QUALIFICATION :

GST practitioner is a qualified person who acts as a bridge between the GST System and the Registered Person. They assist the registered taxpayers in various GST related compliances.

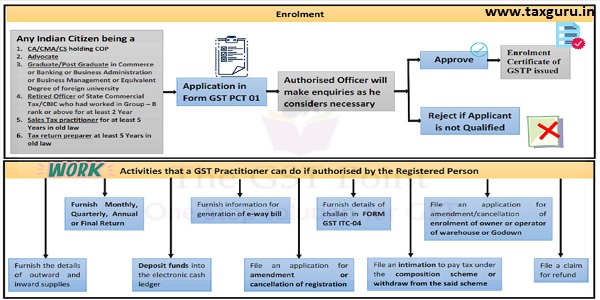

The list of qualified Person eligible to act as a GST Practitioner is given in Rule 83 of the CGST Rules 2017. A Person who is a Solvent Indian Citizen, having a sound mind and who is not convicted by court covered are eligible to be a GST Practitioner provided they satisfy any one of the below qualification:

1. CA or CMA or CS holding COP

2. Advocate

3. Graduate/Post Graduate in Commerce or Banking or Business Administration or Business Management or Equivalent Degree of foreign university

4. Retired Officer of State Commercial Tax/CBIC who had worked in Group – B rank or above for at least 2 Year

5. Sales Tax practitioner for at least 5 Years in old law

6. Tax return preparer for at least 5 Years in old law.

Page Contents

Procedure for Application and Approval as GST Practitioner:

So once you fulfil the eligibility, you can move forward to the common portal and apply to register yourself as a GST Practitioner. Let’s see the step by step process to apply:

STEP 1 : Filling Part A of Form GST PCT 01

- Go to the New Registration option in the GST Common Portal, You may click on this link https://reg.gst.gov.in/registration

- Fill the form. From the Drop down list, select that you are a “GST Practitioner“. Select your state, District, Name (as per PAN), PAN Number, Email and Mobile Number

- Validate the Details using OTP received in Mobile and E-mail. Post Validation, you will get a 15 Digit temporary reference number (TRN)

- Navigate to Services > Registration > New Registration option and select the Temporary Reference Number button. Enter the TRN number and proceed. You will receive OTP in your registered Mobile and Email. Enter the OTP and click on Proceed.

Step 2 : Filling Part B of Form GST PCT 01

Here you need to fill Four Section.

1. General Details : Select you qualification based on which you want to apply. Enter the name of university, year of passing and upload proof of Degree

2. Applicant Details : Enter your basic personal details such as Full name, Fathers name, Gender etc. and thereafter upload you photo

3. Professional Address : Provide the details of your professional address. You are also required to upload Proof of Address.

4. Verification : Accept the declaration that you are a Solvent Indian Citizen and having a sound mind and you are not convicted by court. Enter the place and submit using DSC/EVC

Upon submission, you will get an Application Reference Number (ARN). The status of the application can be viewed through Track Application Status at dash board on the GST Common Portal.

Step 3: Verification of application and issuance of Certificate :

Once you’ve applied, the details will be forwarded to the Appropriate Officer. After making such enquiry as he considers necessary, he’ll either enrol you as an GST Practitioner and issue a certificate in FORM GST PCT 02. He can reject your application on the ground that you are not qualified to be enrolled as a GST Practitioner.

Please note that there is no time limit specified in Rules to accept / reject the application. Thus it is seen that even after applying, the officers do not take any action for multiple months. So, If your application is pending from long or in case you want the certificate quickly then it is advised to contact the officer in person and request for approval.

Duties and Responsibilities of GST Practitioner:

Once officer approve your application, you become a GST Practitioner officially. Now a Registered Person can authorise you to act on his behalf and you can now do many activities. Below is the list of activities which you can undertaken on behalf of a registered person if authorised.

- Furnish the details of outward and inward supplies;

- Furnish monthly, quarterly, annual or final return i.e GSTR1, 3B, 4, 9 etc.

- Make deposit for credit into the electronic cash ledger;

- File a claim for refund;

- File an application for amendment or cancellation of registration;

- Furnish information for generation of e-way bill;

- Furnish details of challan in FORM GST ITC-04;

- File an application for amendment or cancellation of enrolment of owner or operator of warehouse or Godown and

- File an intimation to pay tax under the composition scheme or withdraw from the said scheme:

You need an authorisation to act on behalf of your clients. Once a Registered Person engage you, you can either Accept or Reject the request of engagement. To Accept or Reject the request, you need to login to the GST Common portal and navigate to Services > User Services > Accept / Reject Taxpayer option. Here you will see the list of the Registered Person. Click on the “View” button and you will be able to see the From GST PCT 05. If you want to Accept, then check the consent box and Submit using EVC/DSC. If you want to reject then do not check the consent box and Reject the Application. You can view the list of all the engaged tax payers. To view the list, navigating through Services > User Services > List of Taxpayer. You’ll have an option to remove any or all of your taxpayer.

As per Section 48(3) of the CGST act, 2017, it is mentioned that the responsibility for correctness of any particulars furnished in the return or other details filed by the goods and services tax practitioners shall continue to rest with the registered person on whose behalf such return and details are furnished.

How to perform Activities of GST Practitioner:

To act on behalf of engaged tax payer, you need to login to the GST Common Portal with your Username and Password and click on continue to Dashboard. option. You will be able to see the list of engaged Tax Payers. Click on the GSTIN of the Tax Payer to access the dashboard of the taxpayer. Now you can perform the functions as specified earlier, on behalf of the taxpayer.

Validity and Examination for GST Practitioner:

Your Enrolment shall be valid until it is cancelled. Further if you do not pass the exam conducted by National Academy of Customs, Indirect Taxes & Narcotics (NACIN) within such period as prescribed, then you will not be eligible to stay enrolled. Interestingly, the requirement of exam is prescribed only the Sales Tax Practitioners or Tax Return Preparer. For others, the requirement for exam is not yet prescribed. Thus in short, the validity depends upon two things. One is cancellation and second is passing of examination.

- Cancellation:

Officer can cancel if he found you guilty of any misconduct in connection with any proceedings under the Act. Before cancellation, officer is required to give you a reasonable opportunity of being heard. If you are guilty, then your enrolment shall be cancelled by order in Form GST PCT 04.

Alternatively you can also surrender your enrolment number by navigating through Services > Registration > Application for Cancellation of Enrolment option. Here you need to provide the reason for cancellation and the date from which you want the registration is to be cancelled. After that you need to submit the cancellation form (FORM GST PCT 06) by EVC/DSC. The officer may cancel the enrolment or he may ask for further clarification. You can reply to officer by navigating through Services > Registration > Application for Filing Clarifications. Once the authorised officer cancels your enrolment, he will issue order in Form GST PCT 07.

- Examination :

The requirement of exam is provided only for the Practitioners or Tax Return Preparer. They were required to pass the examination conducted by National Academy of Customs, Indirect Taxes & Narcotics (NACIN) within the end of December 2019. NACIN conducted exams thrice on 31.10.2018, 17.12.2018 and on 12.12.2019. After that, no exams were taken till date. The requirement of passing exam for other professionals can be prescribed by the Commissioner on the recommendations of the Council. Once such requirement is prescribed, you need to pass the exams.

Thus currently, if you are not enrolled as Sales Tax Practitioners or Tax Return Preparer then you are not required to give exam. And if you were registered as Sales Tax Practitioners or Tax Return Preparer and didn’t appeared or appeared but didn’t pass, then you are not eligible to be enrolled.

Author Bio

After getting gstp certificate, do i need to apply for gst number

I NEED INFORMATION ABOUT GST PRACTIONER

The exam is not being held since it was last held in 2019. Only the authorities can answer why it is kept suspended while all other exams are being held now.

i want to become a gst practitioner help me to become a register GST practitioner