Limited Liability Partnership (LLP) is a body corporate having legal entity and can hold property in its own name different from its partners. It is a hybrid of partnership and company form of organization. LLP has limited liability and perpetual succession.

Just like a company consists of members and directors, LLP consists of partners and designated partners respectively. There must be minimum two partners and there is no limit on maximum partners. Also, every LLP shall have minimum two designated partners to fulfill statutory obligations under LLP Act.

Illustrative list of Compliance Requirement under the LLP Act, 2008 and rules made there under:

1. CONTRIBUTION BY PARTNERS:

SECTION 32 READ WITH SUB-RULE (1) AND (2) OF RULE 23:

2. FINANCIAL DISCLOSURES:

SECTION 34 READ WITH SUB RULE (3) OF RULE 24:

> The LLP shall maintain its books of account relating to its affairs for each year of its existence on cash basis or accrual basis and according to double entry system of accounting.

> The LLP shall maintain its books of account at its registered office for a period of eight years.

3. STATEMENT OF ACCOUNT AND SOLVENCY:

> As per Sub Rule 10 of Rule 24 a person who is a qualified Chartered Accountant shall be appointed as the auditor of the LLP for each Financial Year for auditing its accounts.

> As per Sub Rule 11 of Rule 24, designated partners may appoint an auditor or auditors-At any time for the first financial year but before but before the end of the financial year.

-

- At least 30 days prior to the end of each financial year

- To fill a casual vacancy in the office of auditor, including in the case when the turnover or contribution of a LLP exceeds the limit.

- To fill up the vacancy caused by removal of an auditor.

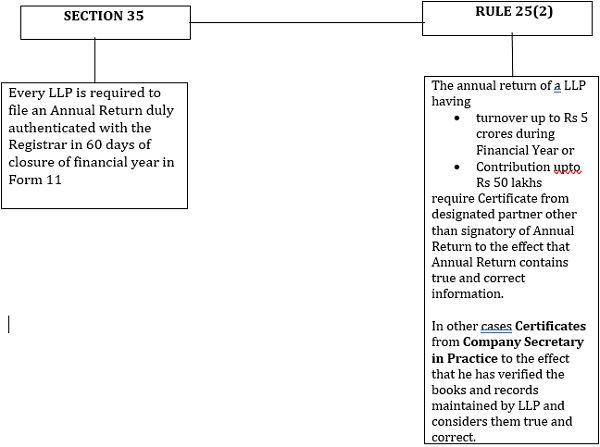

4. ANNUAL RETURN:

5. PRESERVATION OF RECORDS:

Author Bio