FAQs FOR CSR u/s 135 of Companies Act, 2013 (Updated till 24/04/2021)

1. What is Applicability of CSR Committee and what shall be its constitution & Functions?

Applicability

♦ As per Section 135 (1) every Company falling under bellow criteria in Previous Financial Year need to constitute CSR Committee:

| Turnover | Rs. 1000 Cr or More |

| Net Worth | Rs. 500 Cr or More |

| Net Profit | Rs. 5 Cr or More |

Constitution

- Minimum 3 (Three) Directors out of which 1 (One) shall be Independent;

- However, when Company is not mandate to appoint Independent Director constitution shall be minimum 2 (Two)

- With respect to a foreign company covered under these rules, the CSR Committee shall comprise of at least 2 (Two) persons of which one person shall be as specified under clause (d) of sub-section (1) of section 380 of the Act and another person shall be nominated by the foreign company

Exemption for framing CSR Committee

- When the amount of CSR to be spent is less than 50 (Fifty) Lakhs then requirement of CSR committee shall be omitted, the work of CSR Committee can be done by Board itself.

Function

- formulate and recommend to the Board, a Corporate Social Responsibility Policy

- recommend the amount of expenditure to be incurred

- monitor the Corporate Social Responsibility Policy time to time

2. What shall be role, responsibility and duty of Board with regards to CSR?

- After taking into account the recommendations made by the Corporate Social Responsibility Committee, approve the Corporate Social Responsibility Policy;

- disclose Content of Policy in Board Report and website if any;

- ensure that the activities as per Corporate Social Responsibility Policy are undertaken;

- ensure that the adequate CSR is made in every financial year;

- ensure preference to the local area and areas around it where it operates, for spending the CSR is given.

3. What CSR expenditure to be made mandatorily?

Every Company falling under bellow criteria in Previous Financial Year it needs to make CSR expenditure:

| Turnover | Rs. 1000 Cr or More |

| Net Worth | Rs. 500 Cr or More |

| Net Profit | Rs. 5 Cr or More |

4. What shall be the minimum amount to be spent as CSR?

- 2 % (Two Percent) of the Average net profits of the company made during the 3 (Three) immediately preceding financial years or where the company has not completed the period of three financial years since its incorporation, immediately preceding financial years.

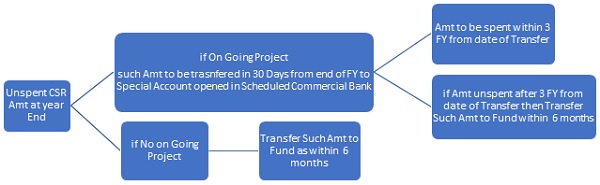

5. What if minimum amount as per Point 4 is not spent?

- Board shall specify the reasons for not spending the amount in Board Report;

- Treatment of unspent amount: –

6. What if excess amount is spent as per Point 4?

- Company may set off such excess amount against the requirement to spend for such number of succeeding financial years.

7. What if default made as per Point 5?

- Company shall be liable to a penalty of twice the amount required to be transferred by the company to the Fund or one crore rupees, whichever is less and;

- every officer of the company who is in default shall be liable to a penalty of one-tenth of the amount required to be transferred by the company to such Fund or two lakh rupees, whichever is less.

8. How net Profit Shall be Calculated for CSR?

- The Calculation Shall be made by allowing and / disallowing income and / expenditure as per Annexure I.

Notes:

- The board shall ensure that the administrative overheads for CSR expenditure shall not exceed five percent of total CSR expenditure of the company for the financial year;

- When company wants to spent for CSR other than itself it shall spend through an entity which is registered by filing e-form CSR 1;

- Fund in which amount to be transferred are Prime Minister’s National Relief Fund, PM Care Fund, Clean Ganga Fund etc;

- Every company which ceases to be a company covered under criteria of CSR for three consecutive financial years shall not be required to –

(a) constitute a CSR Committee; and

(b) Spent for CSR

Annexure I

| Allowable Income | Disallowable Income |

| • Bounties and subsidies received from any Government, or any public authority constituted;

• profits from the sale of any immovable property or fixed assets of a capital nature; • All General Incomes and Revenue. |

• Profits, by way of premium on shares or debentures of the company whether issued or sold;

• profits on sales by the company of forfeited shares; • profits of a capital nature including profits from the sale of the undertaking or any of the undertakings of the company or of any part thereof; • excess amount released by sale of fixed asset to its written down value; • profit for change in Fair Value of Assets; • any amount representing unrealized gains, notional gains or revaluation of assets; |

| Allowable Expenditure | Disallowable Expenditure |

| • All the usual working charges;

• directors’ remuneration; • bonus or commission; • any tax notified by the Central Government as being in the nature of a tax on excess or abnormal profits; • any tax on business profits imposed for special reasons or in special circumstances and notified by the Central Government in this behalf; • interest on debentures issued by the company; • interest on mortgages executed by the company and on loans and advances secured by a charge on its fixed or floating assets; • interest on unsecured loans and advances; • expenses on repairs, whether to immovable or to movable property, provided the repairs are not of a capital nature; • outgoings inclusive of contributions to Bona Fide and Charitable Funds etc.; • depreciation; • any compensation or damages to be paid in virtue of any legal liability including a liability arising from a breach of contract; • any sum paid by way of insurance against the risk of meeting any liability; • debts considered bad and written off or adjusted during the year; • Other general expenses. |

• Income-tax and super-tax payable by the company under the Income-tax Act, 1961, or any other tax on the income of the company

• any compensation, damages or payments made voluntarily, that is to say, otherwise than in virtue of a liability; • loss of a capital nature including loss on sale of the undertaking or any of the undertakings of the company or of any part thereof not including any excess of the written-down value of any asset which is sold, discarded, demolished or destroyed over its sale proceeds or its scrap value; • Loss for change in Fair Value of Assets.

|

Annexure II

Activities which may be considered for CSR:

- Eradicating hunger, poverty and malnutrition, promoting health care including preventive health care, sanitation [including contribution to the Swach Bharat Kosh set-up by the Central Government for the promotion of sanitation and making available safe drinking water;

- promoting education, including special education and employment enhancing vocation skills especially among children, women, elderly and the differently abled and livelihood enhancement projects;

- promoting gender equality, empowering women, setting up homes and hostels for women and orphans; setting up old age homes, day care centres and such other facilities for senior citizens and measures for reducing inequalities faced by socially and economically backward groups;

- ensuring environmental sustainability, ecological balance, protection of flora and fauna, animal welfare, agroforestry, conservation of natural resources and maintaining quality of soil, air and water including contribution to the Clean Ganga Fund set-up by the Central Government for rejuvenation of river Ganga;

- protection of national heritage, art and culture including restoration of buildings and sites of historical importance and works of art; setting up public libraries; promotion and development of traditional art and handicrafts;

- measures for the benefit of armed forces veterans, war widows and their dependents,

- training to promote rural sports, nationally recognized sports, paralympic sports and olympic sports;

- contribution to the prime minister’s national relief fund or PM CARES Fund or any other fund set up by the central govt. for socio economic development and relief and welfare of the schedule caste, tribes, other backward classes, minorities and women;

- Contribution to incubators or research and development projects in the field of science, technology, engineering and medicine, funded by the Central Government or State Government or Public Sector Undertaking or any agency of the Central Government or State Government;

- contributions to public funded Universities; Indian Institute of Technology (IITs); National Laboratories and autonomous bodies established under Department of Atomic Energy (DAE); Department of Biotechnology (DBT); Department of Science and Technology (DST); Department of Pharmaceuticals; Ministry of Ayurveda, Yoga and Naturopathy, Unani, Siddha and Homoeopathy (AYUSH); Ministry of Electronics and Information Technology and other bodies, namely Defense Research and Development Organization (DRDO); Indian Council of Agricultural Research (ICAR); Indian Council of Medical Research (ICMR) and Council of Scientific and Industrial Research (CSIR), engaged in conducting research in science, technology, engineering and medicine aimed at promoting Sustainable Development Goals (SDGs);

- rural development projects;

- slum area development;

- disaster management, including relief, rehabilitation and reconstruction activities.

Author Bio

Dear Sir,

Do you know a Delhi-based company by the name INNOVATIVE FINANCIAL ADVISORS PVT LIMITED (FIINOVATION) is perpetrating a big CSR scam right under the noses of all the enforcement and other agencies.

We are one of the many victims and we suspect the FIINOVATION is involved in some novel scam that has gone undetected. They have a plush, 5-star like office and a very educated and trained staff to allure the unsuspecting NGOs to cough up advance deposits against Legal Agreements for arranging CSR funds for various projects.

Dr. Soumitro Chakraborty, the CEO is the kingpin behind the scam. He does not meet any of the victims even if you make umpteen requests. His staff that includes mostly outwardly well-meaning women staff are hand-in-glove with this fraudster CEO.

Tarakeshwara Foundation is working on preparing a comprehensive case background and send the copies of the same to all the agencies, Ministries, Chambers of Commerce, CII, Companies, NGOs and social media platforms. We can’t digest that an organisation is brazenly looting NGOs and even involved creating fake NGOs to loot CSR funds.

We also seek your advise on the matter.

Thanking you,

For Tarakeshwara Foundation

Sehdev Singh

Co-founder and Managing Trustee

Ph.7006546600, 6397357071, 8500091100

There is no proper record or transparent account of the amount spent on CSR activities to fight the pandemic from 2020 onwards.Moreover how many companies unregistered & Start Up ventures have spent money in CSR activities .No information is available.Dr.S.K.Pachauri IAS Retd

Perfect

And Thanks for sharing this knowledge

In a country where only 2-3% of the population pay taxes government is asking to do CSR expenditures?

It is nothing but a decoy for hiding the real & controversial change/ amendment at that time (Dilution of strict 11% limit on Managerial remuneration & increase in limit of political donation from 5% to 7.5% back then).

Otherwise there is nothing to analyse in this section.

Now what is left in this section —

“You pay 2% to NGO by cheque and they give you money back in cash CSR done.”

i.e. Just another way to loot listed company by their promotor directors.