Government of India

Ministry of Corporate Affairs

Invitation for Public Comments on the Companies (Corporate Social Responsibility Policy) Amendment Rules, 2020.

Dated: 13/03/2020

Corporate Social Responsibility (CSR) for companies has been mandated through Companies Act, 2013 which came into effect since 01.04.2014. Section 135 of the Act enumerates the provisions concerning CSR and the Companies (Corporate Social Responsibility Policy) Rules, 2014 prescribes the rules for implementation. All these were notified on 27th February, 2014 and came into effect since 01.04.2014. The Companies (Amendment) Act, 2019 amended section 135 dealing with Corporate Social Responsibility. The Companies (Amendment) Act, 2019 received President’s assent and was published in Official Gazette on 31st July, 2019.

2. In order to operationalize the Companies (Amendment) Act, 2019, the Companies (Corporate Social Responsibility Policy) Amendment Rules , 2020 has been drafted for carrying out amendments in the Companies (CSR Policy) Rules, 2014.

3. Public comments are therefore hereby solicited on the draft Companies (Corporate Social Responsibility Policy) Amendment Rules, 2020. The draft Companies (Corporate Social Responsibility Policy) Amendment Rules, 2020 may be accessed at the web link mentioned below and comments, if any, may be submitted online therein by end of business hours on 28th March, 2020 positively.

4. Stakeholder may please note that comments should not be sent separately through e-mail or hard copy and should be sent only through the web link created for the purpose.

(Shobhit Srivastava)

Deputy Director, MCA

Link to Submit Public Comments on Draft Companies (Corporate Social Responsibility Policy) Amendment Rules, 2020 – Last Date for Submission of Suggestions is March 28, 2020

http://feedapp.mca.gov.in/csr/

| Download Draft Companies (Corporate Social Responsibility Policy) Amendment Rules, 2020

Download Companies (Corporate Social Responsibility Policy) Rules, 2014 |

——————————————–

GOVERNMENT OF INDIA

MINISTRY OF CORPORATE AFFAIRS

NOTIFICATION

New Delhi, the………………. March, 2020

G.S.R…(E).- In exercise of the powers conferred by section 135 and subsections (1) and (2) of section 469 of the Companies Act, 2013 (18 of 2013), the Central Government hereby makes the following rules further to amend the Companies (Corporate Social Responsibility Policy) Rules, 2014, namely:-

1. Short title and commencement. – (1) These rules may be called the Companies (Corporate Social Responsibility Policy) Amendment Rules, 2020.

(2) They shall come into force on the date of their publication in the Official Gazette.

2. In the Companies (Corporate Social Responsibility Policy) Rules, 2014, in rule 2, in sub-rule (1) –

(i) for clause (c), the following clause shall be substituted, namely :-

“(c) Corporate Social Responsibility (CSR)” means the activities undertaken by a Company in pursuance of its statutory obligation laid down in section 135 of the Act in accordance with the provisions contained in these Rules, but shall not include the following, namely-

i) Activities undertaken in pursuance of normal course of business of the company.

ii) Any activity undertaken by the company outside India.

iii) Contribution of any amount directly or indirectly to any political party under section 182 of the Act.

iv) activities that significantly benefit the employees of the company and their families.

Provided that in case of any activity having less than twenty five percent employees as its beneficiary, then such activity shall be deemed to be CSR activity under these rules.”;

(ii) for clause (e), the following clause shall be substituted, namely :-

“(e) “CSR Policy” means a statement containing the approach and direction given by the board of a company, as per recommendations of its CSR Committee, for selection, implementation and monitoring of activities to be undertaken in areas or subjects specified in Schedule VII of the Act.”

(iii) for clause (f), the following clause shall be substituted, namely :-

“(f) “International Organization” means an organization notified by the Central Government as an international organization under section 3 of the United Nations (Privileges and immunities) Act, 1947 (46 of 1947), to which the provisions of the Schedule to the said Act apply.”

(iv) after clause (f) , following sub-clauses shall be inserted, namely:-

“(g) “Net profit” means the net profit of a company as per its financial statement prepared in accordance with the applicable provisions of the Act, but shall not include the following, namely: –

(i) any profit arising from any overseas branch or branches of the company, whether operated as a separate company or otherwise; and

(ii) any dividend received from other companies in India, which are covered under and complying with the provisions of section 135 of the Act:

Provided that net profit in respect of a financial year for which the relevant financial statements were prepared in accordance with the provisions of the Companies Act, 1956, (1 of 1956) shall not be required to be re-calculated in accordance with the provisions of the Act:

Provided further that in case of a foreign company covered under these rules, net profit means the net profit of such company as per profit and loss account prepared in terms of clause (a) of sub-section (1) of section 381 read with section 198 of the Act.

(h) “Ongoing Projects” means a multi-year project undertaken by a Company in fulfillment of its CSR obligation having timelines not exceeding three years excluding the financial year in which it was commenced, and shall also include such projects that were initially not approved as a multi-year project but whose duration has been extended beyond a year by the Board based on reasonable justification.

(i) “Public Authority” means ‘Public Authority’ as defined in sub-clause (h) of section (2) of Right to Information Act, 2005.”

3. In the said Rules, in Rule 3, in sub-rule (2), in clause (b) for the words, brackets and figure ‘sub-section (2) to (5)’, the words, brackets and figure ‘subsection (2) to (8)’ shall be substituted;

4. In the said Rules, for rule 4, the following rules shall be substituted, namely:-

“CSR Implementation – (1) The Board shall ensure that the CSR activities are undertaken by the company itself or through:

(a) a company established under section 8 of the Act, or

(b) any entity established under an Act of Parliament or a State

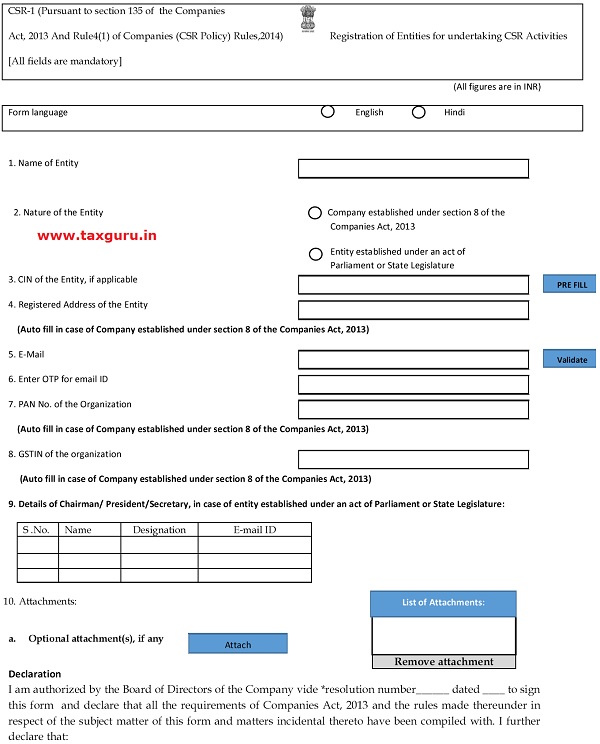

Provided that such company/entity, covered under clause (a) or (b), shall register itself with the central government for undertaking any CSR activity by filing the e-form CSR-1 with the Registrar along with prescribed fee.

Provided further that the provisions of this sub-rule shall not affect the CSR projects or programmes that were approved prior to the commencement of the Companies (CSR Policy) Amendment Rules, 2020.

(2) A company may also collaborate with other companies for undertaking projects or programmes or CSR activities in such a manner that the CSR committees of respective companies are in a position to report separately on such projects or programmes in accordance with these rules.

(3) A company may engage international organizations for designing, monitoring and evaluation of the CSR projects or programmes as per its CSR policy as well as for capacity building of their own personnel for CSR.

Provided that a company may also engage an international organization for implementation of a CSR project subject to prior approval of the central government.

(4) Board of a company shall satisfy itself that the funds so disbursed have been utilized for the purpose and in the manner as approved by it and Chief financial Officer or the person responsible for financial management shall certify to the effect.

(5) In case of ongoing projects, the Board of a company shall monitor the implementation of the project with reference to the approved timelines and year wise allocation and shall be competent to make modifications, if any, for smooth implementation of the project within the overall permissible time period. “

5. In the said Rules, in rule 5, for sub-rule (2), the following sub-rule shall be substituted, namely:-

“(2) The CSR Committee shall formulate and recommend to the Board, an annual action plan in pursuance of its CSR policy, which shall include the following:

(a) the list of CSR projects or programmes that are approved to be undertaken in areas or subjects specified in Schedule VII of the Act;

(b) the manner of execution of such projects or programmes as specified in sub-rule (1) of Rule 4;

(c) the modalities of utilization of funds and implementation schedules for the projects or programmes; and

(d) monitoring and reporting mechanism for the projects or

(e) Details of need and impact assessment, if any, undertaken by the company.”

6. In the said Rules, Rule 6 shall be omitted.

7. In the said Rules, for rule 7, the following rules shall be substituted, namely:-

“CSR Expenditure: (1) The board shall ensure that the administrative overheads incurred in pursuance of sub-section (4) (b) of section 135 of the Act shall not exceed five percent of total CSR expenditure of the company for the financial year.

Provided that a company undertaking impact assessment, in pursuance of sub-rule (3) of Rule 8, may incur administrative overheads not exceeding ten percent of total CSR expenditure for that financial year.

(2) Any surplus arising out of the CSR projects or programmes or activities shall not form part of the business profit of a company and shall be ploughed back into the same project or shall be transferred to the Unspent CSR Account and spent in pursuance of CSR policy and action plan of the company.

(3) The CSR amount may be spent by a company for creation or acquisition of assets which shall only be held by a company established under section 8 of the Act having charitable objects or a public authority.

Provided that any asset created by a company prior to the commencement of Companies (CSR Policy) Amendment Rules, 2020, shall within a period of One hundred and eighty days from such commencement comply with the requirement of this rule, which may be extended by a further period of not more than ninety days with the approval of the board based on reasonable justification.

(4)Unspent balance, if any, towards fulfilment of CSR obligation at the time of commencement of these Rules shall be transferred within a period of thirty days from the end of Financial Year 2020-21 to special account viz., ‘Unspent Corporate Social Responsibility Account’ opened by the company and such amount shall be spent by the company in pursuance of its obligation towards the Corporate Social Responsibility Policy within a period of three financial years from the date of such transfer, failing which, the company shall transfer the same to a Fund specified in Schedule VII, within a period of thirty days from the date of completion of the third financial year.”

8. In the said Rules, in rule 8, after sub-rule (2), following sub-rule shall be inserted, namely:-

“(3) A company having the obligation of spending average CSR amount of Rs 5 Crore or more in the three immediately preceding financial years in pursuance of sub section 5 of Section 135 of the Act, shall undertake impact assessment for their CSR projects or programmes, and shall disclose details of the same in its Annual Report on CSR.”

9. In the said Rules, for rule 9, the following rules shall be substituted, namely:-

“Display of CSR activities on its website: The Board of Directors of the company shall mandatorily disclose the composition of the CSR Committee, and CSR Policy and Projects approved by the Board on their website for public viewing, as per the particulars specified in the Annexure.”

10. In the said Rules, after rule 9, following rule shall be inserted, namely:-

“Rule 10 : National Unspent Corporate Social Responsibility Fund :

(1) The Central Government shall establish a fund called the “National Unspent Corporate Social Responsibility Fund” (herein after referred as “the Fund”) for the purposes of sub-section (5) and (6) of section 135 of the Act. The Fund shall be utilized for the purposes of undertaking CSR projects in the in areas or subjects specified in schedule VII of the Act. Provided that until such fund is created the unspent CSR amount in terms of provisions of sub-section (5) and (6) of section 135 of the Act shall be transferred by the company to any fund as specified in schedule VII of the Act.

(2) The manner of administration, authority for administration of the Fund shall be in accordance with such guidelines as may be prescribed by the Central Government from time to time.”

11. In the said rules, in the annexure,-

(i) The e-form CSR-1 shall be inserted, namely:

1. Whatever is stated in this form and in the attachments thereto is true, correct and complete and no information material to the subject matter of this form has been suppressed or concealed and is as per the original records maintained by the company.

2. All the required attachments have been completely and legibly attached.

To be Digitally signed by

Designation

DIN/PAN/Membership number DSC

Certificate by Practicing professional

I declare that I have been duly engaged for the purpose of certification of this form. It is hereby certified that I have gone through the provisions of the Companies Act, 2013 and Rules there under for the subject matter of this form and matters incidental thereto and I have verified the above particulars (including attachment(s)) from the original/certified records maintained by the Company/applicant which is subject matter of this form and found them to be true, correct and complete and no information material to this form has been suppressed. I further certify that:

1. The said records have been properly prepared, signed by the required officers of the Company and maintained as per the relevant provisions of the Companies Act, 2013 and were found to be in order;

2. All the required attachments have been completely and legibly attached to this form;

3. It is understood that I shall be liable for action under Section 448 of the Companies Act, 2013 for wrong certification, if any found at any stage

* Chartered Accountant (in whole time practice)

* Company Secretary (in whole time practice)

* Cost Accountant (in whole time practice)

(Whether fellow or associate)

Note: Attention is drawn to provisions of Section 448 and 449 which provide for punishment for false statement / certificate and punishment for false evidence respectively.

This e-Form has been taken on file maintained by the register of companies through electronic mode on the basis of statement of correctness given by the Director and professional.

Note:- All drop down to be radio buttons.

(ii) For “format for the annual report on CSR activities to be included in the Board’s Report “, the following format shall be substituted, namely:-

ANNEXURE

FORMAT FOR THE ANNUAL REPORT ON CSR ACTIVITIES TO BE

INCLUDED IN THE BOARD’S REPORT

1. CSR Policy of the Company

2. Composition of CSR Committee:

| S. No. | Name of Director | DIN | Designation / Nature of Directorship |

No. of meetings of CSR Committee held during the year |

No. of meetings of CSR Committee attended during the year |

3. Provide the web-link where Composition of CSR committee, CSR Policy and CSR projects approved by the board is disclosed on the website of the company

4. Provide the details of Impact assessment of CSR projects carried out in pursuance of sub-rule (3) of Rule 8 of Companies (CSR Policy) Rules, 2014, if applicable (attach the report)

5. Average net profit of the company as per section 135(5)

6. (a) Two percent of Average net profit of the company as per section 135(5)

(b) Surplus arising out of the CSR projects/ programmes or

activities for the financial year

(c) Total CSR obligation for the financial year (6a+6b)

7. (a). CSR amount spent / unspent for the financial year:

| Total Amount Spent for the Financial Year |

Amount Unspent | |||

| Total Amount transferred to Unspent CSR Account as per Section 135(6) | Amount transferred to National Unspent CSR Fund as per second proviso to Section 135(5) | |||

| Amount | Date of transfer | Amount | Date of Transfer | |

(b) Details of CSR amount spent against ongoing projects for the financial year:

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | ||

S. No. |

Name of the Project |

Project ID (if avail-able) |

Item from the list of activities in schedule VII |

Local Area (Yes/ No) |

Location of the Project |

Project duration |

Amount alloc-ated for the project (in Rs.) |

Amount spent in the Current

|

Amount trans-ferred to Unspent CSR Account for the project as per Section 135(6) (in Rs.) |

Mode of

|

Mode of Implem-entation – Through Implem-enting Agency |

||

State |

Dist-rict |

Name |

CIN |

||||||||||

| 1 | |||||||||||||

| 2 | |||||||||||||

| 3 | |||||||||||||

| 4 | |||||||||||||

| Total | |||||||||||||

(c) Details of CSR amount spent against other than ongoing projects for the financial year:

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | ||

| S. No. | Name of the Project |

Project ID(if avail-able) |

Item from the list of activities in schedule VII |

Local Area (Yes/No) |

Location of the Project |

Amount Spent for the project (in Rs.) | Mode of Impleme-ntation Direct (Yes/No) |

Mode of Impleme-ntation Through Impleme-nting Agency |

||

| State | Dist-rict | Name | CIN | |||||||

| 1 | ||||||||||

| 2 | ||||||||||

| 3 | ||||||||||

| 4 | ||||||||||

| Total | ||||||||||

(d) Amount spent in Administrative Overheads

(e) Total Amount Spent for the Financial Year (7b+7c+7d)

8. (a) Details of CSR amount spent/ unspent for the preceding three financial years:

| 1 | 2 | 3 | 4 | 5 | |

| Preceding Financial Year |

Amount transferred to Unspent CSR Account under section 135 (6) |

Amount Spent in the Current Financial Year(in Rs) |

Amount transferred to National Unspent CSR Fund as per second proviso to Section 135(5), if any | Amount remaining to be spent in succeeding financial years |

|

| Amount (in Rs) | Date of Transfer | ||||

(b) Details of CSR amount spent for ongoing projects of the preceding financial year(s):

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | ||

S. No. |

Proj-ect ID |

Name of the Proj-ect |

Item from the list of

|

Local

|

Location of the Project |

Finan-cial Year in

|

Project dura-tion |

Total amount alloc-ated for the project (in Rs.) |

Amo-unt

|

Cumu-lative

|

Mode of Imple-menta-tion Direct (Yes/ No) |

Mode of

|

||

State |

Dist-rict |

Name |

CIN |

|||||||||||

| 1 | ||||||||||||||

| 2 | ||||||||||||||

| 3 | ||||||||||||||

| 4 | ||||||||||||||

9. Amount transferred to ‘Unspent CSR Account’ pursuant to sub-rule (4) of Rule 7 of Companies (CSR Policy) Rules, 2014 for the financial year 2014-15 to 2019-20

| S. No. | Preceding Financial Year |

Amount transferred to Unspent CSR Account under section 135 (6) |

| 1 | ||

| 2 | ||

| 3 | ||

| 4 | ||

| 5 | ||

| 6 | ||

| Total |

10. In case of creation or acquisition of asset, furnish the details relating to the asset so created or acquired through CSR spent in the financial year.

(a) Date of creation/ acquisition of the asset(s)

(b) Amount of CSR spent for creation /acquisition of asset

(c) Details of the entity/ public authority under whose name such asset is registered, address etc.

(d) Provide details of the property or asset(s) created/ acquired (including complete address and location of the property)

11. Specify the reason(s) if the company has failed to spend two per cent of the average net profit as per section 135(5):

Sd-

(Chief Executive Officer or

Managing director or Director)

Sd-

(Director or Chief Financial Officer)

Sd-

(Person specified under clause (d) of

sub-section (1) of Section 380 of the Act)

(wherever applicable)

[File No. 05/05/2015-CSR]

(Gyaneshwar Kumar Singh)

Joint Secretary to the Government of India

Note.— The principal rules were published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 129(E), dated the 27th February, 2014 and were subsequently amended by notification number G.S.R. 644(E), dated the 12th September, 2014, notification number G.S.R. 43(E), dated the 19th January, 2015 and notification number G.S.R. 540 (E) dated 23rd May, 2016, notification number G.S.R. 895(E) dated 19th September, 2018.

Source: 1. http://feedapp.mca.gov.in/csr/

2. http://feedapp.mca.gov.in/csr/pdf/draftrules.pdf