Abstract: Significant Beneficial Owners (SBO) regulations were introduced in India to promote corporate transparency and uncover ultimate beneficiaries with significant control over companies. This article explains SBO’s concept, FATF’s global ownership rules, and practical challenges in compliance.

Background

– The Concept of Significant Beneficial Owners (‘SBO’) was introduced in India with the following objectives:

To identifying SBOs to uncover the ultimate beneficiaries or individuals who have significant control over a company but may not be directly listed as shareholders or directors. By identifying SBOs, the government aims to promote transparency in corporate ownership and prevent potential misconduct.

– The FATF’s recommendation 24 introduces tougher global beneficial ownership rules to prevent criminals from concealing illicit activities and dirty money through secret corporate structures. These changes aim to close loopholes and regulatory weaknesses that have allowed fake companies to facilitate criminal activity and tax evasion.

– The new rules will enable investigators to swiftly and easily identify the true ‘beneficial’ owners of companies, thereby aiding in the prevention and combat of financial crime, corruption, and tax evasion while supporting sustainable economic growth. As a member of FATF countries, India has taken proactive measures to address potential risks related to money laundering activities during assessments conducted by FATF and the Asian/Pacific Group on Money Laundering, opting for Significant Beneficial Owner (SBO) provisions within the country.

Introduction of the concept of SBO in India involved the following steps:

- Prior to the Companies (Amendment) Act, 2017, the Companies Act, 2013 (referred to as ‘the Act’) included section 90, which allowed the Central Government to appoint one or more competent individuals to investigate and report on beneficial ownership concerning any share if deemed necessary.

- The Companies (Amendment) Act, 2017, which became effective on 13th June 2018, replaced section 90 with new provisions and introduced the Companies (Significant Beneficial Owners) Rules, 2018 (referred to as ‘SBO Rules’). These new rules required individuals holding significant beneficial ownership in a company to disclose their interests.

- However, due to several practical challenges in implementing the SBO Rules, the Ministry of Corporate Affairs (MCA) made further amendments to these rules through a notification dated 8th February 2019, known as the Companies (Significant Beneficial Owners) Amendment Rules, 2019 (‘the Rules’).

Glossary Section:

Significant Beneficial Owners

As per the section 2(1)(h) of the Act, SBO means an individual, holding in the reporting company, either alone or together with one or more persons or trust, possesses one or more of the following rights or entitlements in such reporting company, namely;

i) 10% or more shares, either indirectly or together with any direct holdings; or

ii) 10% or more voting rights in shares, either indirectly or together with any direct holdings; or

iii) Right to 10% or more distributable profits, either indirectly or together with any direct holdings; or

iv) Right to significantly influence or control decisions in reporting company.

“Member”, in relation to a company, means—

(i) the subscriber to the memorandum of the company,

(ii) every other person who agrees in writing to become a member of the company, or

(iii) every person holding shares of the company and whose name is entered as a beneficial owner in the records of a depository;

Reporting Company means a company incorporated under the Act, required to comply with the requirements of section 90 of the Act.

Majority stake means

(i) holding more than one-half of the equity share capital in the body corporate; or

(ii) holding more than one-half of the voting rights in the body corporate; or

(iii) having the right to receive or participate in more than one-half of the distributable dividend or any other distribution by the body corporate;

Intermediate company/Ultimate holding company means a body corporate, whether incorporated or registered in India or abroad, with the exception of a limited liability partnership.

Significant influence means the power to participate, directly or indirectly, in the financial and operating policy decisions of the reporting company but is not control or joint control of those policies.

In the context of construction of the section 90 of the Act unambiguously stipulates that an individual shall be deemed a SBO if they hold Indirect rights or entitlements or taken together with their direct holdings in the reporting company, as per the specifications detailed in sub-clauses (i), (ii), or (iii) of the SBO definition.

The SBO rules are applicable to both foreign citizens and Indian citizens. These rules encompass all types of companies, whether they are listed or unlisted.

Therefore, we are currently examining the provisions of the Significant Beneficial Owner definition in the context of both direct and indirect holdings, using flowcharts for illustration.

Direct Holding:

An individual is said to have direct holding when he satisfies any of the following criteria:

i) He is the registered owner of shares; or

ii) He is not registered owner, but holds or acquires beneficial interest in the share of the company and has made a declaration in Form MGT-5.

Illustration: 1 Regardless of the percentage, Mr. A’s shareholding would be classified as a direct holding.

Illustration: 2 In this situation, Mr. A’s shareholding would be deemed as a direct holding when assessing his indirect shareholding portion.

Indirect Holdings: An individual is considered to hold a right or entitlement indirectly in the reporting company, if he satisfies any of the following criteria, in respect of a member of the reporting company, namely:

Case 1: Where intermediary company which is a member of the reporting company is a body corporate

- If Individual holds majority stake in the intermediate company

The need to verify this scenario arises only when an individual holds more than a majority stake in the intermediate company. In this scenario, we take the proportionate of the stake held by member in the reporting company.

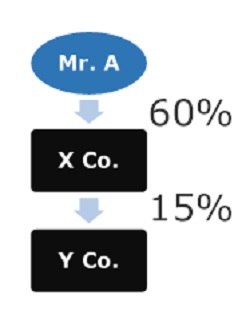

Illustration: 3 The proportionate shareholding of Mr. A amounts to 9% in Y Co. i.e 60%*15% which is below 10%. Accordingly, Mr. A is not considered SBO

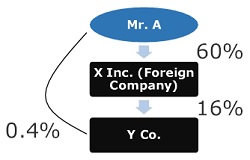

Illustration 4: Mr. A’s shareholding in Y Co. is proportionately calculated at 9.6%, derived from 60% of 16% combined with his direct holding of 0.4%, totaling 10%.

As per the provisions of the section 90 of the Act, Y Co. is required to report Mr. A as a SBO.

Illustration 5: In this scenario, Mr. A does not hold majority stake in the intermediary company. Hence, it is not required for the reporting company i.e. Y Co. to identify and report as SBO.

Moreover, in this situation, there typically cannot be more than two SBOs, as the requirement mandates that the Individual must hold a majority stake in the member of the reporting company unless other situation occurs.

- If Individual holds majority stake in the ultimate holding company in a multilayer structure:

The need to verify this scenario arises only when an individual holds more than a majority stake in the ultimate holding company which has more than one subsidiary companies, provided that restriction on number of layers given under section 186 of the Act is to be complied with. The ultimate holding company refers to the one positioned at the top of the corporate structure. In this scenario, we take the proportionate of the stake held by ultimate holding company in the reporting company via its number of subsidiaries.

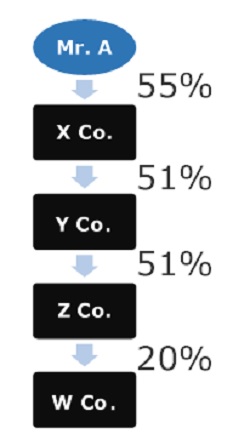

Illustration 6: In this scenario, Mr. A holds majority stake in the ultimate holding company i.e. X Co. and all the intermediate companies hold 51% or more. In this case, his proportionate share in W Co. Will be 11% which meets the criteria for identification and reporting of SBO.

In case, any of the intermediary company fails to holds majority stake then requirement for identification and reporting of SBO is not applicable.

Illustration 7: In this scenario, Mr. A holds majority stake in the ultimate holding company i.e. Mr. A, his propionate share in W Co. being 8.25% which taken together with holding of trust will be 13.25% meeting the criteria for identification and reporting of SBO.

Illustration 7: In this scenario, Mr. A holds majority stake in the ultimate holding company i.e. X Co., and all the intermediate companies hold 51% or more. In this case, his propionate share in W Co. becoming 2.75% which taken together with holding of trust and Mr. B will be 12.75% meeting the criteria for identification and reporting of SBO. , W Co. is obligated to report Mr. A & B as SBO.

Mr. A and Mr. B acting with common intent or purpose to exercise rights or entitlements over a reporting company.

Nevertheless, establishing the relationship between Mr. A and Mr. B, with the aim of identifying a common intent or purpose, proves to be challenging. If the company fails to recognize the connection between Mr. A and Mr. B, it may neglect its responsibility to file the required form.

Illustration 8: In this scenario, Mr. A holds majority stake in X Inc., which is not being an ultimate holding company and all the intermediary companies don’t hold majority stake. Even though his proportionate share meeting the criteria for identification and reporting of SBO. However, it is noticed that upper and intermediary layers not meeting the criteria of being ultimate holding and subsidiary companies. Hence, W Co. is not obligated to report Mr. A as report SBO.

Illustration 9:In this scenario, Mr. A holds majority stake in the ultimate holding company i.e. X Co., and all the intermediary companies hold majority stake. His proportionate share in W Inc. will be 11% which meeting the criteria for identification and reporting of SBO.

However, it is practically not possible to report about SBO as the reporting company being foreign based which does not have branch in India and as per the provisions of prescribed section reporting company is that one which is incorporated in India.

Illustration 10: In this scenario, Mr. A holds majority stake in the ultimate holding company i.e. X Co. His proportionate share in W Inc. will be 11% which meeting the criteria for identification and reporting of SBO.

Nevertheless, practically, it may not be feasible to identify the SBO on a daily basis, especially considering the request changes in the shareholding structure of the listed entity. Reporting companies face the challenge of keeping up with and reporting these changes frequently.

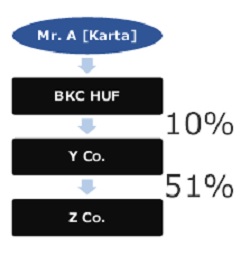

Case 2: Where the member of the reporting company is a Hindu Undivided Family (‘HUF’) and Karta is always an Individual.

The need to verify this scenario arises only when HUF is a member of the reporting company. The calculation of holdings amounting to 10% or more is determined by considering both the holding of the HUF and the direct holding of the Karta in the reporting company.

Illustration 11: In this scenario, Mr. A, Karta of BKC HUF meeting the criteria for identification and reporting of SBO. Therefore, Z Co. is required to report Mr. A as SBO.

Illustration 12: In this scenario, Mr. A, Karta of BKC HUF meeting the criteria for identification and reporting of SBO. Therefore, Z Co. is required to report Mr. A as SBO.

Illustration 13: In this scenario, obligation arises on Y Co. to identify and report Mr. A as SBO. Z Co. will report through filing the form BEN-2 under the category of declaration of holding reporting company.

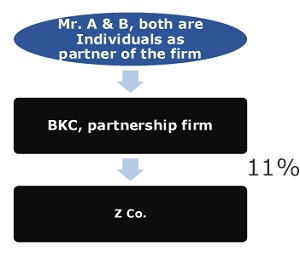

Case 3: Where the member of the reporting company is a partnership entity (through itself or a partner)

- Individual is the partner:

The need to verify this scenario arises only when individual is the partner of partnership firm.

Illustration 14: In this scenario, Mr. A & B would be considered as SBO for reporting by Z Co.

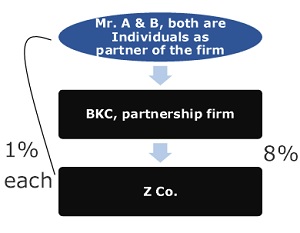

However, in the case of multiple individuals, SBO should be determined proportionately based on their respective contributions to the partnership firm.

Illustration 15: In this scenario, Mr. A & B would not be considered as SBO for reporting by Z Co., as they are not meeting the criteria defined for identification and reporting of SBO.

However, in the case of multiple individuals, SBO should be determined proportionately based on their respective contributions to the partnership firm.

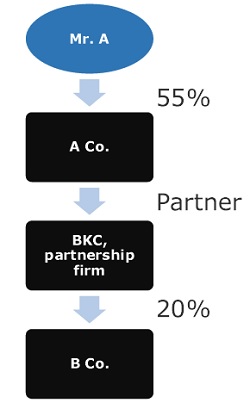

- Individual holds majority stake in the body corporate which is a partner of the partnership entity:

The need to verify this scenario arises only when individual holds majority stake in the body corporate which is a partner of the partnership entity which is also a member of the reporting company. In this scenario, we take the proportionate of the stake held by the firm in the reporting company.

Illustration 16: In this scenario, Mr. A would be considered as SBO for reporting by B Co., as he is holding 11% which is derived from 55%*20% i.e. 11%.

Practical problem-

The clarity of whether B Co. should identify SBO arises when the partnership firm consists of both individuals and body corporates, and the firm holds 10% or more stake in the reporting company. According to a literal interpretation, if a body corporate is a partner in the firm, and an individual member of that body corporate holds a majority stake, then this case must be applied. Otherwise, if the individual does not hold a majority stake, the analysis should be limited to the partnership firm.

Individual holds majority stake in the ultimate holding company of the body corporate which is a partner of the partnership entity:

The need to verify this scenario arises only when individual holds majority stake in the ultimate holding company of the body corporate which is a partner of the partnership entity which is also a member of the reporting company. In this scenario, we take the proportionate of the stake held by the firm in the reporting company.

Illustration 17: In this scenario, Mr. A would be considered as SBO for reporting by B Co., as he is holding 11% which is derived from 55%*20%.

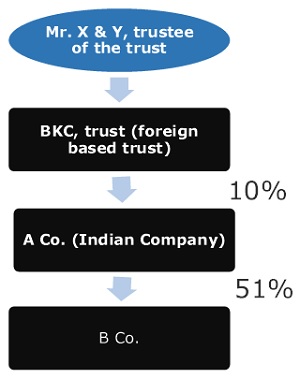

Case 4: Where the member of the reporting company is a trust (through trustee)

- Individual is a trustee in case of a discretionary trust or a charitable trust

The need to verify this scenario arises only when individual is a trustee of discretionary or a charitable trust which is a member of the reporting company.

Illustration 18: In this scenario, Mr. X & Y, trustees would be considered as SBO for reporting by B Co.

Illustration 19: In this scenario, Mr. X & Y, trustees would be considered as SBO for reporting by A Co.,

B Co. is not obligated to identify and report SBO since it does not have a majority shareholder in the form of a Body Corporate.

Illustration 20: In this scenario, Mr. X & Y, trustees would be considered as SBO for reporting by A Co.,

B Co. must submit the form BEN-2 and choose the radio button labeled “Declaration of holding reporting company.” The purpose of this reporting is to demonstrate the identification of the SBO already reported by its holding company.

Illustration 21: In this scenario, Mr. X & Y, trustees would not be considered as SBO for reporting by A Co.,

B Co. is also exempt from identifying and reporting the SBO since its holding company is not classified as a reporting company. In this scenario, the obligation to identify SBO does not apply.

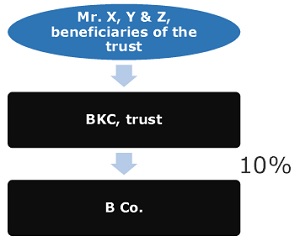

- Individual is a beneficiary in case of specific trust

The need to verify this scenario arises only when beneficiaries are there in the trust. The level of interest held by these beneficiaries is not taken into account during the SBO assessment.

Illustration 22: In this scenario, X, Y & Z being beneficiaries of the trust would be considered as SBO for reporting by B Co. As the beneficial interest of the beneficiaries would not be considered.

We can use for this case the above examples.

In this scenario, X, Y & Z being beneficiaries of the trust would be considered as SBO for reporting by B Co. As the beneficial interest of the beneficiaries would not be considered.

We can use for this case the above examples.

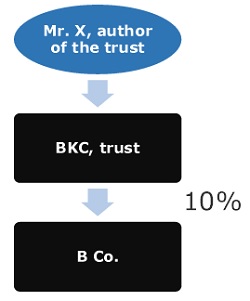

- Individual is the author or settler in case of revocable trust

The need to verify this scenario arises only when individual is an author or settler of the trust which is a member of the reporting company.

In this scenario, Mr. X being an author of the trust would be considered as SBO for reporting by B Co. As the beneficial interest of the beneficiaries would not be considered.

We can use for this case the above examples also.

Moreover, the individual in question does not possess any rights or entitlements in the reporting company indirectly through holdings, as discussed above in flowcharts, however, they could be classified as a SBO if they have the right or actually exert significant influence or control over the company, not solely based on direct holdings.

According to the explanation provided in section 2(1) of the Act, it is not mandatory for the reporting company to identify SBO solely based on a formal agreement or understanding with the individual. Even in the absence of such formal records, if the individual holds rights or entitlements, or exercising control or significant influence over the reporting company, they would still be considered SBO. Additionally, if multiple individuals act with common intent or purpose, they would be regarded as “persons acting together” and all of them would be deemed SBOs. We are explaining these provisions in the below flowcharts with the practical problems.

The question arises: if he does not possess any formal ownership, how can he be classified as SBO. He can establish his connection to B Co. through individuals holding prominent positions in the company, who are accustomed to acting upon his recommendations/advise. Such scenarios are often observed in closely held companies. Further, the Companies Act does not explicitly define financial and operating policy decisions.

Practical Problem;

When multiple companies are part of a corporate structure, identifying the person responsible for controlling the financial and operating policy decisions of a specific company becomes exceedingly challenging.

Reporting the relationship, whether formal or informal, with the relevant individual can be highly complicated. Additionally, the Companies Act does not provide a clear definition of financial and operating policy decisions.

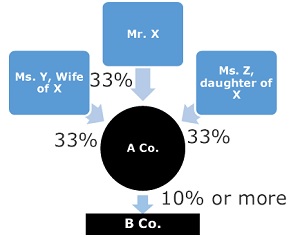

Illustration 24: Unless it can be established that Mr. X, Ms. Y & Ms. Z are not acting together, it shall be deemed that they are acting together and X, Y & Z shall be considered as SBO.

Illustration 25: Scenario 1: In the first scenario, a shareholder agreement exists between A and PQR Co., stating that Mr. A will have control over A Co. Further, Mr. A and A Co. has no stake over B Co. Despite this, Mr. A indirectly participates in the financial and operating policy decisions of B Co. Based on these circumstances, he would be deemed a SBO of B Co.

Scenario 2: In the second scenario, A Co. holds a substantial 99.99% stake in B Co., and Mr. A is not involved in any financial and operating policy decisions. Nevertheless, he would still be considered as the SBO of B Co. under these conditions.

Compliance requirements

|

S.No . |

Name of the form | Who to file | Timelines | Penal Consequences | Remarks |

| 1. | BEN-1 | SBO | (i) Within 90 days from applicability of the SBO rules.

(ii) File within 30 days in case of ownership is acquired subsequent to the applicability |

Imprisonment of up to 1 year and/or fine of INR 1,00,000 which may extend to INR 10,00,000 | MCA notification dated September 10, 2018 clarified that new form BEN-1 and timelines will be specified |

| 2 | BEN-2 | Reporting Company | File within 30 days from receipt of form BEN-1 with the registrar of Companies along with prescribed fees. |

(i) Penalty of INR 10,00,000 which may extend to INR 50,00,000 on the Company and every office in default.(ii) Additional, penalty of INR 1,000 per day in case of continuing default. |

|

| 3 | BEN-3 | Reporting Company | No time line prescribed | (i) If a company fails to maintain register in in BEN-3, then the penalty of INR 10,00,000 which may extend to INR 50,00,000 on the company and every officer in default is leviable.(ii) Additional, penalty of INR 1,000 per day in case of continuing default. |

Maintain register of SBO containing information about nature of interest and other prescribed information. |

Conclusion:

The primary responsibility for identifying and reporting SBOs lies with the reporting company, and this information must be submitted to the RoC within a stipulated time period. The identification of SBOs can become challenging, especially when numerous intermediary companies, including foreign entities, are involved in the corporate structure. Some companies may experience frequent changes in their SBOs, particularly in the case of listed entities. Additionally, establishing relationships between individuals acting informally as a group can pose difficulties during SBO checks.

Failure to comply with SBO disclosure requirements can lead to penalties, fines, or other legal consequences for both the company and the SBOs involved. Companies may need to reevaluate their ownership structures to ensure compliance with SBO regulations, which can lead to more straightforward and transparent ownership arrangements.

Disclaimer:

This is just a proposal for professional services. This is not an opinion. The information contained in this material is intended solely for your internal use. Any disclosure, copy or further distribution of this material or the contents thereof is strictly prohibited.

Author Bio

PQR LLP (Reporting LLP) has 2 Partners:

XYZ LTD hold 80% (Body Corporate)

Mr. L hold 20% (Individual)

XYZ LTD has 3 shareholders:

Mr. X hold 50% (individual),

Mr. A hold 1% (individual) &

ABC PVT LTD hold 49% (body corporate).

ABC PVT LTD has 2 shareholders:

Mr. X holding 99% (individual)&

Mr. M 20% (individual).

Except Mr. L all are related parties in some or the other way.

How will the provisions of LLP (SBO) Rules 2023 will be applicable in this case and what will be the percentage of beneficial interest that will be reported to the reporting LLP by XYZ LTD?

Good attempt