Transportation of Goods by road and tax implications associated with it becomes an important area of discussion in today’s scenario since a major share of goods in India(around 60%) are moved from one place to another via roads. Goods Transport Agency is majorly involved in providing the service of transportation of goods from one place to another and hence we need to have a clear understanding of the GST impact on this sector.

Now Goods can be transported by Road either by a Goods Transport Agency, a Courier Agency and any person other than a Goods Transport Agency or a Courier Agency. Let us understand the meaning of GTA and how it is treated in GST

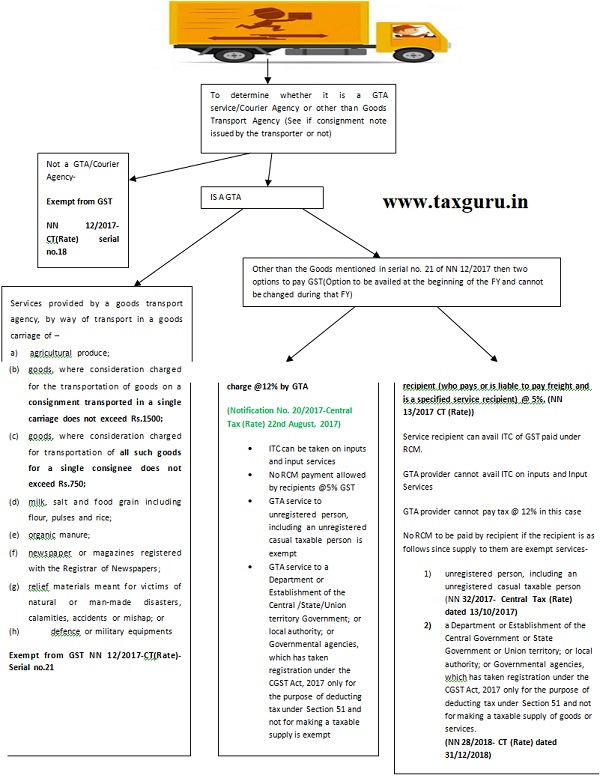

Meaning of Goods Transport Agency (GTA)–

“Goods Transport Agency” means any person who provides service in relation to transport of goods by road and issues consignment note, by whatever name called.

Thus, it can be seen that issuance of a consignment note is an essential condition for a supplier of service to be considered as a Goods Transport Agency. If such a consignment note is not issued by the transporter, the service provider will not come within the ambit of goods transport agency.

Meaning of Consignment Note-

A consignment note is a document issued by a GTA against the receipt of goods for the purpose of transporting the goods by road in a goods carriage. If a consignment note is issued, it means that the lien on the goods has been transferred to the transporter. Now the transporter is responsible for the goods till its safe delivery to the consignee.

A consignment note is serially numbered and contains –

- Name of consignor

- Name of consignee

- Registration number of the goods carriage in which the goods are transported

- Details of the goods

- Place of origin

- Place of destination.

- Person liable to pay GST – consignor, consignee, or the GTA.

Certain service of Transportation of Goods by road exempt under GST

Now a very important point to note here is that certain Service of Transportation of Goods by Road are exempt under GST. In terms of Notification no. 12/2017-Central Tax (Rate) dated 28.06.2017 (sr.no.18), the following services by way of transportation of goods are exempt from GST (Heading 9965):

(a) by road except the services of:

(i) a goods transportation agency;

(ii) a courier agency;

(b) by inland waterways.

Thus, it is to be seen that mere transportation of goods by road, unless it is a service rendered by a goods transportation agency, is exempt from GST.

Example: Mr. Krishna provides service of transportation of goods by road in a horse cart owned by him and does not issue consignment note. Hence this is an exempt service.

Therefore before deciding the taxability of Service of transportation of goods by road it’s important to find whether Consignment Note is issued by the transporter or not. Any document similar to the consignment note will hold the transporter as GTA service provider unless proved otherwise on facts (refer COMMISSIONER CENTRAL EXCISE VERSUS M/S KISAN SAHKARI CHINI MILLS LTD. AND ANOTHER-2017 (3) TMI 1786 – ALLAHABAD HIGH COURT). The facts of each case have to be studied separately and carefully to claim exemption as transport of goods otherwise than GTA.

GTA Services which are exempt(based on type of Goods Transported or to the type of persons to whom the services is provided)

Once we have established that the transporter is a GTA we need to see what type of Goods it is Transporting via its vehicle by road and service provided to what type to persons. Based on this assessment we can segregate out the services which are exempt via Exemption notifications under GST.

As per Notification no. 12/2017-Central Tax (Rate) amended from time to time, the following entries provide exemption to the GTA service.

| SL. No | Chapter | Description of Service | Rate |

| 21 | Heading 9965 or Heading 9967 | Services provided by a goods transport agency, by way of transport in a goods carriage of –

a) agricultural produce; (b) goods, where consideration charged for the transportation of goods on a consignment transported in a single carriage does not exceed Rs.1500; (c) goods, where consideration charged for transportation of all such goods for a single consignee does not exceed Rs.750; (d) milk, salt and food grain including flour, pulses and rice; (e) organic manure; (f) newspaper or magazines registered with the Registrar of Newspapers; (g) relief materials meant for victims of natural or man-made disasters, calamities, accidents or mishap; or (h) defence or military equipments. |

Nil |

| 21A | Heading 9965 or Heading 9967 | Services provided by a goods transport agency to an unregistered person, including an unregistered casual taxable person, other than the following recipients, namely: –

(a) any factory registered under or governed by the Factories Act, 1948(63 of 1948); or (b) any Society registered under the Societies Registration Act, 1860 (21 of 1860) or under any other law for the time being in force in any part of India; or (c) any Co-operative Society established by or under any law for the time being in force; or (d) any body corporate established, by or under any law for the time being in force; or (e) any partnership firm whether registered or not under any law including association of persons; (f) any casual taxable person registered under the CGST Act or the IGST Act or the SGST Act or the UTGST Act. (amended via Notification No. 32/2017- Central Tax (Rate) dated 13/10/2017) |

Nil |

| 21B | Heading 9965 or Heading 9967 | Services provided by a goods transport agency, by way of transport of goods in a goods carriage, to, –

(a) a Department or Establishment of the Central Government or State Government or Union territory; or (b) local authority; or (c) Governmental agencies, which has taken registration under the CGST Act, 2017 (12 of 2017) only for the purpose of deducting tax under Section 51 and not for making a taxable supply of goods or services. (amended via Notification No. 28/2018- Central Tax (Rate) dated 31/12/2018) |

Nil |

| 9B | Chapter 99 | Supply of services associated with transit cargo to Nepal and Bhutan (landlocked countries). | Nil |

Thus on the basis of the above table we conclude the following:

1) If GTA provides service of transportation of certain specified goods in entry no 21 then the service is exempt from GST.

2) If consideration charged for the transportation of goods on a consignment transported in a single carriage does not exceed Rs.1500; or goods, where consideration charged for transportation of all such goods for a single consignee does not exceed Rs.750; is exempt from GST.

3) If Services is provided by a GTA to an unregistered person, including an unregistered casual taxable person, other than the Specified recipients in entry 21A then the service is exempt under GST (effective from 13/10/2017).

4) If GTA service is provided to the persons mentioned in entry 21B and who are registered under GST only for the purpose of deducting tax under Section 51 and not for making a taxable supply of goods or services, the service of GTA is exempt(effective from 31/12/2018)

Examples:

1) XYZ Ltd. receives goods from a GTA in a truck. No other goods are loaded in that truck. A Ltd. pays freight of Rs. 1500/- to GTA. It is exempt since total freight for the consignment in single carriage is Rs.1500 (does not exceed 1500).

2) XYZ Ltd. receives goods from a GTA in a truck. Some other goods not belonging to XYZ Ltd. are also loaded in the truck. XYZ Ltd. pays freight of Rs. 800/- to GTA. The freight of other goods is Rs. 500/-. The service is exempt as the total freight for the truck is Rs. 1300 (does not exceed 1500)

3) In (2) above, if the freight of other goods is Rs. 800/-, then the total freight for the truck is Rs. 1600. Freight for a single consignee (XYZ Ltd) is Rs. 800 (exceeds 750) and total freight for the consignment in single carriage is Rs.1600 (exceeds Rs. 1500). Therefore, exemption is not available and GST to be paid on Rs.800 (single consignment of XYZ Ltd. by XYZ Ltd. or GTA provider)

Note: Services by way of giving on hire to a GTA, a means of transportation of goods is exempt under GST (as per Notification no. 12/2017-CT (Rate) dated 28/06/2017 entry no. 22(b)).

Taxable GTA services

If the Service of GTA is not exempted as per the above table or under any other provisions of GST then it will attract GST and the GTA has two options before him to pay GST as follows:

1) Pay GST @ 12%(CGST6%+SGST6%) with ITC under Forward Charge Mechanism( to be paid by GTA)

2) Pay GST@ 5%(CGST2.5%+SGST2.5%) without ITC under Reverse Charge Mechanism(to be paid by the service recipient i.e the consignor or the consignee)*

However, the GTA has to opt between option 1 and option 2 at the beginning of financial year. If the GTA is availing the option 1 to pay GST under Forward Charge then it has to pay GST@12% on all the GTA service supplies by it unless covered under exemption notification and can avail ITC of goods and services used to provide the GTA services by it. In this case it will not be able to take the benefit of GST@5% to be paid under RCM by the service recipient.

If it avails option 2 at the beginning of the year GST on GTA services is to be paid under RCM by the service recipient (service recipient shall be the consignor or the consignee who pays or is liable to pay the freight to GTA). In this case GTA cannot avail ITC on goods and services used to provide GTA services by it. However the recipient can avail the credit of GST paid on GTA services under RCM.

Note: In option 2 GST to be paid under RCM only by specified category of persons as mentioned in the RCM notification no. 13/2017-CT(Rate) dated 28/06/2017 (to be discussed later)

History of GST on GTA services since the inception of GST as on 1st July 2017 till date:

Initially GTA service was taxable only under RCM where the recipient of GTA service was liable to pay GST @5%. This was covered in the Notification No. 13/2017 of CT (Rate) dated 28th June 2017 (RCM List). The item 1 of this notification states that the whole of GST levied on GTA under section 9 of CGST Act 2017, shall be paid on reverse charge basis by the recipient of services of goods transport agency (GTA) in respect of transportation of goods by road to:

1. any Factory registered under or governed by the Factories Act, 1948

2. any Registered Society

3. any Co-Operative Society established by or under any law; or

4. Any Company

5. any Partnership Firm

6. Association of person

7. any GST registered person

So, if the GTA services are provided to person mentioned above (1 to 7) then such a recipient of the GTA services would be liable to pay GST on Reverse Charge basis and the rate of GST was 5%. It’s to be noted that Individuals & HUF recipients are left out from the applicability of RCM unless they are registered under GST Act.

However there was a little issue with the above scenario. The GTA service providers were not eligible to avail ITC and this led to increase in the cost of services. Generally GTA providers make huge capital investment on vehicles or infrastructure to keep the vehicles and various other expenses and they were not able to claim ITC of the same. So the GTA industry made representations to government regarding this issue and requested to pay GST under Forward charge and hence claim ITC of GST paid on input goods and services. On basis of the representations the government issued the Notification No. 20/2017-CT (Rate) 22nd August, 2017. This notification provides that if the goods transport agency opts to pay the tax on forwards charge basis then, such GTA would be liable to pay central tax @ 6% on all the services of GTA (including used household goods for personal use) supplied by it. So, the tax rate on GTA services on forward charges basis was fixed @12% (6% CGST & 6% SGST). If GTA opts to charge tax on forward charges basis then the service provider & services recipient, both would be eligible to get the input tax credit. However it will lose the benefit of GST@5% to be paid by the service recipient under RCM.

So till 21st August 2017 GTA service was only covered under RCM and only service receiver was liable to pay GST @5% however from 22nd August 2017 GTA service providers have option between forward charge payment by GTA provider @12% and reverse charge payment of GST@5% by recipient.

Registration requirement for GTA providers

There is a lot of confusion around the registration requirement of GTA Providers. So let us discuss the registration requirement of GTA under Option 1 and Option 2 as discussed above.

OPTION 1: When GTA opts to pay under Normal Charge Mechanism

In this option the GTA service provider pays GST@12% on all the GTA services provided by it unless the service is specially expected (refer the table above). GTA service provider is liable to register in the state from where it makes taxable supply of goods/services under GST if aggregate turnover in a financial year exceed Rs. 20 lakhs/10lakhs(special category states).

“aggregate turnover” means the aggregate value of all taxable supplies (excluding the value of inward supplies on which tax is payable by a person on reverse charge basis), exempt supplies, exports of goods or services or both and inter-State supplies of persons having the same Permanent Account Number, to be computed on all India basis but excludes central tax, State tax, Union territory tax, integrated tax and cess”

So if the Aggregate turnover of such GTA providers exceed the prescribed limit in a FY then it is required to get registered under GST, collect GST on Taxable services provided by it @12% and discharge the same to the government by utilization of ITC or by cash.

Addressing Queries that might come up:

1) In case the aggregate turnover is less than 20/10 lakhs however the GTA provides Inter-State service of GTA. Is GTA provider in this case required to take registration compulsorily?

Ans: No it is not required to register. A person making any inter-State taxable supply of goods is required to be registered under GST irrespective of turnover limit(as per Sec 24 of the CGST Act 2017). However there is an exemption from compulsory GST registration even when making interstate supply as follows:

- A person making inter-state supply of services is not required to register under GST if his aggregate turnover is less than Rs 20/10 lakhs (NN. 10/2017-IT dated 13-10-17 as amended vide NN. 03/2019- IT dated 29.01.2019)

- Persons engaged in supply of handicraft goods making inter-state supply are exempt from GST registration, if the aggregate value of all their supplies on all India bases is less than Rs 20 lakhs/10 lakhs per annum.

2) Is GTA provider required to take registration if it is exclusively providing exempt supply of GTA service (refer the table above) and its aggregate turnover exceed 20/10 lakhs?

Ans: Person exclusively engaged in the business of supplying goods/services that are wholly exempt from tax is not required to register under GST even if its Aggregate Turnover exceeds 20/10 lakhs (Section 23 of CGST Act 2017). As soon as it supplies a taxable service or goods and its aggregate turnover (including exempt supplies) exceed 20/10 lakhs it is required to take registration under GST.

OPTION 2: When GTA opts to pay under Reverse Charge Mechanism

In this case the GTA provider is not required to pay GST. The service recipient who pays or is required to pay the freight to the GTA provider is required to pay GST under RCM @5%. GTA provider cannot avail ITC of GST paid on input goods and services however the Service receiver paying under RCM can avail credit of GST paid under RCM. The service recipients who shall pay under RCM for GTA service (NN 13/2017-CT (Rate)) are as follows:

1. any Factory registered under or governed by the Factories Act, 1948

2. any Registered Society under the Societies Registration Act

3. any Co-Operative Society established by or under any law;

4. any Partnership Firm whether registered or not under any law including Association of persons whether registered or not under any law

5. any GST registered person.

6. any body corporate established, by or under any law;

7. any Casual taxable person

Even if the Aggregate Turnover of these 7 types of service recipients mentioned above does not exceed Rs 20/10 lakh(for services) or Rs 40/20 lakhs (for Goods) it has to compulsorily get registered under GST (as per Sec 24(iii) of CGST Act 2017)and pay GST under RCM. However in this case the issue was that if GTA service is provided to an unregistered person then it was not covered initially under RCM and there was a doubt on the taxability of the same.

So to cover this gap Government came up with Notification No. 32/2017- Central Tax (Rate) dated 13/10/2017(amending Notification no. 12/2017-Central Tax (Rate)) to add serial no.21A. This entry said that any Services provided by a goods transport agency to an unregistered person, including an unregistered casual taxable person shall be exempt from GST.

Also if GTA service is provided to the persons mentioned in entry 21B and who are registered under GST only for the purpose of deducting tax under Section 51 and not for making a taxable supply of goods or services, the service of GTA is exempt (entry no 21B was added in the exemption list via Notification No. 28/2018- Central Tax (Rate) dated 31/12/2018 ).

If a GTA service provider is

- exclusively engaged in the business of supplying goods/services that are wholly exempt from tax (Sec 23 of CGST Act) or,

- is only engaged in making supplies of taxable goods/services, the total tax on which is liable to be paid on reverse charge basis by the recipient of such goods or services or both(Sec 23 of the CGST Act 2017, NN 5/2017-CT dated 19/06/2017 w.e.f 22/06/2017)

then it is not required to take registration under GST.

In option 2 most of the supplies of services by GTA is either covered under RCM or is either wholly exempt. Hence as long as it continues to supply exclusively exempt supply or making supplies on which GST is paid under reverse charge only it is not required to take registration under GST even if the aggregate turnover exceeds Rs 20/10 lakhs. However if the GTA provides any supply of Service or Goods or both which is neither exempt nor covered under RCM then it has to check its Aggregate Turnover limit on a continuous basis till it crosses Rs 20/10 lakh and take registration under GST. Even if the GTA is required to register under Option 2 it cannot pay GST under forward charge @12%( both the options cannot be availed at once).

Significance of the term ‘in relation to’ in the definition of GTA

The service includes not only the actual transportation of goods, but other intermediate/ancillary service provided such as-

- Loading/unloading

- Packing/ unpacking

- Trans-shipment

- Temporary warehousing etc.

If these services are not provided as independent activities but are the means for successful provision of GTA Service, then they are also covered under GTA and hence included in the transaction value of GTA service and taxed at the same rate as that of GTA service.

Input Tax Credit to GTA service providers

- If the GTA provider opts for Forward Charge Mechanism payment@12% GST then it can avail all the eligible credit of GST paid on input goods and services. For big and organised GTA providers who make huge capital investments in vehicles and other major expenses it is beneficial to opt for this option since ITC can be availed and cost of service is hence lower. This option is beneficial to both GTA provider and recipient as both can avail ITC paid on GTA service.

- If the GTA provider opts for RCM payment by Service recipient @5% then it cannot avail credit of GST paid on inputs and input services. It’s an additional cost to GTA provider. However if the GTA provider does not make major capital investment and mostly hires out vehicles which is exempt service this is the best option to go for. It reduces the compliance burden on GTA.

Invoicing for GTA

Any GST compliant invoice of a GTA must have following details-

1. Name of the consignor and the consignee

2. Registration number of goods carriage in which the goods are transported

3. Details of goods transported

4. Gross weight of the consignment

5. Details of place of origin and destination

6. GSTIN of the person liable for paying tax whether as consigner, consignee or goods transport agency

7. Name, address and GSTIN (if applicable) of the GTA

8. Tax invoice number (it must be generated consecutively and each tax invoice will have a unique number for that financial year)

9. Date of issue

10. Description of service

11. Taxable value of supply

12. Applicable rate of GST (Rates of CGST, SGST, IGST, UTGST and cess clearly mentioned)

13. Amount of tax (With breakup of amounts of CGST, SGST, IGST, UTGST and cess)

14. Whether GST is payable on reverse charge basis

15. Signature of the supplier

Determining Place of Supply (POS) for a GTA

Most of the people are confused as to what is the POS for GTA services when covered under RCM. It should be noted that POS will be same irrespective of whether GTA pays under Forward charge or chooses the option of RCM payment by the recipient.

In case of Domestic Transaction :

The place of supply of services by way of transportation of goods, including by mail or courier to, –

- Registered Person-shall be location of the registered recipient

- Unregistered Person- shall be the location at which such goods are handed over for their transportation.

Effective from 01st February 2019 an amendment has been brought in Section 12(8) of IGST Act 2017 and the amendment has inserted the following proviso:

Provided that where the transportation of goods is to a place outside India, the place of supply shall be the place of destination of such goods.

In case of Import/Export Transaction :

The place of supply of services by way of transportation of goods other than mail/courier is place of destination of Goods. This is the case when either the GTA or the recipient of GTA service is located outside India.

| Examples | ||||

| Location of GTA(Service Provider) | Location of Service Receiver(The one who pays the freight) | Registration status of Service Recipient | POS | GST Levy |

| Kolkata | Kolkata | Registered | Kolkata (the location of registered recipient) | CGST+SGST(intra-state) Sec 12(8) of IGST Act 2017 |

| Kolkata | Bangalore | Registered | Bangalore (the location of registered recipient) | IGST(inter-state) Sec 12(8) of IGST Act 2017 |

| Kolkata | Bangalore

(example- transfer of household items from Kolkata to Bangalore while house shifting) |

Unregistered | Kolkata

(Location at which such goods are handed over for their transportation) |

CGST+SGST(intra-state)

Sec 12(8) of IGST Act 2017 |

| Kolkata | Bangalore

(example-Export of goods by road outside India say Bangladesh) |

Registered | Bangladesh

(place of destination of such goods) |

IGST(inter-state) Proviso to Sec 12(8) of IGST Act 2017

Note: this is not an export transaction since both GTA and service recipient are located in India |

| Kolkata | Bangladesh(who pays the freight)-Importer located in Bangladesh taking the service of Indian GTA and also paying the freight | Unregistered | Bangladesh (place of destination of Goods) | No GST since it is export of services Sec 13(9) of the IGST Act 2017 |

Summary:

Disclaimer: Every effort has been made to keep the information cited in this article error-free. Suggestions and feedback to improve the task are welcome. The article and opinions therein is based on my understanding of the GST law and provisions prevailing as on date. The opinion may vary according to one’s interpretation of the law. It should not be relied upon as the sole basis for any decision which may affect you or your business.

The author can be approached at agarwal.priyanka1705@gmail.com

Author Bio

Please specify, which section covered and where it is mentioned in GST portal to opt between option 1 ( RCM ) and option 2 ( Forward Charge ) at the beginning of the financial year.

As per NN 5/2017 CT, GTA provider is exempted from taking registration if it provides services liable to tax under 9(3) of CGST Act.

If the GTA provider provides Inter-state GTA service, obviously the aforesaid NN would not apply.

Does it mean, he has to take registration in such case?