The Presenting Officer further submitted that the Auditor of the company i.e. M/s SRBC & Co. LLP, Chartered Accountants, has not comply its duty as per the provision of Section 143(3) of the Companies Act, 2013, with respect to non-quantification of the Related Party Transaction as per para 23A of the IND-AS-24. Hence, non-complying the adequate reporting of the Related Party Transaction as per the provision of the Accounting Standard is the contravention the provision of section 143(3) of the Companies Act, 2013 which impact the view of the stakeholders.

The Presenting officer stated that provision of section 450 of the Companies Act, 2013 empowered the Adjudication Authority to impose penalty where no specific penalty or punishment is provided under the Act;

Therefore, the Auditors Firm M/s. SRBC & Co. LLP, Chartered Accountants is liable to penalize under Section 450 of the Companies Act, 2013 in respect of negligence of their duty as defined u/s 143 (3) of the Companies Act, 2013 being any other person as said provision of law.

MCA imposes penalty of Rs. 50000.

GOVERNMENT OF INDIA

MINISTRY OF CORPORATE AFFAIRS

OFFICE OF THE REGISTRAR OF COMPANIES.

GUJARAT. DADRA 8 NAGAR HAVELI

ROC Shaun. Opp. Rupal Park.

Nr. Mkur Bus Stand. Narangura. Ahmedabad (Gujarat) – 380013.

Tot No.: 079-27438531, Fax : 079-27438371

Website : www.mca.gov.in E-mail : roc.ahmedabad@mca.gov.in

BEFORE THE ADJUDICATING OFFICER

REGISTRAR OF COMPANIES, GUJARAT, DADRA & NAGAR HAVELI

Order No. ROC-GI/ADJ. ORDER/ SUN PHARMA/ Sec.454/ 203-24/457 Dated: 28 APR 2023

ORDER FOR PENALTY UNDER SECTION 454 OF THE COMPANIES ACT, 2013 READ WITH COMPANIES (ADJUDICTION OF PENALTIES) RULES, 2014 AND COMPANIES (ADJUDICATION OF PENALTIES) AMENDMENT RULES, 2019 FOR VIOLATION OF SECTION 143(14) R/W SECTION 188 AND 204 OF THE COMPANIES ACT, 2013 READ WITH RULES MADE THEREUNDER.

IN THE MATTER OF M/s. SUN PHARMACEUTICAL INDUSTRIES LIMITED

(L24230GJ1993PLC019050)

Date of Hearing: 28/03/2023

Present:

1. Shri R.C. Mishra, ICLS (ROC), Adjudicating Officer

2. Neelambuj, ICLS (AROC), Presenting Officer

3. Mansi Gokhle, ICLS (Trainee Officer)

4. Shri Prince Kumar, ICLS (Trainee Officer)

Company/ Officers/ Authorised Representative etc.:

1. Mr. Paul Michael Alvares, Partner of M/s SRBC & Co. LLP, Chartered Accountants appeared

2. Mr. Amit Singh, Partner of M/s SRBC &Co. LLP, Chartered Accountants appeared

3. Mr. Sidhant Rish, Partner of M/s SRBC &Co. LLP, Chartered Accountants appeared

Appointment of Adjudication Authority:-

1. The Ministry of Corporate Affairs vide its Gazette Notification No. A-42011/112/2014-Ad.II dated 24.03.2015 has appointed the undersigned as Adjudicating Officer in exercise of the powers conferred under section 454 of the Companies Act, 2013 (hereinafter known as Act) read with Companies (Adjudication of Penalties) Rules, 2014 (Notification No. GSR 254(E) dated 31.03.2014) for adjudging penalties under the provisions of Act.

Company/any other Person in default;

2. M/s. SRBC & Co. LLP, Chartered Accountants was appointed as Statutory Auditors through e-form ADT-1 vide SRN: G54601208, dated-03/10/2017 from FY 2017-18 to FY 2021-22 by Board of Directors of M/s. SUN PHARMACEUTICAL INDUSTRIES LIMITED (SPIL), which is a company registered under the provisions of the Companies Act, 2013 in the State of Gujarat, having CIN: L24230GJ1993PLC019050 and presently having its registered office situated at “SPARC, Tandalja, Vadodara390012, India”.

Fact about of the case and Show Cause Notice;

3. The Inquiry of M/s. SUN PHARMACEUTICAL INDUSTRIES LIMITED under Section 206(4) of the Companies Act, 2013 ordered by Ministry of Corporate Affairs in the affair of the company covering Financial Years 2014-15, 2015.16, 2016-17 and 2017 In connection to the Inquiry, the Inquiry Officer has issued Show Cause Notice vide office letter No. ROC-GJ/ADJ/U/S 454/ SUN PHARMA/2022-23/5472 TO 5474, dated 10.11.2022 to the Statutory Auditor of the company for FY 2017-18 to M/s SRBC & Co LLP, Chartered Accountants in respect of non-disclosure of material related parties transaction details, as per the requirement of IND-AS-24 of M/s Aditya Medisales Ltd.

Reply of Auditor and physicals hearing:-

4. In respect of the aforesaid notice, M/s SRBC & Co LLP, Chartered Accountants submitted their written reply on 6. December, 2022 which is taken on record. In respect of the Adjudication notice, they had present before Adjudication Authority office on 28. March, 2023 for physical hearing. They submitted that the M/s SRBC & Co LLP, Chartered Accountants, had audited the financial statement of the company with utmost diligence adhering to the requirements of the Companies Act, 2013, Standards of Auditing and other applicable audit requirements. They submitted that M/s Aditya Medisales Ltd disclosed as Related Party in Note no. 52 and Note no. 75 of the Standalone and Consolidated financial statements respectively of the company for the financial year ended March 31, 2018 (FY 2017-18). They have made further submission during the process of Adjudication are as under;

1. Aditya Medisales Ltd (AML) was disclosed as a Related Party under IND-AS 18 disclosure in the FY 2017-18.

2. Transaction with AML were disclosed as part of Related Party transaction in FY 2017-18 under category of “Others”.

3. SRBC & Co LLP is of in view that this is in compliance with the requirements of IND-AS 24.

4. They have also submitted that there are no elements of fraud as per the provision of the Companies Act, 2013.

Hence as per their opinion, they have complied the requirement of provision of the Companies Act, 2013, IND-AS-24 and SEBI (LODR)2015 and no penalty ought to be levied against them.

Submission of the Presenting Officer;

5. The Presenting Officer submitted that the Statutory Auditor play a crucial role while conducting Audit and submission their report. In this case, the Statutory Auditor has made omission of the adequate facts while reporting of the Related Party Transaction (RPTs) and thus negligence in their duty as per the provision of section 143(3) of the Companies Act, 2013.

6. The Presenting Officer further submitted as under;

A. Pursuant to clause (h) of sub-section (3) of section 134 of the Act and Rule 8(2) of the Companies (Accounts) Rules, 2014, the company need to disclose Material RPT in AOC-2 (also prescribed in AOC-2). Hence. the transaction as defined under Rule 15 of The Companies (Meetings of Board and its powers) Rules, 2014 is called Material RPT.

Therefore, as per the said rules sale, purchase or supply of any goods or materials, directly or through appointment of agent, amounting to ten per cent. or more of the turnover of the company or rupees one hundred crore, whichever is lower is called Material RPT.

Hence, the transaction made by the company exceed from 10% of the annual consolidated turnover i.e. FY 2016-17 (10% of Rs 8308.28 Cr i.e. Rs 830 Cr) or Rs. 100 Cr whichever is lower called Material Transaction.

B. Further, as per the regulation 23 of SEBI(Listing Obligation and Disclosure Requirement) Reg, 2014.

The listed entity shall formulate a policy on materiality of related party transactions and on dealing with related party transactions.

Explanation.- A transaction with a related party shall he considered material if the transaction(s) to he entered into individually or taken together with previous transactions during a financial year. exceeds ten percent of the annual consolidated turnover of the listed entity as per the last audited financial 5 statements of the listed entity.

Hence, the transaction made by the company exceed from 10% of the annual consolidated turnover i.e. FY 2016-17 (10°A, of Rs 8308.28 Cr i.e. Rs 830 Cr) is called Material Transaction.

C. Also, as submitted by the Auditor that the transaction of AML has been merged with others. But which is not appropriate in terms of IND-AS-24.

As per para 24 and 24 A of Ind AS-24 which is stated which stated as under;

24. Items of a similar nature may be disclosed in aggregate except when separate disclosure is necessary for an understanding of the effects of related party transactions on the financial statements of the entity.

24A. Disclosure of details of particular transactions with individual related parties would frequently be too voluminous to be easily understood, Accordingly, items of a similar nature may be disclosed in aggregate by type of related party. However, this is not done in such a way as to obscure the importance of significant transactions. Hence, purchases or sales of goods are not aggregated with purchases or sales of fixed assets. Nor a material related party transaction with an individual party is clubbed in an aggregated disclosure.

Hence, as per para 24A of Ind AS-24, the Auditor is need to disclose Material RPTs transaction separately as per para 18, 19, 20 of IND-AS-24.

7. The Presenting Officer further stated that the inquiry of the subject company is based on Whistle Blower Complaint in respect of Related Party Transaction, Money Diversion from Sun Pharmaceutical Industries Ltd to Aditya Medisales Ltd and other group companies. In the said matter, the Serious Fraud Investigation Office (SF10), Ministry of Corporate Affairs also made research and shared a Market Research and Analysis Report (MRAU) to this office in year 2019. Accordingly, the Inquiry into affairs of the company is independently directed by the Ministry of Corporate Affair to this office to investigate the Related Party Transaction matter of the Sun Pharmaceutical Industries Ltd. with Aditya Medisales Ltd covering the FY 2014-1S to 2017-18 and the omission of reporting of Related Parties Transaction (RPTs) and violation of the Companies Act, 2013.

It is observed from the ledger submitted by the company in respect of the transaction of FY 2017-18 with Aditya Medisales Ltd. that the cumulative sales transactions exceed from Rs.900 Cr. Hence, the transaction fall under the purview of Material Related Party Transaction. It is found that the Auditor has not reported ANY Material Related Party Transaction as per the requirement of IND-AS-24 (10./0 of Rs 8308.28 Cr i.e. Rs 830 Cr) or Rs .100 Cr whichever is lower)

Therefore. the Auditor has not reported and quantified any Material Related Party Transaction as per the requirement of para 24A of the IND-AS-24. Instead of reporting the said material transaction separately, the company has merged the same with OTHERS. It is found that the apart from Aditya Medisales Ltd, the company intervened into Material Related Party Transaction with Sun Pharma Laboratories Limited, Sun Pharma Medisales Private Limited, Be-Tabs Pharmaceuticals (Pty) Ltd, Sun Pharma Global (FZE), Sun Pharmaceutical Industries, Inc., Sun Pharmaceutical Industries (Europe) 8.y., which fall under the ambit of Material RPT. The Auditor failed to report the said material transaction separately in its Report for the FY 201718 as per the para 24A of IND-AS-24.

8. The Presenting Officer further stated that merely stating name of RPTs is not adequate in disclosing the Related Party Transactions. It is equally important that MATERIAL RPTs to be pointed out and quantified separately considering the special significance attached to the quantum of shareholders money involved. Negligence on this count, is taken on account and penalty under section 450 of the Companies Act, 2013 should be impose for not discharging their statutory duty. Further, it is found from the record of the company that the Auditor of the company made noncompliance in respect of said provision in FY 2018-19, 2019-20, 2020-21 and 202122 also.

9. The Presenting Officer further submitted that the Auditor of the company i.e. M/s SRBC & Co. LLP, Chartered Accountants, has not comply its duty as per the provision of Section 143(3) of the Companies Act, 2013, with respect to non-quantification of the Related Party Transaction as per para 23A of the IND-AS-24. Hence, non-complying the adequate reporting of the Related Party Transaction as per the provision of the Accounting Standard is the contravention the provision of section 143(3) of the Companies Act, 2013 which impact the view of the stakeholders.

10. The Presenting officer stated that provision of section 450 of the Companies Act, 2013 empowered the Adjudication Authority to impose penalty where no specific penalty or punishment is provided under the Act;

Therefore, the Auditors Firm M/s. SRBC & Co. LLP, Chartered Accountants is liable to penalize under Section 450 of the Companies Act, 2013 in respect of negligence of their duty as defined u/s 143 (3) of the Companies Act, 2013 being any other person as said provision of law.

ORDER

11. After hearing the matter in detail, the Adjudicating Officer has given due regard to the following facts while passing the order, namely;

a. The amount of disproportionate gain or unfair advantage, whenever quantifiable, made as a result of default.

b. The amount of loss caused to an investor or group of investors as a result of the default_

c. The repetitive nature of default.

12. Having considering the submission made by the Presenting Officer, counter submission made by the Auditor and aforesaid facts & circumstances, the undersigned has reasonable cause to believe that the Auditor of the company has failed to discharge their duty as per the provisions of Section 143(3) of the Companies Act, 2013 read with Accounting Standard (IND-AS). In view of the facts narrated above, the Auditor of the company, in default are liable for penalty as per Section 450 of the Act being any other person as per the said provision of law.

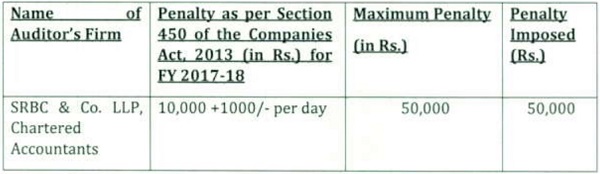

13. Having considered the facts and circumstances of the case and submissions made by Presenting Officer, counter submission made by the Auditor M/s SRBC & Co. LLP, Chartered Accountants Firm and after taking into accounts the facts & factors above, I hereby imposed a penalty on Auditors Firm as per table below for violation of section 143(3) of the Companies Act, 2013 for FY 2017-18. I am of the opinion that penalty is commensurate with the aforesaid failure for not discharging theirs statutory duty.

Penalty on Auditors Firm for default;

14. The noticee shall pay the amount of penalty by way of e-payment available on Ministry website www.mca.gov.in under “Pay miscellaneous fees” category in MCA fee and payment Services under Rule 3(14) of Company (Adjudication of Penalties) (Amendment) Rules, 2019 within 60 days from the date of receipt of this order and copy of this adjudication order and Challan/SRN generated after payment of penalty through online mode shall be filed in INC-28 under the MCA portal without further reference.

15. Appeal against this order may be filed in writing with the Regional Director, North Western Region, Ministry of Corporate Affairs, ROC BHAVAN, OPP. RUPAL PARK, NR. ANKUR BUS STAND, NARANAPURA, AHMEDABAD (GUJARAT)-380013 within a period of sixty days from the date of receipt of this order. in e-form ADJ (i.e. Memorandum of Appeal), setting forth the grounds of appeal and shall be accompanied by the certified copy of this order. [Section 454(5) & 454(6) of the Companies Act, 2013 read with the Companies (Adjudicating of Penalties) Rules, 2014 as amended by Companies (Adjudication of Penalties) Amendment Rules, 2019].

16. Your attention is also invited to Section 454(8)(i) and 454(8) (ii) of the Companies Act, 2013, which state that in case of non-payment of penalty amount, the company shall be punishable with tine which shall not less than Twenty Five Thousand Rupees but which may extend to Five Lakhs Rupees and officer in default shall be punishable with Imprisonment which may extend to Six months or with fine which shall not be less than Twenty Five Thousand Rupees by which may extend to one Lakhs Rupees or with both.

The adjudication notice stands disposed of with this order.

R.C.Mishra, (ICLS)

Registrar of Companies & Adjudicating Officer

Gujarat, Dadra & Nagar Haveli

To:

ROC-GJ/ADJ.ORDER/SUN PHARMA/Sec.454/2023-24

Mr. Paul Alvares

Partner of M/s SRBC & Co. LLP

Ground Floor, Tower C, Unit 1,

Panchshil Tech Park One, Loop Road,

Pune-411006

Copy to:

1. The Director Legal, Ministry of Corporate Affairs

2. The Regional Director, (NWR), Minis, of Corporate Affair, Ahmedabad-380013 (for information please)

3. Office Copy

4. Email to content manager for publication on the Ministry website.