This is premium content. Please become a Premium member. If you are already a member, login here to access the full content.

Notice issued in the name of amalgamated company is void

Case Law Details

- Case Name

- M/s Images Credit and Portfolio (P) Ltd. (amalgamated with Sainath Associates Pvt. Ltd.) Vs ACIT (ITAT Delhi)

- Appeal Number

- Only available for paid members

- Date of Judgement/Order

- Only available for paid members

- Courts

- All ITAT, ITAT Delhi

Upgrade to Basic or Premium to download.

Already Upgraded? Log in.

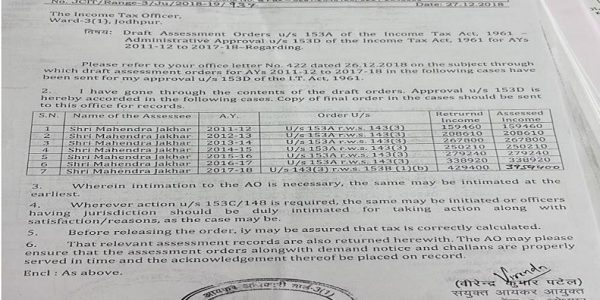

Admittedly the assessment for the year under consideration has been completed on the basis of notice under Section 153C dt. 14.9.2010. Notice has been issued in the name of M/s Image Credit & Portfolio Ltd. That the Hon’ble Delhi High Court, which is the Jurisdictional High Court, has passed the order dt. 25th day of May,2010 under Section 394 of the Companies Act, 1956 approving the amalgamation of the assessee company with M/s Sainath Associates Pvt.Ltd. The relevant finding of their Lordships held as under.

“THIS COURT DOTH HEREBY SANCTION THE SCHME OF

AMALGAMATION set forth...

Such instances happen to come across; albeit it is , even common sense, apart frm legal sense, should dictate, is a ridiculously wasteful exercise costing the otherwise valuable time and energy of everyone directly or indirectly concerned / impacted;particularly, of the judiciary. Unless and until such instances are taken quite seriously, and Revenue tries and makes it a point to bring about moral and ethical behavior, from the lowly AO level to the higher-ups, by resort to effective coercive steps, there could be no improvement in the administration of the tax law expected of;but further degradation will be inevitable.

Any solution , it goes without adding, lies in Strict monitoring and close control over the ‘public servants’ in discharge of their respective duties of office, more so diligently and consciously.

That should be the strategic philosophy could conceivably be no different also in regard to the administration of the State laws; e.g. commercial tax laws, within the realm of state administration.