CS Rashmi H

Unlocking New Avenues for Corporate Restructuring under the Companies (Compromises, Arrangements and Amalgamations) Amendment Rules, 2025.

The fast-track merger has become the preferred method of merger due to its simplified and time-saving process. Unlike mergers or amalgamations under Sections 230–232 of the Companies Act, 2013, fast-track mergers receive quicker approval, as they are processed under Section 233 through the Regional Director with limited questionnaires.

Section 469 of the Companies Act, 2013 empowers the Central Government to frame rules on matters covered under the Act. Exercising this authority, the government introduced the Companies (Compromises, Arrangements and Amalgamations) Amendment Rules, 2025, which came into effect on 4th September 2025. This amendment modifies the earlier Companies (Compromises, Arrangements and Amalgamations) Rules, 2016 and significantly broadens the categories of companies eligible for a fast-track merger under Section 233. These rules aims to promote faster approvals, unlock synergy benefits, and reduce compliance requirements for the transferor company.

Companies Eligible for Fast-Track Merger under Section 233 (Prior to 2025 Amendment):

As per Section 233 of the Companies Act, 2013 read with the Companies (Compromises, Arrangements and Amalgamations) Rules, 2016, fast-track mergers were previously permitted in the following cases:

1. Between two or more small companies; or

2. Between a holding company and its wholly-owned subsidiary; or

3. Between one or more start-up companies and one or more small companies; or

4. Between a foreign holding company (incorporated outside India) and its wholly-owned Indian subsidiary, subject to the following conditions:

a) Both the transferor and transferee companies must obtain approval from the Reserve Bank of India (RBI);

b) The transferee Indian company must comply with the provisions of Section 233;

c) A declaration must be submitted as per Rule 25A (4) of the 2017 CAA Rules, if the foreign company shares a land border with India.

Expanded Scope under Amendment Rules, 2025:

The Companies (Compromises, Arrangements and Amalgamations) Amendment Rules, 2025 have widened the categories of companies eligible for a fast-track merger. The following additional types of mergers and amalgamations are now permitted:

1. Between two or more unlisted companies (excluding Section 8 companies), provided that:

a. Neither companies outstanding loans, debentures, or deposits exceeding 200 crore; and

b. Neither companies have defaulted in the repayment of such loan, debenture ot deposit.

2. Between a listed or unlisted Holding Company and its listed or unlisted Subsidiary Company, provided that:

a. The Transferor Company (or companies) is not listed on a stock exchange.

3. Between one or more subsidiary companies of a holding company and one or more other subsidiaries of the same holding company, provided that:

a. The transferor company (or companies) are not listed on a stock exchange.

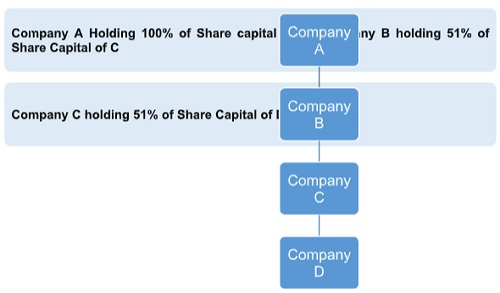

Visual Presentation for point 3:

In the above case, a fast-track merger was permitted only between Company A and Company B, i.e., a holding company and its wholly-owned subsidiary. However, with the Companies (Compromises, Arrangements and Amalgamations) Amendment Rules, 2025 coming into force, a scheme of merger, amalgamation, transfer, or division between Company A, Company B, Company C, and Company D or any combination of merger, amalgamation, transfer, or division is now allowed, thereby widening the scope for companies to undertake a fast-track merger for the Company.