How to match the books of accounts input tax credit balance with GST Credit ledger who opts QRMP scheme.

(Assumption that the tax payer will pay the tax on the basis of self-assessment method)

Registered tax payer has paid the tax through GST PMT 06 for one month after considering input tax credit available. althotogether that might be possible for during the self assessment of second or third month excess amount of input tax credit is available as compare with outwards tax liability.

Taxpayers will be provided with a draft GSTR-3B, which will contain the details of the liability to be paid by taxpayers in the quarterly GSTR-3B. This will be prepared on the basis of the supplies declared in FORM GSTR-1 for the quarter. It will also contain data from the optional IFF, if any is filed in either of the first two months of the quarter. The said system computed values will also be auto-populated in quarterly GSTR-3B. Now if you have excess credit available in the last month of quarter compare with first two month,

Following question are arise while filing the aforesaid type of GST return.

1. How to offset cash liability which are already paid.

2. Shall full amount of ITC taken in GTSR 3B or not.

Let me explain with the below example might be you can get more clarity.

Suppose, a registered person have been availed the scheme for quarter January -21 to March-21. Now in the month of January-21 registered person has Rs 6,00,000/- outward supply on which tax liability is Rs 30,000/- of CGST and SGST each, and for the said month registered person has 10,000/- Input tax credit of CGST and SGST each after reconciliation of GSTR 2A.

So, tax payer has paid the liability through cash payment of which amount is Rs 20,000/- each of CGST and SGST.

Now, for the second month (Feb-21) same registered person has tax liability of Rs. 50,000 of CGST and SGST each and Rs.80, 000 of input tax credit of CGST and SGST each. Hence, excess amount of Rs.30, 000/- of each CGST and SGST credit is available and registered person would not not deposit any amount for said month.

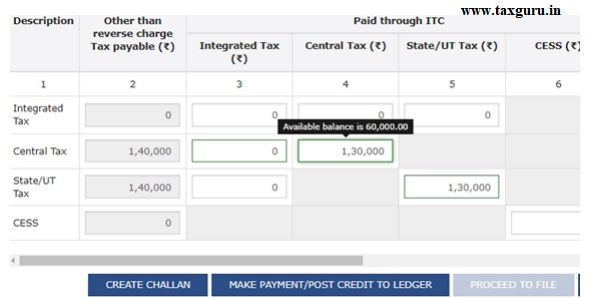

Now primarily important month is March -21, the registered person has outward tax liability is Rs 60,000/- of CGST and SGST each and the input tax credit is available 1, 00,000 of CGST and SGST So, the balance amount of Rs. 40,000/- of each CGST and SGST tax credit is available and registered person would not deposit any amount of tax for the said month.

Taxpayers will be provided with a draft GSTR-3B, which will contain the details of the liability to be paid by taxpayers in the quarterly GSTR-3B. This will be prepared on the basis of the supplies declared in FORM GSTR-1 for the quarter .It will also contain data from the optional IFF (2,80,000/-) and total input tax credit after reconciling of GSTR 2A (2,10,000/-).

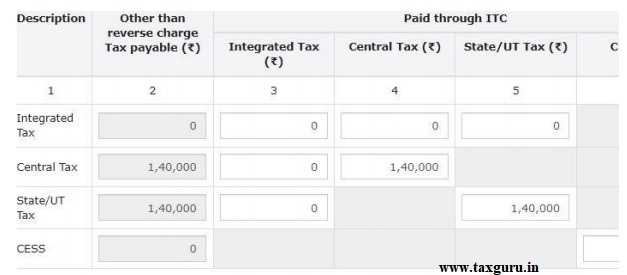

Now, the problem is how to utilise the cash balance of Rs10,000 of CGST and SGST each, which are paid through GST PMT 06 in the month of January-21.as compare to auto population amount in GSTR 3B which are reflect excess amount of ITC is available and registered person is not required to deposit any payment during the quarterly filling the GSTR 3B ( march-21) So, you can manually adjusted from input tax credit in the form GSTR 3B from Input tax credit (balance credit of Rs.60, 000 is matched with books after adjustment) and after that adjustment the balance payment of Rs 10,000 is automatically paid through cash balance available on GST portal and your return is matched with GSTR 1, Cash ledger and books of accounts.

So, you can manually adjusted from input tax credit in the form GSTR 3B from Input tax credit (balance credit of Rs.60, 000 is matched with books after adjustment) and after that adjustment the balance payment of Rs 10,000 is automatically paid through cash balance available on GST portal and your return is matched with GSTR 1, Cash ledger and books of accounts.