INTRODUCTION

The Ministry of Corporate Affairs (MCA) vide its General Circular No. 12/2020 dated 30/03/2020, introduced the Companies Fresh Start Scheme, 2020 for one-time application of condonation of delay of filling the various documents, forms, returns, etc. with the MCA and granting of immunity from launching of any prosecution or proceedings for imposing penalty on account of delay associated with certain filings.

OBJECTIVE OF THE SCHEME

The Scheme has been launched with a view to:

- Incentivize compliance;

- Reduce non-compliance burden of various companies;

- Waiver of additional fees levied for late filings of documents;

- Provide an opportunity to ‘Inactive Companies’ to obtain the status of ‘Dormant Company’.

PERIOD / CURRENCY OF THE SCHEME AND FORMS INCLUDED

The Scheme has been made applicable for a period starting from April 01, 2020 to September 30, 2020.

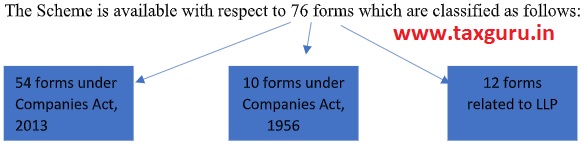

The Scheme is available with respect to 76 forms which are classified as follows:

APPLICABILITY OF THE SCHEME

Under this Scheme, any ‘Defaulting Company’ is permitted to file belated documents which were due for filing on any given date in accordance with provisions of the Scheme.

Here, Defaulting Company shall mean a company defined under Companies Act, 2013, and which has made a default in filing of any of the documents, statements and the returns etc including annual statutory documents on the MCA-21 registry.

PLOT OF THE SCHEME

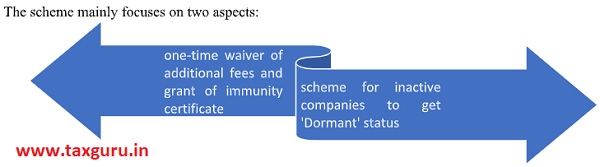

The scheme mainly focuses on two aspects:

Aspect 1 – One-time waiver of additional fees and grant of immunity certificate

In this, the companies shall be allowed a one-time waiver of additional fees to be levied on filings of any pending documents, statements or returns. Only normal fees shall be payable for completing the pending compliance which shall be as per the provision of Section 403 of the Companies Act, 2013. Also, the companies shall be given an immunity certificate that shall grant an immunity to the company in respect of the launching of any prosecution or proceedings for imposing penalty on account of delay associated with such filings.

Note: Immunity under this scheme shall be granted only in respect of delayed filings of any documents, statements or returns but not against any substantive violation of law.

Form for immunity certificate – The company shall file an application under FORM CFSS-2020 for grant of immunity certificate after the closure of the scheme but not later than six months from the closure of the scheme i.e. from October 01, 2020 to March 31, 2021.

Effect of Immunity – The Designated Authority (ROC) shall withdraw the prosecutions before any courts and proceedings pending before Adjudicating Authority in respect of which the immunity has been granted by the Designated Authority (ROC).

Aspect 2 – Scheme for Inactive Companies

Inactive Company means a company which has not been carrying on any business or operation, or has not made any significant accounting transaction during the last two financial years, or has not filed financial statements and annual returns during the last two financial years.

Under this Scheme, Inactive companies, along with filing form CFSS-2020, are given two options i.e.

NON-APPLICABILITY OF THE SCHEME

The Scheme shall not apply to :

- Companies against which action for final notice of striking off the name u/s 248 of Companies Act, 2013 has already been initiated by the Designated Authority (ROC);

- Where any application has already been filed by the companies for action of striking off the name of the company from the register of companies;

- Companies which have already been amalgamated under the scheme of arrangement or compromise under Companies Act, 2013;

- Where application has already been filed for obtaining Dormant status under Section 455 of the Companies Act, 2013;

- Vanishing Companies; (A Company shall be categorized as Vanishing Company if it falls under any of the criteria: a) a company fails to file returns with ROC for a period of two years; b) a listed company fails to file returns with the stock exchange for a period of two years; c) the company does not maintain its registered office at address registered with ROC; d) the company’s directors are not traceable.)

- Where any increase in authorised share capital is involved i.e. Form SH-7;

- Any charge related documents i.e. CHG-1, CHG-4, CHG-8, CHG-9.

CONCLUDING REMARKS

The Designated Authority (ROC) shall take necessary action against those companies which did not avail the Scheme and are still defaulting in the filing of these documents even after the closure of the Scheme.

CREDIT SOURCE

1. MCA General Circular – https://taxguru.in/company-law/companies-fresh-start-scheme-2020.html

2. Webinar by ICSI on CFSS, 2020 – https://youtu.be/In0YCAOLZEk

Author Bio