The Securities and Exchange Board of India (SEBI) has barred fugitive businessman Vijay Mallya from accessing the securities markets for three years, citing his involvement in routing funds through overseas bank accounts to secretly trade shares of his group companies. An investigation revealed that between January 2006 and March 2008, Mallya used Matterhorn Ventures, a Foreign Institutional Investor (FII), to covertly trade shares of Herbertsons Ltd and United Spirits Ltd (USL) by routing funds through various overseas accounts with UBS AG. SEBI found that Matterhorn Ventures was misrepresented as a non-promoter public shareholder despite its 9.98% shareholding being funded by Mallya, violating the Prohibition of Fraudulent and Unfair Trade Practices (PFUTP) Regulations.

As a consequence, SEBI has barred Mallya from buying, selling, or dealing in securities directly or indirectly for three years and has restrained him from associating with any listed company in any capacity during this period. This action follows a previous SEBI ban in June 2018, which prohibited Mallya from the securities market for three years due to manipulative activities and improper transactions in USL shares. Additionally, he was barred from holding a director or key managerial position in any listed company for five years. SEBI’s recent order underscores the importance of regulatory compliance and the integrity of the securities market.

Securities and Exchange Board of India

QJA/AA/IVD/ID4/30592/2024-25

BEFORE THE SECURITIES AND EXCHANGE BOARD OF INDIA

ORDER

UNDER SECTION 11B READ WITH SECTION 11(1) OF THE SECURITIES AND EXCHANGE BOARD OF INDIA ACT, 1992

In respect of

Mr. Vijay Mallya

[PAN No. AENPM6247A]

In the matter of routing of funds to the Indian Securities market using overseas bank accounts with UBS AG

Background:

1. Securities and Exchange Board of India (‘SEBI’) had suo-moto taken up the instant matter for further investigation based on the findings in the communication from the Financial Services Authority (now known as Financial Conduct Authority and hereinafter referred to as ‘FSA / FCA’) to ascertain whether there was any routing of funds to the Indian Securities Market by Mr. Vijay Mallya (hereinafter referred to as the ‘Noticee’), Chairman of the UB Group and individual controlling shareholder of United Spirits Limited (‘USL’) during the relevant period, through his bank accounts with UBS AG, London (‘UBS’) in violation of the provisions of the SEBI Act, 1992, SEBI (Prohibition of Fraudulent and Unfair Trade Practices relating to Securities Market) Regulations, 2003 (hereinafter referred to as the ‘PFUTP Regulations, 2003’) and the rules and regulations framed thereunder during the period from January 01, 2006 to March 31, 2008. However, wherever deemed necessary, period outside the investigation period is considered.

2. The investigation, prima facie, revealed that that the Noticee had used a sub-account i.e. Matterhorn Ventures, a Foreign Institutional Investor (FII), as an investment vehicle to indirectly trade in scrips of his own group entities in India i.e. Herbertsons Limited (‘Herbertsons’) and USL. Thus, the investigation revealed that the amounts paid to Matterhorn Ventures were routed by the Noticee by opening various beneficiary accounts with UBS and routing these funds through these accounts, indirectly, to the Indian Securities Market. It was observed that this financial route (FII route) was taken by the Noticee in the names of various overseas registered entities, thereby, concealing the true identity of his investments in Indian Securities market. Furthermore, it was observed that the said FII was shown as a non-promoter public shareholder in the shareholding pattern of Herbertsons whereas, Matterhorn Venture’s holding of 9.98% shares actually belonged to the promoter category.

3. In view of the above, it was alleged that the acts of the Noticee of dealing in securities of listed companies of his group in India, indirectly, in a fraudulent manner and by employing a manipulative and deceptive artifice was in violation of the provisions of Regulations 3(a), (b) and (d) of the PFUTP Regulations, 2003 read with Section 12A(a) and (c) of the SEBI Act, 1992. Further, by showing the shareholding of Matterhorn Ventures in Shareholding Pattern of Herbertsons under the non-promoter public holding category, the Noticee is alleged to have misrepresented the truth and concealed a material fact known to him in violation of the provisions of Regulation 4(2)(f) of the PFUTP Regulations, 2003.

SHOW CAUSE NOTICE, REPLIES AND PERSONAL HEARING:

4. A Show Cause Notice dated April 13, 2023 (‘SCN’) was issued to the Noticee calling upon him to show cause as to why direction(s) under Section 11B(1) read with Section 11(1) of the SEBI Act, 1992 should not be issued against him for the alleged violations of provisions of law mentioned above. The said SCN was sent via Air Mail and was duly delivered to the Noticee on his address/es viz. Ladywalk Queen Hoo Lane, Tewin, Welwyn, AL6 OLT, United Kingdom and 18-19 Cornwall Terrace, Regent’s Park, London NW1 4QP, Greater London, England. Thereafter, vide letter dated June 15, 2023, the Noticee, while acknowledging receipt of the SCN raised preliminary objections to the proceedings initiated against him vide the said SCN, which are summarized as under and requested for copies of (a) emails dated May 24, 2007 and May 25, 2007, and (b) bank statements of Venture New Holding Limited (‘VNHL’) referred in the SCN, relevant to the charges levelled in the SCN:

4.1 The Noticee submitted that the SCN pertains to purported securities transactions and purported monetary dealings which appear to be of 2006 and 2007 i.e. atleast 15 years old. Therefore, it is the case of the Noticee that there has been an egregious delay in SEBI initiating an inquiry or investigation in relation to the aforesaid 15 years old purported securities transactions and money dealings.

4.2 The Noticee further states that even assuming arguendo that the purported securities transactions and monetary dealings did allegedly take place, there is nothing in the SCN to show that the said dealings disrupted the functioning of the market or had any detrimental impact on the market or investor confidence or undermine the people’s faith and trust in SEBI as the protector of securities law in India.

4.3 The Hon’ble Supreme Court has repeatedly held that in the absence of any period of limitation, the authority is required to exercise its powers within reasonable period.

5. I note from the records available in the file that after seeking consent from FCA for sharing the copies of emails dated May 24, 2007 and May 25, 2007 with the Noticee, SEBI, vide letter dated October 26, 2023, while stating that the relevant extract of the bank statements of VNHL has been already shared along with the SCN issued as Annexure C, granted an opportunity to the Noticee to inspect the aforementioned emails. The said letter was duly delivered to the Noticee. Considering that the Noticee neither availed the opportunity to inspect the documents nor filed any reply to the said letter even after approx. 1 year 3 months from the issuance of the SCN, upon allocation of the said matter to me, in compliance with the principles of natural justice, it was felt appropriate to grant an opportunity of hearing to the Noticee in the matter. Accordingly, an opportunity of hearing was provided to the Noticee on March 14, 2024. It may be noted that the Noticee did not avail of the said opportunity. However, vide letter dated March 12, 2024 (received vide email dated March 12, 2023 and March 13, 2024), the Noticee, while reiterating the preliminary objections raised by him vide his reply dated June 15, 2023, submitted that the SCN issued in respect of the purported transactions and monetary dealings referred therein, being barred by law of limitation, is non-est, void and cannot be proceeded with. The Noticee further has submitted his concern with regards to SEBI not providing the copies of the bank statements of VNHL and the emails dated May 24, 2007 and May 25, 2007 referred in the SCN and instead SEBI providing for a physical opportunity to inspect the said documents.

6. In order to address the concerns raised with respect to the request of documents, vide email dated March 19, 2024, the Noticee was once again provided with the relevant extract of the bank statements of VNHL and legible copies of emails dated May 24, 2007 and May 25, 2007 referred in the SCN. Further, as the Noticee had not filed any reply to the allegations made against him in the SCN, he was advised to file his reply, if any, within 15 days from the date of the email. Vide email dated March 28, 2024, the Noticee, while acknowledging the receipt of the said documents, once again requested for the entire bank account statements of VNHL instead of the relevant extract. Accordingly, vide email dated April 12, 2024, SEBI provided the bank statements of VNHL to the Noticee. Further, time till April 30, 2024 was provided to the Noticee to file his reply in the matter. However, vide email dated April 28, 2024, the Noticee requested for grant of additional time till May 31, 2024 to file his reply to the SCN. The said request of the Noticee was partly acceded to and vide email dated May 02, 2024, time till May 20, 2024 was granted to file a reply. Further, vide the said email, an opportunity of personal hearing was also provided to the Noticee on May 28, 2024. However, the Noticee, vide his email dated May 20, 2024, requested for short extension till May 27, 2024 to file his reply to the SCN on the ground of summer vacation in High Court of Bombay and most of the lawyers being unavailable. In order to proceed with the case by following the principles of natural justice, the said request of the Noticee was acceded to and the Noticee was advised to file his reply to the Noticee before the scheduled date of hearing i.e. May 28, 2024. Vide email dated May 27, 2024, the Noticee filed his reply to the SCN vide letter dated May 27, 2024. The Noticee in the said reply reiterated his submissions made in the letter dated June 15, 2023 and further stated that the said proceedings initiated against him by SEBI appear to be to perpetuate the order dated March 31, 2008 passed by the former Whole Time Member, SEBI under Sections 11(1), 11(4) and 11B of the SEBI Act, inter alia, restraining the Noticee from “holding position as Director or Key Managerial Person of a listed company for a period of fine years from the date of this order” which expired on May 31, 2023. The submissions of the Noticee in a nutshell are summarized as under:

6.1 The proceedings initiated by SEBI against the Noticee for the purported transactions and monetary dealings for the period of 2006 and 2007 are with egregious delay.

6.2 Under the various Regulations framed under the SEBI Act and circulars issued by SEBI, books of accounts and records are required to be maintained for either 5 or 8 years. For instance, (i) Regulation 15 of the SEBI (Registrars to an Issue/ Share Transfer Agents) Regulation, 1993 mandates that a registrar to an issue or share transfer agent preserves “books of accounts and other records and documents” for 8 years; and (ii) SEBI Circular dated August 30, 2016 bearing no. SEBI / HO / CDMRD/DMP/CIR/P/2016/74 issued under Section 11(1) of the SEBI Act, 1992 refers to Rule 14 and 15 of Securities Contracts (Regulation) Rules, 1957 which mandates that “books of accounts and other records and documents” be preserved for a period of 2 to 5 years and Regulation 18 of the SEBI (Stock Brokers and Sub-Brokers) Regulations, 1992 mandates preservation of “Specified books of accounts and other records” for 3 years.

6.3 Even under the Companies Act, 2013, books of accounts, vouchers and Annual Returns filed with the Registrar of Companies are required to be maintained for 8 years where as the Income Tax Act, 1961 prescribes 8 years and Central Excise Act and Service Tax Act prescribes 5 years.

6.4 Therefore, the Noticee submits that he is unable to confirm or verify the veracity and authenticity of the further documents belatedly made available to him by SEBI given that such old records are not available with him nor are they accessible any longer. In view of the same, the Noticee states that he is put to a serious, unfair and inequitable handicap which is violative of all norms of fairness, equity and principles of natural justice.

6.5 The Noticee reiterates that even assuming arguendo that the purported securities transactions and monetary dealings did allegedly take place, there is nothing in the SCN to show that the said dealings disrupted the functioning of the market or had any detrimental impact on the market or investor confidence or undermine the people’s faith and trust in SEBI as the protector of securities law in India.

6.6 While placing reliance on judgments of the Hon’ble Supreme Court in the cases of SEBI Vs. Bhavesh Pabari (2019) 5 SCC 90 para 35 and SEBI Vs. Sunil Krishna Khaitan and Others (2023) 2 SCC 643 paras 92 and 93 and decisions of the Hon’ble SAT in SIC Stock & Services P. Ltd Vs. SEBI decided on September 02, 2022 in Appeal No. 639 of 2021 following the decision in SEBI Vs. Bhavesh Pabari, the Noticee submits that the issuance of SCN after a lapse of 15 years cannot and does not amount to SEBI exercising its powers within reasonable period.

6.7 Therefore, the Noticee submits that the SCN is non-est, void and cannot be proceeded with. Further, he states that the hearing purportedly scheduled by SEBI on May 28, 2024 is an empty formality to make a show of having allegedly complied with the principles of natural justice and that SEBI should cease and desist to proceed any further with the SCN or any investigation in the matter.

7. From the chronology of events of the case, it is noted that the SCN was issued to the Noticee on April 13, 2023 in the subject matter. Further, an opportunity to inspect the requested documents was provided to the Noticee vide SEBI letter dated October 26, 2023 and further, were provided to him vide SEBI email dated April 12, 2024. However, it is noted that the Noticee, did not respond on merits or on the violations alleged in the SCN. Also, despite providing two opportunities of hearing to the Noticee on March 14, 2024 and May 28, 2024, the Noticee has not availed of the same. However, considering that “audi alteram partem” being one of the fundamental principles of natural justice which lays down the proposition that a fair opportunity of answering / defending the case must be granted before passing an order against any person, it was felt appropriate to grant the Noticee with a last and final opportunity of personal hearing which was accordingly provided to the Noticee on June 13, 2024. Further, the Noticee was also advised to file his reply on merits on or before the scheduled date of hearing. However, I note that the Noticee, despite receipt of the email dated May 31, 2024 granting the last and final opportunity of hearing on June 13, 2024, neither made any submissions on the allegations made in the SCN on merits nor did he attend the hearing on the scheduled date. Instead, he has chosen to raise objection about delay in initiation of the proceedings against him and that hearing is an empty formality.

8. In the instant case, I note that the Noticee has been given ample and sufficient opportunities to file his reply on merits and to defend his case. Three opportunities of hearing were also granted to him on March 14, 2024, May 28, 2024 and June 13, 2024. However, by not availing of the said opportunities the Noticee has voluntarily waived his right to be heard. In this context, it is pertinent to note the observations of the Hon’ble Securities Appellate Tribunal (SAT) in the case of Sanjay Kumar Tayal & Others Vs. SEBI (Appeal No. 68 of 2013 decided on February 11, 2014), wherein, the Tribunal has, inter alia, observed that “………… appellants have neither filed reply to show cause notices issued to them nor availed opportunity of personal hearing offered to them in the adjudication proceedings and, therefore, appellants are presumed to have admitted charges levelled against them in the show cause notices…”.

9. In view of the same, I am constrained to proceed with passing of order in the matter based on the available documents / material on record.

CONSIDERATION OF ISSUES AND FINDINGS:

10. I have carefully perused the allegations levelled against the Noticee in the SCN issued, the preliminary objections raised by the Noticee vide his letters dated June 15, 2023, March 12, 2024 and May 27, 2024 and the material available on record. I find that in order to appreciate the charges levelled against the Noticee, it would be apposite to refer to the above-stated relevant provisions of the SEBI Act, 1992 and PFUTP Regulations, 2003 which have a bearing on the allegations made against the Noticee. These relevant provisions are reproduced hereunder for facility of reference:

PFUTP Regulations, 2003:

3. Prohibition of certain dealings in securities

No person shall directly or indirectly—

a) buy, sell or otherwise deal in securities in a fraudulent manner;

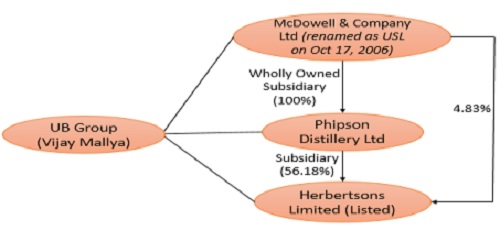

b) use or employ, in connection with issue, purchase or sale of any security listed or proposed to be listed in a recognized stock exchange, any manipulative or deceptive device or contrivance in contravention of the provisions of the Act or the rules or the regulations made there under;

c) ..

d) engage in any act, practice, course of business which operates or would operate as fraud or deceit upon any person in connection with any dealing in or issue of securities which are listed or proposed to be listed on are cognized stock exchange in contravention of the provisions of the Act or the rules and the regulations made there under.

4. Prohibition of manipulative, fraudulent and unfair trade practices

(2). Dealing in securities shall be deemed to be a manipulative fraudulent or an unfair trade practice if it involves any of the following—

(a)…………

(e)………………..

(f) knowingly publishing or causing to publish or reporting or causing to report by a person dealing in securities any information relating to securities, including financial results, financial statements, mergers and acquisitions, regulatory approvals, which is not true or which he does not believe to be true prior to or in the course of dealing in securities.

SEBI Act, 1992

Prohibition of manipulative and deceptive devices, insider trading and substantial acquisition of securities or control.

12A. No person shall directly or indirectly –

(a) use or employ, in connection with the issue, purchase or sale of any securities listed or proposed to be listed on a recognized stock exchange, any manipulative or deceptive device or contrivance in contravention of the provisions of this Act or the rules or the regulations made thereunder;

(b) employ any device, scheme or artifice to defraud in connection with issue or dealing in securities which are listed or proposed to be listed on a recognised stock exchange;

(c) engage in any act, practice, course of business which operates or would operate as fraud or deceit upon any person, in connection with the issue, dealing in securities which are listed or proposed to be listed on a recognised stock exchange, in contravention of the provisions of this Act or the rules or the regulations made thereunder;

11. I note that in order to adjudge the charges in the present case, it is important to understand the scheme / artifice devised by the Noticee as alleged in the SCN to route the funds through FII to the Indian securities market. However, before going into the matter on merits, the preliminary objections raised by the Noticee with respect to initiation of the instant proceedings against him are being dealt with.

Preliminary issues raised and findings:

Delay:

12. The Noticee, vide his replies dated June 15, 2023, March 12, 2024 and May 27, 2024, has raised a preliminary objection on initiation of the present proceedings against him with a delay of almost 15 years. It is the case of the Noticee that the purported securities transactions and purported monetary dealings appear to be of the years 2006 and 2007 and initiation of the instant proceedings with such a delay has put the Noticee to a serious, unfair and inequitable handicap which is violative of all norms of fairness, equity and principles of natural justice.

13. In order to deal with the said objection raised by the Noticee, I find it pertinent to look at the chronology of events, before and after, initiation of the instant proceedings for the alleged violations of securities laws in respect of the Noticee.

14. I find that pursuant to the findings from FSA’s communication dated January 22, 2010, vide which certain information was provided to SEBI by FSA, SEBI, suo-moto had taken up the matter for further investigation to ascertain whether there was any routing of funds to Indian Securities market by the Noticee through his bank accounts with UBS AG, London to trade, inter alia, in the scrip of UB group companies during the period from April 01, 2006 to March 31, 2008. I also find that an email query dated August 01, 2013 was also received from Economic Times, inter alia, seeking clarification as to whether FSA had confirmed some of the names including that of the Noticee to SEBI about routing of funds to India and if SEBI has investigated into the same. In order to investigate into the transactions, the email communications provided by FSA between an employee of UBG AG viz. Jaspreet Ahuja and the Noticee were examined. Further, I find that in order to ascertain the transaction details mentioned in the email correspondence, price volume data for all the companies controlled / promoted by the Noticee were examined. Information / documents were sought from foreign authority viz. FCA – UK in the year 2013 with respect to the overseas entities, prima facie, found to be involved in the routing of funds. Thereafter, vide order dated June 18, 2014, in exercise of the powers conferred under Section 19 read with Section 11 and 11C of the SEBI Act, 1992, an Investigating Authority was appointed to undertake the investigation in the matter. Considering the formalities and approvals required for sharing of information and the regular follow ups, the data / information from FCA – UK was received in multiple tranches in the years 2014, 2016, 2018 and 2020. Based on the information provided by FCA – UK, further information was sought from other foreign authorities viz. MAS (Singapore), JFSC (Jersey) and FINMA (Switzerland) in the year 2020 and from SEC (USA) in the year 2021. Furthermore, information was sought from UB Group companies (March 2014 onwards), bank accounts of the Noticee and various related entities were analysed to ascertain the fund flow, summonses were issued to the employees of UBS AG, London Bank (July 2014 onwards), statements were recorded, correspondence was done with FSC, Mauritius (in December 2022) and MAS, Singapore (in October 2020), correspondence was made with Deutsche Bank (in the year 2022-23), data was analysed relating to FII Investments, etc. Finally, in 2021, information pertaining to VNHL was obtained from MAS, Singapore. Therefore, considering the number of entities involved in the alleged transactions and the involvement of overseas regulatory bodies / entities and data to be sought from such overseas financial authorities, the investigation in the instant case was concluded only in March 2023 and the proposed enforcement action was initiated against the Noticee by way of issuance of a SCN on April 13, 2023.

15. Thus, I note that in the instant case, SEBI itself started preliminary investigation into the case after receiving the email from FSA in 2010 and further, only after ascertaining certain fundamental data and facts, in 2014 i.e. after appointment of the Investigating Authority, SEBI had started with the detailed and formal investigation into the activities of the Noticee. For the said purpose, SEBI had to collect and collate information and data from various sources including approaching foreign regulators for assistance in procuring information and documents from concerned entities outside India from several jurisdictions. The foreign regulators also had to collect this information from the concerned entities in order to furnish it to SEBI. Thus, the process of collection of information in the matter was complex, tedious and time consuming. It is noted that as the activity under investigation was that of routing of funds through entities located in different jurisdictions, reliance is placed on the decision of the Hon’ble SAT in the case of Jindal Cotex Ltd and Others Vs. SEBI (Appeal No. 376 of 2019 decided on February 05, 2020), wherein, while dealing with a plea of delay, the Hon’ble Tribunal observed that,

“………….. arguments on delay in investigation and consequently affecting natural justice are also devoid of any merit in the matter since this Tribunal is aware of the complexity involved in the entire manipulative GDR issue; how long it took SEBI to gain information relating to the various entities from multiple jurisdictions in the matter of PAN Asia Advisors Limited (Supra) and Cals Refineries Limited (Supra) etc

16. Similarly, in the case of V. Films Ltd Vs. SEBI (Appeal No. 168 of 2020 decided on February 15, 2021), the Hon’ble SAT observed that,

“Having heard the learned counsel for the parties on this issue, we find that there is no doubt that there has been a delay in the issuance of the show cause notice after 10 years from the date of the GDRs issue. However, on this ground of delay, the proceedings cannot be quashed for the reasons that we find that an investigation was required to be done beyond the borders of India which took time.” (Emphasis supplied)

17. In addition, it is pertinent to further note that upon issuance of the SCN on April 13, 2023 by Air Mail, the sequence of events in the instant case are as under:

| Date | Particulars |

| 15.06.2023 | While raising preliminary objections on initiating enforcement proceedings, Noticee sought for certain documents. |

| 26.10.2023 | Clarification was given to the Noticee on the documents sought and further, an opportunity to inspect the documents requested was provided. |

| 23.01.2024 | As no reply was received from the Noticee, opportunity of hearing was granted to the Noticee on 14.03.2024 |

| 12.03.2024 | The Noticee, while reiterating the submissions made vide his reply dated June 15, 2023, requested for the entire bank statements of Venture New Holdings Limited instead of the extract provided in October 2023 and the copies of the emails dated May 24, 2007 and May 25, 2007. |

| 19.03.2024 | SEBI email clarifying to the Noticee that the relevant extract and the email copies have already been provided along with the SCN. |

| 28.03.2024 | Letter from the Noticee seeking the entire bank statements of Venture New Holdings Limited |

| 12.04.2024 | Vide SEBI email, the documents sought for by the Noticee were provided to him after procuring them from MAS, Singapore. Further, time till April 30, 2024 was provided to file reply on merits to the SCN. |

| 27.04.2024 | Extension of time till May 31, 2024 sought by the Noticee. |

| 02.05.2024 | Time till May 20, 2024 to file reply was granted and further, next date of hearing was scheduled on May 28, 2024 and communicated to the Noticee. |

| 20.05.2024 | Noticee sought another extension till May 27, 2024 to file his reply. |

| 24.05.2024 | The said request was again acceded to and Noticee was advised to submit his reply on or before the date of hearing i.e. May 28, 2024 |

| 27.05.2024 | Noticee filed his preliminary objections on initiation of the proceedings against him. No reply filed on merits. Submitted that opportunity of hearing provided to him is an empty formality to show compliance with principles of natural justice. |

| 28.05.2024 | Did not avail of the opportunity of hearing. |

| 31.05.2024 | Last and final opportunity of hearing was provided to the Noticee on June 13, 2024 and vide the said SEBI email, Noticee was advised to file his reply on merits on or before the scheduled date of hearing. |

| 13.06.2024 | Noticee neither filed any reply on merits nor appeared for the hearing scheduled on this date. |

18. From the above chronology of events, it can be seen that the SCN was issued to the Noticee on April 13, 2023 in the subject case. The Noticee has only raised objection on the delay involved in initiating action. Further, vide SEBI letter dated October 26, 2023, an opportunity to inspect the documents was also provided to the Noticee. However, the said opportunity was not availed by the Noticee. Further, vide email dated April 12, 2024, clarification on the documents sought was also provided. It is noteworthy that the Noticee, till date, has not filed any reply on merits. Also, opportunities of hearings were provided to the Noticee on March 14, 2024, May 28, 2024 and June 13, 2024. However, the Noticee has not availed the said opportunities to defend his case.

19. In view of the above, even though the instant proceedings were initiated against the Noticee in April 2023 itself, the above sequence of events shows the non-cooperation on the part of the Noticee to participate in the said proceedings and disregard to the regulatory proceedings and communications. I find that admittedly, even though the transactions involved in the matter are for the years 2006-07, the fact that material/ documents such as (i) extracts of transactions with Venture New Holdings Limited, (ii) transactions undertaken by Matterhorn Ventures, email dated January 31, 2023 from UBL, (iii) beneficial ownership documents, etc. have been provided to the Noticee based on which the charges have been levelled against the Noticee in the SCN cannot be ignored. I note that the Noticee was also provided with the entire bank account statement of VNHL and emails dated May 24, 2007 and May 25, 2007 between Jaspreet Ahuja, employee of UBS, and the Noticee which have been relied upon in the SCN. In Natwar Singh vs Director of Enforcement and Another (2010) 13 SCC 255, the Hon’ble Supreme Court held that the fundamental principle remains that nothing should be used against the person which has not been brought to his notice. If relevant material is not disclosed to a party, there is prima- facie unfairness irrespective of whether the material in question arose before, during or after the hearing. The Supreme Court further held that the law is fairly well settled, namely that if prejudicial allegations are to be made against a person, he must be given particulars of that before the hearing so that he could prepare his defence.

20. I note that the fact that the Noticee, even after the receipt of the said documents, has chosen not to file any reply on merits and did not avail the opportunities of hearing provided to him further substantiates the position that the Noticee, has willingly, not participated in the proceedings and the same cannot be ignored. I find that raising an objection of delay, without even attempting to defend the charges levelled on him in the SCN appears to be a tactic devised by the Noticee to evade the present proceedings and the allegations levelled in the SCN and further, to camouflage such allegations by highlighting the delay.

21. Here, I would like to place reliance on the observations of the Hon’ble SAT in the case of Anant R Sathe Vs. SEBI (Appeal No. 150 of 2020) decided on July 17, 2020, wherein, the Hon’ble SAT, while re-affirmed the principle elucidated in the decision in the case of Shruti Vora Vs. SEBI (Appeal Lodging No. 28 of 2020) decided on February 12, 2020, observed that the authority is required to supply the documents that they rely upon while serving the show cause notice which if done is sufficient for the purpose of filing an efficacious reply in defence.

22. In view of the above facts and chronology of events, it is concluded that even though the transactions alleged in the instant proceedings are for the period of 2006 – 07, I find the SEBI investigation required collection and collation of data / information from foreign authorities with respect to foreign entities and that the entire fact finding process in the matter was complex, tedious and time consuming given the fact that it involved approaching cross border regulators for assistance in procuring information and documents in respect of entities located outside India from many jurisdictions. Furthermore, the fact that the relevant and relied upon documents were sufficiently provided to the Noticee during the present proceedings in order to enable him to defend his case fairly, I am of the considered view that the said objection of delay cannot be considered and is merely an attempt on the part of the Noticee to evade participation.

Opportunity of hearing, an empty formality:

23. I find that the Noticee, vide his letter dated May 28, 2024, while reiterating the objections raised by him in his reply dated June 15, 2023 with respect to initiation of the proceedings against him, stated that the opportunity of hearing provided to him in the instant proceedings is an empty formality to make a show of having allegedly complied with the principles of natural justice. Here, I note that the principles of natural justice are principles followed in order to make a sensible and reasoned decision on a particular issue / charge in hand. These principles did not originate from any divine power, but are the outcome of judicial thinking, as well as the necessity to evolve the norms of fair play. The said principles of justice are procedural in nature and their aim is to ensure delivery of justice to the parties. Adherence to rules of natural justice, as recognised by all courts, is of supreme importance, when a quasi-judicial body embarks on determining the issues involved and / or violations of the provisions of law. Rules of natural justice hedge against any blatant discrimination against the rights of individuals. These rules are intended to prevent injustice being done by any authority while determining the issues before them. The said principles of natural justice are firmly grounded in Articles 14 and 21 of the Constitution of India.

24. The first principle of natural justice is “audi alteram partem” which is one of the fundamental principles of natural justice laying down the proposition that a fair opportunity of answering / defending the case must be granted before passing of an order by an authority against any person. The said opportunity has to be real, reasonable and effective. Therefore, denial of such opportunity of being heard can make a proceeding void ab initio. In Chairman Mining Board Vs. Ramjee 1977 AIR 965 SC, the Hon’ble Supreme Court has observed as under:

“Natural justice is no unruly horse, no lurking landmine, nor a judicial cure-all. If fairness is shown by the decision-maker to the man proceeded against, the form, features and the fundamentals of such essential procedural propriety being conditioned by the facts and circumstances of each situation, no breach of natural justice can be complained of. Unnatural expansion of natural justice without reference to the administrative realities and other factors of a given case can be exasperating. Courts cannot look at law in the abstract or natural justice as a mere artefact… If the totality of circumstances satisfies the Court that the party visited with adverse order has not suffered from denial of reasonable opportunity the Court will decline to be punctilious or fanatical as if the rules of natural justice were sacred scriptures.”

25. In the instant case, as can be seen from the preceding paragraphs, ample opportunities have been given to the Noticee to file his reply to the SCN on merits and to defend his case. Further, in compliance with the abovementioned principle of natural justice, opportunities of hearing were granted to him with sufficient notice so as to present his case before me. The request for extending the time to file reply has been considered and the timelines have been extended and opportunity of hearing has also been adjourned on two to three occasions. Further, despite the Noticee stating that the granting of hearing is a mere formality to show compliance with the principles of natural justice, considering the facts of the case, a last and final opportunity of hearing was granted to the Noticee on June 13, 2024. However, the Noticee, instead of submitting a reply to the SCN on merits and appearing on the scheduled date/s of hearing has chosen to refuse the said opportunities by stating that the same being an empty formality to show compliance with the principles of natural justice. I find that it is well settled law that refusal to participate in an enquiry without a valid reason cannot be pleaded as violation of natural justice at a later stage.

26. Having addressed the preliminary objections and issues raised by the Noticee in his submissions, I would now proceed to deal with the case on merits.

27. I note that the SCN alleges that the Noticee has abused the FII route to trade in the Indian Securities Market by concealing his identity in the names of various overseas registered entities, in whose names the bank accounts were opened with UBS, even though the Noticee allegedly was the actual beneficial owner of each of the front entities in a fraudulent manner by employing manipulative and deceptive artifice by indulging in purchase and sale of securities of Herbertsons / USL detrimental to the investors and with an intent to defraud them. In view of the same, the SCN alleges the Noticee to have violated the provisions of Regulations 3(a), (b) and (d) of the PFUTP Regulations, 2003 read with Sections 12A(a) and 12A(c) of the SEBI Act, 1992. The SCN further alleges the Noticee to have misrepresented the truth and concealed a material fact known to him that the FII holding of 9.98% shares in the name of Matterhorn Ventures shown in the non-promoter public shareholding category in the shareholding pattern of Herbertsons actually belonged to the promoter category, thereby violating the provisions of Regulation 4(2)(f) of the PFUTP Regulations.

28. I note from the material available on record and from the SCN that an email communication dated May 24, 2007 between Jaspreet Ahuja (employee of UBS) and email id vjm@ubmail.com was investigated by SEBI. The contents of the said communication are reproduced as under:

“# Total number of shares bought: 633,333 shares @ average price of Rs. 398.43

# Total number of shares sold: 408, 333 shares @ average price of Rs. 952.24

# Total Loan Amount: USD 6,150,000

# Net Gain Till Date: approx. USD 5.51 million

# Price movement today: closing Rs. 1142

High Rs. 1195

Low Rs. 1130”

29. UBL, during the investigation, vide email dated January 31, 2023, had confirmed that the email id vjm@ubmail.com belonged to the Noticee. Further, upon analysing and examining the email communication along with the price volume data of the scrip of United Spirits Limited (“USL”) as on May 24, 2007, it was noted that the communication between the Noticee and Jaspreet Ahuja was referring to the trades in the scrip of USL during the relevant period, details of which are as under:

(source: BSE email dated December 09, 2022)

| TRADE DATE |

SCRIP LONG NAME |

OPEN RATE |

HIGH RATE |

LOW RATE |

CLOSE RATE | NO OF TRADES | NO OF SHARES TRADED |

| 2007-05-24 | UNITD SPR |

1171.00 | 1195.00 | 1130.00 | 1142.05 | 9730 | 277688 |

30. I further note that as per the shareholding pattern of USL for the quarter ending June 2006, United Breweries Holdings Limited (“UBHL”) along with the Noticee was shown as Indian promoters holding 36.32%. The shareholding pattern of UBHL available for March 31, 2010 revealed that the Noticee was the ultimate promoter and held 51.44% shares along with other related entities. Therefore, I find that the Noticee controlled USL through UBHL and was in turn, the ultimate individual controlling shareholder of USL.

31. It is further revealed in the investigation undertaken by SEBI that the Noticee had opened various accounts with UBS in the names of multiple entities of which he was the Beneficial Owner. The fact that the Noticee was the ultimate beneficial owner of the various accounts opened with UBS, London or UBS, Singapore was ascertained from KYC and beneficial ownership documents of the said accounts during the relevant period. Details of the said entities and the account numbers with UBS are as under:

(i) Sole Account UV – Highland Trading (“Highland Trading”) (Acc. No. 364567)

(ii) Birchwood Hills Inc (“Birchwood”) (Acc. No. 389458)

(iii) Suncoast Valley Inc (“Suncoast”) (Acc. No. 389459)

(iv) Bayside Enterprise Inc (“Bayside”) (Acc. No. 389460)

(v) VNHL (Acc. No. 138154)

32. In order to further examine the transactions in the said accounts, bank account statements of all the above mentioned entities related / associated with the Noticee were analysed. Upon examination of the said bank account statements, certain details pertaining to counterparties to different transactions made in the account of Vijay Mallya and his related entities under various accounts were noticed. The extracts of the bank account transactions as received from FCA, UK and MAS, Singapore are as under:

(i) Account No – 364567 (Sole Account UV – Highland Trading)

DATE |

CUR REN Y |

DEBIT AMOUNT |

CREDIT AMOUNT |

NAME OF COUNTERPARTY |

COUNTERPAR TY ACC NO |

COUNTERPA RTY BANK NAME |

17/01/2006 |

USD |

1,27,824 |

BIRCHWOOD HILLS INC IA90 |

38945801 |

UBS AG LONDON |

|

17/01/2006 |

USD |

1,43,510 |

BAYSIDE ENTERPRISE INC IA90 |

38946001 |

UBS AG LONDON |

|

17/01/2006 |

USD |

1,43,570 |

SUNCOAST VALLEY INC IA90 |

38945901 |

UBS AG LONDON |

|

30/01/2006 |

GBP |

9,293 |

OASIS CORPORATE SERVICES |

NO ACCOUNT NUMBER QUOTED |

HSBC BANK PLC |

|

08/03/2006 |

GBP |

9,293 |

RETURNE OF FUNDS OASIS CORPORATE SERVICES |

10189632 |

HSBC BANK PLC |

|

13/03/2006 |

USD |

72,714 |

369939 F G IA90 |

36993901 |

UBS AG LONDON |

|

22/03/2006 |

USD |

50,000 |

VENTURE NEW HOLDING LTD |

NO ACCOUNT NUMBER QUOTED |

UBS AG SINGAPORE |

|

07/08/2006 |

USD |

5,00,000 |

UB GULF FZE |

1701270501 |

SCB |

|

08/08/2006 |

USD |

90,000 |

BIRCHWOOD HILLS INC IA90 |

38945801 |

UBS AG LONDON |

|

08/08/2006 |

USD |

1,50,000 |

SUNCOAST VALLEY INC IA90 |

38945901 |

UBS AG LONDON |

|

08/08/2006 |

USD |

1,50,000 |

BAYSIDE ENTERPRISE INC IA90 |

38946001 |

UBS AG LONDON |

|

14/09/2006 |

USD |

13,000 |

UBS FEE |

|||

09/02/2007 |

USD |

1,65,000 |

369939 F G IA90 |

36993901 |

UBS AG LONDON |

|

01/03/2007 |

USD |

3,00,000 |

VENTURE NEW HOLDING LTD |

NO ACCOUNT NUMBER QUOTED |

UBS AG SINGAPORE |

|

01/03/2007 |

USD |

3,00,000 |

364567 U V IA90 |

36993901 |

UBS AG LONDON |

|

23/07/2007 |

USD |

25,50,000 |

VENTURE NEW HLDG LTD NO. 1009156 |

11381540007 |

UBS AG SINGAPORE |

|

23/07/2007 |

USD |

25,50,000 |

369939 F G IA90 |

36993901 |

UBS AG LONDON |

|

01/08/2007 |

USD |

9,50,000 |

VENTURE NEW HLDG LTD NO. 1009156 |

11381540007 |

UBS AG SINGAPORE |

|

01/08/2007 |

USD |

9,50,000 |

369939 F G IA90 |

36993901 |

UBS AG LONDON |

|

31/01/2008 |

USD |

1,00,000 |

369939 F G IA90 |

36993901 |

UBS AG LONDON |

|

06/08/2008 |

USD |

1,00,000 |

369939 F G IA90 |

36993901 |

UBS AG LONDON |

(ii) Account No – 369939 (Sole Account FG – Vijay Mallya)

DATE |

CUR RENCY |

DEBIT AMOUNT |

CREDIT AMOUNT |

NAME OF COUNTERPARTY |

COUNTER PARTY ACCOUNT NUMBER |

COUNTERPARTY BANK NAME |

13/03/2006 |

USD |

72,714 |

364567 U V IA90 |

36456703 |

UBS AG LONDON |

|

09/02/2007 |

USD |

1,65,000 |

364567 U V IA90 |

36456703 |

UBS AG LONDON |

|

01/03/2007 |

USD |

3,00,000 |

364567 U V IA90 |

36456701 |

UBS AG LONDN |

|

23/07/2007 |

USD |

25,50,000 |

364567 U V IA90 |

36456701 |

UBS AG LONDN |

|

01/08/2007 |

USD |

9,50,000 |

364567 U V IA90 |

36456701 |

UBS AG LONDN |

|

11/12/2007 |

USD |

40,00,040 |

CONTINENTAL ADMINISTRATION |

ING BANK |

||

18/12/2007 |

USD |

40,00,000 |

CONTINENTAL ADMINISTRATION SERVICES |

6385818 |

ING BANK |

|

18/12/2007 |

EUR |

10,222 |

369939 F G |

36993902 |

UBS AG LONDON |

|

18/12/2007 |

USD |

14,697 |

369939 F G |

36993904 |

UBS AG LONDON |

|

31/01/2008 |

USD |

1,00,000 |

364567 U V IA90 |

36456703 |

UBS AG LONDN |

|

06/08/2008 |

USD |

1,00,000 |

364567 U V IA90 |

36456701 |

UBS AG LONDN |

|

20/11/2008 |

USD |

10,00,000 |

CONTINENTAL ADMINISTRATION SERVICES |

183592 |

UBS AG SINGAPORE |

(iii) Account No – 389458 (Birchwood Hills Inc)

DATE |

CUR RENCY |

DEBIT AMOUNT |

CREDIT AMOUNT |

NAME OF COUNTERPARTY |

COUNTER PARTY ACC NO |

COUNTERPART Y BANK NAME |

17/01/2006 |

USD |

1,27,824 |

364567 U V IA90 |

36456701 |

UBS AG LONDON |

|

22/02/2006 |

USD |

17,00,040 |

VENTURE NEW HOLDING LTD |

138154 |

UBS AG SINGAPORE |

|

01/03/2006 |

USD |

3,50,040 |

VENTURE NEW HOLDING LTD |

138154 |

UBS AG SINGAPORE |

|

08/08/2006 |

USD |

90,000 |

364567 U V IA90 |

36456701 |

UBS AG LONDON |

|

15/09/2006 |

USD |

20,301 |

UBS FEE |

|||

02/10/2006 |

USD |

10,822 |

UBS TRUSTEES (BAHAMAS) LTD |

52017/01.10 |

UBS BAHAMAS LTD |

(iv) Account No – 389459 (Suncoast Valley Inc)

DATE |

CUR RENCY |

DEBIT AMOUNT |

CREDIT AMOUNT |

NAME OF COUNTERPARTY |

COUNTER PARTY ACC NO |

COUNTERPA RTY BANK NAME |

17/01/2006 |

USD |

1,43,570 |

364567 U V IA90 |

36456701 |

UBS AG LONDON |

|

22/02/2006 |

USD |

17,00,040 |

VENTURE NEW HLDG LTD NO. 1009156 |

138154 |

UBS AG SINGAPORE |

|

01/03/2006 |

USD |

3,50,040 |

VENTURE NEW HLDG LTD NO. 1009156 |

138154 |

UBS AG SINGAPORE |

|

08/08/2006 |

USD |

1,50,000 |

364567 U V IA90 |

36456701 |

UBS AG LONDON |

|

19/09/2006 |

USD |

20,301 |

UBS FEE |

|||

02/10/2006 |

USD |

10,819 |

UBS BAHAMAS LTD |

52017/01.10 |

UBS AG BAHAMAS |

|

23/07/2007 |

USD |

20,50,000 |

VENTURE NEW HLDG LTD NO. 1009156 |

11381540007 |

UBS AG SINGAPORE |

|

03/01/2008 |

USD |

15,000 |

UBS FEE |

(v) Account No – 389460 (Bayside Enterprise Inc)

DATE |

CURR ENCY |

DEBIT AMOUNT |

CREDIT AMOUNT |

NAME OF COUNTERPARTY |

COUNTER PARTY ACC NO |

COUNTERPARTY BANK NAME |

17/01/2006 |

USD |

1,43,510 |

364567 U V IA90 |

36456701 |

UBS AG LONDON |

|

22/02/2006 |

USD |

17,00,040 |

VENTURE NEW HOLDING LTD |

138154 |

UBS AG SINGAPORE |

|

01/03/2006 |

USD |

3,50,040 |

VENTURE NEW HOLDING LTD |

138154 |

UBS AG SINGAPORE |

|

08/08/2006 |

USD |

1,50,000 |

364567 U V IA90 |

36456701 |

UBS AG LONDON |

|

15/09/2006 |

USD |

20,301 |

UBS FEE |

|||

02/10/2006 |

USD |

10,819 |

UBS TRUSTEES (BAHAMAS) LTD |

52017/01.10 |

UBS (BAHAMAS) LTD |

|

23/07/2007 |

USD |

20,50,000 |

VENTURE NEW HLDG LTD 1009156 |

11381540007 |

UBS AG SINGAPORE |

|

03/01/2008 |

USD |

15,000 |

USB FEE |

(vi) Account No – 138154 (Venture New Holding Limited)

| Transaction Booking Date |

Particulars | Credit/ Debit |

Local Currency |

Amount (USD) |

| 2/23/2006 | INCOMING PAYMENT: BAYSIDE ENTERPRISE INC; DEBIT:11003130001 CREDIT:11381540007 BAYSIDE ENTERPRISE INC IA90 138 154 | Credit | USD | 17,00,000 |

| 2/23/2006 | INCOMING PAYMENT: BIRCHWOOD HILLS INC; DEBIT:11003130001 CREDIT:11381540007 BIRCHWOOD HILLS INC IA190 138 154 | Credit | USD | 17,00,000 |

| 2/23/2006 | INCOMING PAYMENT: SUNCOAST VALLEY INC; DEBIT:11003130001 CREDIT:11381540007 SUNCOAST VALLEY INC IA90 138 154 | Credit | USD | 17,00,000 |

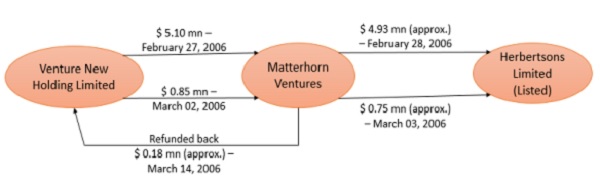

| 2/27/2006 | OUTGOING PAYMENT: BEING SUBSCRIPTION FOR ZINALROTHORN; DEBIT:11381540007 CREDIT:11390140008 ONE OF OUR CLIENT MATTERHORN VENTURES SPC BEING SUBSCRIPTION FOR ZINALROTHORN | Debit | USD | –

51,00,000 |

| 3/2/2006 | OUTGOING PAYMENT: BEING SUBSCRIPTION OF ZINALROTHORN SHARE CLASS; DEBIT:11381540007 CREDIT:11390140008 138 154 MATTERHORN VENTURES SPC BEING SUBSCRIPTION OF ZINALROTHORN SHARE CLASS | Debit | USD | -8,50,000 |

| 3/2/2006 | INCOMING PAYMENT: BAYSIDE ENTERPRISE INC; DEBIT:11003130001 CREDIT:11381540007 BAYSIDE ENTERPRISE INC IA90 138 154 | Credit | USD | 3,50,000 |

| 3/2/2006 | INCOMING PAYMENT: BIRCHWOOD HILLS INC; DEBIT:11003130001 CREDIT:11381540007 BIRCHWOOD HILLS INC IA190 138 154 | Credit | USD | 3,50,000 |

| 3/2/2006 | INCOMING PAYMENT: SUNCOAST VALLEY INC; DEBIT:11003130001 CREDIT:11381540007 SUNCOAST VALLEY INC IA90 138 154 | Credit | USD | 3,50,000 |

| 3/14/2006 | INCOMING PAYMENT: REDEMPTION IN ZINALROTHORN; DEBIT:11390140008 CREDIT:11381540007 | Credit | USD | 1,77,465.

70 |

| 3/22/2006 | OUTGOING PAYMENT: HIGHLAND TRADING; DEBIT:11381540007 CREDIT:11003130001 VENTURE NEW HOLDING LTD HIGHLAND TRADING UBS AG LONDON (LONDON BRANCH) | Debit | USD | -50,000.00 |

| 3/1/2007 | OUTGOING PAYMENT: HIGHLAND TRADING; DEBIT:11381540007 CREDIT:11003130001 VENTURE NEW HOLDING LTD HIGHLAND TRADING UBS AG LONDON (LONDON BRANCH) | Debit | USD | -3,00,000 |

| 7/23/2007 | OUTGOING PAYMENT: BAYSIDE INC; DEBIT:11381540007 CREDIT:11003130001 VENTURE NEW HLDG LTD NO. 1009156 BAYSIDE INC UBS AG LONDON (LONDONBRANCH) | Debit | USD | -20,50,000 |

| 7/23/2007 | OUTGOING PAYMENT: BIRCHWOOD HILLS;DEBIT:11381540007 CREDIT:11003130001 VENTURE NEW HLDG

LTD NO. 1009156 BIRCHWOOD HILLS UBS AG LONDON(LONDON BRANCH) |

Debit | USD | -20,50,000 |

| 7/23/2007 | OUTGOING PAYMENT: HIGHLAND TRADING; DEBIT:11381540007 CREDIT:11003130001 VENTURE NEW HLDG LTD NO. 1009156 HIGHLAND TRADING UBS AG LONDON (LONDON BRANCH) | Debit | USD | -25,50,000 |

| 7/23/2007 | OUTGOING PAYMENT: SUNCOAST VALLEY;DEBIT:11381540007 CREDIT:11003130001 VENTURE NEW HLDG LTD NO. 1009156 SUNCOAST VALLEY UBS AG LONDON(LONDON BRANCH) | Debit | USD | -20,50,000 |

| 8/1/2007 | OUTGOING PAYMENT: HIGHLAND TRADING; DEBIT:11381540007 CREDIT:11003130001 VENTURE NEW HLDG LTD NO. 1009156 HIGHLAND TRADING UBS AG LONDON (LONDON BRANCH) | Debit | USD | -9,50,000 |

| 9/7/2007 | OUTGOING PAYMENT: MATTERHORN VENTURES SPC; DEBIT:11381540007 CREDIT:11003130001 VENTURE NEW HLDG LTD NO. 1009156 MATTERHORN VENTURES SPCREMITTANCE DEUTSCHE BANK (MAURITIUS) LTD PORT LOUIS | Debit | USD | -21,00,000 |

| 8/14/2008 | INCOMING PAYMENT: CONTINENTAL ADMINISTRATION; DEBIT:11835920002 CREDIT:11381540007 CONTINENTAL ADMINISTRATION SERVICES LTD. 138 154 | Credit | USD | 1,23,67,0

00 |

33. From the analysis of the transactions appearing in the above statements, the following is noted:

33.1 Amount of $ 2,050,000 was received in the bank account of VNHL each, from Bayside, Birchwood and Suncoast as under:

> Amount of $ 1,700,000 was received from each of the above named three entities on February 23, 2006

> Another amount of $350,000 was received from each of above named three entities on March 02, 2006

Accordingly, a total amount of $ 6,150,000 was received in the account of VNHL from the above named three entities of which the Noticee was the beneficial owner.

33.2 Further, out of $ 6,150,000 received from these entities, an amount of $ 5,950,000 was transferred to Matterhorn Ventures SPC (Account no. 11390140008) for subscription to Zinalrothorn Share Class as under:

| Date of transfer | Amount of transfer |

| February 27, 2006 | $ 5,100,000 |

| March 02, 2006 | $ 850,000 |

33.3 Further, an incoming payment of $177,466 on March 14, 2006 was received from Matterhorn Ventures in the account of VNHL.

34. In view of the above, the fund flow between the Noticee to the various overseas entities in which the Noticee was the ultimate beneficial owner is displayed pictorially as under:

35. I note that during the investigation period, Matterhorn was a SEBI registered sub-account of FII – Matterhorn Advisory Singapore Pte Ltd with Code – 2000975 and had traded in the scrip of USL. An analysis of the transactions undertaken by Matterhorn in the scrip of USL during the period January 01, 2006 to December 31, 2008, as provided by the Custodian, ICICI Bank, revealed that Matterhorn had acquired 9,50,000 shares of Herbertsons through block deals in the following manner:

| DEAL DATE |

CLIENT NAME | DEAL TYPE | QUANTITY | PRICE (INR) | AMT (INR) (Mn) |

AMT (USD) (Mn)* |

| 28-Feb-06 | Matterhorn Ventures | Buy | 8,29,900 | 263.35 | 21,85,54,165 | 4.93 |

| Phipson Distillery Ltd |

Sell | 3,73,000 | 263.35 | 9,82,29,550 | ||

| McDowell Co. Ltd | Sell | 4,56,900 | 263.35 | 12,03,24,615 | ||

| 03-Mar-06 | Matterhorn Ventures | Buy | 1,20,100 | 275 | 3,30,27,500 | 0.75 |

| Phipson Distillery Ltd |

Sell | 1,20,100 | 275 | 3,30,27,500 | ||

| Total Buy/Sell | 9,50,000 | 25,15,81,665 | 5.68 | |||

+ Source: https://www.poundsterlinglive.com/bank-of-england-spot/historical-spot-exchange-rates/usd/USD-to-INR-2006

+ Conversions in USD are made considering exchange rate for the dates Feb 28, 2006 and Mar 03, 2006

36. Furthermore, from the fund flow in the bank accounts of related / associated entities of the Noticee and the examination during the investigation, I note that the said shares of Herbertson were purchased by Matterhorn immediately on the very next day from the date the funds were transferred by VNHL to Matterhorn. The fund transferred / received to / from Matterhorn Ventures SPC by VNHL is displayed as under:

| Transaction Booking Date |

Particulars | Credit/ Debit |

Local Ccy | Base Amount(USD) |

| 2/27/2006 | OUTGOING PAYMENT: BEING SUBSCRIPTION FOR ZINALROTHORN; DEBIT:11381540007 CREDIT:11390140008 ONE OF OUR CLIENT MATTERHORN VENTURES SPC BEING SUBSCRIPTION FOR ZINALROTHORN | Debit | USD | -51,00,000 |

| 3/2/2006 | OUTGOING PAYMENT: BEING SUBSCRIPTION OF ZINALROTHORN SHARE CLASS; DEBIT:11381540007 CREDIT:11390140008 138 154 MATTERHORN VENTURES SPC BEING SUBSCRIPTION OF ZINALROTHORN SHARE CLASS | Debit | USD | -8,50,000 |

| 3/14/2006 | INCOMING PAYMENT: REDEMPTION IN ZINALROTHORN; DEBIT:11390140008 CREDIT:11381540007 | Credit | USD | 1,77,465.70 |

| 9/7/2007 | OUTGOING PAYMENT: MATTERHORN VENTURES SPC; DEBIT:11381540007 CREDIT:11003130001 VENTURE NEW HLDG LTD NO. 1009156 MATTERHORN VENTURES SPCREMITTANCE DEUTSCHE BANK (MAURITIUS) LTD PORT LOUIS | Debit | USD | -21,00,000 |

37. The fund flow, along with the dates, is as shown below:

38. I further note from the material on record that the shareholding pattern of Herbertsons for the quarter ending December 31, 2005 on BSE website displayed Phipson Distillery Ltd (“Phipson”), McDowell & Company Ltd (“McDowell”) and UBHL as Indian Promoters of Herbertsons holding 53,49,775 shares (56.18%), 4,59,809 shares (4.83%) and 22,46,756 (23.59%), respectively. In addition, Phipson was found to be a Wholly Owned subsidiary of McDowell and Herbertsons was found to be a subsidiary of Phipson. The pictorial representation of the shareholdings is as under:

39. I note that the shareholding of McDowell and Phipson was partially transferred to Matterhorn through block deals on February 28, 2006 and March 03, 2006 and post these transfers of shares, Matterhorn was shown as a Non-Promoter Holding under subsection of FIIs in the Shareholding Pattern of Herbertsons as on March 31, 2006. Post-merger of Herbertsons with McDowell (merger effective from July 01, 2005), Matterhorn was allotted 6,33,333 shares of USL in exchange to 9,50,000 shares of Herbertsons in the ratio of 2:3 on October 27, 2006. McDowell was later renamed as USL on October 17, 2006.

40. Furthermore, in addition to the email communication mentioned in the preceding paragraph no. 28 above, FCA, vide letter dated January 15, 2018, had provided some more email communications between the Noticee and Jaspreet Ahuja in the same mail trail with the same subject line. Some of the relevant correspondence between the Noticee and Jaspreet Ahuja in email/s dated May 25, 2007 is as under:

Vijay Mallya – “Is the net gain of $ 5.51 mio after paying ALL loans?” Jaspreet Ahuja – “Only the gain on the sale to date is 5.51 $ and the loan taken was 6.15 $”

Vijay Mallya – “So Jazzy what’s the net gain after paying back ‘ALL’ UBS loans (for share acquisition + US property and anything else)?”

Jaspreet Ahuja – “Boss that I’ll tell you on Tuesday – I took only the loans pertaining to the kids into the account.

From memory there was a $ 3.4 mn loan on personal account – there was an additional loan of $ 1 mn for the US property and there was $ 6.15 minute for the kids. I am using the present sale proceeds to pay down the loans.

The stock seems to be finding its levels between 1100 and 1200 – which is a very good sign of consolidation. If there is no immediate news driver we could look to sell some more at the 1200 + levels – in my view….”

41. From the analysis of the above email communication between Jaspreet Ahuja and the Noticee, it is noted that a net gain of $5.51 Million was made by the Noticee from the purchase and sale of the shares of USL. Upon calculating the profits based on the purchase / sale of shares of USL, I find that a profit of $5.69 million was made till the date of the said email communication i.e. May 2007. The table showing the profit calculation is as under:

Company |

Date when the trade was executed and were settled (Please indicate separate date) |

Type Of Trans action |

Buy/ Sale |

Cr/ Dr |

Quant ity |

Amt (INR) |

Excha nge Rate |

Conve rsion Date |

Amt. (INR) |

Amt. (USD) |

|

Trade Date |

Settled

|

||||||||||

HERBE RTSONS LTD |

28/02/2006 |

02/03 /2006 |

Clearing House Trade |

Buy |

Cr |

829, 900 |

218,554, 165 |

44.29 |

28-Feb-06 |

218, 554,165 |

4,934, 617 |

HERBERT SONS LTD |

03/03/ 2006 |

07/03 /2006 |

Clearing House Trade |

Buy |

Cr |

120, 100 |

33,027 ,500 |

44.11 |

03-Mar-06 |

33,02 7,500 |

748, 838 |

HERBE RTSONS LTD |

27/10/ 2006 |

08/12/ 2006 |

Corporate action Event – Merger Debit |

– |

Dr |

950, 000 |

– |

251,58 1,665 |

5,683, 455 |

||

UNITED SPIRITS LTD |

27/10/ 2 006 |

08/12 /2006 |

Corporate action Event – Merger Credit |

– |

Cr |

633, 333 |

– |

||||

UNITED SPIRITS LTD |

25/01/2 007 |

31/01/ 2007 |

Clearing House Trade |

Sale |

Dr |

684 |

613 ,620 |

44.08 |

31-Jan-07 |

613, 620 |

13,921 |

UNITED SPIRITS LTD |

25/01/ 2007 |

31/01/ 2007 |

Clearing House Trade |

Sale |

Dr |

844 |

757,553 |

44.08 |

31-Jan-07 |

757 ,553 |

17,186 |

UNITED SPIRITS LTD |

29/01/ 2007 |

01/02/ 2007 |

Clearing House Trade |

Sale |

Dr |

71, 529 |

64,206 ,870 |

44.02 |

01-Feb-07 |

64,206 ,870 |

1,458 ,584 |

UNITED SPIRITS LTD |

29/01 /2007 |

01/02/2 007 |

Clearing House Trade |

Sale |

Dr |

22 ,490 |

20,183,079 |

44.02 |

01-Feb-07 |

20,18 3,079 |

458 ,498 |

UNITED SPIRITS LTD |

31/01/ 2007 |

02/02/ 2007 |

Clearing House Trade |

Sale |

Dr |

12 ,000 |

10,769 ,574 |

44.01 |

02-Feb-07 |

10,76 9,574 |

244 ,707 |

UNITED SPIRITS LTD |

31/01/2 007 |

02/02 /2007 |

Clearing House Trade |

Sale |

Dr |

50 ,786 |

45,574 ,114 |

44.01 |

02-Feb-07 |

45,57 4,114 |

1,035 ,540 |

UNITED SPIRITS LTD |

15/05 /2007 |

17/05/ 2007 |

Clearing House Trade |

Sale |

Dr |

5, 040 |

4,282 ,155 |

40.61 |

17-May-07 |

4,28 2,155 |

105 ,446 |

UNITED SPIRITS LTD |

15/05 /2007 |

17/05/ 2007 |

Clearing House Trade |

Sale |

Dr |

17,767 |

15,090 ,656 |

40.61 |

17-May-07 |

15,090 ,656 |

371, 600 |

UNITED SPIRITS LTD |

16/05/ 2007 |

18/05/ 2007 |

Clearing House Trade |

Sale |

Dr |

40 ,193 |

35,274 ,536 |

40.38 |

18-May-07 |

35,274 ,536 |

873, 565 |

UNITED SPIRITS LTD |

16/05/ 2007 |

18/05 /2007 |

Clearing House Trade |

Sale |

Dr |

62,000 |

54,420 ,419 |

40.38 |

18-May-07 |

54,42 0,419 |

1,347 ,707 |

UNITED SPIRITS LTD |

18/05/2 007 |

22/05/ 2007 |

Clearing House Trade |

Sale |

Dr |

41,150 |

45,326 ,258 |

40.15 |

22-May-07 |

45,32 6,258 |

1,128 ,923 |

UNITED |

18/05/ 2007 |

22/05 /2007 |

Clearing |

Sale |

Dr |

83,850 |

92,335 ,353 |

40.15 |

22-May-07 |

92,335 ,353 |

2,299 ,760 |

SPIRITS LTD |

House |

||||||||||

Trade |

|||||||||||

–

| Sale Value for 408333 shares | USD 9,355,436 |

| Buy Value for 408333 shares * | USD 3,664,331 |

| Net Gain till May 25′ 07 | USD 5,691,104 |

Notes:

1. Conversion Rate’s Source: https://www.poundsterlinglive.com/bank-of-england-spot/historical-spot-exchange-rates/usd/USD-to-INR-2006

2. Conversions in USD are made considering exchange rate for the ‘Trade Date’ in case of ‘Buy’ transactions and ‘Settled Date’ in case of ‘Sale’ transaction.

3. Buy Value for 408333 shares has been calculated proportionately using Total Cost of 950,000 shares of Herebertsons converted into 633,333 shares of USL (i.e., 5683455/633333 * 408333)

42. The abovementioned details of purchase and sale of shares of USL and the profits made by executing the said trades further substantiates that the email correspondence between the Noticee and the employee of UBS viz. Jaspreet Ahuja dated May 24, 2007 and May 25, 2007 was with respect to the trades in the shares of USL.

43. From the foregoing, I find that the email communication between the Noticee with one of the employees of UBS viz. Jaspreet Ahuja clearly reveals the reference being made to the trades executed in the scrip of USL by using the bank accounts held by the Noticee and his related entities with UBS. The Price volume data for USL as on May 24, 2007 further substantiates the same. I find that, in order to trade in the shares of USL and Herbertson, the Noticee devised a scheme of opening multiple accounts in various names with UBS including the names of Bayside, Suncoast, Birchwood, etc. of which the Noticee was the ultimate Beneficial owner. These three entities had transferred a total amount of $6.15 mn to VNHL whose Beneficial owner was again the Noticee. Later, VNHL further transferred this amount onward to Matterhorn Ventures for subscription to one of its share classes. Matterhorn Ventures (SEBI Code 2000975) was found to be a registered sub-account of an FII – Matterhorn Advisory Singapore Pte Ltd. that operated during investigation period. I further find that from the amount transferred by VNHL to Matterhorn (which was routed through the Noticees using overseas accounts of certain entities owned by the Noticee), Matterhorn had immediately purchased the shares of Herbertsons, a company listed in India at the relevant time, which was promoted and controlled by the Noticee. Further, Matterhorn had acquired 9,50,000 shares in Herbertsons on February 28, 2006 and March 03, 2006 through block deals as mentioned in preceding paragraph no. 39. Subsequently, pursuant to merger of Herbertsons with USL, Matterhorn Ventures was allotted 6,33,333 shares of USL in exchange to 9,50,000 shares of Herbertsons in the ratio of 2:3 on October 27, 2006.

44. From the fund flow between the entities, all owned and controlled by the Noticee along with the email correspondence between the Noticee and the employee of UBS, I find that the Noticee had indirectly used the sub-account of the FII i.e. Matterhorn Ventures as an investment vehicle to indirectly trade in the scrips of his own group companies in India i.e. Herbertsons and USL by way of funding the said FII.

45. I find that SEBI (Foreign Institutional Investors) Regulations, 1995 (“FII Regulations”) prescribes registration and regulation of the activities of FIIs, various investment conditions and restrictions applicable to the FIIs, the ‘code’ of conduct to be observed by them while participating in the Indian Securities Market and other matters connected therewith. In terms of Regulation 2(1)(f) of the FII Regulations, ‘Foreign Institutional Investor’ means an institution established or incorporated outside India which proposes to make investment in India in securities. Further, in terms of Regulation 2(1)(k) of the FII Regulations, ‘sub-account’ includes foreign corporates or foreign individuals and those institutions, established or incorporated outside India and those funds or portfolios, established outside India, whether incorporated or not, on whose behalf investments are proposed to be made in India by a foreign Institutional Investor. Accordingly, FIIs are institutions which are incorporated outside India and which propose to make investments in the Indian securities market on behalf of sub-account, who are also established or incorporated outside India.

46. Further, on perusal of Regulation 15A(1) of the FII Regulations, I find that the said provision states that no FII may issue, or otherwise deal in off shore derivative instruments (ODIs), directly or indirectly, unless such ODIs are issued only to persons who are regulated by an appropriate foreign regulatory authority and such ODIs are issued after compliance with ‘know your client’ norms. Therefore, the FII Regulations govern only such aspects of the investments made through FIIs which are made only on behalf of sub-accounts who are resident outside India or issue ODIs to persons in a foreign territory who are regulated by an appropriate regulatory authority. Thus, I note that the FII Regulations and the framework around it were made for orderly channelization of foreign investments into India. Therefore, the FII Regulations are not meant to serve as a conduit for Indian entities to invest or reinvest in India by using their bank accounts held with overseas accounts or by using their capital stashed abroad.

47. It is, however, noted from the modus operandi adopted by the Noticee in the instant case that this financial route i.e. the FII route was used by the Noticee to trade in the Indian Securities market by concealing his identity by way of layering the transactions in the names of various overseas registered entities and opening accounts in their names in UBS-UK Bank, even though the Noticee himself was the actual beneficial owner of each of these front entities. I find that as the investments through the FII route are only meant for persons /entities resident outside India to facilitate them to have an exposure in the Indian securities market, from the scheme devised by the Noticee, it is clearly established that the Noticee has, by way of a design, abused the FII mechanism /route for investing his surplus funds kept abroad and had not revealed the same to the investors of these companies in India. I, therefore, find that the Noticee has glaringly resorted to making investments through the FII route by masking his identity under the garb of an FII i.e. Matterhorn Ventures to the detriment of the interest of shareholders of Indian companies.

48. Here, reliance is placed on the judgement of the Hon’ble Supreme Court in the case of Securities and Exchange Board of India Vs. Kanaiyalal Baldevbhai Patel (2017) 15 SCC 1, wherein the Hon’ble Apex Court, made an attempt to elucidate the meaning of the term ‘unfair trade practice’ and observed that,

“Broadly trade practice is unfair if the conduct undermines the ethical standards and good faith dealings between parties engaged in business transactions. It is to be noted that unfair trade practices are not subject to a single definition; rather it requires adjudication on case to case basis. Whether an act or practice is unfair is to be determined by all the facts and circumstances surrounding the transaction. In the context of this regulation a trade practice may be unfair, if the conduct undermines the good faith dealings involved in the transaction. Moreover, the concept of ‘unfairness’ appears to be broader than and includes the concept of deception or fraud.”

49. Further, the Hon’ble Supreme Court in the judgement of Kanaiyalal Baldevbhai Patel (supra), went ahead and observed that,

“14. To attract the rigor of Regulations 3 and 4 of the 2003 Regulations, mens rea is not an indispensable requirement and the correct test is one of preponderance of probabilities. Merely because the operation of the aforesaid two provisions of the 2003 Regulations invite penal consequences on the defaulters, proof beyond reasonable doubt as held by this Court in Securities and Exchange Board of India Vs. Kishore R. Ajmera (supra) is not an indispensable requirement. The inferential conclusion from the proved and admitted facts, so long the same are reasonable and can be legitimately arrived at on a consideration of totality of the materials, would be permissible and legally justified.”

50. In addition, attention is also drawn on the observations of the Hon’ble Supreme Court in the case of Narayanan Vs. Adjudicating Officer, Securities and Exchange Board of India (2013) 12 SCC 152, wherein, the Hon’ble Apex Court, while stressing upon the importance of prevention of market abuse and prevention of market integrity, stated that,

“35. Prevention of market abuse and preservation of market integrity is the hallmark of Securities Law. Section 12A read with Regulations 3 and 4 of the Regulations 2003 essentially intended to preserve ‘market integrity’ and to prevent ‘Market abuse’……. .

Securities market is based on free and open access to information, the integrity of the market is predicated on the quality and the manner on which it is made available to market. ‘Market abuse’ impairs economic growth and erodes investor’s confidence. Market abuse refers to the use of manipulative and deceptive devices, giving out incorrect or misleading information, so as to encourage investors to jump into conclusions, on wrong premises, which is known to be wrong to the abusers.”

51. In view of the above, after considering the totality of the facts and material available, I, without any hesitation, find that the said acts of the Noticee in abusing the framework of the FII Regulations and dealing in securities of listed companies of his group of companies in India, indirectly, in a fraudulent manner and by employing a manipulative and deceptive artifice, thereby, indulging in purchase and sale of securities of Herbertsons / USL clearly was detrimental to the investors at large and was with an intention to deceit the market players in violation of the provisions of Regulation 3(a), (b) and (d) of the PFUTP Regulations, 2003 and Section 12A(a) and 12A(c) of SEBI Act, 1992.

52. I further find from the shareholding pattern of Herbertson available on the BSE website for the quarter ending December 31, 2005 that Phipson, McDowell and UBHL were shown as Indian Promoters of Herbertsons holding 53,49,775 shares (56.18%), 4,59,809 shares (4.83%) and 22,46,756 (23.59%), respectively. As already mentioned in the preceding paragraph no. 38 and 39, Phipson was wholly owned subsidiary of McDowell and Herbertsons was subsidiary of Phipson. Thus, I find that all the said companies were belonging to the same group i.e. UB group of which the Noticee was the Chairman. These shares of Herbertsons were partially transferred to Matterhorn through block deals dated February 28, 2006 and March 03, 2006. Post such transfer of shares, Matterhorn Ventures was shown as a Non-Promoter Public Shareholder under sub-section of ‘FIIs’ in Shareholding Pattern of Herbertsons as on March 31, 2006. As already found in the above paragraphs, the entire transaction in the shares of Herbertsons and USL was funded by the Noticee, indirectly, through VNHL by routing funds through overseas bank accounts and therefore, the shareholding of Matterhorn Ventures of 9.98% shares of Herbertsons actually belonged to the promoter category being totally funded by the Noticee. In view of the same, I find and conclude that the Noticee indeed had misrepresented the truth and concealed a material fact known to him that the shareholding shown in the name of Matterhorn actually belonged to the promoter category as the same was totally funded by the Noticee thereby, violating the provisions of Regulation 4(2)(f) of the PFUTP Regulations, 2003.

53. I note that Section 11 of the SEBI Act, 1992 confers a duty on the Board to protect the interests of investors in securities and to promote the development of and to regulate the securities market. The said objectives are all interlinked. In order to develop the securities market, it is necessary that the interest of investors is protected. Any manipulation in the market would impact the interest of investors adversely. The existence of manipulative practices would result in loss of trust of these investors in the Indian securities market impacting market integrity. In view of the same, a robust securities market is important for the growth and development of the economy. Thus, it is important that market is regulated and steps are taken to discourage any manipulation or wrong practice in order to protect the interest of investors, keep the trust of the investors intact as well as to develop the securities market. To achieve the objectives of the SEBI Act, 1992, SEBI, as a market regulator, is entrusted under the statute to take such measures as it deems fit. Thus, the power to take all measures, as may be necessary, to discharge its duty under the statute has been conferred in widest amplitude. Pursuant to the said objective, PFUTP Regulations, 2003 have been formulated with the main objective of preventing fraudulent activities in order to boost investor confidence in the securities market and to provide an environment conducive to increased participation and investment in the securities market.

54. I find that the Noticee, in the instant case, has devised a scheme to indirectly trade in the shares of his own group companies through layered transactions / fund flow using his overseas related companies through FII route in order to keep his identity masked and trade in the Indian Securities market in defiance of the regulatory norms. Such acts of the Noticee are not only fraudulent and deceptive but are a threat to the integrity of the securities market. I further note that earlier, vide order dated June 01, 2018, the WTM, SEBI had debarred the Noticee from accessing the securities market and prohibited him from buying, selling or otherwise dealing in the securities in any manner for a period of 3 years from the date of the said order (e. from June 01, 2018 till May 31, 2021) for manipulative activities such as diversion of funds and / or improper transactions in the scrip of USL in violation of the PFUTP Regulations, 2003 read with the SEBI Act, 1992 Further, vide the said order, SEBI had also restrained the Noticee from holding a position as Director or Key Managerial Person of a listed Company for a period of 5 years from the date of the said order (i.e. from June 01, 2018 till March 31, 2023). I further find that the said order was challenged before the Hon’ble SAT, which later was dismissed due to want of prosecution which ultimately resulted in attainment of finality of the directions issued by the WTM, SEBI in the order dated June 01, 2018. Thus, I find that the Noticee has been indulging in manipulative and fraudulent activities and indulging in unfair trade practices while dealing in the securities market in violation of the securities laws.

55. In view of the aforesaid findings, I find that appropriate directions under Section 11B read with Section 11(1) of the SEBI Act, 1992 in order to protect the market integrity and deter such activities from the markets would meet the ends of justice.

ORDER AND DIRECTIONS

56. In view of the foregoing observations and findings, I, in exercise of the powers conferred upon me under Section 11(1) and 11B read with Section 19 of the SEBI Act, 1992, hereby direct the following: