Introduction: –

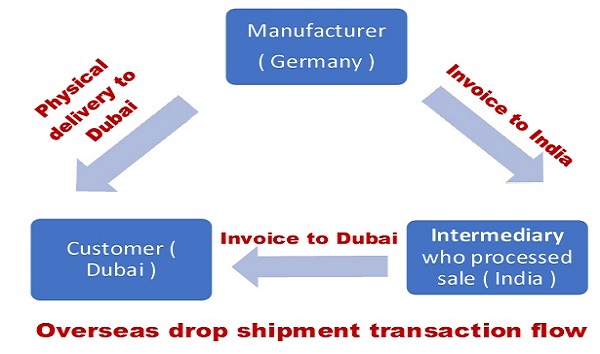

What is drop shipment transaction?

“Delivery of merchandise from a manufacturer or original supplier direct to a buyer, without passing through the warehouse of a distributor or retailer (who generated and processed the sale).”

Drop shipment is a supply chain management. In this type of transaction, the person, who generated and processed the sale, does not keep goods in stock but instead transfers customer orders and shipment details to either the manufacturer or another retailer or wholesaler, who then ships the goods directly to the customer.

In this article, we will study impact of GST on overseas drop shipment transactions.

It is needless to quote here that the said transaction is very well covered under term supply as per Section 7 of CGST Act, 2017. However, following questions may arise :-

(i) Whether inward supply in the said transaction amounts to import?

(ii) Whether outward supply in the said transaction amounts to export?

(iii) If it is export, whether it can be exported under bond or letter of undertaking without payment of IGST?

(iv)What other provisions shall be considered? This article will answer all above questions.

In the said transaction, two kinds of supplies are involved – Inward supply and Outward supply. Provisions of IGST Act, 2017, have to be studied in this regard. Let’s study such supplies one by one.

Impact of GST on inward supply –

Discussion on the law: –

As per section 2(10) of IGST Act, 2017, ‘‘import of goods” with its grammatical variations and cognate expressions, means bringing goods into India from a place outside India.

As per section 2(10) of IGST Act, 2017, ‘‘import of goods” with its grammatical variations and cognate expressions, means bringing goods into India from a place outside India.

It implies that there must be physical movement of goods into India from place outside India and hence inward supply, in abovementioned transaction, cannot be construed as an import of goods.

Also, as per section 12 of Customs Act, 1962, duties of customs shall be levied on goods imported into or exported from India. Hence, unless the goods cross customs frontiers of India, no customs duty can be levied.

As per section 5(4) of IGST Act, 2017, “The integrated tax in respect of the supply of taxable goods or services or both by a supplier, who is not registered, to a registered person shall be paid by such person on reverse charge basis as the recipient and all the provisions of this Act shall apply to such recipient as if he is the person liable for paying the tax in relation to the supply of such goods or services or both.”

It implies that in the said transaction as supplier from India is procuring goods from Manufacturer (Germany), who is unregistered person, IGST shall be payable on reverse charge basis.

However, as per notification no. 38/2017- Central Tax (Rate) dt. 13th October, 2017, reverse charge on procurement from unregistered persons has been suspended till 31st March, 2018. Hence, no reverse charge is payable on inward supplies after notified date till 31st March, 2018.

Conclusion: –

(i) Above inward supply cannot be construed as an “import of goods”.

(ii) No customs duty or IGST is payable on inward supply only if goods are supplied during 13th October, 2017 to 31st March, 2018. From 1st April, 2018 onwards, reverse charge shall be applicable and IGST shall be payable u/s 5(4) of IGST Act, 2017.

Impact of GST on outward supply –

Discussion on the law: –

As per section 2(5) “export of goods” with its grammatical variations and cognate expressions, means taking goods out of India to a place outside India.

It implies that physical movement of goods to a place outside India is important to construe transaction as an export and hence the said outward supply, in abovementioned transaction, is not an export.

As per section 7(5)(a) of IGST Act, 2017, supply of goods or services or both, when supplier is located in India and the place of supply is outside India, shall be treated as supply of goods or services or both in the course of inter-state trade or commerce.

In above transaction, supplier is located in India.

As per section 10(a) of IGST Act, 2017, place of supply of goods other than supply of goods imported into or exported from India, shall be where the supply involves movement of goods, whether by the supplier or the recipient or by any other person, the place of supply of such goods shall be the location of the goods at the time at which the movement of goods terminates for delivery to the recipient.

In above example, movement of goods is involved (from Germany to Dubai.) Location at which the movement of goods terminates for delivery to the recipient is Dubai. Hence, place of supply is Dubai i.e outside India. Hence, this transaction shall be treated as inter-state transaction and hence, IGST shall be paid.

Zero rated supply – As per section 16(1) of IGST Act, 2017, “Zero rated supply” means (a) export of goods and (b) supply of goods to SEZ units or Developers. As outward supply, in the said transaction, could not be treated as an export, hence, it cannot be termed as “Zero rated supply”. It implies that such outward supply cannot be made without payment of IGST under bond or letter of undertaking.

Conclusion: –

(i) Above outward supply cannot be construed as an “export of goods”.

(ii) IGST is payable on outward supply of goods at the rate specified on goods.

(iii) As the said transaction cannot be termed as “zero rated supply”, it cannot be done without payment of IGST under bond or letter of undertaking.

Worth to note: –

Profitability, in such type of transactions, will play vital role. If IGST is not collected from customer on outward supply, then profitability percentage shall be more than the GST rate applicable for such goods. Otherwise, such transaction could not be profitable to taxable person. Another option of re-export of imported goods on furnishing bonds as specified under Customs Act, 1962 and rules thereunder can be looked into.

Note: This article was written on 4th January, 2018.

Is it possible to give the reply as “YES” or “NO”

so that person like me can understand.

(i) Whether inward supply in the said transaction amounts to import? “YES” or “NO”

(ii) Whether outward supply in the said transaction amounts to export? “YES” or “NO”

(iii) If it is export, whether it can be exported under bond or letter of undertaking without payment of IGST? “YES” or “NO”

Also, please let us have opinion about the foreign remittance Inward/outward.

Hello CA Yogesh Sir,

I want to know. Since the service Manufacturer is from Hongkong and he ships the product to customer in USA. The sales are done through my ebay.com account. Products are fine jewelry, like rings and earrings. Now my Sole Prop. company is based in India and I get the direct payment to my bank account by purpose code p0101 from paypal. How will my tax be calculated. If according to you I need to pay IGST then how much should I be paying. I have done a a lot of research online and I have not been very clear on how to deal with this situation.

Regards

Sunil Kr.

Dear Sir,

This is with reference to sec. 10(a); for the purposes of determining the nature of transaction i.e inter- intra, we must refer to the provisions of sec. 7(5) of IGST Act. Here it is clearly mentioned that if any transaction is not covered elsewhere but supply is in taxable territory, then only it shall be treated as Inter-state.

but in present case, Dubai is not taxable territory, therefore, it shall not be treated as inter-state supply and no tax is required to be paid.

please correct me, if i am wrong.

Exemption upto Rs. 5,000/- was given vide notification no. 8/2017 – Central Tax (Rate) dt. 28th June, 2017. Hence, above Rs.5,000/- in a singe day, registered person needed to pay RCM u/s 9(4) of CGST Act, 2017. However, as per notification 38/2017 – CT (R) dt. 13th October, 2017, limit of Rs. 5,000/- was withdrawn and government exempts all such supplies from payment of RCM u/s 9(4).

Similar notification was issued under IGST. Notification no. 32/2017 dt. 13th October, 2017, exempts all inter-state supplies from payment of tax u/s 5(4) of IGST Act, 2017.

Notification 38/2017-CT (R) dt 13-10-2017 merely exempts INTRA-STATE SUPPLIES that too upto a value Rs. 5000/- in a single day from payment of GST by the Recipient of goods under RCM – Sec 9 (4) of CGST Act, 2017, till 31-03-2018.

Your subject is dealing with import of goods from a foreign supplier, who is unregistered and such transaction is considered as INTER-STATE sale and attracts IGST and there is NO EXEMPTION exist as of today, irrespective of Value of goods Supplied by the unregistered person located abraod and received / imported by the Importer in India.

Please check and correct me, if I am wrong,