Suppose there is only one bank in your area. That bank has a Rule that the depositors can’t directly deposit the amount, rather they are required to pay the amount to someone else (Say Mr. X). If Mr. X doesn’t deposit your funds specifying your account number, then the bank will not give you the Credit.

Now compare the Bank with the GST Law, you as the depositor and Mr. X as your supplier. You need to pay taxes to the supplier and if the supplier does not pay taxes to the Government, then you are not eligible for the Input Tax Credit [Section 16(2)(C) of the CGST Act 2017. Now this is the law of the Land and if you do not follow it, then there will be litigation. There is a very interesting case law in this regard, where The Hon’ble Madras High Court in M/S. D.Y. Beathel Enterprises versus The State Tax Officer has quashed the order imposing GST liability on the recipient on account of non-payment of tax by the supplier of goods. But if you want to avoid litigations, Notices of GSTR 2A vs. GSTR 3B mismatches etc. then the best way is to use available information to identify whether the Supplier is trustworthy and tax compliant or not

Information available along with degree of relevance:

Many useful information is available in the GST Common Portal which can help you to identify tax compliant suppliers. You can fetch the information just by using the supplier’s PAN card number. Here is the summary image containing the list of details which are available in the GST Common Portal and degree of relevance to identify whether or not the supplier is trustworthy & tax compliant.

How to access informations:

Step 1:

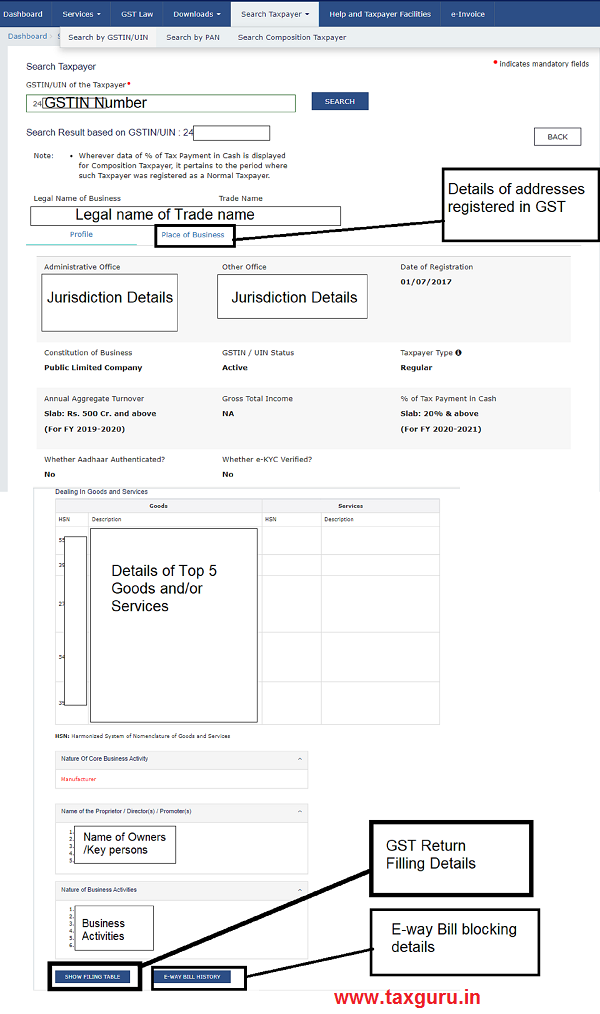

Step 1: Login to the GST Common portal and Navigate to Search Taxpayer à Search by PAN

Step 2: Enter the PAN number and click on search.

Step 3: List of all the GSTIN obtained using that PAN Number will be displayed. Click on any GSTIN.

Step 4: Click on Search. You will get all the above details except Place of Business, Filling details, E-waybill details.

Step 5: To get the GST Return Details, click on “Show Filling Table”. To get the E-waybill Details, click on “E-Waybill History” and to get place of business details, click on “Place of Business Details”

See the below image to get an idea about the detail’s availability

What are the highly relevant details for identification?

What are the highly relevant details for identification?

As you can see that among 21 details, only 4 are highly relevant. Read this short summary to understand how you can analyse the available information.

1. Return Filling Table: This is the most important information. Here you can see the filling month and Date of filling of all the GST Returns filed by your supplier. You can compare the actual filing date with the due date and if your supplier does not file the returns regularly in the past, then you may expect that he/she will delay in future too. For the delay/non filing of returns, you might face disallowance of Input Tax Credit. You need to be careful before dealing with these types of suppliers.

2. GSTIN/UIN Status: If the Status is anything other than “Active”, you should avoid dealing with the supplier. The status can be inactive, cancelled Suo-moto, cancelled on application by the taxpayer or suspended. In all these cases, the supplier can not pass on the Input Tax Credit. In other words, the supplier’s GSTIN should be in “Active” status.

3. Tax Payer Type: Type as “Regular” can collect GST and issue Tax Invoice. Other types of taxpayers such as composition, Tax Collector, ISD can not issue tax invoice. Thus, if you receive any Goods and/or Services, check whether the Taxpayer type is “Regular” or not.

4. E-Waybill History: If returns of two consecutive tax periods are not filled, then the generation of E-Way Bill will be restricted for all types of outward supply. You will get the details of restrictions imposed on e-waybill generation (if any) and the period of restriction. If there are no details, then it can be concluded that the supplier is tax compliant.

What are moderately relevant details for identification?

1. Number of GST Registration obtained using the same PAN: A person is required to obtain a separate GST Number for each state if he is doing business from multiple states. Also, A person may obtain multiple registration in the same state. When you search Taxpayer using PAN, you will get the list of all the GSTIN obtained using that PAN. Higher number of registrations indicated that the business is situated at multiple places. Usually, persons having multiple registrations are more tax compliant.

2. Date of Registration: Older the GST Registration date, better the chances of tax compliances by supplier because in GST, for each day of delay, there are late fees. Also, officers can cancel the GST number if returns are pending to be filled for multiple months. Thus, if the registration date is old and status is Active, then you can rely on the supplier.

3. Constitution of Business: Generally, companies are better tax compliant than proprietorship or partnership businesses because companies need to fulfil compliances of Companies Act too.

4. Annual Aggregate Turnover:Higher turnover can be an indicator that the supplier is tax compliant. In India, many tax compliances of various Acts are linked with Turnover. In other words, higher the turnover, higher will be the number of compliances. For each non-compliances, there are separate penalties. Thus, a business having higher turnover generally does not take the risk of non-compliance.

5. Nature of Business Activity: A business can undertake multiple business activities such as retail, wholesale, export, import, SEZ supply, Service providers etc. Generally, a business which has multiple business activities is more tax compliant.

6. Place of Business: A business can have multiple branches, sales offices or multiple Wearhouse. Higher number of addresses indicates that the business is situated at multiple locations. Higher the number of places, better the chance that the supplier is tax compliant.

Details which are not very strong indicators

1. Gross Total Income: If a business has high Income, then you can conclude that they can be a tax compliant supplier.

2. Percentage of Tax Payment in Cash: If a business is paying taxes using cash ledger, then this detail indicates how much percentage of total tax payment is made using Cash Ledger. Higher Percentage is better.

3. Whether Aadhaar Authenticated: Due to increased Fake Invoicing cases, businesses are required to do Aadhaar Authentication. “Yes” is better.

4. Whether e-KYC verified: Due to increased Fake Invoicing cases, businesses are required to do e-KYC verification. “Yes” is better.

5. Nature of Core Business Activity: In GST the core business activities are – Manufacturer, Trader, Service Provider & Others. If a supplier’s core business activity is manufacturing, then you can conclude that they are not a regular or large service provider. If they are supplying you Goods, then the chance of compliances is better.

6. Trade Name: This is the name of the business which is known by the public. Usually, businesses are known by their Brand name. Popular brands are better tax compliant.

Above 6 details are not very relevant to determine whether the supplier is tax compliant or not. You need to consider the other indicators along with these to come to a conclusion.

Details which are not relevant:

Details such as State GST Jurisdiction, Centre GST Jurisdiction, Name as per PAN i.e., Legal Name, details of Goods or services and the name of owners/ important persons are not relevant for determination of the tax compliant nature of business.

You can use the information and make decisions accordingly whether you want to deal with the supplier or not because prevention is better than cure.

*****

Disclaimer: The contents of this article are for information purposes only and do not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

Author Bio

REJOINDER(:

1. “You wrote that HE (Supplier) ALONE is responsible and directly answerable to the GOVT.”

Rejoinder: That is indisputably the correct, and only correct, legal position; YES or no ?

2. “But department is asking answers from Recipient. I can give you many such notices.”

Rejoinder: That is most certainly , if you have any valid objection , duly address to the ‘department’ ; emphatically -not me – AGREE !!!?

3. “Further please enlighten me about the misleading part of this article along with the correct information. I even quoted the High Court Judgement and also informed the fact that department send notices.”

Rejoinder: That is MAINLY the GREY AREA in your writeup, me was extremely left confused!!!!!!

Before making you understand why so, suggest you should again look through the Judgment, -if not done as yet- and let me know, – is that not case squarely falling under the Type- ‘ REGULAR’

(i.e. according to me , – the normal type !)

Also, check and let me know whether or not in all your clients’ cases, wherever so required, TAX Invoice (apart from Price Invoice, separately issued) has been duly issued ; that is, as MANDATED by the LAW , for an amount, no less or more than- NET of ITC.

PS: Just for your INFO., me have shared, as always my won’t, your write-up with my ‘CONNECTIONS’ ,- all of them senior Advocates and CAs in field practice for long, inviting their FEED back if any.

courtesy

First of all Thank you so much for sharing this article with you connections. Do let me know their feedback(s).

Going further, I want to emphasis the fact that the purpose of this article is to enable recipient in identification of non tax compliant suppliers because Section 16(2)(c) of the CGST Act will restrict the Input Tax Credit of genuine recipient. I am not commenting on the constitutional validity of this section, I am not arguing on the merit of issuing notices of mismatches between 2A and 3B, I am not going into the fake invoicing cases. There are many issues with Rule 36(4) of CGST Rule, there are many arguments on the validity of GSTR 2A/2B form. If I cover everything in details then the main purpose of this post will not be fulfilled.

I will prepare a separate article discussing the issuing revolving around Section 16(2)(C), GSTR 2A,2B,3B, Rule 36(4), Notices, Litigations but as I wrote “Prevention is better than cure”, this article will help recipient to take an informed decision so that this litigations can be avoided.

Lastly I would love to discuss with you the legality and other aspects and cover them in my next article. I have your email id and I’ll contact you before writing my next article.

Thank You

Having taken the trouble of sending the Rejoinder, just clarify the point raised in Item 3, for my own INFO. and to have my personal thoughts cleared on that particular aspect and also share with the others connected to me with a view provoke more on the indicated lines.

In fact, shared your write-up simply to make them aware of the intricacy of the GST law Implications and why a lot more STUDY , in-depth is warranted by everyone in practice, though me not one having retired almost TWO decades ago.

ADMN. (Owner)< "I have your email id and………………."

How Come ?

“………..Now compare the Bank with the GST Law…..”

So far as what one knows,have never heard of – or well nigh impossible to imagine, – any SUCH BANK in operation, or ANY SUCH Rule of any BANK ; premised that seemingly is a very poor /fictitious analogy, that might have to be totally ignored , as a non-starter, for any purpose such as herein.

Besides, as commonly felt and urged in legal circles, the ‘supplier’ collects GST as mandated by the law, as an agent of the GOVT. As such, if in a given case or particular instance, he fails to make payment of the GST collected to the GOVT., HE ALONE is responsible and directly answerable to the GOVT., – by no sane reasoning or logic; and, therefore, NOT THE RECIPIENT of the supply . Accordingly, to deny ITC benefit to the recipient ,and in turn to his customer would be patently wrong and ostensibly quite absurd.

ADMN. It is regrettable that such a patently misleading Article has been displayed, without any consideration of the dire consequences thereof, adversely impacting the vested rights and lawful interests of both the recipient of supply ) and its customer !?!

COURTESY

(For “THE COMMON GOOD”)

Please read the very first word of this article “Suppose”. I know there is no such bank which has this rule. I used this example so that the reader can related with the things which are happening in GST.

Further after reading you comment, it’s certain that you don’t have proper practical exposure of GST. You wrote that HE (Supplier) ALONE is responsible and directly answerable to the GOVT. But department is asking answers from Recipient. I can give you many such notices.

Further please enlighten me about the misleading part of this article along with the correct information. I even quoted the High Court Judgement and also informed the fact that department send notices. Every one can’t approach the Courts and in this article I shared the details which can help a recipient to analyse the tax compliant nature of the supplier so that s/he can reduce the chances of litigation. If this is misleading as per your point of view, then I completely disagree with you.

If a recipient is able to analyse whether the supplier is tax compliant or not, then what is the issue? Also I would like to draw your attention toward Section 149 of the CGST Act 2017 which talks about Compliance Rating. This rating is not yet implemented but once it is implemented, anyone can analyse the compliant nature of registered person.

I used lines such as “You need to be careful before dealing with these types of suppliers.”, “You need to consider the other indicators along with these to come to a conclusion.” throughout the article. Further there is clearly written disclaimer. Businessman normally tries to avoid litigations and this article can help them do that

Recepient cannot claim ITC, if Supplier does not deposit the GST to Govt. He will be Show Caused if he does so under section 16(2)(c) of CGST Act 2017. So it is prudent to check the background of the supplier before purchasing.

The article is well written.

“GST: How to identify if your supplier is Tax Compliant”

“ ………..there is only one bank in your area. That bank HAS A RULE THAT # the depositors can’t directly deposit the amount, rather they are required to pay the amount to someone else (Say Mr. X). If Mr. X doesn’t deposit your funds specifying your account number, then the bank will not give you the Credit.”

“Now compare the Bank with the GST Law, …………. You need to pay taxes to the supplier and IF THE SUPPLIER DOES NOT PAY TAXES TO THE GOVERNMENT, THEN YOU ARE NOT ELIGIBLE FOR THE INPUT TAX CREDIT [SECTION 16(2)(C) OF THE CGST ACT 2017. NOW THIS IS THE LAW OF THE LAND AND IF YOU DO NOT FOLLOW IT, THEN THERE WILL BE LITIGATION. …………………….There is a very interesting case law in this regard, where But if you want to avoid litigations, Notices of GSTR 2A vs. GSTR 3B mismatches etc. THEN THE BEST WAY IS TO USE AVAILABLE INFORMATION TO IDENTIFY WHETHER THE SUPPLIER IS TRUSTWORTHY AND TAX COMPLIANT OR NOT…”

IMPROMPTU(Reaction)

# ALL said (may be, DONE or not), me curious / am craving to know, – is there anyone ‘in field practice’, strugging with the intricacies/irresolute problems already faced with, – of any such ‘BANK’ OR ‘RULE’ operating /in force on this blessed planet of ours ?

Two IDIOMS (irresistably come to mind) :

“BARKING UP THE WRONG TREE” –

“NOT SEEING THE WOODS FOR THE TREE “(or FOREST!)

Not just stop short of it, but also ‘inspire others’ to follow suit , likewise – Agree ??!!??

Yes Sir. majority persons in field practice are facing issues for this Rule. Tax officers are sending notices of mismatched of GSTR 2A and GSTR 3B. So if the taxpayer can get an indication before dealing, then the instances of mismatches can be reduced.

I wonder if I understood you properly on this.

We can find out from such way but more tools are available to search in bulk to save times.