LTIMindtree Limited Vs ACIT (ITAT Mumbai)

ITAT Mumbai held that TPO was correct in concluding that the rate at which loan is taken by the Appellant cannot be taken as internal CUP to benchmark the loan given by the Appellant to its AE as there is a difference in credit rating of the Appellant and its AE.

Facts- The case of the Appellant was selected for scrutiny and notice under Section 143(2) of the Act was issued. During the assessment proceedings, AO noted that the Appellant has entered into the international transactions with its Associated Enterprises (AEs) and therefore, reference was made to Transfer Pricing Officer (TPO) u/s. 92CA(1) of the Act.

It was also observed that the revenue earned from onsite services provided by the Appellant cannot be considered as export of software from India derived from STPI Units located in India. Therefore, proposed disallowance of 53.40% of the deduction claimed by the Appellant u/s. 10A of the Act in proportion of Software Development Expenses plus Administration & Another Expenses incurred by the Appellant outside India aggregating to INR 871,75,78,841/- and the total Software Development Expenses plus Administration & Another Expenses incurred by the Appellant aggregating to INR 1632,29,65,745/- and computed the amount of disallowance

On the basis of the above directions issued by the DRP, the Assessing Officer passed the Final Assessment Order, dated 15.01.2014, at assessed income of INR 205,26,28,060/- after (a) making Transfer Pricing Addition of INR 2,72,430/-, (b) making proportionate disallowance of INR 172,94,09,811/- out of deduction of INR 263,04,15,538/- claimed by the Appellant under Section 10A of the Act in the Return of Income.

Conclusion- We find that the Appellant has adopted the rate of interest on which funds were borrowed by the Appellant as internal CUP to benchmark interest rate on which funds were given to the subsidiary. In our view, TPO was correct in concluding that the rate at which loan is taken by the Appellant cannot be taken as internal CUP to benchmark the loan given by the Appellant to its AE. In the facts of the present case, it cannot be disputed that there is a difference in credit rating of the Appellant and its AE. In our view, the same would impact the rate at lending to the Appellant/AE. Accordingly, we confirm the rejection of internal CUP as adopted by the Appellant for benchmarking the international transaction under consideration.

Held that for the Assessment Year 2009-10 deduction claimed by the Appellant under Section 10A of the Act in respect of revenue from onsite services cannot be denied on the ground that the onsite services are not connected to the eligible units located in India.

FULL TEXT OF THE ORDER OF ITAT MUMBAI

1. The present appeal is directed against the Assessment Order dated, 15/01/2014, passed under Section 143(3) read with Section 144C(13) of the Income Tax Act, 1961 [hereinafter referred to as „the Act’], as per directions, dated 31/12/2013, issued by the Dispute Resolution Panel-III, Mumbai (hereinafter referred to as „the DRP’) under Section 144C(5) of the Act while disposing Objection Number 161 pertaining to Assessment Year 2009-10.

2. The Grounds of Appeal raised by the Assessee are as under:

1. “On the fats and in the circumstances of the case and in law, the learned Assessing Officer, relying on the direction of Dispute Resolution Panel – III, Mumbai [“DRP”], erred in making addition of Rs. 2,72,430/- by way of adjustment to the transfer price of the international transaction entered in to by the appellant with its associated enterprise by invoking the provisions of Section 92CA(3) of the Act.

2. On the facts and in the circumstances of the case and in law, the learned Assessing Officer, relying on the direction of DRP, erred in treating the onsite software development services as “supply of manpower” and “body shopping” and not as “export of software” so as to reduce the claim of the appellant under Section 10A of the Act by Rs. 172,94,09,811/-.

3. Without prejudice to Ground no.2, on the facts and in the circumstances of the case and in law, the learned Assessing Officer, relying on the direction of DRP, erred in adopting the proportion of software development costs incurred outside India to quantify and disallow the claim attributable to “supply of manpower” / “body shopping” as aforesaid.

4. Without prejudice to Ground no. 2 and 3, on the facts and the circumstances of the case and in law, the learned Assessing Officer, relying on the direction of DRP, erred in holding that the onsite software development services rendered by the appellant to its customers do not form part of exports of the Undertaking comprised in the Software Technology Park Units (“STPI Units”) and on that basis holding that in any case the deduction under Section 10A needed to be recomputed and reduced to Rs. 151,70,24,446/-.

5. Without prejudice to Ground no. 2, 3 and 4, of the facts and in the circumstances of the case and in law, the learned Assessing Officer, relying on the direction of DRP, erred in holding that communication charges of Rs. 9,27,34,738/-incurred in Indian Rupees and expenditure in foreign currency of Rs. 8,82,15,41,969/- are liable to be excluded from the export turnover for the purpose of computing the deduction under Section 10A of the Act.

6. The appellant company craves leave to add, to, to amend, to alter or modify any or all the aforesaid grounds of appeal.”

3. The Appellant has also raised the following additional ground of appeal vide letter, dated 23/06/2017:

1. “Without prejudice to grounds 2 and 3, on the facts and in the circumstances of the case and in law, the Assessing Officer be directed to adopt actual profitability of onsite work instead of determining the profit by adopting the proportion of software development cost incurred outside India for calculation of disallowance u/s 10A attributable to “supply of manpower”/”body shopping” and also grant DIT relief of Rs. 11,52,25,628/- in respect of the same.”

4. The relevant facts in brief are that the assessee filed return of income for the Assessment Year 2009-10 on 26.09.2010 declaring total income of INR 30,25,87,218/- under normal provisions of the Act which was revised on 29.03.2011. In the revised return of income, the Appellant declared total income of INR 32,29,45,823/-under normal provision of the Act. The case of the Appellant was selected for scrutiny and noticed under Section 143(2) of the Act was issued.

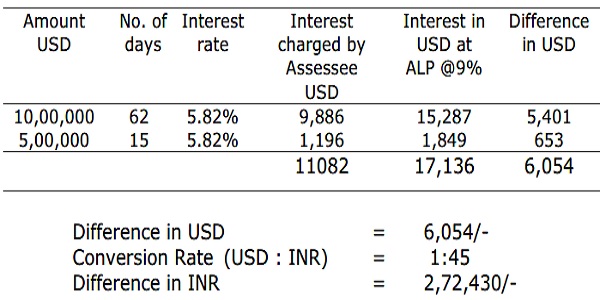

5. During the assessment proceedings, the Assessing Officer noted that the Appellant has entered into the international transactions with its Associated Enterprises (AEs) and therefore, reference was made to the Transfer Pricing Officer (“in short TPO”) under Section 92CA(1) of the Act on 21.09.2010. The TPO, vide order, dated 26.12.2012 passed under Section 92CA(3) of the Act, proposed transfer pricing adjustment to INR 2,72,430/- in respect of interest received by the Appellant on loan advanced by the Appellant to its AE. The above transfer pricing adjustments were incorporated in the Draft Assessment Order, dated 28.03.2013.

6. In the Draft Assessment Order, the Assessing Officer also proposed disallowance of INR 172,94,09,811/- out of aggregate deduction of INR 263,04,15,538/- claimed by the Appellant under Section 10A of the Act on the ground that the Appellant was engaged in providing services which were in the nature „Body Shopping‟ as opposed to export of software as contended by the Appellant. The Assessing Officer, without prejudice to the aforesaid disallowance of deduction under Section 10A of the Act, observed even if the Appellant is considered to be engaged in the business of export of software, the revenue earned from onsite services provided by the Appellant cannot be considered as export of software from India derived from STPI Units located in India. Therefore, proposed disallowance of 53.40% of the deduction claimed by the Appellant under Section 10A of the Act in proportion of Software Development Expenses plus Administration & Another Expenses incurred by the Appellant outside India aggregating to INR 871,75,78,841/- and the total Software Development Expenses plus Administration & Another Expenses incurred by the Appellant aggregating to INR 1632,29,65,745/- and computed the amount of disallowance as under:

|

S.No. |

Particulars | Amount of Disallowance (INR) |

| 1 | Profit derived from overseas branches not considered as export services from India i.e. 53.40% of [Business Income of eligible units as per return Rs. 281,96,61,057 – Interest Income of Rs. 2,51,16,781 as below] |

149,22,86,643 |

| 2 | Interest income excluded from export profits | 2,51,16,781 |

| 3 | Depreciation allowed on software expenses treated as capital expenditure in earlier years | (3,78,978) |

| Total disallowance out of exemption claimed u/s 10A | 151,70,24,446 | |

In alternative and on without prejudice basis, the Assessing Officer concluded that in case the services provided by the Appellant are held to be in the nature of export of software derived from STPI Units located in India, then also a disallowance of INR 11,73,66,586/- was warranted out of deduction claimed by the Appellant under Section 10A of the Act in view of the following:

– The communication charges and other expenditure incurred in foreign currency were required to be excluded from the export turnover in view of provisions contend in Explanation 2(iv) to Section 10A of the Act.

– interest income of INR 2,51,16,781/- was required to be excluded from the profits of undertaking while computing deduction under Section 10A of the Act, depreciation of INR 3,78,978/-

– Additional depreciation of INR 3,78,978/- was to be allowed in view of the fact that the software expenditure was treated as capital expenditure in Assessment Years 1998-99, 2001-02 & 2002-03.

7. Thus, vide order dated 28.03.2013, the Assessing Officer proposed Transfer Pricing Adjustment of INR 2,72,430/- and disallowance of INR 172,94,09,811/- out of deduction claimed by the Appellant under Section 10A of the Act.

8. The Appellant filed objections against the Draft Assessment Order, dated 28.03.2013, before DRP. The DRP rejected the objections raised by the Appellant challenging Transfer Pricing Adjustment of INR 2,72,430/-. DRP also concluded that Assessing Officer was justified in denying proportionate deduction under Section 10A of the Act and making a disallowance of INR 172,94,09,811/-; and that communication expenses and other expenses incurred in foreign exchange are to be excluded from export turnover in terms of Explanation 2(iv) to Section 10A of the Act. DRP dismiss the objections relating to exclusion of interest income from the profits of the eligible business on the ground that the same were not pressed by the Appellant. Thus, the DRP rejected the objections raised by the Appellant vide, order dated 31.12.2013.

9. On the basis of the above directions issued by the DRP, the Assessing Officer passed the Final Assessment Order, dated 15.01.2014, at assessed income of INR 205,26,28,060/- after (a) making Transfer Pricing Addition of INR 2,72,430/-, (b) making proportionate disallowance of INR 172,94,09,811/- out of deduction of INR 263,04,15,538/- claimed by the Appellant under Section 10A of the Act in the Return of Income.

10. Being aggrieved, the Appellant is now in appeal before us challenging the Final Assessment Order, dated 15.01.2014, on the grounds reproduced in paragraph 2 above which are taken up hereinafter in seriatim.

Ground No. 1

11. Ground No.1 raised by the Appellant against the Transfer Pricing Addition of INR 2,72,430/-. The facts relevant to the adjudication of the aforesaid ground are that during the assessment proceeding the Transfer Pricing Officer noted that the Appellant had granted short-term loan of USD 1.5 million during the relevant previous year to its AE (i.e., GDA Technologies Inc., USA) for meeting its working capital requirements at the effective rate of 5.82%, being London Interbank Offer Rate’ (LIBOR) – 3 month maturity plus 400 Basis Points. The Appellant had benchmark the aforesaid loan transaction with the foreign currency secured loan taken by the Appellant from HSBC Bank and ABN Amro Bank during the same period. The aforesaid loans were taken by the Appellant with the spread over LIBOR ranging from 200 to 350 basis points. Since the loans given by the Appellant to AE were at the interest rate of LIBOR plus 400 Basis Points, it was contended by the Appellant that the aforesaid loan to the AE was at Arm’s length.

12. However, the TPO was not convinced and therefore, asked the Appellant vide order sheet entry, dated 04.12.2012, to show-cause why the rate of interest received on corporate bonds rated by CRISIL issued in India should not be applied. The Appellant, in response, submitted that the CRISIL based credit rated bonds issued in India carry interest rate in INR and therefore, cannot be used to benchmark loan given by the Appellant in USD. The Appellant had applied internal Comparable Uncontrolled Price (CUP), by taking interest charged on loan received by the Appellant on the basis of LIBOR rate which was internationally recognized rate for foreign currency transactions. On perusal of submission furnished by the Appellant the TPO noted that Appellant had raised funds at the average rate of 6.05% whereas it had advanced loans to AE at the average rate of 5.82% which was below the rate the Appellant itself had raised loans. The TPO rejected the internal CUP adopted by the Appellant on the ground that the rate at which the Appellant had borrowed funds cannot be taken as comparable with the rate at which the Appellant has granted loan on account of the difference in the credit rating of the Appellant and the AE. In order to support the aforesaid conclusion the TPO computed the credit rating of the Appellant and the AE by adopting interest coverage ratio and debt equity ratio to conclude that on account of difference in credit ratings the AE would not have been able to get loans at the same rate as the Appellant on account of comparatively lower credit rating of the AE. Thereafter, the TPO proceeded to examine the applicability of External CUP with AE as a tested party and cost plus method.

13. In order to locate External CUP the TPO found the corporate bond rates at which the AE could have borrowed funds as per the aforesaid credit rating determined by the TPO. Taking the 5 year corporate bond yield for bond rates in USA available in public domain till 01.01.2006, corresponding to the credit rating of the AE/Appellant, the TPO concluded that the Appellant would have been able to get loan at the interest rate of 5.03% whereas the AE would have got loan at the interest rate of 8.68%. Further, the AE would have also incurred expenses to raise bonds and had undertaken the risk of failure to raise funds in recessionary market. Similarly, taking the average yield of 5 year bonds for Financial Year 2008-09 obtained from CRISIL, corresponding to the credit rating of the Appellant/AE, the TPO concluded that the AE that the Appellant would have been able to get loan at the interest rate of 10.05% whereas the AE would have got loan at the interest rate of 17%. On the basis of the aforesaid, the TPO concluded that the rate of interest and the spread would defer from country to country. Therefore, the TPO increase the rate of interest of 6.05% at which the assessee had taken loan in USD in proportion to rate at which AE would have been able to borrow in India and the rate at which Appellant would have been have been able to borrow in India. Thus, computing the applicable rate as under:

6.05% x 17% = 10.23%

10.05%

In view of the above, the TPO proceeded to hold that the contention of the Appellant that the LIBOR rate is used for benchmarking of international transaction is not correct. As a LIBOR rate is determined by the rate at which borrow the funds which is different from the rate at which bank offers loan which depends upon fact as such as financial strength and credit rating of the borrower. Therefore, the rate at which the AE would get loan from the bank would not be same as the rate at which the Appellant would get the same loan. Therefore, in the case of the Appellant LIBOR + Method used by the Appellant would not qualify as a CUP.

14. Having concluded as above, the TPO applied Cost Plus Method to arrive at Arm‟s Length interest rate of 8.32%. According to the TPO the cost of borrowing to the Appellant was 6.05%. Since, the Appellant had not charged from the AE service/financial charges, to make the transaction comparable with the third party transaction the TPO thought it appropriate to add Net Interest Margin (NIM) being the measure of difference between the income generated by a bank & other financial institutions, and the amount of interest paid out to their lenders. The TPO computed the average NIM of 5 Indian banks at 2.28 %, and added the same to cost of borrowing to the Appellant, to arrive at the figure of 8.32%. Thereafter, taking into consideration the average of the US Corporate Bond Rate, Indian Corporate Bond Spread applied on LIBOR rate, and the LIBOR rate, the TPO determined the average rate of 9% as the reasonable arm’s length interest for the transaction and thus, proposed Transfer Pricing Adjustment of INR 2,72,430/- which was computed as under:

15. The above Transfer Pricing Adjustment was incorporated in the Draft Assessment Order against which Objections were filed by the Appellant before DRP. However, the DRP decline to interfere and the Assessing Officer pass the Final Assessment Order making transfer pricing addition of INR 2,72,430/-. Therefore, the Appellant is in appeal before us on this issue.

16. We have considered the submissions made by the Learned Senior Counsel appearing for the Appellant which can be summarized as follows. The contentions advanced on behalf of the Appellant were two fold. First, the TPO erred in rejecting the internal CUP adopted by the Appellant. Second, the TPO failed to apply any of the methods while arriving at the rate of 9% and holding the same should be Arm’s Length rate of interest. Without prejudice to the aforesaid, it was also contended on behalf of the Appellant that the Cost Plus Markup method has been applied by the TPO incorrectly. The Learned Senior Counsel took us through the relevant extracts of the order passed by the TPO and documents placed in the paper-book to support the aforesaid contentions and placed reliance on the judicial precedents.

17. Per contra, the Ld. Departmental Representative supported the Transfer Pricing Adjustment by placing reliance on the Transfer Pricing Order, dated 26.12.2012 and submitted that the TPO has made the detailed analysis while rejecting the internal CUP adopted by the Appellant and had rightly made adjustments to the base rate of 6.05% on which loan in USD was taken by the Appellant to make the same comparable with the loan taken by the AE. He submitted that the order passed by the TPO deserves to be upheld.

18. We have considered the rival submissions and perused the material on record including the judicial precedents cited by both the sides. In the case of Commissioner of Income Tax–I vs. M/s Cotton Naturals (I) Pvt. Ltd. : [2015] 231 Taxman 401 (Delhi)/ 276 CTR 445 (Delhi)[27-03-2015] cited on behalf of the Appellant, the Hon’ble Delhi High Court had rejected the comparability test applied by the Transfer Pricing Officer in that case. The Hon’ble Delhi High Court concluded that interest that would have earned by an assessee by advancing a loan to an unrelated party in India (with a similar financial health as its subsidiary) could not be used to benchmark the interest on loan granted by such assessee to the its aforesaid subsidiary outside India repayable in foreign currency. The currency in which the loan is re-paid normally determines the rate of interest. Therefore, it was held that there was no justification in applying PLR prevailing in India for outbound loan transaction where as Indian parent is giving loan to a foreign subsidiary. Reliance was also placed on behalf of the Appellant on judicial precedents where the transfer pricing officer had accepted CUP as the most appropriate method and applied PLR for determining the arm’s length rate of interest, and the Tribunal had rejected the aforesaid approach of the TPO. However, in the case before us we find that the facts are different to the extent that (a) the TPO has rejected internal CUP adopted by the Appellant as most appropriate method and (a) TPO has adopted Cost Plus Method, and for determining arm’s length interest rate in respect of outbound loan given by the Appellant to its subsidiary, the TPO has not adopted PLR but made adjustment to the rate of interest payable on foreign currency/USD loan taken by the Appellant.

19. We find that the Appellant has adopted the rate of interest on which funds were borrowed by the Appellant as internal CUP to benchmark interest rate on which funds were given to the subsidiary. In our view, TPO was correct in concluding that the rate at which loan is taken by the Appellant cannot be taken as internal CUP to benchmark the loan given by the Appellant to its AE. In the facts of the present case, it cannot be disputed that there is a difference in credit rating of the Appellant and its AE. In our view, the same would impact the rate at lending to the Appellant/AE. In this regard, it would be pertinent to refer to the following observations made by the Hon’ble Delhi High Court in the case of Cotton Naturals (I) Pvt. Ltd (supra):

“43. Normally there would be a difference between the lending rate and borrowing rate in each country. Some authors and writers suggest that the average or mid-point between the two should be taken. However, others like Klaus Vogel, have suggested that economic purpose and substance of the debt-claim or debt for which granting of credit calls for the lending rate would be determinative. Thus, in case of a capital investment, the borrowing rate will apply, whereas in case of credit allowed to a customer on sale of goods, the lending rate would apply. We do not deem it necessary to enter into this controversy and express our view as regards the same.

44. We are also not expressing any view on adjustment for lack of security as this issue does not arise for consideration in terms of the observations of the DRP.” (Emphasis Supplied)

20. Appreciating the difference in the lending and the borrowing rate the TPO had used NIM (i.e. Net Interest Margin) for making the adjustment. We note that the TPO was taken the interest rate of 6.05%, being the rate at which loan in USD was taken by the Appellant, as the base. However, while computing the amount of markup, the Appellant has taken the NIM of various banks without taking into consideration the currency in which borrowing/lending was done by such banks. Therefore, we find merit in the contention advance on behalf of the Appellant to the extent that the TPO has, in effect, adopted a hybrid method.

21. Accordingly, in view of the above, we confirm the rejection of internal CUP as adopted by the Appellant for benchmarking the international transaction under consideration. However, we remand the issue back to the file of Assessing Officer/TPO for adjudication afresh. During the course of hearing the Ld. Senior Counsel appearing for the Appellant had, relying upon „Statement showing cost of borrowing during the FY 2008-09’ placed at page 17 of the paper-book, submitted that the cost of borrowing was computed incorrectly at 6.05% by taking „Interest as per Annual Accounts‟ (i.e. INR 8,26,06,178/-) as the total interest cost whereas the actual cost of borrowing comes to around 3.18%. We direct the Assessing Officer to verify the claim of the Appellant and determine the cost of borrowing accordingly for the purpose of adjudication as aforesaid. In terms of the aforesaid, the issue remanded to the file of the Assessing Officer/TPO, and Ground No. 1 raised by the Appellant is partly allowed.

Ground No 2 & 3

22. Ground No. 2 & 3 pertain to the disallowance of INR 172,94,09,811/- out of deduction of INR 263,04,15,538/- claimed by the Appellant under Section 10A of the Act. In this regard, the Ld. Senior Counsel appearing for the Appellant vehemently contended that the Assessing Officer has failed to appreciate the business of the Appellant and by incorrectly appreciating the terms and conditions of one of the contracts entered into by the Appellant with its clients, the Assessing Officer has incorrectly concluded that the Appellant is engaged in the business of „Body Shopping‟. In this regard, he relied upon Note placed at Page 244 & 245 of the paper-book which reads as under:

“Larsen & Toubro Infotech Limited (LTIL) India is engaged in providing software development services to global clients in the areas of Financial Services, Manufacturing and Product Engineering Services (Telecom). LTIL India has software development centres at Mumbai (Powai and Navi Mumbai), Pune, Chennai, Bangalore and Mysore.

LTIL uses a mixed/hybrid model for providing Software Development Services, wherein, services are rendered both from offshore development centres in India and at onsite locations of the customers in various countries. Nearly 98% of customer contracts in terms of revenue are of this type containing both offshore and onsite software development projects. Very small proportion of contracts (i.e. only 2% of revenue), are in the nature of pure onsite contracts and these are in the nature of Software Development Projects for SAP/ERP Development & Implementation which are required to be executed at client site. Employees working onsite are under the supervision and control of the Project/Delivery Manager from LTIL India. E.g. contract with Mushrif Trading & Contracting Company is enclosed herewith for your reference.

Providing software services to overseas customers requires a combination of onsite services and offshore services. This is required for the following reasons: when a customer is transitioning the work from his IT team to outsourced vendor like us, detailed knowledge transfer is planned followed by scoping of work that needs to be done onsite as it requires proximity to customer and the work that can be offshored. Second, there is a need of certain technical staff to be onsite for better understanding of customer’s ongoing requirements and translating the same to the offshore team for cost effective and timely delivery of services to the customer. Third, in cases where certain software development services are required to be integrated with other systems at customer’s end, it requires interaction at customer site. Thus, onsite and offshore services are an integral part of software services delivery and are managed in a manner which ensures cost effective and timely execution. From customer’s viewpoint, the customer is interested in keeping the onsite requirement to the minimum considering the higher cost involved for onsite services.

The onsite as well as offshore employees work under the supervision and control of LTIL’S Engagement Manager/ Delivery Manager Project Manager. There are service level agreements on key parameters of service delivery such system up-time, response time, level of compliance to customer’s standards etc. and these are jointly delivered by the onsite and offshore teams.

LTIL has branch offices in various countries, through which ting is done to customers in both cases of Offshore and Onsite services provided to the customers.

This is done basically to comply with the local laws of the respective countries and ease of collection of service fees charged from customers in those specific countries in many countries, there are VAT/ GST regulations requiring un to charge the same to the clients which necessitate billing to be done in respective countries. We have been trying to get the customers to agree to enter into contract with India address and we have been able to achieve this for certain clients such as Chevron Texaco Inc, USA, Freescale Semiconductor Inc., USA, Motorola Inc., USA, Samsung Electronics, South Korea, etc. E.g. contract with Chevron is enclosed for your reference.

As regards contracts entered into with customers through overseas 15 branches, these branches are part of LTIL India organization only and operate as front-end offices of the company in various countries where customers are located. These front end offices are basically working as marketing arm of LTIL India. E.g. contract with Hitachi Ltd is enclosed herewith for your reference.

In certain cases, customer wants control of the data shared during software development projects, due to the confidentiality requirements. In some other cases, customers observe our capabilities and in the Initial phase, they require our professionals to be onsite and once we gain their trust, we are able to get work orders involving onsite and offshore work or some work orders which can be largely executed from offshore. E.g. contract with the Thales is enclosed for your reference.

From the above explanation of LTIL’s business model, it can be observed that in LTIL’S business model of providing software development services through a combination of onsite and offshore services, the onsite services are effectively connected with offshore services. Hence, the onsite services are not in the nature of “Manpower Supply” which is referred to as “Body Shopping”.

Even in case of the small proportion of 2% business which is done through onsite project development, the onsite activities are under the control and supervision of LTIL-India. E.g. contract with Mushrif Trading & Contracting Company as also enclosed above for your reference.

Hence we submit that LTIL India is eligible for exemption on its 100% export profits as it has complied with all the conditions required for claiming benefit of Sec 10A.”

In order to support the above submission, the Ld. Sr. Counsel for the Appellant took us through the relevant clauses of various contracts placed at Page 63 to 222 of the paper-book.

23. Further, the Ld. Sr. Counsel appearing for the Appellant also relied upon submissions, dated 12.02.2013, to contend that the Assessing Officer had erred in excluding communication expenses of INR 9,54,60,091/- and other expenditure incurred in foreign currency aggregating to INR 8,82,15,41,969/- from the export turnover on the ground that provisions of Explanation 2(iv) to Section 10A of the Act are not attracted. In this regard, reliance was placed on the decision of the Tribunal in the case of M/s Patni Telecom P. Ltd. vs. ITO [2009] 308 ITR (AT) 414 (Hyderabad). Without prejudice to the aforesaid, the Ld. Senior Counsel appearing for the Appellant submitted that, in any case, as per the decision of the Special Bench of the Tribunal in the case of Income-tax Officer, Company Ward-VI(1), Chennai vs. Sak Soft Limited :[2009] 121 TTJ 865 (Chennai) (SB)[06-03-2009] if the „export turnover‟ is arrived at after excluding certain expenses, the same should also be excluded in computing the „total turnover‟.

24. Per contra, the Ld. Departmental Representative vehemently contended that the Appellant would not engaged in the business of Software Development and therefore, not entitled to claim depreciation for the revenue stated to have been received by the Appellant from on-site development of software. He submitted that the Appellant was engaged in Body Shopping and in this regard relied upon clauses contained in various contracts placed on record by the Appellant pertaining to „supplier staff‟ or „staffing‟. He submitted that the clients exercise full control over the personnel provided by the Appellant on full time basis to the clients. He submitted that the overseas branches generated revenues from the aforesaid employees which could not have been considered as export of services from India derived from eligible units located in India. Without prejudice to the foresaid, the Ld. Departmental Representative submitted that the Assessing Officer was correct in excluding communication expenses and other expenses incurred in foreign currency as mandated by the provisions of Explanation 2(iv) to Section 10A of the Act.

25. We have considered the rival submissions and perused the material on record including the judicial precedents cited during the course of hearing. Before dealing with the issue raised in the present appeal, we deem it appropriate to refer to the legal background as succinctly noted by the Tribunal in its decision in the case of DCIT Circle 11(4), Bangalore, Vs. M/s. iGate Global Solutions Ltd. [IT(TP)A No.286/BANG/2013, Assessment Year 2007-08, dated 05/08/2019] which read as under:

“19. Section 10A is a special provision in respect of newly established undertakings in free trade zones etc. Sub-section (1) of this section provides for a deduction of profits and gains as are derived by an undertaking from the export, inter alia, of computer software for a specified period. It is not disputed that the assessee satisfied all the requisite conditions for becoming eligible to deduction under this section, which is apparent from the action of the AO in himself allowing deduction to some extent. The dispute is only to restricting the amount of deduction in respect of the alleged profits derived by the assessee from DTM and onsite charges, which in the opinion of the AO, were not derived from export of computer software.

20. The assessee is engaged in the business of computer software development from its eligible units. At this stage, it would be apposite to consider the meaning of `Computer software’ given in Explanation 2(i) of section 10A as: `(a) any computer programme recorded on any disc, tape, perforated media or other information storage device; or (b) any customized electronic data or any product or service of similar nature, as may be notified by the Board, – which is transmitted or exported from India to any place outside India by any means’. It transpires from the definition of the `computer software’ that it has two clauses. The first clause deals with a computer programme which is recorded on any disc or tape etc., which may usually be off the shelf product or in other words, a product which is available as such with the assessee and is not required to be customized. The second clause deals with a customized electronic data or any product, which is required to be tailor-made. Whereas the first clause encompasses a computer programme which has already been developed by the assessee on a standard basis and is exported as such, the second clause covers developing a new computer software as per the specific requirements of the customer.

21. One has to pass through various stages to develop a computer software, such as, Conceptualization, Planning, Designing, Developing, Testing and then Maintaining. In the Conceptualization stage, the requirements of the customer are first identified to form a view of the work to be done. In the Planning stage, an overall plan of proceeding with is formalized. In the Designing stage, blueprint of the work to be done is drawn. In the Development stage, which is also called coding stage, the actual work is started for translating the plan into action. It is one of the most important stages of software development. In this stage, the work is divided into several modules/programmes, each of which is independently developed and coded. This activity of development of modules and coding may be done simultaneously or one after another, depending upon the nature of module and its placement or setting within the overall product. The development stage produces a final software product, which is then tested on stringent standards to ensure that it measures up to the required specifications. Once the computer software or the product passes through the testing stage, it is given to the customer for actual use. Any product so developed may need maintenance and then upgradation with the passage of time. A close scrutiny of the life cycle of a customized software, as discussed above, discerns that a lot of interaction is required between the computer software developer and the customer, which is almost present in most of the stages of software development, starting with conceptualization itself. In developing a computer software of large magnitude, it is quite possible that a Software Developer may have to visit the site of the customer several times for having an on the spot information and properly appreciating the needs so as to make the final product compliant with the requirements. There can be several other reasons necessitating a customer abroad insisting a software developer in India to develop software fully or partly at his site overseas. The stage of testing in a customized software can be properly done only at the site of the customer. The nitty-gritty of the matter is that a customized software cannot be ordinarily developed without spending some time on site with the customer. Considering the objective of deduction u/s 10A and realizing practical issues and difficulties, the Finance Act, 2001 inserted Explanation 3 w.e.f. 1.4.2001 providing: `For the removal of doubts, it is hereby declared that the profits and gains derived from on site development of computer software (including services for development of software) outside India shall be deemed to be the profits and gains derived from the export of computer software outside India.’ The Explanation contains a deeming provision and gives a practical solution to the problem by providing that profits from on site development of computer software and services for development of software outside India shall be deemed to be the profits and gains derived from the export of computer software outside India. Undeterred by the Explanation 3, some of the authorities kept on refusing the claim of the assesses u/s 10A, as is the case under consideration, to the extent of the profits derived from onsite development of computer software and rendering of services by technical manpower outside India. The CBDT had to step in by issuing a Circular No.1/2013 dated 17.1.2013 providing that (a) : `it is clarified that the software developed abroad at a client’s place would be eligible for benefits under the respective provisions, because these would amount to ‘deemed export’ and tax benefits would not be denied merely on this ground’ and (b) `that profits earned as a result of deployment of Technical Manpower at the client’s place abroad specifically for software development work pursuant to a contract between the client and the eligible unit should not be denied benefits under sections 10A, 10AA and 10B provided such deputation of manpower is for the development of such software and all the prescribed conditions are fulfilled.’ It was brought to the notice of the CBDT that the AOs were not even following the clarification given in the Circular dated 17.1.2013. Once again, the CBDT issued Instruction No. 17/2013 dated 19.11.2013 clarifying that: `The undersigned is directed to convey that the field authorities are advised to follow the contents of the Circular in letter and spirit. It is also advised that further appeals should not be filed in cases where orders were passed prior to issue of Circular but the issues giving rise to the disputes have been clarified by the Circular’. There is hardly any need to accentuate that income-tax authorities are mere implementing agencies of the Parliament intent expressed through the enactment. They cannot suo motu usurp the power to indirectly legislate by not following the mandate of the provisions. Other income-tax authorities are bound to follow the command of the CBDT given through Circulars, even if they are not personally agreeable with the same.

22. On going through the directive of the Explanation 3 and the Circulars issued by the CBDT, which are binding on the authorities under the Act, it is vivid that the benefit of deduction under section 10A caters not only to profits earned from export simplicitor of computer software but also to any profits and gains derived from onsite development of computer software and also services for development of software rendered outside India. So long as there remains a live link between onsite development of computer software and services for development of software with the development of software from the eligible undertaking, the consideration awarded for onsite development for computer software and rendering services for development of services outside India cannot be excluded from the purview of deduction u/s.10A. However, what is essential for such onsite development or rendering of software development services outside India to qualify for the benefit of deduction is that these should be in furtherance of the development of the software product undertaken by the eligible enterprise. If onsite services are de hors the product which the assessee undertook to deliver to the foreign customer, then any profit and gain arising from such services cannot be considered as eligible for deduction. The determinative test to qualify for the benefit of deduction, in our considered opinion, is that the rendition of onsite services etc. outside India by the assessee should be an integral part of the overall computer software development project, which the assessee undertook to do for its foreign customer. So long as the onshore activities etc. performed outside India remain in furtherance of the final product to be delivered, there can be no doubt on the eligibility of profit from such activities for deduction.”

26. In the appeal before us also, it is not disputed that the Appellant had units eligible for deduction under Section 10A of the Act. The Assessing Officer has allowed part deduction claimed by the Appellant under Section 10A of the Act and the dispute before us is limited to the Revenue derived from on-site software development services. The contention of the revenue is that the Appellant is engaged in providing personnel and is, therefore, engaged in body shopping. On the other hand, the contention of the Appellant is providing software development services to the customers in discharge of its contractual obligations. Thus, the first issue is arises for consideration is whether the Appellant is engaged in providing software development services as claimed by the Appellant. The answer to a query regarding the nature of services provided by an assessee would depend upon the facts and circumstances of each case requiring examination of the business model and contractual obligations of such assessee. It is admitted position that 98% of the Revenue is earned by the Appellant under mixed/hybrid model requiring, both, services in India and onsite services outside India. Only 2% of the Revenue earned by the Appellant comes from the pure onsite services rendered outside India. The Appellant has placed before us the extracts of the following contracts (at page 63 to 222 of the paper-book) (a) Contract for Information Technology Services with Mushrif Trading & Contracting Co. [for short „Mushrif Contract‟] (b) Information Technology Services Agreement with Chevron U.S.A. Inc. [for short „Chevron Agreement‟] (c) Master Services Agreement on Software Development with Hitachi Limited, Japan [for short „Hitachi Agreement‟] and (d) Fixed Price Agreement with Thales, France (DAG/S&HT/2007/A262) [for short „Thales Agreement‟]. The Ld. Senior Counsel for the Appellant appearing before us relied upon the recitals and various clauses of the aforesaid agreement dealing with the scope/provision/location of services, obligations of the Appellant in relation to staff/personnel working on the project, price/consideration for services and its payment, to support the contention that the Appellant was engaged in providing software development services as per the contracts entered into by the Appellant with its clients. Countering the aforesaid submissions, the Ld. Departmental Representative placed reliance upon Clause 12 „Supplier Staff‟ of Chevron Agreement and Clause 14 „Staffing‟ of Hitachi Agreement to drive home the point that the Appellant was engaged in body shopping. He vehemently contended that Appellant was essentially supplying personnel who were under complete control and management of the clients and, therefore, Assessing Officer has rightly denied deduction claimed by the Appellant under Section 10A of the Act. However, on perusal of the agreements including the specific clauses highlighted by the Ld. Departmental Representative, we are of the view that the Appellant is not engaged in body shopping in view of the following:

26.1 Perusal of Mushrif Contract we find that according to the recital the Appellant has been engaged to implement, develop, create, test and deliver ERP/Software services. Clause 4 of the Mushrif Agreement dealing with „Notice of Delay‟, inter alia, provides that the Appellant could hire sub-contractors to provide some or all of the services set out in the relevant work order with prior written consent of the client. Further, the compensation structure provided in Clause 5 included fixed price compensation payable on completion of the services/milestone. Clause 10 dealing with „Ownership and Rights‟ provided, inter alia, that the intellectual property rights developed pursuant to work orders shall be owned by the client. As per Clause 11 dealing with „Representation and Warranties‟, the Appellant represented that it shall perform services in accordance with the degree of scale and care exercised by a service provider providing substantially similar services. The aforesaid agreement did not have any clauses pertaining to staff/personnel.

26.2. Next we take up the Chevron Agreement. The Ld. Departmental Representative had relied upon Clause 12 „Supplier Staff‟ of the Chevron Agreement and therefore, we proceed to first examine the same. The Ld. Departmental Representative had highlighted the facts Clause 12.1 provides that subject to approval by the client „Supplier Account Executive‟ appointed by the Appellant would serve on a full time basis as the primary representative and shall have overall responsibilities for managing/coordinating the performance of obligations by the Appellant and shall also be authorized to act on behalf of the Appellant. Similarly, Clause 12.2 provides that all „Key Supplier Personnel‟ working on the project shall work on full time basis. Before assigning any individual to key supplier position, the Appellant is required to notify the client, provide resume/ regarding such individual and obtain written approval of the client for such assignment. Further, Clause 12.2 (c) provides that the Appellant shall not replace „Supplier Account Executive‟/‟Key Supplier Personnel‟ for a period of two years. In our view, the terms and conditions highlighted by the Ld. Departmental Representative must be read in understood in the context of the rights and obligations of the parties under the agreement. On perusal of various provisions contained in Clause 12 we find that the provisions are intended to ensure continuous supply of quality services as represented by the Appellant. The limited control exercised by the client over assignment for specified duration and removal of the staff for the project cannot be treated at par with the right to appoint and terminate the employment of staff. As per Clause 12.1, the „Supplier Account Executive’ bares the responsibilities of managing/coordinating the Appellant’s obligations and also has the authority to act on behalf of the Appellant. Clause 12.2(c)/(d) do not bar replacement/re-assignment of personnel and also recognizes the right to the Appellant to terminate services of the employee/staff. Clause 12.3 clearly castes obligation on the Appellant to recruit/hire „Project Staff’ required for providing the services under the agreement. Clause 12.4 and 12.5 requires to application maintain „Buffer Staff’ and „Relief Staff’ of 15 to 20% of the Project Staff and 3 to 5% of Project Staff, respectively. The aforesaid clauses when read with the Clause 3 „Services’ read with Exhibit 2 „Statement of Work’ giving details of possible services which could be availed by the client, clearly shows that the subject matter of the agreement under consideration is software development services and not supply of personnel as contended by the Revenue.

26.3 Under Hitachi Agreement also the Appellant has been engaged for providing program support and services as specified in Article 3 of the said agreement for a firm/fixed price to be settled between the parties for each work/supplement project. In our view, merely because the Hitachi Agreement requires that the personnel deployed for the contract would serve on a full time basis with the client (and not for any other client of the Appellant) cannot lead to a conclusion that the Appellant is supplying personnel and not providing services to its clients.

26.4. Perusal of Thales Agreement shows that it is a fixed price contract for work including software development, associated technical documentation, etc. The aforesaid agreement does not contain a clause akin to Clause 12 of the Chevron Agreement, however, according to the Ld. Departmental Representative as per the terms of the agreement the Appellant can change assigned employee only after approval from Thales. In our view, the limited right/control exercised by the client cannot be viewed de-hors the other terms and conditions contained in contract to arrive at a conclusion that the Appellant is engaged in body shopping.

26.5. Thus, on perusal of the extract of various contracts placed before us and the clauses of contracts relied upon by the Assessing Officer in the assessment order and referred to by the Ld. Departmental Representative during the course of arguments, we are of the view that the Appellant is not engaged in body shopping qua the contracts/agreements placed before us. There is nothing on record to suggest that the Appellant is engaged in body shopping. Accordingly, we hold that for the Assessment Year 2009-10 deduction claimed by the Appellant cannot be denied on the ground that the Appellant is engaged in body shopping. Accordingly, Ground No. 2 raised in the present appeal is allowed and therefore, Ground No. 3, raised by the Appellant on without prejudice basis, as well as Additional Ground raised by the Appellant is disposed off as being infructuous.

Ground No. 4

27. According to the Assessing Officer the onsite services provided by the Appellant were not connected to the units in India and therefore, could not be considered as export of software from India derived from STPI Units located in India. Therefore, the Assessing Officer had concluded that 53.40% of the deduction claimed by the Appellant under Section 10A of the Act should be disallowed on proportionate basis. The case set up by the Assessing Officer was that the services are provided outside India by staff controlled by the foreign branches and are billed by the foreign branches (incorrectly stated to be subsidiaries by the DRP) and therefore, not linked to the eligible units located in India.

28. We note that during the authorities below the Appellant had explained that the invoicing was done in the name of branches for the convenience of complying with the requirements of the jurisdictional VAT/GST regulations. Further, as per the decision of the Co-ordinate Bench of the Tribunal in the case of M/s. iGate Global Solutions Ltd. (supra) the test to be applied is whether the onsite services form integral part of the overall computer software project. The Revenue has not contended that the onsite services do not form part of the computer project. Further, the Revenue has also accepted that 98% of the revenues earned by the Appellant are from hybrid model requiring, both, off-shore services from India and onsite services outside India. The foreign branches are part of the Appellant, though the same may be assessed in the status of Permanent Establishment outside India and treated separate/distinct from the Appellant as per tax regulations. In our view, while the finding by the Assessing Officer that the onsite services rendered by the Assessing Officer are not connected to the eligible units is without any basis, the finding returned by the DRP that the billing is done by foreign subsidiaries is contrary to the material on record. The CBDT had, vide Circular No.1/2013 dated 17.1.2013, as well as vide Instruction No. 17/2013 dated 19.11.2013, clarified that the benefit of Section 10A would be available in respect of the profits earned as a result of deployment of technical manpower at the client‟s place abroad for software development work provided all the prescribed conditions are fulfilled. The Assessing Officer has allowed part deduction under Section 10A of the Act in respect of eligible units and therefore, it can be inferred that the other conditions stand fulfilled in the case of the Appellant. Thus, we hold that for the Assessment Year 2009-10 deduction claimed by the Appellant under Section 10A of the Act in respect of revenue from onsite services cannot be denied on the ground that the onsite services are not connected to the eligible units located in India. Accordingly, Ground No. 4 raised in the appeal is allowed.

Ground No. 5

29. This takes us to the issue of computation of deduction under Section 10A of the Act. The Assessing Officer was of the view that while computing deduction under Section 10A of the Act following should be excluded from export turnover (a) communication charges, (b) expenditure in foreign currency, (c) interest income, and (d) additional depreciation. Therefore, on a without prejudice basis, the Assessing Officer computed deduction under Section 10A of the Act at INR 251,47,86,799/- and computed the disallowance of INR 11,73,66,598/- (INR 263,21,53,385/- minus INR 251,47,86,799/-). The CIT(A) confirmed the order passed by the Assessing Officer and therefore, the Appellant is before us in appeal on this issue.

30. In Ground No. 5 the Appellant has challenged the exclusion of communication charges of INR 9,27,34,738/- and foreign currency expenses of INR 8,82,15,41,969/- from the „Export Turnover‟ for the purpose of computing deduction under Section 10A of the Act.

31. We have considered the rival submission and perused the material on record. The Learned Senior Counsel appearing for the Appellant had submitted that the Appellant was no engaged in export of software and was providing software development services. The telecommunication charges were not related to the delivery of software outside India and therefore, not be excluded from the „Export Turnover‟ as defined in Explanation 2(iv) to Section 10A of the Act for the purpose of determining the quantum of deduction under Section 10A of the Act. As regards, the expenses incurred in foreign currency outside India, the stand of the Appellant before the Assessing Officer and CIT(A) was that the same are not to be excluded that the Appellant has not provided independent technical services. Per Contra, the Learned Departmental Representative relied upon the definition of „Export Turnover‟ as contained in Explanation 2(iv) of Section 10A of the Act and the order passed by the Assessing Officer and the CIT(A).

32. While adjudicating Ground No.1 and 2 above, we have accepted the contention of the Appellant that the Appellant was engaged in providing onsite software development services after examining the scope services of the agreements placed before us. Therefore, we accept the contention advanced on behalf of the Appellant that the Appellant is not engaged in export of computer software and has provided software development services to its clients outside India. Section 10A provides for deduction in respect of profit and gains derived by an undertaking, inter alia, from export of computer software. The Appellant is eligible to claim deduction under Section 10A of the Act since Explanation 3 to Section 10A clarifies that profits and gains derived from the services of development of computer software shall be deemed to be the profits and gains derived from the export of computer software outside India. Explanation 2(iv) to Section 10A provides for exclusion of, inter alia, telecommunication charges attributable to delivery of computer software outside India, and since the telecommunication expenses of INR 9,27,34,738/- are related to provision of software development services and not to delivery of computer software outside India, the same are, in our view, not required to be excluded from the „Export Turnover‟. However, as regards the foreign currency expenses aggregating to INR 8,82,15,41,969/- are concerned, we are of the view the same have to be excluded from the „Export Turnover‟ in case the same are connected with the provision of technical services outside India. The Appellant has provided the following break-up of the aforesaid foreign currency expenses of INR 8,82,15,41,969/-: (a) Overseas Staff Costs – INR 5,41,21,70,046/-, (b) Foreign Travel – INR 15,26,63,738/-, (c) Agency Commission – INR 35,74,600/-, and (d) Others (includes overseas office expenses) – INR 3,25,31,33,585/-. The Appellant has admittedly provided software development services to clients outside India which are in the nature of technical services as is clear on perusal of scope of services contained in the agreements on which reliance was placed by the Appellant to establish that the Appellant is engaged in providing onsite services for development of computer software for its clients outside India. However, neithern Assessing Officer nor the CIT(A) has returned a finding regarding nexus between the foreign currency expenses of INR 8,82,15,41,969/-, and rendering of technical services outside India. Though the Appellant has contended that the same have not been incurred in relation to provision of technical services outside India, there is nothing on record to determine the nature of expenses. The head under which the expenses have been aggregated is also not determinative. Accordingly, in the aforesaid facts and circumstances we deem it appropriate to remand this issue to the file of the Assessing Officer to identify and exclude from „Export Turnover‟ the expenses incurred in foreign exchange which are connected to providing services of software development outside India for the purpose of computing deduction under Section 10A of the Act. It is clarified that while computing the quantum of deduction under Section 10A of the Act the amount excluded from „Export Turnover‟ by the Assessing Officer shall also be excluded from „Total Turnover‟ as per the judgment of the Hon‟ble Supreme Court in the case of CIT, Central – III Vs. HCL Technologies Limited: 404 ITR 719 SC. In terms of the aforesaid, Ground No. 5 raised by the Appellant is partly allowed.

33. In result, the present appeal preferred by the Assessee is partly allowed.

Order pronounced on 30.05.2023.