How to respond the email received from GSTN regarding Aggregate Turnover exceeding 5 crores for FY 2019-2020

This article contains the critical analysis of email received from Email-ID ‘noreply@gstn.gov.in’ on 04/08/2020 regarding confirmation of Aggregate Turnover exceeding 5 crore for FY 2019-20 in GSTR 3B. This article also explain steps to be taken in various cases along with Practical Examples regarding response to be submitted regarding such email (email enclosed within this article) regarding Taxpayers above 5 crores & below 5 crore Turnover as per GSTR 3B and/or Books of Accounts.

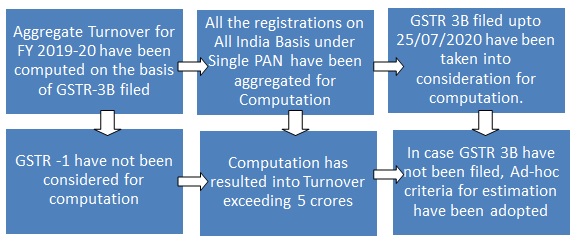

1.1 Aggregate Turnover Methodology as per Email

1.2 Case A: Aggregate Turnover as GSTR 3B is less than 5 crore

1.3 Case B: Aggregate Turnover as per GSTR 3B is more than 5 crore

Ignore the email, as purpose of the email is to ensure the correct selection of Filing Status of GST Taxpayer i.e. Below 5 Crore or Above 5 crore. You have already been selected as ‘Above 5 crore Taxpayer’. Government has extended dates for GST filings as notified vide Notf. No. 52/2020 dated 24.06.2020 and Notf. No 57/2020-CT dated 30.06.2020 based on criteria of Turnover i.e. 5 crore.

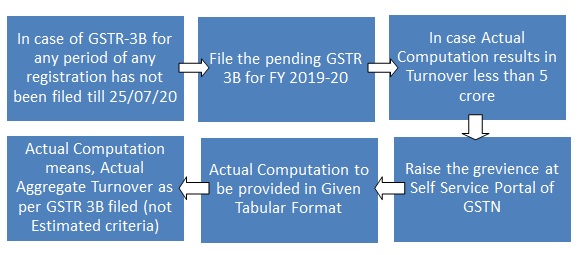

1.4 Case C: Aggregate Turnover as per Books is less than 5 crore, but Reported Turnover as per GSTR 3B is more than 5 crore

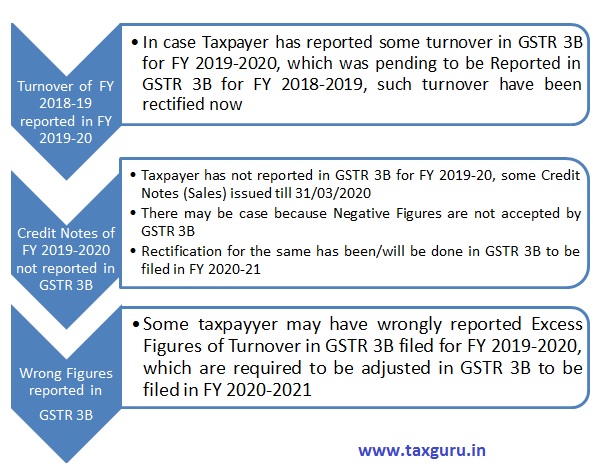

There can be case, which has resulted into reporting of Turnover as per GSTR 3B exceeding 5 crore, but actual Turnover as per books of accounts is less than 5 Crores e.g.-

In such cases, Tabular Format as given in the email, should be filled & detailed computation of aggregate turnover as per Books of accounts (Computed as per GST Law) should be annexed in the Grievance raised. Facts/Reason must be disclosed along-with working sheet.

1.5 Case D: Aggregate Turnover as per Books is more than 5 crore, but you have not received any such Email

Kindly ensure you are filing GST Returns during FY 2020-21 according to actual due dates applicable to you as per various notifications issued, even if GST Portal’s system is not considering the same. You may be liable to Late Fees (even if GST portal is not auto-computing) & Interest as applicable for Taxpayer with Turnover above 5 crores. Fact should be raised at Grievance Portal & actual due dates to be followed always.

1.6 Case E: Aggregate Turnover as per Books as well as GSTR 3B is below 5 Crores, but you have also received such Email

In such cases, Tabular Format as given in the email should be filled & detailed computation of aggregate turnover as per Books of accounts (Computed as per GST Law) should be annexed in the Grievance raised. Facts/Reason must be disclosed along-with working sheet.

1.7 Computation of Aggregate Turnover –

‘Aggregate turnover’, has been computed as per defined u/s 2(6) of the CGST Act,

- Same has been computed based Sum of the turnover as declared in GSTR 3B in

below tables –

Table 3.1(a) – Outward taxable supplies (other than zero rated, nil rated and exempted)

Table 3.1(b) – Outward taxable supplies (zero rated)

Table 3.1(c) – Other Outward Taxable supplies (Nil rated, exempted); and

Table 3.1(e) – Non-GST Outward Supplies

1.8 Content of the email

Contents of such email received on 04/08/2020 from GSTN have been reproduced below for the better understanding of readers:-

“ Dear 03ABCDE1234F1Z2 (Trade Name)

Your aggregate turnover for the financial year 2019-20 has been computed by GST system based on the returns filed in Form GSTR-3B by all registrations on the common PAN. The same has been found to be more than Rs. 5 Cr where returns of FY 2019-20 filed upto 25th July, 2020 have been considered for the said computation.

Your attention is drawn to definition of ‘Aggregate turnover’, defined under clause 6 of section 2 of the CGST Act, 2017. Accordingly, following methodology to compute aggregate turnover has been adopted:

(a) Turnover declared in Table 3.1(a), 3.1(b), 3.1(c) and 3.1(e) of GSTR-3B has been accounted for the computation.

(b) If the return of a tax period which was due to be filed but has not been filed for any of the GSTINs registered on the common PAN, the turnover of that period has been estimated by way of extrapolation as under:

[(Turnover declared/ No. of GSTR-3B filed) * No. of GSTR-3B liable to be filed]

(c) The turnover (including extrapolated turnover) of GSTINs has been summed up at PAN level.

Further, it is brought to your notice that the above turnover will be used for certain validations in the System such as determining due date of return filing, computation of late fee by the system. You can also use the same for reporting interest on delayed payments based on self-assessment basis.

If any discrepancy is found in the turnover data based on the computation, as explained above and the actual turnover, the taxpayer may file a grievance at https://selfservice.gstsystem.in for redressal. The taxpayers are advised to upload the information while raising complaint in following format, which will enable our team to resolve the same:

| PAN | ABCD1101F | Legal name | ABC Ltd | |||

| Sr. No. | GSTIN | Registration grant date | Tax period of last GSTR-3B filed | Date of filing of last GSTR-3B | STATUS (Active/ Cancelled) | Turnover as per taxpayer (Rs.)** |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 |

| 1 | e.g. Punjab’s GSTN | 01/07/2017 | Mar-2020 | 31/07/2020 | Active | 3.50 Crore |

| 2 | Delhi’s GSTN | 01/04/2019 | June-2020 | 01/08/2020 | Active | 1.00 Crore |

| 4.50 Crore | ||||||

**FY 2019-2020

****

Disclaimer: The contents of this article are for information purposes only and does not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

Article Contributed by:

CA Sagar Gambhir | FCA, DISA (ICAI) | casagargambhir@gmail.com

Author can be reached at casagargambhir@gmail.com for any queries, issues & recommendations relating to article.

Author Bio

sir I am a composition dealer and I have received a mail that I have exceeded aggregate turnover in 2019 -20 but I have not exceeded the turnover. how to reply to this email give suggestions.

Sir, if our turnover was exceeded Rs.5 Crore during the financial year 2019-20, how to report the same with gst portal, can you please guide me.

Sir, I am registered as regular tax payer. I file GSTR-1 quarterly. I have mentioned wrong GSTIN for a B2B dealer in GSTR-1 for the quarter ended on 31st March’20 Bill date is 18-1-20. I filed GSTR-1 in July’20 due to covid.

Query- How to amend/change the GSTIN for B2B dealer in GSTR-1 ?? Pls explain

Note- All other particulars are correct. Only GSTIN is wrongly mentioned in GSTR-1

Thanks a lot ..

Sir, I have filed Quarterly GSTR-1 for June’2020 quarter on 6-8-20. Whether i need to pay Both Interest & Late fees due to delay in filing of GSTR-1 ?

Also, tell how to pay Intt & Late fees due to delay in filing of GSTR-1 as there is no column in GSTR-1 for its payment ??

We have also received a message like this however it is a co-operative housing society. Out of total turnove 95% are exempt turnover. Aggregate turnover crossing 5Cr.

could you guide how we can writeup to the GSTN?