INTRODUCTION:

Buyback can be defined as repurchasing of its own securities by the company. The main objective of buyback by companies is to make use of the idle cash lying with them and ultimately improving the earning per share (EPS).

Some of the reasons why a company should consider buyback are

1. It helps the promoters to consolidate their shares.

2. Buyback is a tax-effective means of rewarding the shareholders.

3. It improves the earning per share of the company.

4. It also gives confidence to the shareholders at the time of falling prices.

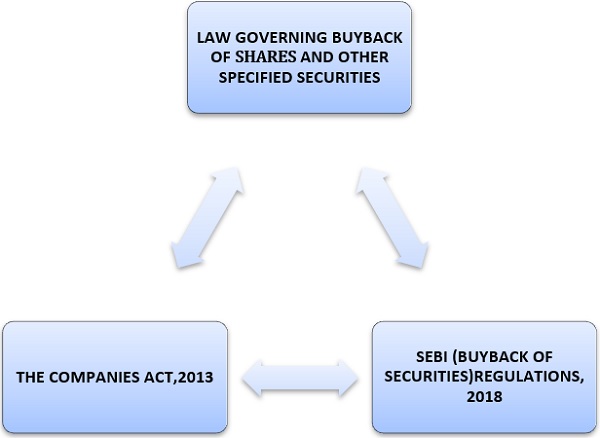

However, the SEBI (Buyback of securities)regulations shall be applicable only to buyback of shares or other specified securities of a listed company in accordance with the applicable provisions of the Companies Act.

This article contains a brief summary of buyback under the Companies Act, 2013–

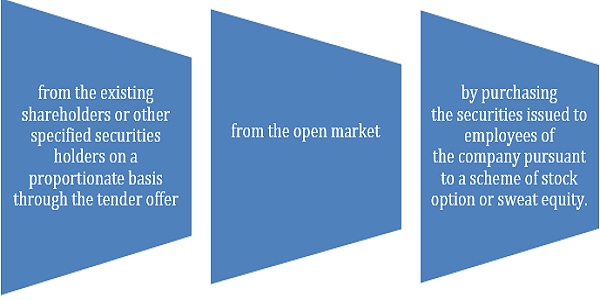

METHODS OF BUYBACK:

MODES OF BUYBACK-

A company can buyback its shares and other specified securities out of-

> its free reserves;

> the securities premium account; or

> the proceeds of the issue of any shares or other specified securities

Provided that no buy-back of any kind of shares or other specified securities shall be made out of the proceeds of an earlier issue of the same kind of shares or same kind of other specified securities.

FORMALITIES TO BE FOLLOWED FOR BUYBACK-

There are some pre and post buyback formalities which are required to be followed in buyback. Such procedure is dicussed in details below-

PRE-BUYBACK FORMALITIES-

1. the articles of the company must authorise such buyback. However, if articles are silent then it can be amended by passing SR in GM.

2. A Special Resolution must be passed at a company authorisisng the buyback.

3. A company is allowed to buyback upto 25% of paid up equity share capital and free reserves in a financial year.

4. the ratio of the aggregate of secured and unsecured debts owed by the company after buy-back is not more than twice the paid-up capital and its free reserves. In simple words, the debt equity ratio of the company can be maximum 2:1 after such buyback.

5. all the shares or other specified securities for buy-back are fully paid-up

6. a declaration of solvency is required to filed with Registar of Companies (ROC) signed by at least two Directors of the company, one of whom shall be the managing director, if any, in form SH-9.

7. An affidavit is required to be filed stating that the Board of Directors of the company has made a full inquiry into the affairs of the company as a result of which they have formed an opinion that it is capable of meeting its liabilities and will not be rendered insolvent within a period of one year from the date of declaration adopted by the Board.

8. The company which has been authorized by a special resolution shall, before the buy-back of shares, file with the Registrar of Companies a letter of offer in Form No. SH.8, along with the fee dated and signed on behalf of the Board of directors of the company by not less than two directors of the company, one of whom shall be the managing director, where there is one.

POST BUYBACK FORMALITIES:

1. The company shall maintain a register of buyback in Form SH-10 containing the following details-

♦ Details of shares and securities so bought

♦ The consideration paid for the shares or securities bought back

♦ The date of cancellation of shares or securities

♦ the date of extinguishing and physically destroying the shares or securities

2. The company, after the completion of the buy-back shall file with the Registrar a return in the Form No. SH.11 along with the fee.

3. a certificate in Form No. SH.15 is also required to be annexed to the return signed by two directors of the company including the managing director, if any, certifying that the buy-back of securities has been made in compliance with the provisions of the Act and the rules made thereunder.

4. Where a company buys back its own shares or other specified securities, it shall extinguish and physically destroy the shares or securities so bought back within seven days of the last date of completion of buy-back.

5. After completion of buyback, company shall not make any furthur issue of the same kind of shares and securities including allotment of new shares within a period of six monrths of buyback except by way of a bonus issue, conversion of warrants, stock option schemes, sweat equity or conversion of preference shares or debentures into equity shares.

PROCEDURE OF BUY BACK IN OPEN OFFER

1. After the offer letter is submiited to ROC in form SH-8, now within 20 days offer letter must be dispatched to all equity shareholders.

2. Offer period will be minimum 15 days and maximum 30 days from the date of dispatch of offer letter. However, offer period can be less than 15 days if agreed by all the members.

3. During the offer period shareholders interested in buyback will surrender their shares.

4. After the offer period closes the company shall comply with the following-

OTHER IMPORATANT POINTS TO BE CONSIDERED IN BUYBACK-

1. In case buyback is upto 10% of paid-up equity share capital and free reserves , buyback can be done by passing board resolution in place of special resolution.

2. The notice of the meeting at which the special resolution is proposed to be shall be accompanied by an explanatory statement stating all the facts in pursuant to buyback as per Rule 17 (Companies Share Capital and Debentures).

3. the company shall not withdraw the offer once it has announced the offer to the shareholders;

4. the company shall not utilize any money borrowed from banks or financial institutions for the purpose of buying back its shares

5. The entries in the register maintained in Form SH-10 shall be authenticated and kept in custody by the secretary of the company or by any other person authorized by the Board for the purpose.

6. Where a company purchases its own shares out of free reserves or securities premium account, a sum equal to the nominal value of the shares so purchased shall be transferred to the capital redemption reserve account and details of such transfer shall be disclosed in the balance sheet.

7. No company shall, directly or indirectly, purchase its own shares or other specified securities in case such company has not complied with the provisions of sections 92, 123, 127 and section 129.

8. “specified securities” includes employees’ stock option or other securities as may be notified by the Central Government from time to time.

9. “free reserves” includes securities premium account.

Author Bio