Summary of Companies (Corporate Social Responsibility Policy) Amendment Rules, 2021

♣ On 22.01.2021, the Ministry of Corporate Affairs notified the Companies (Corporate Social Responsibility policy) Amendment Rules, 2021

♣ These amendments have introduced some significant changes to provide framework for implementation of new provisions of the Companies (Amendment) Act 2019 and Companies (Amendment) Act 2020.

–

–

–

WHAT ARE IMPLICATIONS IN CASE OF UNSPENT CSR FUNDS ?

–

Increased Rigor on Internal Control

- Board to satisfy that CSR fund is utilized for the purpose approved by it

- CFO or person responsible for financial management to certify for CSR fund utilization

- Board to monitor implementation of ongoing projects with respect to approved timelines

- New disclosure templates applicable for FY 2020-21:

- Excess CSR spend carried forward & set- off

- Surplus arising out of CSR projects

- Unspent CSR amount transferred to “Unspent CSR Account” and/or “Schedule VII funds”

- Separate disclosure for “ongoing projects” and “other than ongoing” projects

- Details of capital assets created under CSR

–

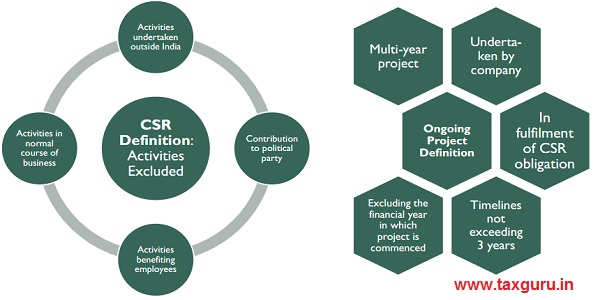

COMPARISON OF CSR AMENDMENT RULES, 2021

| Particular | Prior to notification of rules | After notification of rules |

| Ongoing Project Definition | Not defined | Multi-year project undertaken by company in fulfilment of CSR obligation not exceeding 3 years excluding financial year in which it was commenced |

| Mandatory Registration of Implementation agency | Earlier, No requirement of Mandatory registration | From 1 April 2021, Entities carrying out CSR activities are required to file with the Central government, an e-form namely CSR -1 to generate Unique registration number. |

| Carry forward and set off the CSR expenditure | Earlier, Carry forward and/or set off was not allowed | Amended rules now allows carry forward and set off such excess amount against the requirement to spend for immediately succeeding 3 financial years |

| Mandatory Transfer of unspent CSR amount. | Unspent amount was not required to be transferred to any fund | Mandatory transfer of unspent CSR amount is required to be transferred to funds specified in schedule VII |

| Responsibility of a Board and CFO/person responsible for financial management | Earlier, responsibility was not specifically provided | Board shall be responsible to:

satisfy itself that the funds so disbursed have been utilized for the purposes and in the manner as approved by it. monitor the implementation of the project with reference to the approved timelines CFO or the person responsible for financial management shall certify to the effect |

| Annual action plan by CSR Committee | CSR committee shall institute a transparent mechanism for implementation of projects or programmes or activities undertaken by company | The CSR Committee shall formulate and recommend to the Board, an annual action plan which shall include:

|

| Annual Report on CSR activities to be included in Board’s Report – Content | 1. Brief outline of CSR policy

2. Composition of CSR Committee 3. Prescribed CSR expenditure along with details of spending 4. Details of Implementation agency 5. Reason if the company fails to spend 2% of net profits as obligation |

1. Brief outline of CSR policy

2. Composition of CSR Committee 3. Prescribed CSR expenditure 4. Reason if the company fails to spend 2% of net profits as obligation 5. Web-link of the website where CSR Committee, CSR policy and CSR projects are disclosed 6. Details of amount available for set-off (financial year wise), if any 7. Details of CSR amount spend to be categorised in “ongoing projects” and other then ongoing projects” 8. Details of Unspent CSR amount for 3 preceding F.Y 9. Details of CSR amount spent in F.Y for “ongoing projects” of the preceding F.Y’s. |

| Penalty Clause | No specific penalty was prescribed earlier for non-compliance | Penalty Clause if company fails to:

1. Disclose unspent amount in Annual Report on CSR 2. Transfer Unspent Amount relating to other than ongoing project in Fund Specified in Schedule VII Within Specified Time 3. Transfer unspent amount relating to ongoing project into unspent CSR account within specified time 4. Transfer amount remaining in unspent CSR account after 3 years into fund specified in schedule VII within specified time Penalty amount: 1. Company in default: 2 times the amount required to be transferred to fund specified in schedule VII or Rs. 1 crore; whichever is less 2. Every officer in default: 1/10th of amount required to be transferred to fund specified in schedule VII or Rs. 2 lacs: whichever is less |

| Website Disclosure | Disclose contents of CSR policy on the company’s website, if any, | New Disclosure on Website, if any –

|

Author Bio