic concepts of accounting

- Unaccounted bank transactions

- Lack of Financial discipline or disclosures

- Large scale non-performing assets unreported

- Loans extended without security or adequate documentation- even where Board may so mandate

- Charging of personal expenses to books

- Charging of unsupported expenses and booking unsupported income

- Non- maintenance of books of accounts and statutory records

- Routing of corrupt money and crime money through their bank accounts using exempted Companies as a money laundering layer

- Recording of non-existent assets

- Unaccounted liabilities or contingent liabilities

- Syphoning of funds

- Unreported Frauds impacting controls, efficiency, existence

- Large unreported cash transactions

- Diversion of funds and misuse of funds

- No observation of laws governing transactions

- How to determine eligibility for FDI, ODI, tenders, services, supplies in the absence of reliable financial statements.

- Even normal business agreements, collaborations, joint venture, national and international bidding, private equity investments, private placements, preferential issues, valuations all will become meaningless as there will be no credible support to various decisions.

- All items of CARO report and main audit report will remain unexamined causing significant loss to Company, shareholders, investors, banks, government and entire economy and society

- Economy will be hit adversely: The withdrawal of audit requirement will be suicidal and will hit the Indian economy very deeply and below the belt.

- No credibility to financial statements: How the lenders, vendors, suppliers, lessors, customers, employees, regulators, Government departments, RBI, export and import agencies, customs, GST department and income tax department and other stakeholders will rely on the financial statements of such Companies and entities.

- The above list is only illustrative and not exhaustive.

8. NFRA is not a regulator: It is completely incorrectly stated by the Consultative paper that NFRA is an independent regulator of accounting and auditing. This role is clearly provided to the Institute of Chartered Accountants of India by the parliament by The Chartered Accountants Act, 1949.

The NFRA is constituted with a limited objective of review of suggestions received from ICAI in respect of accounting and auditing standards and to advise to the Government on such ICAI suggestions. NFRA is not even authorised to bring in any accounting standard or auditing standard unless it is so approved and recommended by the ICAI.

The role to oversee quality of audit and enforce compliance is also of advisory in nature as per clear mandate of section 132. The Rules notified by MCA are beyond the scope of the Companies Act 2013 and against principles of delegated legislation. A separate note on ultra- wires and vague provisions of Section 132, ultra-wire rules and illegal actions of NFRA is being separately submitted to the Government of India.

9. Ease of Doing Business: The consultation paper is being issued by misusing the “ease of doing business” nomenclature. The Ease of Doing Business indicators as per World Bank are from 11 areas of business regulation such as:

a) Starting a Business,

b) Dealing with Construction Permits,

c) Getting Electricity,

d) Registering Property,

e) Getting Credit,

f) Protecting Minority Investors,

g) Paying Taxes,

h) Trading across Borders,

i) Enforcing Contracts, and

j) Resolving Insolvency.

The regulation of Accounting and Auditing are not within the framework of “Ease of Doing Business” and in fact the proposed suggestion to consider removal of audit requirement will negatively impact in “Ease of Doing Business” by adversely impacting Getting Credit, Protecting Minority Investors, Enforcing Contracts, and Resolving Insolvency in the absence of credible financial statements.

10. The noble intention of Honourable PM Shri Narendra ji Modi is adversely impacted by the proposal as the proposal will hit at the very root of the business entity by withdrawing basic systems, controls, operating procedures and financial discipline in the absence of auditor as an independent professional friend, philosopher and guide of the business. In his address on Audit Day (i.e. 16th November 2021), Honourable PM Shri Narendra ji Modi said, “Audit Is An Important Part of Value Addition”. He also added that, “Audit has significantly improved reporting of NPA in Banks and also built transparency in the ecosystem”.

11. Positive role of Auditors: In fact, the Auditors have played a very significant role in growth and development of their clients by helping them in making sustained growth by a continuous professional advise and guidance on internal controls, best business and ethical practices , growth strategies, financial discipline, tight controls on leakage of revenue and unrequired or undesirable expenditure, ensuring checks on diversion and misuse of funds, cost control, management accounting , treasury management, restructuring , capital structuring, and so on.

12. Negative thoughts against Audit are malicious: There is a section of malicious and negative thought led group of persons who will always keep on looking at the services and support provided by auditing community to businesses with suspicion. Their entire logic and arguments are based on certain exceptional cases where auditors could not professionally mange their actions and deeds. It is however not understood by the critique that 99.99% business organisations across the world are growing, and prospering based on professional advise of auditors on all matters of financial discipline, financial management, internal controls, SOPs, system design, system review and monitoring of actual operations by best auditors in the world. The conflict of interest is clearly managed by ethical guidelines issued by the Institute of Chartered Accountants of India.

12. Users of General Purpose Financial statements (GPFS): The para 2.5.2 of the consultative paper read as follows:

2.5.2. The objective of GPFS is to provide financial information about the reporting entity that is useful to existing and potential investors, lenders and other creditors in making decisions relating to providing resources to the entity. Those decisions involve decisions about:

a) buying, selling or holding equity and debt instruments;

b) providing or settling loans and other forms of credit; or

c) exercising rights to vote on, or otherwise influence, management’s actions that affect the use of the entity’s economic resources.

It may be noted that GPFS contain financial information that is useful and relevant to a wide set of external parties such as Regulators, Tax Authorities, Suppliers, Employees and the public at large.

However, in recent times, the accounting standard-setting bodies whose standards form the primary bases for preparing GPFS, have consciously decided that the “Primary Users” of GPFS will be only those listed above in this para 2.5.2.

What needs emphasis is that both such “Primary Users” and the information needs for the kind of decisions detailed above, are not likely to be found in a preponderant majority of MSMCs. Therefore, both Accounting and Auditing Standards, and the requirement of mandatory statutory audit, as applicable to other (i. e. non MSMCs or large) companies would be both unnecessary and unjustified on cost benefit considerations.

The person who has authored the consultation paper seems to have not realised the usage of General Purpose Financial statements (GPFS) by various stakeholders. Even the aforesaid para appreciate that General Purpose Financial statements will be useful for primary users for making various decisions e.g.

- Existing Investors – shareholders, debenture holders, depositors

- Potential Investors – in equity, quasi equity , as business partners

- Lenders

- Creditors

In terms of views of the consultative papers the GPFS can be used only for:

- Buying, selling, or holding of debt instruments

- Providing or settling of loans and other forms of credit

- Exercising right to vote on , otherwise influence the management actions that influences the use of entity’s resources.

- Contain useful information for regulators, tax authorities, suppliers, employees and public at large.

14. Lack of Understanding the need of reliable Financial statements: The conclusion in para 2.5.2 that the aforesaid primary user may not find the need of information contained in financial statements, for the aforementioned decisions in Companies with net worth up to Rs 250 Crore MSMC Companies is far from truth and understanding of real need of Financial statements by all kind of micro, small, midsize and large organisations for a large number of matters including the one listed in para 2.5.2.

15. In case Audit Exemption Proposal is Accepted, it will have following adverse impact:

- Accounting is backbone of business- In the absence of auditors-accounting will collapse-negative impact on all businesses, NGOs, industries, commerce, employment-absence of qualifies CA will hit India’s reputation.

- Impact on entire business fraternity and their families

- Corporate Governance zero

- Tax compliance and collection to hit

- Start-up entities to suffer and may not be able to even raise funds needed in the absence of reliable and credible financial statements.

- Industrial and business growth to suffer

- SME Growth will suffer as Auditor’s guide growth of SME Businesses.

16. Need for Accounting, Auditing, and financial statements: Para 2.5.2 further conclude, without any basis that accounting standards, auditing standards and requirement of auditing is unnecessary and unjustified on cost benefit consideration for entities up to INR 250 Crore net worth. This conclusion reflects that the thought process of author of consultative paper and those who authorised it to be published on behalf of the Government, without a proper process lack basic knowledge and understanding of the importance of accounting, auditing, and accounting standards.

17. Why is Audit Important?

Mandatory audit is meeting the needs of: –

- Regulators – RBI, SEBI, TRAI, MCA

- Trade, Industry, and commerce

- Banks and Lenders

- Vendors and Customers

- Collaborator

- Income Tax department and GST department

- Shareholders including

a) Domestic Investors

b) Minority Shareholders

c) Foreign Institutional Investors

d) Private Equity Funds

e) Mutual Funds

f) Strategic Investors

g) Investors in Start ups

18. If Audit is Exempted

- Board of directors, CFO and CEO including independent directors will have to certify the compliance of GAAP and Accounting Standards

- Are the Directors or KMP capable to examine and certify?

- Accounting and auditing including financial statements preparation and disclosure-need deep expertise

- In the absence of auditor or CAs – who will assure truth, fairness, and completeness

- Audit cost is low – Value Added is High

19. Data presented in the consultative paper : An Analysis

a) Extract of Table 1.1. from the Consultative Paper

| Table 1.1. Summary Status of Filing of Annual Financial Statements/MGT-7 for FY 2018-19 | ||||||||

| Com-pany Type | Total Active Companies | AFS/MGT-7 Filing Data | ||||||

| Total number of filings | Companies with Net Worth below ₹ 250 crores | Companies with Net Worth above ₹ 250 crores |

||||||

| Number of Comp-anies |

% | Number of Comp-anies |

% | Number of Comp-anies |

% | Number of Comp-anies |

% | |

| Private Limited of which | 10,85,178 | 94.43% | 5,68,556 | 52.39% | 5,66,935 | 94.57% | 1,621 | 45.43% |

| Private Limited | 10,62,418 | – | 5,60,405 | 5,58,784 | – | 1,621 | – | |

| One Person Comp-any |

22,760 | – | 8,151 | 8,151 | – | – | – | |

| Public Limited Of which | 63,989 | 5.57% | 34,499 | 53.91% | 32,552 | 5.43% | 1,947 | 54.57% |

| Listed | 6,915 | – | 4,349 | 3478 | – | 871 | ||

| Unl-isted | 57,074 | – | 30,150 | 29,074 | – | 1,076 | ||

| Total | 11,4-9,167 | 100% | 6,03,055 | 52.48% | 5,9-9,487 | 100% | 3,568 | 100% |

Comments:

1. Only 871 Listed Companies are above the threshold of Net worth of Rs. 250 Crores, considered as MSMC by the paper. It is clear from the above that 80% of listed companies in India are MSME as per NFRA criteria of net worth below Rs 250 crore.

2. Only 3,568 Companies are above the threshold of Net worth of Rs. 250 Crores, considered as MSMC by the paper.

3. About 6 Lakh Companies which are filing regular returns are less than Net worth of Rs 250 crore.

b) Extract of Table 1.3 from the Consultative Paper

Net Worth Based Analysis |

||||||||||

Table 1.3 Companies with Net Worth below ₹ 250 crores (all amount in crores except no. of companies) |

||||||||||

No. of Companies |

Turnover Analysis |

Indebtedness Analysis |

||||||||

Net Worth Range (₹ Crores) |

Private |

Public |

Total No. of Comp-anies |

Total Net Worth (₹ Crores) |

No. of com-panies with +ve Turnover |

No. of com-panies with zero

|

Tur-nover range (Min &Max) (₹ Crores) |

No. of comp-anies

|

No. of com-panies with Zero

|

Indebt-edness Range (Min &Max) (₹ Crores) |

Positive NetWorth |

||||||||||

>=200-<250 |

497 |

246 |

743 |

1,65,888 |

678 |

65 |

0 & 5,960 |

496 |

247 |

0 & 2,771 |

>=100-<200 |

2,192 |

1086 |

3,278 |

4,58,021 |

2,928 |

350 |

0 & 16,780 |

2,272 |

1,006 |

0 & 18,413 |

>=50-<100 |

4,383 |

1,514 |

5,897 |

4,12,461 |

5,031 |

866 |

0 & 19,538 |

3,801 |

2,096 |

0 & 8,525 |

>=25-<50 |

7,501 |

1,947 |

9,448 |

3,32,026 |

7,878 |

1,570 |

0 & 14,081 |

6,208 |

3,240 |

0 & 8,236 |

>=10-<25 |

18,032 |

3,233 |

21,265 |

3,31,823 |

17,193 |

4,072 |

0 & 21,260 |

13,743 |

7,522 |

0 & 9,959 |

>=5-<10 |

22,274 |

2,675 |

24,949 |

1,76,764 |

19,893 |

5,056 |

0 & 10,468 |

16,158 |

8,791 |

0 & 1,779 |

>=1-<5 |

79,570 |

5,992 |

85,562 |

2,03,538 |

66,039 |

19,523 |

-0.03 & 64,265 |

54,987 |

30,575 |

0 & 6,540 |

>=0.5-<1 |

39,584 |

1,868 |

41,452 |

29,880 |

31,016 |

10,436 |

0 & 5,145 |

25,571 |

15,881 |

0 & 1,507 |

>=0.2-<0.5 |

49,762 |

1,997 |

51,759 |

17,132 |

37,977 |

13,782 |

-0.47 & 4,242 |

30,165 |

21,594 |

0 & 1,600 |

>=0-<0.2 |

2,25,471 |

6,712 |

2,32,183 |

9,770 |

1,32,787 |

99,396 |

0 & 5,223 |

91,043 |

1,41,140 |

0 & 4,833 |

Subtotal (A) |

4,49,266 |

27,270 |

4,76,536 |

21,37,302 |

3,21,420 |

1,55,116 |

– |

2,44,444 |

2,32,092 |

– |

Negative Net Worth |

||||||||||

>=50000 & above |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

>=25000-<50000 |

0 |

4 |

4 |

-1,41,290 |

4 |

0 |

2,720 & 54,900 |

4 |

0 |

113 & 72,700 |

>=10000-<25000 |

0 |

11 |

11 |

-1,53,176 |

11 |

0 |

11.8 & 17,300 |

11 |

0 |

55.2 &29,600 |

>=5000-<10000 |

4 |

10 |

14 |

-1,02,959 |

9 |

5 |

0 & 23,900 |

12 |

2 |

0 &19,800 |

>=1000-<5000 |

25 |

72 |

97 |

-2,05,983 |

80 |

17 |

0 & 21,500 |

94 |

3 |

0 & 28, 600 |

>=250-<1000 |

112 |

154 |

266 |

-1,25,867 |

193 |

73 |

0 & 9,110 |

251 |

15 |

0 & 9,330 |

>=200-<250 |

41 |

26 |

67 |

-14,916 |

42 |

25 |

0 & 2,240 |

65 |

2 |

0 & 5,590 |

>=100-<200 |

186 |

137 |

323 |

-45,557 |

232 |

91 |

0 & 1,770 |

299 |

24 |

0 & 3,750 |

>=50-<100 |

340 |

193 |

533 |

-37,743 |

358 |

175 |

0 & 12, 900 |

479 |

54 |

0 & 5,620 |

>=25-<50 |

622 |

265 |

887 |

-30,712 |

562 |

325 |

0 & 36,800 |

789 |

98 |

0 & 3,820 |

>=10-<25 |

1,588 |

456 |

2,044 |

-31,779 |

1,328 |

716 |

0 & 2,400 |

1,787 |

257 |

0 & 2,840 |

>=5-<10 |

2,205 |

419 |

2,624 |

-18,602 |

1,731 |

893 |

0 & 3,150 |

2,237 |

387 |

0 & 1,750 |

>=1-<5 |

11,004 |

1,056 |

12,060 |

-26,908 |

7,857 |

4,203 |

0 & 7, 960 |

10,228 |

1,832 |

0 & 2,230 |

>=0.5-<1 |

8,340 |

464 |

8,804 |

-6,280 |

5,826 |

2,978 |

0 & 287 |

7,308 |

1,496 |

0 & 567 |

>=0.2-<0.5 |

14,881 |

582 |

15,463 |

-4,983 |

10,050 |

5,413 |

0 & 540 |

12,366 |

3,097 |

0 & 678 |

>=0-<0.2 |

78,321 |

1,433 |

79,754 |

-3,702 |

40,665 |

39,089 |

0 & 249 |

52,282 |

27,472 |

0 & 1,610 |

Subtotal (B) |

1,17,669 |

5,282 |

1,22,951 |

-9,50,457 |

68,948 |

54,003 |

– |

88,212 |

34,739 |

– |

Total |

5,66,935 |

32,552 |

5,99,487 |

11,86,845 |

3,90,368 |

2,09,119 |

– |

3,32,656 |

2,66,831 |

– |

Comments: The following important facts can be noted from the table.

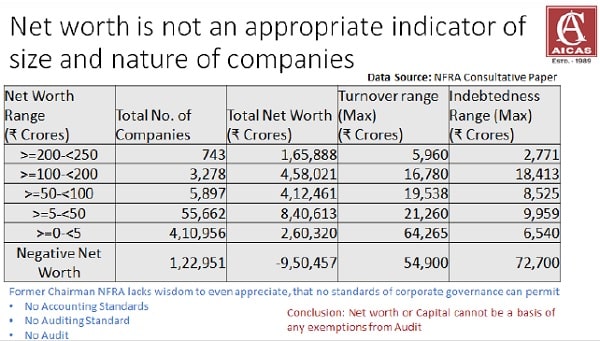

- Even companies up to Rs 20 lakh net worth there are cases of maximum indebtedness range of up to Rs 4,833 crores in some cases and turnover range up to Rs 4,242 crores.

- Company with up to Rs 10 crore net worth has indebtedness range of up to Rs. 1,779 crore and turnover range of up to Rs 10,468 crore.

- The whole table shows that in almost are categories of net worth below Rs 250 crore. The turnover range is between maximum of Rs 4242 crores to Rs 64,265 Cr and Indebtedness range is maximum Rs 1,507 Cr to Rs 18,413 crore and

- Even in negative net worth cases the maximum turnover range is between Rs. 287 crore to Rs. 54,900 crores and indebtedness range at maximum is from Rs 567 crore to Rs 72,700 crore.

- The table 1.3 itself clearly provides a big diversity among Indian companies and exempting companies from audit based on the criteria of net worth will be disastrous as will be clear from the following data, which establish that Net worth is not an appropriate indicator of size and nature of companies:

c) Extract of Table 1.4 from the Consultative Paper

Table 1.4 Turnover Analysis of Companies with Net Worth below ₹ 250 crores (all amount in crores except no. of companies) |

||||||||||

No. of Companies |

Net Worth Analysis |

Indebtedness Analysis |

||||||||

Turnover Range (₹ Crores) |

Private |

Public |

Total No. of Compa-nies |

Total Turnover (₹ Crores) |

No. of companies with +ve Net Worth |

No. of comp-anies with negative Net Worth |

Net Worth range (Min &Max) (₹ Crores) |

No. of comp-anies

|

No. of compa-nies with zero

|

Indebt-edness Range (Min &Max) (₹ Crores) |

>=25,000 &above |

1 |

4 |

5 |

2,13,295 |

1 |

4 |

-48,720 & 3.83 |

5 |

0 |

8.97 & 72,709 |

>=10,000-<25,000 |

10 |

17 |

27 |

4,12,707 |

14 |

13 |

-19,831 & 191 |

24 |

3 |

0 & 20,494 |

>=5,000-<10,000 |

11 |

17 |

28 |

2,01,554 |

19 |

9 |

-11,476 & 211 |

25 |

3 |

0 & 16,131 |

>=1,000-<5,000 |

254 |

159 |

413 |

7,23,512 |

340 |

73 |

-35,300 &249 |

358 |

55 |

0 & 29,569 |

>=800-<1,000 |

165 |

78 |

243 |

2,14,200 |

220 |

23 |

-3,468 & 243 |

219 |

24 |

0 & 28,598 |

>=500-<800 |

640 |

251 |

891 |

5,47,526 |

831 |

60 |

-3,337 & 249 |

775 |

116 |

0 & 13,452 |

>=200 – <500 |

3,321 |

1,083 |

4,404 |

13,29,059 |

4,170 |

234 |

-6,556& 249 |

3782 |

622 |

0 & 9,959 |

>=100 – <200 |

5,760 |

1,288 |

7,048 |

9,82,077 |

6,653 |

395 |

-14,375 &249 |

6045 |

1,003 |

0 & 20,445 |

>=50 – <100 |

8,790 |

1,497 |

10,287 |

7,22,440 |

9,663 |

624 |

-9,716 & 249 |

8706 |

1,581 |

0 & 6,224 |

>=25 – <50 |

14,212 |

1,615 |

15,827 |

5,59,003 |

14,864 |

963 |

-1,053 & 247 |

13,354 |

2,473 |

0 & 6,540 |

>=10 – <25 |

26,509 |

2,011 |

28,520 |

4,54,875 |

26,267 |

2,253 |

-15,108 & 248 |

23,459 |

5,061 |

0 & 15,313 |

>=5 – <10 |

25,756 |

1,529 |

27,285 |

1,95,221 |

24,678 |

2,607 |

-3,050 & 248 |

21,350 |

5,935 |

0 & 6,833 |

>=1 – <5 |

73,648 |

3,197 |

76,845 |

1,86,180 |

65,893 |

10,952 |

-2,314 & 248 |

54,171 |

22,674 |

0 & 14,000 |

>=0.5 – <1 |

34,359 |

1,339 |

35,698 |

26,072 |

28,613 |

7,085 |

-942 & 242 |

21,842 |

13,856 |

0 & 3,357 |

>=0.2 – <0.5 |

38,900 |

1,593 |

40,493 |

13,420 |

31,048 |

9,445 |

-2,406 & 248 |

22,214 |

18,279 |

0 & 1,577 |

>0 – <0.2 |

1,36,914 |

5,437 |

1,42,351 |

8,064 |

1,08,143 |

34,208 |

-950 & 241 |

59,247 |

83,104 |

0 & 4,833 |

<=0 |

1,97,685 |

11,437 |

2,09,122 |

-1 |

1,55,119 |

54,003 |

-9,369 & 249 |

97,080 |

1,12,042 |

-0.72& 9,332 |

Total |

5,66,935 |

32,552 |

5,99,487 |

67,89,203 |

4,76,536 |

1,22,951 |

3,32,656 |

2,66,831 |

||

Comments

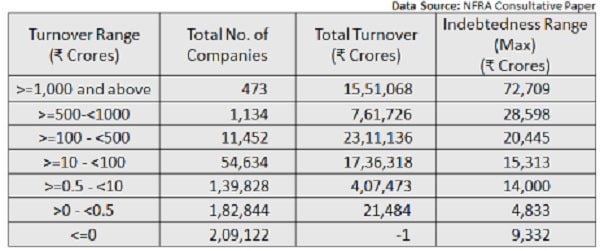

- Table has analysed companies with turnover from 0 turnover up to Rs 25,000 Cr turnover (with net worth up to Rs 250 crores)

- 23,346 companies have turnover from Rs 50 crore to Rs 25000 cr.

- Companies above Rs 50 Cr turnover has net worth range from (-) Rs 48,720 Cr to Rs 250 cr.

- Even company with Rs. 3.83 Cr net worth has turnover of more than Rs 25,000 cr.

- 3,32,656 companies out of companies with net worth less than Rs 250 Cr have debt ranging up to maximum of Rs 72,709 Cr.

- Even companies with less than Rs. 10 Cr turnover have debt range (max) of Rs 1,577 Cr to Rs 14,000 cr.

- The company with less than Rs 1 Cr turnover has a maximum debt range up to Rs 9,332 cr.

- Thus, exempting Indian companies from actual facts being so varied as per table 1.4 are clearly dangerous for the economic system. Low Turnover companies may have very high debt and will leave a large turnover remaining uncovered as is clear from following table :

Extract of Table 1.5 from the Consultative Paper

Table 1.5 Indebtedness Analysis of Companies with Net Worth below ₹ 250 crores (all amount in crores except no. of companies)

Table 1.5 Indebtedness Analysis of Companies with Net Worth below ₹ 250 crores (all amount in crores except no. of companies) |

||||||||||

No. of Companies |

Net Worth Analysis |

Turnover Analysis |

||||||||

Indebt-edness Range (₹ Crores) |

Private |

Public |

Total No. of Compa-nies |

Total Indebt-edness |

No. of comp-anies with +ve

|

No. of comp-anies with neg-ative Net Worth |

Net Worth range (Min &Max) (₹ Crores) |

No. of comp-anies with +ve

|

No. of comp-anies with zero & neg-ative turn-over |

Turn-over Range (Min &Max) (₹ Cro-res) |

>=25,000 & above |

0 |

5 |

5 |

64082 |

0 |

5 |

-35,300 & -2,640 |

5 |

0 |

907 & 31,800 |

>=10,000-<25,000 |

3 |

13 |

16 |

1,14,005 |

1 |

15 |

-19,800 & 154 |

16 |

0 |

1.1 & 21,500 |

>=5,000-<10,000 |

10 |

27 |

37 |

1,27,628 |

8 |

29 |

-9,940 & 195 |

33 |

4 |

0 & 23,900 |

>=1,000-<5,000 |

173 |

185 |

358 |

2,81,595 |

139 |

219 |

-6,120 & 249 |

302 |

56 |

0 & 36,800 |

>=800-<1,000 |

74 |

55 |

129 |

37,066 |

74 |

55 |

-3,810 & 249 |

103 |

26 |

0 & 15,179 |

>=500-<800 |

273 |

146 |

419 |

98,914 |

256 |

163 |

-6,790 & 247 |

332 |

87 |

0 & 5,960 |

>=200 – <500 |

1,060 |

502 |

1,562 |

3,43,633 |

1037 |

525 |

-4,770 & 249 |

1,243 |

319 |

0 & 13,124 |

>=100 – <200 |

1,695 |

676 |

2,371 |

5,39,871 |

1744 |

627 |

-48,700 & 249 |

1,949 |

422 |

0 & 54,945 |

>=50 – <100 |

3,300 |

1,003 |

4,303 |

6,86,302 |

3330 |

973 |

-10,649 & 247 |

3,534 |

769 |

0 & 14,683 |

>=25 – <50 |

6,251 |

1,401 |

7,652 |

7,38,248 |

6066 |

1586 |

-1,850 & 249 |

6,307 |

1,345 |

0 & 9,466 |

>=10 – <25 |

16,081 |

2,354 |

18,435 |

9,13,833 |

14514 |

3921 |

-614 & 248 |

15,137 |

3,298 |

0 & 7,960 |

>=5 – <10 |

20,165 |

1,950 |

22,115 |

5,99,014 |

17404 |

4711 |

-424 & 246 |

18,004 |

4,111 |

0 & 64,265 |

>=1 – <5 |

69,559 |

4,026 |

73,585 |

7,73,869 |

55671 |

17914 |

-304 & 249 |

56,366 |

17,219 |

0 & 19,384 |

>=0.5 – <1 |

35,007 |

1,554 |

36,561 |

1,61,512 |

26408 |

10153 |

-544 & 245 |

26,671 |

9,890 |

-0.956 & 3,614 |

>=0.2 – <0.5 |

45,284 |

1,775 |

47,059 |

1,63,897 |

33440 |

13,619 |

-121 & 239 |

33,294 |

13,765 |

-0.476 & 10,468 |

>0 – <0.2 |

1,14,310 |

3,738 |

1,18,048 |

1,79,524 |

84351 |

33,697 |

-2,050 & 249 |

72,280 |

45,768 |

0 & 5,145 |

<=0 |

2,53,690 |

13,142 |

2,66,832 |

9,66,210 |

232093 |

34,739 |

-9,720 & 249 |

1,54,789 |

1,12,043 |

-0.032 & 14,434 |

Total |

5,6-6,935 |

32,552 |

5,99,487 |

67,8-9,203 |

4,76,536 |

1,22,951 |

3,9-0,365 |

2,0-9,122 |

||

- Companies with negative net worth of even (-) Rs. 2,640 cr to (-) Rs. 25,300 cr.

- 5 such companies have debt over Rs 25,000 crores, with turnover range of Rs 907 Cr to 31800 Crores

- Companies with negative net worth of even (-) Rs. 3,810 crore to positive net worth of Rs 250 crore has indebtedness of even above Rs 1,000 crore or more with turnover range of Rs. 0 Cr to Rs 15179 Cr.

- The entire Table 1.5 is a clear and evidence that Indian corporate are a complex situation and trying to bring exemption regulations based on Net worth criteria or Turnover criteria or Indebtedness criteria, all can backfire on the financial system. Also, it may be noted that this analysis is only talking of year-end figures and not the peak balances.

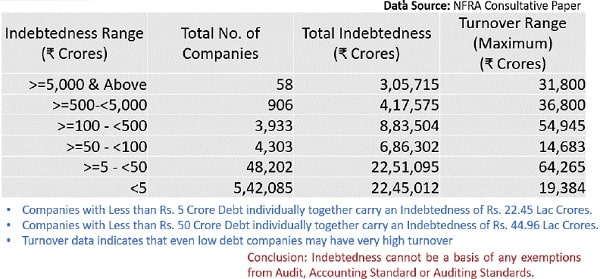

- Companies with Low Debt may have high turnover and substantial Overall Debt Exposure as would be clear from table below:

20. Additional issues

- The Data collated by NFRA Consultative paper captures historically reported data which only captures year end figures: –

- The data ignores

- Mid-Year Peak Indebtedness

- Significant Transactions of Non-Revenue nature which may not appear in yearend balances

- Advances (given or taken during the year)

- Transactions getting settled on net basis

- Size of Investments held by the company

- The data given by them in their report itself supports the case of strengthening the audit function further, and not for any possible relaxation.

a) Extract of Table 1.6 from the Consultative Paper

| Payments to Auditors Analysis | |||

| Table 1.6 Payments to Auditors Analysis of Companies with Net Worth below ₹ 250 crores (all amount in actuals except no. of companies) | |||

| No. of Companies | |||

| Auditors Payments Range (₹ Actuals) | Private | Public | Total No. of Companies |

| >=50,00,000 | 177 | 87 | 264 |

| >=10,00,000-<50,00,000 | 3,818 | 1,004 | 4,822 |

| >=5,00,000-<10,00,000 | 4,887 | 1,185 | 6,072 |

| >=1,00,000-<5,00,000 | 33,357 | 4,966 | 38,323 |

| >=50,000-<1,00,000 | 34,272 | 2,977 | 37,249 |

| >=25,000-<50,000 | 78,430 | 4,714 | 83,144 |

| >=10,000-<25,000 | 1,23,390 | 6,336 | 1,29,726 |

| >=5,000-<10,000 | 74,694 | 3,090 | 77,784 |

| >=1,000-<5,000 | 38,127 | 1,764 | 39,891 |

| >0-<1,000 | 754 | 63 | 817 |

| 0 | 1,75,025 | 6,367 | 1,81,392 |

| <0 | 1 | 2 | 3 |

| Total | 5,66,932 | 32,555 | 5,99,487 |

Comments:

- This table only reflects that the Audit profession is not being adequately paid, as most of the companies with fairly large net worth, turnover, indebtness are still paying relatively low Audit fee.

- It may be appropriate if the ICAI as a regulator is permitted to undertake a detailed analysis and work out few parameters based on which fee can be determined.

- In our view best criteria would be based on time actually spent by differently qualified and experienced persons for which a minimum fee can be prescribed by ICAI MCA (as per formulae of determination of cost of time spent plus over needs as a percentage over Salary/annual income plus a markup of about x % to words margin for the firm

- Similar cost can be worked out for trainee staff, partners and Sr. Partners and billing can be at a minimum of per hour rate, subject to overall limit based on turnover, debt or net worth can be fixed as range of fee for stat audit and internal audit assignment. Fee can never be limited to profit as it is misconduct as per case of ethics.

b) Extract of Table 1.7 from the Consultative Paper

| Table 1.7: Estimated Cost of Audit | |||||

| Turnover Range (In Rs. crores) | Estimated Audit Fees | Avg PBT per Company (in Rs. Lakhs)* | Avg. of Estimated Audit Fees as % to PBT# |

||

| Small Firm – Small Town (in Rs. Lakhs) | Small Firm –Mid Tier City (in Rs. Lakhs) | Small Firm – Metro City (in Rs. Lakhs) | |||

| >=25,000-<50,000 | 37.09 | 62.43 | 106.19 | 2,144 | 4.95% |

| >=10,000-<25,000 | 33.95 | 57.15 | 97.22 | 22,132 | 0.44% |

| >=5,000-<10,000 | 22.07 | 37.15 | 63.20 | 10,969 | 0.58% |

| >=1000-<5000 | 13.80 | 23.23 | 39.51 | 4,798 | 0.82% |

| >=800-<1000 | 8.11 | 13.65 | 23.21 | 3,535 | 0.66% |

| >=500-<800 | 6.47 | 10.89 | 18.52 | 2,308 | 0.80% |

| >=200 – <500 | 4.03 | 6.78 | 11.53 | 1,560 | 0.74% |

| >=100 – <200 | 3.62 | 6.10 | 10.38 | 770 | 1.35% |

| >=50 – <100 | 3.26 | 5.49 | 9.34 | 398 | 2.34% |

| >=25 – <50 | 2.94 | 4.95 | 8.43 | 203 | 2.68% |

| >=10 – <25 | 2.64 | 4.44 | 7.56 | 105 | 4.65% |

| >=5 – <10 | 2.38 | 4.00 | 6.80 | 53 | 8.25% |

| >=1 – <5 | 2.14 | 3.60 | 6.13 | 25 | 15.86% |

Comments:

- The estimates given in the table are hypothetical and are far away from reality.

- The Appendix 1 attached to the table is also far away from real and actual time required to be spent on audit.

- Now most of the audit firm have latest digital tools and analysis, determination of concern areas, verification, bringing out exceptions and taking out audit issues is all undertaken, by software like Inflo, ACL, Idea, Excel, ERP inbuilt tools and of course firm specific special artificial intelligence developed by the firm.

- The number of hours required to be spent is much low as compared to what is calculated in the table and accordingly concluding drawn by consultative paper are all the critical and are to be rejected.

- The audit fee being currently paid is too low as analysed by NFRA but risk of Indian companies is increasing and audit is important.

21. International Scenario: An Analysis

A detailed analysis of international exemption from statutory audit has been done, which is highly appreciated. It is important to observe that most of the jurisdiction have the criteria based on

-

- Turnover

- No. of employees

- Balance Sheet Total Assets

- Most countries have negligible black or parallel economy – Laws are very tough and Investors are protected

- The purchasing power parity of India and its per capita income is quite low as compared to developed economies included in NFRA Consultative Paper.

- In India, there can be significant monetary transactions even in small capital, small turnover or with low number of employees.

- No Exemption from Audit is required in India, in view of analysis given herein, and to avoid risk of tax evasion, money laundering, and loss of complete credibility.

Looking into tabular analysis of actual Indian data of company is actual borrowing actual turnover, net worth and other criteria being so complexly intermixed, applying an interventional formula or base will be hitting the Indian Eco-System suddenly so deep, that we all will be shocked. The table analysis has proved beyond doubt that no audit exemption can be thought of.

22. Audit Documentation and Standard: The auditing and accounting standards cannot be diluted. The smaller firms and small Companies as defined by ICAI may be given specific exemptions from the identified provisions including AS 15 employee benefits, Deferred tax, Fair value, and others as may be recommended by ICAI. Similarly, Audit Documentation and audit procedures can be different in case of small Companies.

- We need to upgrade the Audit quality including depth of audit and to meet audit expectations, technology absorption, Artificial intelligence is the solution

- Fraud, diversion of funds, misuse of funds all can be reduced significantly by appointment of independent auditors by ensuring:

- Mandatory appointment of Joint Auditors

- Limited number of large audits per firm

- Public interest Entity audit to be appointed by a transparent system, like CAG appointment system

- Smaller firms to be joint auditors-mandatorily, with a large firm in case of larger audits.

23. Tax Audit Limit: The Govt of India has set the tax audit limit at Rs 100 lakhs turnover and in case of 95% plus digital transactions the limit is Rs. 1000 lakhs. The recent enhancement of the limit is too fast and may have repercussion even beyond contemplation like, massive fall in tax revenue, enhancement of scrutiny additions, increased non-compliances

24. GST Audit: The recent move for doing away GST Audit shortly after it’s introduction without fully appreciating the contribution of GST Audit in overall compliance, reconciliation, and record sanitisation. The Collection of Taxes during the months of finalisation of GSTR-9 (via DRC03) in the process of GST audit is substantial. The same is a contribution of Audit Community to Governments’ Revenue.

25. Answer to Specific Questions raised by NFRA in their Consultative Paper

1. Question No. 1

Do you think that Micro, Small and Medium Companies (MSMCs) depending upon some criteria and threshold should be exempted from the mandatory statutory audit under Companies Act, 2013? If not, why not and if yes, what would be the criteria and thresholds for exemption?

Response to Question No. 1

Micro, Small and Medium Companies (MSMCs) should not be exempted from the mandatory statutory audit under Companies Act, 2013. In the preceding pages we have given several basis and analysis which clearly establish that any such move will be against the National Economic Interest and will adversely effect growth of trade, commerce and business. The detailed reasoning of how this exemption will negatively impact has been explained in detail in the preceding pages, while to summarise the following are critical Risk of Unaudited financial statements, which may be taken note of: –

- Lack of Corporate Governance

- Financial statements may be drawn without books of accounts

- Non-compliance of Generally Accepted Accounting Principles and basic concepts of accounting

- Unaccounted bank transactions

- Lack of Financial discipline or disclosures

- Large scale non-performing assets unreported

- Loans extended without security or adequate documentation- even where Board may so mandate

- Charging of personal expenses to books

- Charging of unsupported expenses and booking unsupported income

- Non- maintenance of books of accounts and statutory records

- Routing of corrupt money and crime money through their bank accounts using exempted Companies as a money laundering layer

- Recording of non-existent assets

- Unaccounted liabilities or contingent liabilities

- Syphoning of funds

- Unreported Frauds impacting controls, efficiency, existence

- Large unreported cash transactions

- Diversion of funds and misuse of funds

- No observation of laws governing transactions

- How to determine eligibility for FDI, ODI, tenders, services, supplies in the absence of reliable financial statements.

- Even normal business agreements, collaborations, joint venture, national and international bidding, private equity investments, private placements, preferential issues, valuations all will become meaningless as there will be no credible support to various decisions.

- All items of Companies Audit Report Order (CARO) report and main audit report will remain unexamined causing significant loss to Company, shareholders, investors, banks, government and entire economy and society

- The above list is only illustrative and not exhaustive.

- Economy will be hit adversely: The withdrawal of audit requirement will be suicidal and will hit the Indian economy very deeply and below the belt.

- No credibility to financial statements: How the lenders, vendors, suppliers, lessors, customers, employees, regulators, Government departments, RBI, export and import agencies, customs, GST department and income tax department and other stakeholders will rely on the financial statements of such Companies and entities.

2. Question No. 2

Do you think there is a requirement for a separate set of auditing standards for MSMCs as it exists for accounting standards? If no, why not and if yes, what should be the basis for the same?

Response to Question No. 2

This question requires detailed research, analysis and dwelling upon by The Institute of Chartered Accountants of India. In terms of Companies Act, 2013 it is for The Institute of Chartered Accountants of India to propose Auditing Standards for all or any class of companies which can further be evaluated by Board of NFRA and further recommended to Ministry of Corporate Affairs. We humbly submit that the Parliament of India has rightly structured this, and we leave it to the Judgement and wisdom of The Institute of Chartered Accountants of India to decide if there is a need to propose a different set of standards or some relaxations from the existing standards to Audits of Specific class or size of companies.

3. Question No. 3

The cost of conducting an audit as per the prescribed standards is an important input for the responses to Questions 1 and 2. Do you agree with the approach for estimating standard cost of audit computed by NFRA? If not, which areas/ assumptions need changes?

Response to Question No. 3

Chartered Accountant firms charge a reasonable professional fee for the work done by them. We must also appreciate that Profit or Earning is not the sole objective for any Professional. Chartered Accountancy is a Noble Profession and understands that they are partners in Nation Building. The costing analysis captured in the paper overlooks the ground realities and is based on wrong assumptions. All Chartered Accountant Firms comply with all Auditing Standards and test the compliance of Accounting Standards by clients while performing Audit. The quality of Audit has been deeply monitored by The Institute of Chartered Accountants of India over the last 7 decades and is continuously improving with Continued Professional Training, Education and Research. In addition to deep education and training, the chartered accountants have developed expertise, excellence and insight and are able to provide very high quality professional audit to ensure that the financial statements are of highest quality and are free from material misstatements, fraud or error. The quality of audit is further monitored by detailed Peer Review Exercise undertaken by the Peer Review Board of ICAI. The Government of India has further setup Quality Review Board for a Hot Review of select companies in terms of The Chartered Accountants Act, 1949. The Institute of Chartered Accountants of India further monitor published financial statements through Financial Reporting Review Board. All such reviews have provided adequate guidance to the membership at large to continuously improve and excel in their Audits.

4. Question No. 4

Do you think the current exemption thresholds for CARO, ICFR and statutory audit applicability need to be standardised and made uniform? If no, why not and if yes, what would be the criteria and thresholds?

Response to Question No. 4

This criteria of current threshold for CARO and ICFR has been determined on the basis of detailed research, analysis and dwelling upon by The Institute of Chartered Accountants of India and an active consultation with Ministry of Corporate Affairs has resulted in a balanced threshold. Based on our detailed review, research and consultation with various stakeholders, we believe that these criteria do not require any modification.

Note: The above input is based on a detailed discussion with 1,000+ CA firms and with many stakeholders and the Members of All India Chartered Accountants Society. We may be allowed an opportunity of being heard by NFRA Board. The invite may be sent on: +91 9811040004 / +91 9711310004 or email on aicas.cfo@gmail.com

Enclosed: Brief Power Point Presentation capturing key highlights and executive summary of our comments. The Presentation forms part of our comments.