An inquiry by the Institute of Chartered Accountants of India (ICAI) Disciplinary Committee has found CA. Shrikant Yadav not guilty of professional misconduct. The charges, filed by the Deputy Registrar of Companies, alleged that Yadav was negligent in certifying Form DIR-12 for the appointment of a director, Shri Umapati, to M/s Skyline Innovation Technology India Private Limited. The department claimed Umapati failed to disclose his interest in four other entities on Form DIR-2, an attachment to Form DIR-12. The committee, however, concluded that the primary responsibility for the declaration of interest rests with the director, not the certifying professional. It noted that Yadav had exercised due diligence by obtaining confirmation via a WhatsApp message before certification. The committee also pointed out that Form DIR-2 had been left blank by the director, and no conclusive evidence was provided by the complainant to prove the existence of the undisclosed directorships. Therefore, the committee determined that Yadav was not grossly negligent and did not commit professional misconduct under Item (7) of Part I of the Second Schedule of the Chartered Accountants Act, 1949.

DISCIPLINARY COMMITTEE [BENCH — II (2024-2025)1

[Constituted under Section 21B of the Chartered Accountants Act, 1949]

Findings under Rule 18(17) and Rule 19(2) of the Chartered Accountants (Procedure of Investigations of Professional and Other Misconduct and Conduct of Cases) Rules, 2007

File No: PR/G280/2022-DD/195/2022/DC/1631/2022

In the matter of:

Smt. Kamna Sharma

Deputy-Registrar-of-Companies,

Office of the Registrar of Companies

……Complainant

-Versus-

CA. Shrikant Yadav

……Respondent

Members Present:

CA. Ranjeet Kumar Agarwal, Presiding Officer (in person)

Mrs. Rani S. Nair, IRS (Retd.), Government Nominee (Through VC) Shri Arun Kumar, lAS (Retd.), Government Nominee (in person) CA. Cotha S Srinivas, Member (in person)

DATE OF FINAL HEARING : 18th June, 2024

DATE OF DECISION TAKEN : 18th September, 2024

Parties Present:

Authorized Repiesentative of the Complainant Department: Shri. Gaurav, Deputy Registrar of Companies (Through VC)

Respondent: CA. Shrikant Yadav (Through VC)

Counsel for the (Respondent: CA. Vaibhav Goel (Through VC)

1. BACKGROUND OF THE CASE:

1.1 It was stated by the Complainant Department that it had come to the knowledge of Central Government that certain individuals viz., Directors / Shareholders I entities in `Mis Skyline Innovation Technology India Private Limited’ (hereinafter referred to as ‘Company’) had engaged dummy persons as subscribers to MOA and directors and registered the Company with ROC, Delhi & Haryana by using forged documents / falsified addresses / signatures. Further, Director Identification Number (DIN) was obtained by furnishing false / forged document.

1.2 The companies I individuals / entities directly or indirectly connected with the Company might be engaged in;illegal / suspicious activities viz, money laundering, tax evasion and non-compliance of various provisions of laws.

1.3 Certain professionals had connived with the Company / its directors / subscriber to MOA and individuals who were acting behind the Company and had incorporated the Company and were also assisting in running of these Companies for illegal / suspicious activities in violation of various laws and also certified various reports / e-forms filed with Ministry of Corporate Affairs on MCA-21 Portal with false information or by concealing the material facts / information to hide the real identity of persons behind the companies particularly at the time of incorporation by certifying professional.

2. CHARGES IN BRIEF:

2.1 The Company had filed Form DIR-2 (which is a consent to act as the director of the Company), as an attachment to Form D1R-12 in respect of appointment of Shri Umapati as its director, wherein the said Form DIR-12 had been certified by the Respondent, but the said director i.e., Shri Umapati had disclosed wrong information in respect of his interest in other companies / entities in Form D1R-2 which was attached to Form D1R-12. Thus, it was alleged that the Respondent was liable for action for concealing information from MCA and providing wrong information to MCA.

3. THE RELEVANT ISSUES DISCUSSED IN THE PRIMA FACIE OPINION DATED 25th AUGUST 2022 FORMULATED BY THE DIRECTOR (DISCIPLINE) IN THE MATTER IN BRIEF, ARE GIVEN BELOW:

3.1 The Complainant alleged that the Respondent had certified Form DIR-12 of the Company in respect of the appointment of one director, namely Shri Umapati. In this regard, it was alleged that though at the time of appointment and filing DIR-12, Shri Umapati was interested in four other entities, but the said interest was not disclosed in the alleged Form DIR-12 and also in Form DIR-2 which was attached to Form DIR-12. In this regard, firstly, on perusal of Form DIR-2 which is a consent to act as a director of Company’ and has been filed by the said director, it was noted that in Point no. 11 to the Form reads as under: –

No. of companies in which am .already a director and out of such companies the names of the companies in which I am a Managing Director, Chief Executive Officer, Whole time Director, Secretary, Chief Financial Officer, and Manager.

3.2 In respect of the above point, it was noted that the said director had not mentioned anything or provided any details / answer and left it blank. Further, on perusal of Form D1R-12, which was certified by the Respondent, it was noted that at Point no. 5(1)(xxi) of the said Form number of entities had been mentioned to be ZERO while disclosing the said director’s interest in other entities. Thus, it was noted that no specific details of said director’s interest in other entities were given in Form DIR-2. Even his interest had not been mentioned as Zero / NIL in Form DIR-2 by the said director and thus, was completely left blank. However, at Point 5(1)(xxi) of Form–D1R-12; in–response to said director’s interest in other entities, it mentioned that he had interest in ZERO entities. Thus, it was not ascertainable that in the absence of any specific information in Form DIR-2 regarding Shri Umapati’s interest in other entities, why and how the same could be assumed to be ZERO / NIL interest at the time of certifying and filing Form D1R-12.

3.3 Section 168(1) and 170(2) of the Companies Act 2013 and. Rule 15 and 18 of Companies (Appointment and Qualification of Directors) Rules, 2014 read as under:

“Section 168: Resignation of director

(1) A director may resign from his office by giving a notice in writing to the company and the Board shall on receipt of such notice take note of the same and the company shall intimate the Registrar in such manner, within such time and in such form as may be prescribed and shall also place the fact of such resignation in the report of directors laid in the immediately following general meeting by the company: –

Provided that a director may also forward a copy of his resignation along with detailed reasons for the resignation to the Registrar within thirty days of resignation in such manner as may be prescribed.” (emphasis added)

“Seciion 170: Register of directors and key managerial personnel and their shareholding.

(2) A return containing such particulars and documents as may be prescribed, of the directors and the key managerial personnel shall be filed with the Registrar wrthrrt thirty days from the appointment of every director and key managerial personnel, as the case may be, and within thirty days of any change taking place.” (emphasis added)

“15: Notice of resignation of director:

The company shall within thirty days from the date of receipt of notice of resignation from a director, intimate the Registrar in Form D1R- 12 and post the in for Mation on its website, if any.” (emphasis added)

“18: Return containing the particulars of directors and the key managerial personnel.

A return containing the particulars of appointment of director or key managerial personnel and changes therein, shall be filed with the Registrar in Form D1R-12 along with such fee as may be provided in the Companies (Registration Offices and Fees) Rules, 2014 within thirty days of such appointment or change, as the case may be.” (emphasis added)

3.4 From the above, it was noted that the Company is required to file Form DIR-12 with ROC / MCA in respect of appointment and resignation of director(s) of the Company. It was also noted that Rule 18 of Companies (Appointment and Qualification of Directors) Rules, 2014 also refers to the Companies (Registration Offices and Fees) Rules, 2014. In this regard, it was further noted that Rule 8(1) to (10) of Companies (Registration Offices and Fees) Rules, 2014 reads as under:3

“8. Authentication of documents:

(1) An electronic form shall be authenticated by authorized signatories using digital signature.

(2) Where there is any change in directors or secretaries, the form relating to appointment of such directors or secretaries has to be filed by a continuing director orithe secretary of the company.

(3) The authorized signatory and the professional, if any, who certify e-form shall be responsible for the correctness of the contents of e-form and correctness of the enclosures attached with the electronic form.

(4) Every person authorized for authentication of e-forms, documents or applications etc., which are required to be filed or delivered under the Act or rules made there under, shall obtain a digital signature certificate from the Certifying Authority for the purpose of such authentication and such certificate shall not be valid unless it is of class, 11 or Class HI specification under the Information Technology Act, 2000 (21 of 2000).

(5) The electronic forms required to be filed under the Act or the rules there under shall be authenticated on behalf of the company by the Managing Director or Director or Secretary of the Company or other key managerial personnel.

(6) Scanned image of documents shall be of original signed documents relevant to the e-forms or forms and the scanned document image shall not be left blank without bearing the act signature of authorized person.

(7) It shall be the sole responsibility of the person who is signing the form and professional who is certifying the form to ensure that all the required attachments relevant to the form have been attached completely and legibly as per provisions of the Act, and rules made thereunder to the forms or application or returns filed.

(8) The documents or form or application filed may contain a power of attorney issued to an Advocate or Chartered Accountant or Cost Accountant or Company Secretary who is in whole time practice and to any others person supported by Board resolution to make representation to the registering or approving authority ‘failing which director or key managerial personnel can make representation before such authority.

(9) Where any instance of filing document, application or return etc., containing a false or misleading information or omission of material fact, requiring action under section 448 or section 449 is observed, the person shall be liable under section-448 and 449 of the Act.

(10) Without prejudice to any other liability, in case of certification of any form, document, application or return under the Act , containing wrong or false or misleading information or omission of material fact or attachtents by the person, the Digital Signature Certificate shall be de-activated by the Central Government till a final decision is taken in this regard.” (Emphasis added)

3.5 Thus, according to afore-mentioned Rule 8(3) and 8(7) of Companies (Registration Offices and Fees) Rules, 2014, while it was the responsibility of the Respondent to ensure that all required attachments relevant to Form DIR-12 had been attached completely and legibly as per provisions of the Act, and Rules made there under to the said Form, it was clear that the Respondent was also responsible for the correctness of the contents of 6-form and correctness of the enclosures attached with the electronic Form. Also, the said Form DIR-2 which was attached to Form DIR-12 did not contain the complete information and thus, cannot be said to be complete in all respects. Further, the reporting done in respect of disclosure of interest of Shri Umapati in Form DIR-12 was also not supported by any specific document since Form DIR-2 was itself silent about the number of entities in which the said director had interests. Accordingly, it was viewed that the Respondent was negligent and did not exercise required due diligence while performing his professional duties and thus, the Respondent was prima fade GUILTY of Professional Misconduct falling within the meaning of Item (7) of Part-I of Second Schedule to the Chartered Accountants Act, 1949.

3.6 The Director (Discipline) in his Prima Facie Opinion dated 25th August 2022 opined that the Respondent was Prima Fade Guilty of Professional Misconduct falling within the meaning of Item (7) of Part I of the Second Schedule to the Chartered Accountants Act, ‘1949. The said Item of lice Schedule to the Act, states as under:

Item (7) of Part I of the Second Schedule:.

“A Chartered Accountant in practice shall be deemed to be guilty of professional misconduct if he:

X X X X

(7) does not exercise due diligence or is grossly negligent in the conduct of his professional duties.”

3.7 The Prima Facie Opinion formed by the Director (Discipline) was considered by the Disciplinary Committee in its meeting held on 19th September 2022. The Committee on consideration of the same, concurred with the reasons given against the charges and thus, agreed with the Prima Facie opinion of the Director (Discipline) that the Respondent is GUILTY of Professional Misconduct falling within the meaning of Item (7) of Part – I of the Second Schedule to the Chartered Accountants Act, 1949 and accordingly, decided to proceed further under Chapter V of the Chartered Accountants (Procedure of Investigations of Professional and Other Misconduct and Conduct of Cases) Rules, 2007.

4. DATE(S) OF WRITTEN SUBMISSIONS/PLEADINGS BY PARTIES:

4.1 The relevant details of the filing of documents in the instant case by the parties are given below:

| S. No. | Particulars | dated |

| 1. | Date of Complaint in Form ‘I’ filed by the Complainant | 15.03.2022 |

| 2. | Date of Written Statement filed by the Respondent | 18.06.2022 |

| 3. | Date of Rejoinder filed by the Complainant | 21.07.2022 |

| 4. | Date of Prima facie Opinion formed by Director (Discipline) | 25.08.2022 |

| 5. | Written Submissions filed by the Respondent after Prima Facie Opinion | 05.06.2023,

27.06.2024 |

| 6. | Written Submissions filed by the Complainant after Prima Facie Opinion | 17.09.2024 |

5. SUBMISSION OF THE RESPONDENT ON PRIMA FACIE OPINION:

5.1 The Committee noted that the Respondent in his submissions dated 5th June 2023 and 27th June 2024, in respnse to the Prima Facie Opinion, inter-alia, stated as under: –

a) Shri Umapati had not disclosed his interest in other Companies I entities in Form DIR-2 which was attached to Form DIR-12 as he was purportedly interested in four other entities. Thus, it was alleged that the Respondent has provided wrong information on Form DIR-12.

b) The following documents were verified by the Respondent while certifying D1R-12:

i. KYC Documents of the Director, Shri Umapati, such as PAN, Aadhar, Photo etc.

ii. Registered office documents such as NOC from landlord.

iii. Certified true copy of the resolution passed at the Meeting of the Board of Directors of the Company on 24th May 2021.

iv. Form DIR-2 dated 27th May 2021 whereby Shri Umapati consented to act as a Director of the Company.

C) The said Fuim DIR-2 is thus the consent of the individual given to the Company whereby he agrees to act as a director of the proposed company and is a mandatory attachment while filing e- Form DIR-12 on MCA Portal. The said statutory obligation to disclose correct and complete information in Form DIR-2 is cast upon him pursuant to the provisions of section 152(5) of the Companies Act, 2013 and Rule 8 of Companies (Appointment and Qualification of Directors) Rules, 2014. Form DIR-2 submitted by Shri Umapati, which was a mandatory attachment to Form DIR-12 was relied upon by the Respondent besides seeking information from the Officials of the company.

d) The Respondent had verified and certified the particulars of the Form (including attachment(s)) from the original/certified records maintained by the Company besides seeking information from the Company which was subject matter of e-form DIR-12.

e) Form DIR-2 did not contain any specific detail about the specific Interest of the Director in other entities as it was left blank by Shri Umapati meaning thereby that he had no interest to disclose under Point no.11 of the said DIR-2 Form.

f) The Complainant did not adduce any evidence on record to substantiate that Shri Umapati had interest in other entities and thus the allegations raised in the extant complaint have not been corroborated to prove them against the Respondent.

g) The error is procedural in nature.

h) Lapse did not result in any undue favour to the Company or to the Director involved. There is no ill motive on the part of the Respondent in certifying DIR-12.

I) The Respondent had obtained confirmation that the director is not a director in any other company before filing Form DIR-12; Relevant Extract of the communication through WhatsApp is attached along with certificate u/s 65B of the Indian Evidence Act.

j) During the course of hearing, the Complainant has accepted that no enquiry has been conducted by ROC with the company(ies) or the concerned director to ascertain whether the declaration made by him in Form DIR-2 (forming part of FORM DIR-12 as attachment) is correct or not.

k) The Respondent cannot be held guilty without any concrete evidence as the number of directorships appearing on MCA Website may be due to variety of reasons and it cannot be taken as sacrosanct.

I) The Respondent had no motive to suppress or provide false/incorrect information to the Complainant. There was no such situation where Respondent had any suspicion about the documents shared by the concerned director is false/incorrect or incomplete. On keeping the area blank as mentioned above, the Respondent had confirmed via WhatsApp and on receipt of confirmation, Form DIR-12 was filed.

6. SUBMISSION OF THE COMPLAINANT DEPARTMENT ON PRIMA FACIE OPINION:

6.1 The Complainant Department vide email dated 17th September 2024 provided the copy of the Inquiry Report dated 25th April 2022 which was shared with the Respondent via email on the same date.

7. BRIEF FACTS OF THE PROCEEDINGS:

7.1 The details of the hearing(s) fixed and held/adjourned in said matter are given as under: –

| S. No. | Particulars | Date(s) of meeting |

Status of hearing |

| 1. | 1st Hearing | 09.06.2023 | Part heard and Adjourned. |

| 2. | 2nd Hearing | 23.04.2024 | Adjourned due to paucity of time. |

| 3. | 3rd Hearing | 17.05.2024 | Part-Heard and Adjourned. |

| 4. | 4th Hearing | 18.06.2024 | Concluded and decision on the conduct of the Respondent reserved. |

| 5. | — | 18.09.2024 | Decision on the conduct of the Respondent taken. |

7.2 On the day of the first hearing held on 9th June 2023, the Committee noted that the Respondent was present through video conferencing mode. The Committee further noted that neither the Complainant was present, nor any intimation was received from his side, despite the notice/email being duly served upon her. The Respondent was administered on Oath. Thereafter, the Committee -enquired from the .Respondent as to whether he was aware-of the charges. On the same, the Respondent replied in the affirmative and pleaded Not Guilty to the charges leveled against him. Thereafter, looking into the fact that this was the first hearing, the Committee decided to adjourn the hearing to a future date. With this, the hearing in the matter was part heard and adjourned.

7.3 On the day of the second hearing held on 23rd April 2024, the Committee adjourned the hearing in the case due to paucity of time.

7.4 On the day of the third hearing held on 17th May 2024, the Committee noted that the Authorized representative of the Complainant Department and the Respondent along with his Counsel were present befoe it through video conferencing. The Committee further noted that subsequent to the last hearing held in the case on 9th June 2023 being the first hearing in the case, there had been a change in the composition of the Committee which was duly intimated to the Authorized Representative of the Complainant Department, the Respondent and -his -Counsel who were present before the Committee. Thereafter, the case was taken up for a hearing. On being asked by the Committee to substantiate their case, the authorized representative of the Complainant Department referred to the contents of Complaint made in Form ‘I’ against the Respondent.

Subsequently, the Counsel for the Respondent presented the Respondent’s line of defence, inter-alia, reiterating the written submissions made by him on the Prima Facie Opinion. On consideration of the submissions made by the authorized representative of the Complainant Department and the Counsel for the Respondent, the Committee posed certain questions to them which were responded by them. Thus, on consideration of the submissions and documents on record, the Committee directed the authorized representative of the Complainant Department to provide their submissions the following within next 02 Weeks with a copy to the Respondent to provide his comments thereon, if any: –

1. Response to the written submissions made by the Respondent on the Prima Facie Opinion.

The Committee also advised the Respondent if he wishes to make any further written submissions in the case, may do so, with a copy to the Complainant Department. With the above, the hearing in the case was part heard and adjourned.

7.5 On the day of the fourth hearing held on 18th June 2024, the Committee noted that the Authorized representative of the Complainant Department and the’ Respondent along with his Counsel was present before it through video conferencing. The Committee noted that in the last meeting, the Complainant, Department was asked to provide their response to the written submissions made by the Respondent on the Prima Facie Opinion. However, no response was received from them. During the present hearing in the case, the Committee asked the Counsel for the Respondent to make their final submissions to defend their case. The Counsel for the Respondent presented the Respondent’s line of defence, inter-alia, reiterating that with respect to certification of Form DI R-12, his scope was limited only to verification of the originals with the attachments and to ensure that the contents of the attachments match to the fields of the Form DIR-12. On consideration of the submissions made by the Counsel for the Respondent, the Committee posed certain questions to him which were responded to by him. Thus, on consideration of the submissions and documents on record, the Committee decided to conclude the hearing in the case with the direction to the Respondent to provide the following within next 07 days with a copy to the Complainant Department to provide their comments thereon, if any: –

1. To submit the copy of Management Representation Letter obtained for the purpose of Certifications of Form DIR-12.

Accordingly, the decision on the conduct of the Respondent was kept reserved by the Committee. With this, the hearing in the case was concluded and judgment / decision was reserved.

7.6 Thereafter, the Committee at its meeting held on 29th August 2024, noted that the Respondent–vide email dated 27th June 2024 provided his response. On consideration of the documents and submissions on record, the Committee advised the office to send a separate communication to the concerned ROC(s) with a copy to the office of DGCoA to provide a copy of the complete Investigation/Inquiry report so that the Committee can arrive at a logical conclusion in the said case. Accordingly, an email dated 9th September 2024 was sent to the Complainant Department. in response thereto, the Complainant Department vide email dated 17th September 2024 provided a copy of the inquiry report in the instant case which was also shared with the Respondent vide email dated 17th September 2024.

7.7 Thereafter, at its meeting held on 18th September 2024, the Committee based on the facts, documents and oral and written submissions on record, passed its judgment in the captioned case,

8. FINDINGS OF THE COMMITTEE:

8.1 The Committee noted that the conduct of the Respondent has been examined only with respect to the charge alleged against him as regards the certification of Form DIR-12 of the Company on 27th May 2021 in respect of the appointment of one director namely Shri Umapati wherein though at the time of appointment and filing Form DIR-12, Shri Umapati was interested in four other entities, but the said interest was not disclosed in the alleged Form DIR-12 and also in Form DIR-2 which was attached to Form DIR-12.

8.2 In this regard, the Committee noted as per the instruction Kit for filing Form DIR 12, the purpose of filing Form DIR 12 is as follows:

“Every company,-whether-new-or-existing,-.is-required.to_file.an_eForm for_ particulars of its directors and key managerial personnel of the company with the Registrar, within 30 days from the date of appointment/ resignation and -of any change taking place in their designations.

Further, Rule 8 of Companies (Appointment and qualification of Directors) Rules, 2014 provides as under:

“Every person who has been appointed to hold the office of a director shall on or before the appointment furnish to the company a consent in writing to act as such in Form No. DIR-2:

Provided that the company shall, within thirty days of the appointment of a director, file such consent with the Registrar in Form No. DIR-12 along with the fee as provided in in the Companies (Registration Offices and Fees) Rules, 2014.”

Accordingly, in the said case, the Respondent had certified the Form DIR 12 for the appointment of new director i.e. Shri Umapati in place of Shri Shalini Dev Sagar. The details of appointrrienticessation/certification of the Company filed vide Form DIR – 12 of Directors is as under: –

| S. No. | Name of Director | Appointment cessation | Date of consent given by new directors |

Date of Board Meeting approving cessation | Date of Certification of DIR -12 |

| 1. | Shri Urnapati, | Appointment | 27.05.2021 | — | 27.05.2021 |

| 1. . | Smt. Shalini Devi Sagar. |

Cessation | N.A. | 24.05.2021 | 27.05.2021 |

8.3 The Committee on perusal of Form DIR-2 which is a ‘consent to act as a director of Company’ and has been filedj by the said director and attached to Form DIR 12 noted that Point no. 11 to the Form reads as under

`No. of companies in which I am already a director and out of such companies the names of the companies in which I am a Managing Director, Chief Executive Officer, Whole time Director, Secretary, Chief Financial Officer, and Manager.’

8.4 In respect of the above point, the Committee noted that the said director did not mention anything or provided any details / answer and left it blank.

8.5 Further, on perusal of Form DIR-12 which- has been certified by the Respondent, the Committee noted that at Point no. 5(1)(xxi) of the said Form, number of entities have been mentioned to be ZERO while disclosing the said director’s interest in other entities.

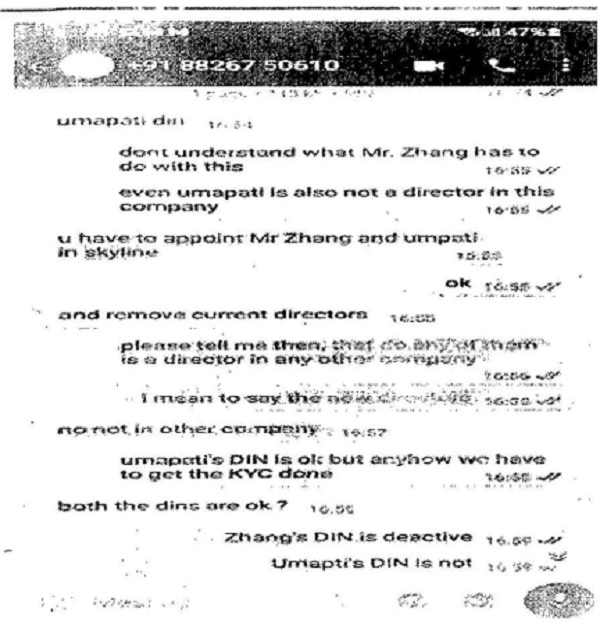

8.6 The Committe .also noted that the Respondent brought on record the copy of WhatsApp communication dated 19th May 2021 wherein he obtained confirmation as regard director’s interest in other Companies before certifying Form DIR-12 on 27th May 2021 along with the Certificate u/s 65B of the Indian Evidence Act. The relevant extract of the WhatsApp communication is given below:-

—

8.7 The Committee noted that as per MCA records, the Company under question was incorporated on 24th December 2019 with Mr. Kuldeep Nagpal and Mr. Zixia Zhang(foreign nationality) as the directors of the Company. The Committee also noted that Mr. Umapati was initially appointed as an additional director of the Company on 20th April 2020.Mr. Zixia Zhang and Mr. Umapati resigned from the position of the director and additional director respectively of the Company on 13th March 2021. The Respondent did not certify any of the Form(s) with respect to the incorporation or said change in the directorship of the Company. He certified the Form D1R 12 for the subsequent appointment of Shri Umapati as a new director of the Company with effect from 24th May 2021 which is the basis of the charge against the Respondent in the instant case. The Committee also noted that in the context of the instant Company, a disciplinary case against another Chartered Accountant who had certified Form INC-22(with respect to change in the registered office of the Company) on 13th March 2021 had also been filed by the Complainant Department which has been dealt separately.

8.8 The Committee further noted that the inquiry Report dated 25th April 2022 submitted by the Complainant Department, inter-alia, provided as under:

“As per records available on MCA Portal, it is observed that:-

- The subject company is not carrying on any business or operation since incorporation. The subject company has neither filed any financial statements and annual returns since incorporation nor obtained the dormant status pursuant to section 455 of the companies Act, 2013.

Presently the company is managed by following directors namely UMAPATI (DIN: 08738045) and Bishnu Des (DIN: 09182526). As per information available on MCA-21 portal the DIN of Shri Umapati is De-activated due to non-filing of 3KYC.

The physical verification of registered office of the subject company was carried but and the company’s office was not available at the registered addresS situated at SF-1 221 2nd Floor IT Complex MD Megapoils Village Tikari Sohna Road Gurgaon FIR 122001, Haryana.

ConcluSion:

….., it is proposed that this office may be allowed to strike-off the name of company by following due process u/s 248 of the Companies Act, 2013…..”

8.9 The Committee also noted that the said Inquiry Report did not have any observations against the Respondent. Also, the instant Company is still active since its incorporation i.e., from 24th December 2019 as per the record of the Ministry of Corporate Affairs and as on date, there are 2 Directors in the Company i.e., Mr. Umapati and Mr. Bishnu Das.

8.10 The Committee further noted that the Respondent while certifying the Form DIR-12 of the instant Company had given the following declaration: –

Certificate by practicing professional

I declare that I have been duly engaged for the purpose of certification of this form. It is hereby certified that I have gone through the provisions of the Companies Act, 2013 and Rules thereunder for the subject matter of this form and matters incidental thereto and I have verified the above particulars (including attachment(s)) from the original/certified records maintained by the Company/applicant which is subject matter of this form and found them to be true, correct and complete and no information material to this form has been suppressed. I further certify that:

- The Said records have been properly prepared, signed by the required officers of the Company and maintained as per the relevant provisions of the Companies Act, 20113 and were found to be in order;

- All the required attachments have been completely and legibly attached to this form,

- It is understood that I shall be liable for action under Section 448 of The Companies Act, 2013 for wrong certification, if any found al any utaga.

8.11 The Committee was of the view that filling up of Form DIR 2 and ensuring the correctness of the contents of the same is the sole responsibility of the Director of the Company. The role of the Respondent as a certifying professional for Form D1R 12 to which DIR 2 is attached cannot be stretched to the point that the onus of verifying each and every detail as contained in attachments/declarations of Director be fastened on him. Thus, the primary responsibility on declaration of interest in other entities in Form DIR 12 rests with the Director concerned and in the instant case, the Respondent had exercised necessary due diligence by corroborating the contents ofIthe same with necessary documents/information while certifying the Form DIR-12.

8.12 Thus, looking into the facts and circumstances of the case, the Committee was of the view that no case of misconduct is made out against the Respondent and accordingly, decided to hold the Respondent Not Guilty of Professional Misconduct falling within the meaning of Item (7) of Part I of the Second Schedule to the Chartered Accountants Act 1949 in respect of the Charge alleged against him.

8.13 While arriving at its Findings, the Committee also observed that in the background of the instant case the Complainant Department informed that the Company was registered with ROC, NCT of Delhi & Haryana by engaging dummy persons as subscribers to MOA & Directors by furnishing forged documents with falsified addresses I signatures, Director Identification Number (DIN) to MCA. Further, certain professionals in connivance with such individuals/directors/subscriber to MOA assisted in incorporation and running of these Companies for illegal/suspicious activities in violation of various laws by certifying e-forms/various reports etc. on MCA portal with false information concealing the real identities of such individuals. However, no evidence of the involvement of the Respondent to that effect had been brought on record by the Complainant Department. The role of the Respondent was limited to certification of Form DIR -12 which has been examined by–the Committee. Further, the Committee noted that the Complainant Department during the course of hearing in its written submissions brought on record a copy of an Inquiry report dated 25th April 2022 submitted to the Regional Director, MCA proposing that the Complainant Department be allowed to strike-off the name of Company by following due process u/s 248 of the Companies Act, 2013. However, the instant Company is still active as per MCA records. In this regard, the Committee was of the view that in case the Complainant Department has any evidence to substantiate the violations as pointed out in the said Report against any Chartered Accountant, .they may consider filing a separate complaint with the Disciplinary irectorate of ICAI as the charge alleged against the Respondent in the instant case was limited to certification of Form DIR-12 in which the interest of the Director in other entities was not reflected, has been examined by the Committee.

9. CONCLUSION:

9.1 In view of the findings stated in above paras, vis-à-vis material on record, the Committee gives its charge wise findings as under: –

| Charges (as per PFO) | Findings | Decision of the Committee |

| Para 2 as given above | Paras 8 to 8.12 as given above | NOT GUILTY – Item (7) of Part I of the Second Schedule |

9.2 In view of the above observations, considering the oral and written submissions of the parties and material on record, the Committee held the Respondent NOT GUILTY of Professional Misconduct falling within the meaning of Item (7) of Part-I of the Second Schedule to the Chartered Accountants Act, 1949.

ORDER:

10. Accordingly, in terms of Rule 19 (2) of the Chartered Accountants (Procedure of Investigations of Professional and Other Misconduct and Conduct of Cases) Rules, 2007, the Committee passes an Order for closure of this case against the Respondent.

Sd/-

(CA. RANJEET KUMAR AGARWAL)

PRESIDING OFFICER

Sd/-

(MRS. RANI S. NAIR, I.R.S. RETD.)

GOVERNMENT NOMINEE

Sd/-

(MR. ARUN KIJMAR, I.A.S., RETD.)

GOVERNMENT NOMINEE

Sd/ –

(CA. COTHA S SRINIVAS)

MEMBER