1. A Draft Valuers Bill, 2020 has been drafted to establish a National Institute of Valuers (NIV) on basis of recommendations by a Committee of Experts constituted by the Ministry of Corporate Affairs (MCA) to examine the need for an institutional framework to regulate and develop valuation as a profession.

2. The Committee of Expert (CoE) constituted by Govt. of India (GoI) vide order No. 12/9/2019-PI dated 30th August 2019, to prepare the report examining the need for an institutional framework for regulation and development of Valuation Professionals.

3. The Registered Valuer concept in India was the first time brought by the Companies Act, 2013 in formal manner. Though the valuer’s concept was in existence earlier, the profession per se was not regulated by any parliamentary rules and regulations.

4. The proposed law creates a new regulator – National Institute for Valuers, to promote the development of, and to regulate the profession of valuers and market for valuation services and to protect the interests of users of valuation services in India.

COMMITTEE OF EXPERTS’ RECOMMENDATION

1. The CoE has recommended enactment of an exclusive statute to provide for the establishment of the National Institute of Valuers (Institute / NIV) to protect the interests of users of valuation services in India and to promote the development of, and to regulate the profession of Valuers and market for valuation services. The Institute shall register and regulate Valuer Institutes, VPOs and Valuers.

2. Valuation should be developed as a discipline of knowledge such that Valuers are not only valuation professionals, but also the most valuable professionals.

3. For many practitioners of valuation, it is a part-time vocation, often as an extension of their primary profession, and moving ahead they should be full-time valuation practitioners just like doctors, CAs, etc.

4. Recommends centralized institutional framework for development and regulation of valuation profession in the Draft Valuers Bill, 2020 since Valuation profession is largely in the self-regulation mode today, except for 3000+ Valuers regulated under the Valuation Rules.

5. Protection of Valuers: Only the Institute should have authority to take action against a Valuer, after following due process. No court should take cognisance of any offence against a Valuer, save on a complaint made by the Institute or the Central Government.

6. Valuation Standards: The Institute should lay down valuation standards based on the recommendations of the Valuation Standards Committee. It shall be mandatory for Valuers to conduct valuation as per the valuation standards.

7. Presumption of bona fide: By definition, divergent views are possible in the field of valuation. If expressions of opinion on the value are lightly interdicted, it would be counterproductive to the objective of developing a vibrant market for the valuation services. Therefore, there should be a presumption of bona fide for the valuation conducted by a Valuer.

8. The framework should not be limited to valuations under the Companies Act and IBC, but should cover valuations under all other laws in a phased manner in due course.

VALUATION SERVICES

1. At present, the valuation practice of a Registered Valuer (RV) qualified under Insolvency and Bankruptcy Board of India (IBBI) pertain to mostly valuation services for requirements under the Companies Act, 2013 and that under Insolvency and Bankruptcy Code, 2016 and such RVs are regulated by the IBBI. However, valuation services required under several other acts, namely as mentioned hereunder, are being carried out by unregulated practitioners and the Draft Valuers Bill, 2020 aims at consolidating all such valuation services required under other acts to be carried out by the specified Registered Valuer (RV) and be regulated by the proposed new regulator – National Institute for Valuers (NIV).

2. “Valuation services” under the proposed law means the services relating to valuation of any asset or liability-

(a) which is required under the provisions of-

(i) the Banking Regulation Act, 1949 (10 of 1949),

(ii) the Securities Contacts (Regulation) Act, 1956 (42 of 1956),

(iii) the Wealth Tax Act, 1957 (27 of 1957),

(iv) the Income Tax Act, 1961 (43 of 1961),

(v) the Securities Exchange Board of India Act, 1992 (15 of 1992),

(vi) the Insurance Regulatory and Development Authority Act, 1999 (41 of 1999),

(vii) the Foreign Exchange Management Act, 1999 (42 of 1999),

(viii) the Securitisation and Reconstruction of Financial Assets and Enforcement of Securities Interest Act, 2002 (54 of 2002),

(ix) the Prevention of Money Laundering Act, 2002 (15 of 2003),

(x) the Limited Liability Partnership Act, 2008 (6 of 2009),

(xi) the Companies Act, 2013 (18 of 2013),

(xii) the Pension Funds Regulatory and Development Authority Act, 2013 (23 of 2013),

(xiii) the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015 (22 of 2015),

(xiv) the Insolvency and Bankruptcy Code, 2016 (31 of 2016), or

(xv) any other law, as may be prescribed.

(b) which arises from the needs of the market, as may be specified.

3. Understandably, this proposed act has covered 15 different acts for the purpose of valuation and on being notified in the Official Gazette, its scope of regulation and applicability shall have far reaching consequences over all types of Valuation services under such acts being carried out by only the qualified Registered Valuer as described under the proposed law over which the National Institute of Valuers (NIV) shall exercise regulation, inspection and exercise and recommend punishment, whenever required.

4. It is specified in the proposed law that Companies (Registered Valuers and Valuation) Rules, 2017 effectuated under Section 247 of the Companies Act, 2013 shall stand rescinded from such date appointed by the Central Government and related changes shall be made in the Companies Act, 2013 to bring it into effect.

OVERRIDING EFFECT OF THE PROPOSED BILL

On being passed in the Official Gazette, Valuers Act, 2020 shall have overriding effect on any other law in regard to any inconsistency existing between both the Acts.

VALUER

1. The “Valuer” means a valuer who is registered as such under section 50 and includes a ‘valuation entity’, ‘associate valuer, ‘fellow valuer’ and ‘honorary valuer. Section 48 classifies valuers in four classes of valuers, namely:

(a) valuation entities- An entity can also be registered as a Valuer if majority of its partners or directors are Valuers

(b) associate valuers- Shall be an associate valuer and on registration shall be entitled to prefix letters ‘AV’ to his name.

(c) fellow valuer- Who has been in practice for at least five years shall be entitled to prefix the letters ‘FV’ to his name.

(d) honorary valuer- On recognition of such extra-ordinary contribution to the valuation profession is entitled to use ‘HV’ to his name, but he shall not practice.

ASSET CLASSES

1. In the beginning, registration of Valuers should be available for three asset classes, such as land and building, plant and machinery and securities and financial assets.

2. Assets displaying similar characteristics will be grouped into closest class.

3. The National Institute of Valuers (NIV) shall be allowed to add / subtract an asset class as well as increase / decrease the scope of an asset class, with changing needs.

4. An individual can register as Valuer in all three classes, if he meet the eligibility criteria for all three classes.

REGISTRATION OF VALUERS

1. The registration of the valuers shall be asset class wise.

2. A valuer, who is registered under the Companies (Registered Valuers and Valuation) Rules, 2017 made under the Companies Act, 2013 (18 of 2013), as on the date of commencement of provisions of this Chapter, shall be deemed to be an associate valuer registered under this Act.

3. A person, who is eligible under the law and enrolled with a valuation professional organisation as a member, may make an application to the Institute for a certificate of registration as a valuer.

4. However, registration as valuer will not permit a person to start his practice as a valuer.

5. No person shall act as a valuer or hold out as a valuer except under, and in accordance with, a certificate of registration granted under this Act. A valuer shall not render valuation services except under, and in accordance with, the conditions of a certificate of practice granted under this Act.

6. The Bill recognizes four paths for becoming Valuer, two temporary and two permanent;

7. No person shall act as a valuer without having a certificate of registration.

8. A valuer shall not render valuation services without holding Certificate of Practice (COP)

9. A valuer shall not be eligible to hold a certificate of practice, while he is in the employment of any person.

10. A whole-time directorship of a company registered as valuer entity shall not be considered as employment.

11. For now, Clause 51 of the Bill do not forbid, per se, to hold more than one certificate of practice at a time. In other words, Practicing CS, CA and CMA may continue their existing profession while practicing as a Valuer. Therefore, the person may continue the existing profession while working as a value.

12. However, moving ahead full time practice is expected after market matures, Valuer may have to choose which profession to follow, one may not simultaneously have COPs of other professions such as CA, CS, CMA etc.

13. No age limit prescribed like Insolvency Professionals, one can practice till he is of sound mind.

14. Valuers Entity (VE)

A Partnership firm, LLP or a Company, other than a subsidiary, can be registered as VE, if (a) its primary objective is to provide valuation services. The objective shall be considered primary where at least 50% of revenue is derived from valuation services.

(b) not undergoing an insolvency resolution, liquidation or bankruptcy process;

(c) majority of its partners/directors are valuers having COP;

(d) none of its partners/directors, is a partner/director of another VE

(e) at least one of its partners/directors, is a valuer of the asset class for which entity is seeking registration.

(f) The partnership firm or company, and all its partners/directors, who are valuers, shall be jointly and severally liable.

(g) A partner/director shall not be liable where the acts of omission and commission were without his knowledge or he had exercised all due diligence to prevent the same.

TRANSITIONAL ARRANGEMENT

1. A valuer, who is registered under the Companies (Registered Valuers and Valuation) Rules, 2017, shall be deemed to be an associate valuer under this Act,

2. Valuer engaged in valuation services having qualification may seek registration within 3 years after clearing the exam and training.

3. Valuers engaged in valuation services and meeting eligibility norms under the valuation rules, except required qualifications may seek registration within 2 years.

4. Registered valuer organizations (RVO) recognized under the Valuation Rules shall become Valuation professional organization (VPO).

5. Principal Regulator IBBI has been discharging the function under the valuation rules, shall pass on the authority when the Institute (NIV) is established.

CONDUCT OF VALUATION

1. A valuer shall, while conducting a valuation or rendering valuation services, comply with the valuation standards as notified or modified by the Institute.

2. Until the valuation standards are notified or modified by the Institute, a valuer shall make valuations or render valuation services in accordance with –

(a) Internationally accepted valuation standards and guidelines; or

(b) Valuation standards and guidelines adopted by the valuation professional organisation of which he is a member. For Eg: A Chartered Accountant who is a Registered valuer may adhere to the ICAI Valuation Standards 2018 when preparing Valuation Reports.

3. A valuer shall conduct a valuation, render valuation services and prepare valuation reports in such form and manner as may be specified.

4. A valuer shall not outsource valuation services to another person, except to the extent and the manner, as may be specified. The expression “outsource” means the use of a third party to perform the services which have been sought by a client from the valuer. The services which are generally expected to be carried out by a valuer shall not be outsourced. The services which are generally not expected to be carried out by a valuer may be outsourced.

5. A valuer may seek the opinion or get valuation conducted by another valuer of an asset class, where the scope of valuation services includes a valuation of any asset or liability belonging to an asset class in respect of which he is not registered. He shall disclose the details of such opinion or valuation in his report and he and the other valuer, as the case may be, shall be jointly and severally responsible for such valuation.

6. Therefore, Valuer can get the opinion from the other valuer only when, that valuer is not dealing in same class of assets. Otherwise, the same may tantamount to outsourcing.

7. Where a valuer considers it necessary to get an opinion in relation to the rendition of valuation services, he may engage one or more experts for assistance, subject to making disclosures. An “expert” includes an engineer, a chartered accountant, a company secretary, a cost accountant and any other person who is authorised to issue a certificate in pursuance of any law for the time being in force, except a valuer registered under the provisions of this Act.

8. The valuer shall be deemed to be responsible for the opinion or valuation so received. However, the valuer shall not be deemed to be responsible if he proves that he had exercised due diligence.

9. A valuation report shall not carry a disclaimer or condition, which has potential to dilute the responsibility of the valuer under this Act or makes the valuation unsuitable for the purpose for which the valuation was conducted and the valuation report shall be admissible as expert evidence within the meaning of section 45 of the Evidence Act, 1872.

10. A valuer shall not conduct a valuation where he has any conflict of interest. Where a valuer comes to know of or discovers any conflict of interest while conducting a valuation, he shall immediately apprise the same to the stakeholders.

11. A valuer shall not charge a fee which is linked to the value of assets undervaluation or success of the relevant transaction.

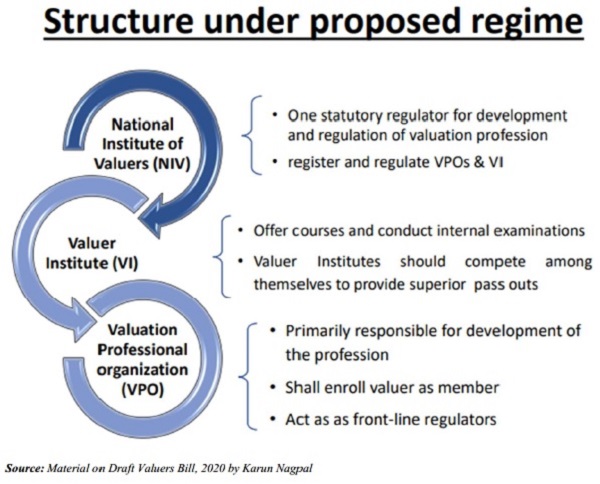

STRUCTURE OF REGULATORY MECHANISM

Source: Material on Draft Valuers Bill, 2020 by Karun Nagpal

1. NATIONAL INSTITUTE OF VALUERS, a bureaucratic organization having a duty of the Institute to promote the development of, and to regulate the profession of valuers and market for valuation services, and to protect the interests of users of valuation services, by such measures as it thinks fit. This shall be the supreme body to regulate Valuers, VI, VPO, framing rules and regulation, syllabus, and overall monitoring.

2. NIV shall be governed by a council with the chairperson, eight elected members and representative of MCA/MoF, RBI/SEBI/IBBI and three whole-time members of whom at least one shall be an administrative law member.

3. NIV will recognize universities/institutes / VPOs as valuer institutes on being satisfied with their credentials, and let them deliver courses strictly as per the prescribed norms and compete among themselves for excellence, and monitor and review their performance.

4. COMMITTEE OF VALUERS, a committee of NIV, consists of 20 valuer members to advise on any issue relating to the profession of valuers and market for valuation services.

Valuation Standards Committee, a committee of NIV, shall recommend:

(a) valuation standards; and

(b) valuation guidelines,

to be used by valuers for valuation services.

5. Central Government will notify the Valuation Standard in consultation with a valuation standard committee comprising of representatives of MCA, RBI, IRDA, MoF, CBDT, CBIC, IBBI, SEBI, and PFRDA. No representative of VPO or ICSI/ICAI/ICoAI.

6. VALUATION PROFESSIONAL ORGANISATION shall-

(a) Promote the professional development of its members;

(b) Promote professional and ethical conduct amongst its members

(c) Monitor the activities of its members to ensure compliance with this act, rules and regulations;

(d) Redress grievances of users against its members;

(e) Safeguard the rights, privileges and interests of its members; any

(f) Other functions as may be specified by the Institute (NIV)

7. VALUER INSTITUTE shall-

(a) deliver educational courses in accordance with the syllabus and in the manner of delivery, as may be specified;

(b) levy such fee from students undergoing educational courses as may be commensurate with its cost of delivery in a competitive market environment; and

(c) endeavour to arrange financial support for deserving students who cannot afford the full cost of the educational course.

8. Currently, RVOs are also eligible to conduct educational courses, but under the bill, they will need to get registered as VI separately

PROFESSIONAL FEES

1. The Committee is of the view that there should be no constraints on fees.

2. Any fixed fee is prone to two problems, being as follows:

- Fixed by the regulator may not be the market clearing price.

- The minimum fee has the tendency to be the maximum fee and the maximum fee has the tendency to be the minimum fee for the market participants.

3. No two valuations are equal or two valuers are equal.

4. Therefore, no fees prescribed in the bill, left open for market to decide.

VALUATION REPORT

1. The valuation report should be signed by an individual valuer, same as in case of audit report signed by CAs.

2. In case of entity structure, Valuation reports shall be signed by a partner/director, who is a valuer of the relevant asset class.

3. Valuation report should covers all material relevant matters with more detailed reason and analysis.

4. Report should not carry disclaimers, which has potential to dilute the responsibility of valuers.

5. NIV will determine the extent of disclosure to be made in the valuation report.

6. Valuation report shall be admissible as expert evidence within the meaning of section 45 of the Evidence Act, 1872.

OFFENCES AND PENALTIES:

1. Two Schedules are proposed for professional misconduct of Valuers.

2. The First Schedule deals with deemed professional misconducts which are not severe but which may lead to penalty extending to Rs 2 Lakh or 3 times the amount of loss – Being higher of the two.

3. The Second Schedule deals with deemed professional misconducts which are more severe and which may lead to penalty extending to Rs 10 Lakh or 3 times the amount of loss – Being higher of the two.

4. Criminal complaint can be lodged against valuer for misconducts listed in the Second Schedule of the proposed draft.

5. If any person contravenes any of the provisions of this Act or the rules or regulations made thereunder for which no penalty or punishment is provided in this Act, such person shall be punishable with fine which shall not be less than one lakh rupees but which may extend to two crore rupees.

6. Notwithstanding anything in the Code of Criminal Procedure, 1973, offences under this Act shall be tried by the Special Court established under Chapter XXVIII of the Companies Act, 2013.

7. No Court shall take cognizance of any offence punishable under this Act, save on a complaint made by the Institute or the Central Government or any person authorised by the Central Government in this behalf.

Disclaimer: The content of this document is for general information purpose only. The author shall not accept any liability for any decision taken based on the advice. You should carefully study the situation before taking any decision.

Author Bio

Very nicely explained. Most of the doubts were cleared.

KS CHIRANJEEVI, IBBI VALUER (P&M/C)