Summary: Tax Deducted at Source (TDS) on payments to non-residents (NRs) in India ensures tax compliance and prevents evasion. Section 195 of the Income Tax Act outlines the TDS requirements for such payments. Non-residents generating income in India may face double taxation, which is mitigated through Double Taxation Avoidance Agreements (DTAAs) or relief under Sections 90 and 91. Payments to NRs establish a business connection when activities, such as contract conclusion or stock delivery, are carried out in India on their behalf. Additionally, significant economic presence, defined by revenue exceeding ₹2 crores or interactions with at least 3 lakh users, also constitutes a business connection. Specific exemptions exist under Explanation 1 to Section 9(1)(i), while Explanation 5 clarifies the treatment of assets deriving value from Indian properties, as seen in the Vodafone case. Certain royalty payments, defined broadly to include software use, patent licenses, and technical services, are taxable unless exempted through specific provisions like Notification No. 21/2012. These provisions ensure clarity and compliance for transactions involving NRs, facilitating international business while safeguarding tax interests.

In India, tax is typically deducted at source to prevent tax evasion by placing the responsibility on Individual or entity making the payment, regardless of the status of the recipient, if the payment falls under the provisions of the Income Tax Act.

Non-residents who often generate income from various sources, in India would face taxation in both India and their country of residence, leading to double taxation.

To avoid this, international principles stipulate that the same income should not be taxed twice, which is where Double Taxation Avoidance Agreements (DTAAs), become very significant in providing relief and encouraging cross border transactions.

To address such situations, the Income Tax Act, 1961 provides relief (Sec. 90 & Sec. 91) from double taxation through either Bilateral Relief or Unilateral Relief.

In India, relief is granted through the credit method under Section 91 for taxes paid in countries with which India does not have a DTAA.

With this context in mind, let’s now understand on how tax should be deducted at source (TDS) on any payments made to NRI or a Foreign company.

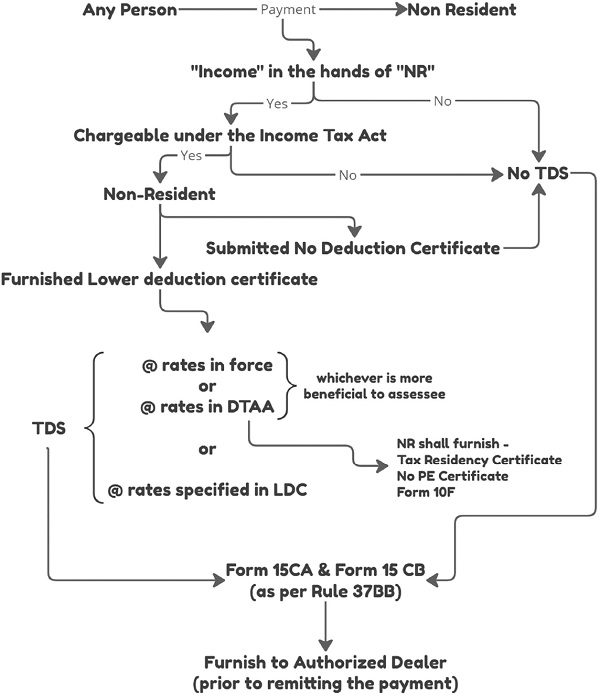

Sec.195 outlines the TDS provisions for making payments to Non-residents.

TDS on Payments to NRs

Business Connection

Include any business activity carried out through a person acting on behalf of the non-resident.

- Must

- have an authority, to conclude contracts or

- habitually concludes contracts or

- plays the principal role leading to conclusion of contracts

- Habitually maintain a stock from which he regularly delivers on behalf of NR.

- Habitually secure order in India mainly or wholly for NR.

Further there may be situations when the person acting on behalf of the non-resident secure order for other non-residents.

Business connection for other non-residents is established if it’s controlled by the non-resident or vice versa or is subject to same control as that of non-resident.

“Agents having independent status are not included in business connection”

Explanation 2A to Sec. 9(1)(i)

Significant Economic Presence of a non-resident in India shall also constitute business connection in India (irrespective of place of agreement or residence or place of business or rendering of services in India or not).

– In respect of any goods, services or property carried out by NR with any person in India including provision of download of data or software in India > Aggregate of payment arising from such transaction or transactions during the previous year should exceed Rs. 2 crores.

– Systematic & continuous soliciting of business activities or engaging in interaction with users in India > the number of users should be at least 3 lakhs.

Explanation 1 to Sec. 9(1)(i)

Following shall not, be treated as business connection in India

Explanation 5 to Sec. 9(1)(i) – Vodafone Caselaw

Further, an asset or a capital asset being any share or interest in a company or entity registered or incorporated outside India shall be deemed to be and shall always be deemed to have been situated in India, if the share or interest derives directly or indirectly, its value substantially from the assets located in India

Not applicable to Foreign Institutional Investors (FII) and Foreign Portfolio Investors (FPI)

Declaration of Dividend by Foreign company outside India doesn’t have the effect of transfer of any asset underlying assets located in India. Hence, such income is not deemed to accrue or arise in India.

Exception – Income shall not be deemed to accrue or arise to a non-resident from transfer, outside India, of any share of, or interest in, a company or an entity registered or incorporated outside India

- Foreign company or entity directly or indirectly owns the assets situated in India

AND

- Transferor, directly or indirectly, at any time in the twelve months preceding the date of transfer, doesn’t hold – The right of management or control; or 5% of the Total voting power or shares

Royalty –

Consideration for –

- Transfer of all or any rights (including the granting of license) in respect of

- Imparting of any information concerning the working of, or the use of

- Imparting of any information concerning technical, industrial, commercial or scientific knowledge, experience or skill

- Use or right to sue any industrial, commercial or scientific equipment but not including the amounts referred u/s 44BB

- Transfer of all or any rights (including the granting of a license) in respect of any copyright, literacy, artistic or scientific work including films or video tapes for use in connection with television or with radio broadcasting

of any patent, invention, model, design, secret formula or process or trade mark or similar property

Note – Sale, distribution or exhibition of cinematographic films is also covered within scope

- Rendering of any services in connection with the activities referred in above clauses.

- Use or right to use of computer software

CG has, vide Notification No. 21/2012 dated 13th June 2012 to be effective from 1st July, 2012, exempted where payment is made by the transferee for acquisition of software from a resident transferor, the provisions of Sec. 194J would not be applicable if –

- Software acquired without any modification by the transferor

- Tax already deducted either under Sec. 194J or Sec. 195 on payment for any previous transfer of such software &

- Transferee obtains a declaration from the transferor that tax has been so deducted along with the PAN of the transferor.

No tax is required to be deducted at source under Sec. 195, if the amount paid by resident Indian end-users to non-resident, as consideration for the resale or use of the computer software through EULA (end-user license agreements or distribution agreements) is not royalty.

| Product | Purchased by | Purchased from |

| Computer Software | End-user, Resident in India | Foreign, non-resident supplier or manufacturer |

| Resident Indian Companies – acting as distributors or resellers | ||

| Foreign, non-resident vendor who resells the same to resident Indian distributors or end-users | ||

| Computer software affixed onto hardware and is sold as an integrated unit/equipment | Resident Indian distributors or end-users |

Royalty Income shall not be deemed to accrue or arise in India, if –

- It’s for supply of computer software along with computer hardware under the scheme of CG

- Transfer of property is already taxable “Capital Gain”

Rule 37BB

Furnishing of information for payment to a non-resident (Form No. 15CA) – shall be e-signed and furnish to Authorised Dealer prior to remitting the payment.

Overview of the Tax Deducted at Source (TDS) on Foreign Payments

Author is a finance and tax professional based in Bangalore, and can be contacted via email at abhinav_prasad2@outlook.com

Author Bio