♦ Introduction:

Tug-of-war between taxpayer and Government is not a new phenomenon under indirect taxation laws, be it over eligibility of input tax credit/cenvat credit, classification of goods/services, granting of interest on delayed refund, etc. Over the years various matters have reached to Supreme Courts, High Courts and Tribunals across the Nation. However, an interesting tug-of-war between the taxpayer and Government is already emerging and likely to escalate over coming years on the issue of applicability of interest rate @18%/24% p.a for non-reflection of Input Tax Credit in GSTR-2A/GSTR2B. On one hand, Department is already demanding interest @ 24% p.a for Input Tax Credit which has not appeared in GSTR-2A of the taxpayer and on the other hand taxpayer is ready to pay interest only @ 18% p.a. Before we analyse the issue in detail, let us pictorially try and understand the system which GST law had originally envisaged.

♦ Legal Provisions:

Section 50 of CGST Act

(1) Every person who is liable to pay tax in accordance with the provisions of this Act or the rules made thereunder, but fails to pay the tax or any part thereof to the Government within the period prescribed, shall for the period for which the tax or any part thereof remains unpaid, pay, on his own, interest at such rate, not exceeding eighteen per cent., as may be notified by the Government on the recommendations of the Council.

Provided that the interest on tax payable in respect of supplies made during a tax period and declared in the return for the said period furnished after the due date in accordance with the provisions of section 39, except where such return is furnished after commencement of any proceedings under section 73 or section 74 in respect of the said period, shall be levied on that portion of the tax that is paid by debiting the electronic cash ledger.

(2) The interest under sub-section (1) shall be calculated, in such manner as may be prescribed, from the day succeeding the day on which such tax was due to be paid.

(3) A taxable person who makes an undue or excess claim of input tax credit under sub–section (10) of section 42 or undue or excess reduction in output tax liability under sub–section (10) of section 43, shall pay interest on such undue or excess claim or on such undue or excess reduction, as the case may be, at such rate not exceeding twenty–four per cent., as may be notified by the Government on the recommendations of the Council.

Section 42 of CGST Act

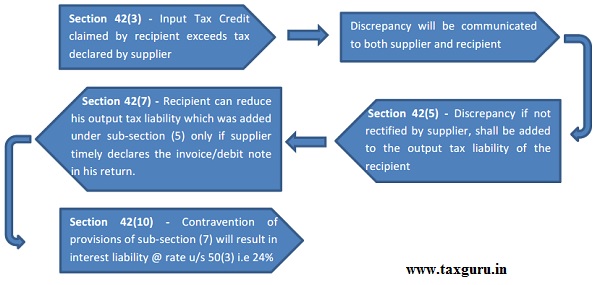

(10) The amount reduced from output tax liability in contravention of the provisions of sub–section (7) shall be added to the output tax liability of the recipient in his return for the month in which such contravention takes place and such recipient shall be liable to pay interest on the amount so added at the rate specified in sub–section (3) of section 50.

(7) The recipient shall be eligible to reduce, from his output tax liability, the amount added under sub–section (5) if the supplier declares the details of the invoice or debit note in his valid return within the time specified in sub-section (9) of section 39.

(5) The amount in respect of which any discrepancy is communicated under sub–section (3) and which is not rectified by the supplier in his valid return for the month in which discrepancy is communicated shall be added to the output tax liability of the recipient, in such manner as may be prescribed, in his return for the month succeeding the month in which the discrepancy is communicated.

(3) Where the input tax credit claimed by the recipient in respect of an inward supply is in excess of the tax declared by the supplier for the same supply or the outward supply is not declared by the supplier in his valid returns, the discrepancy shall be communicated to both such persons in such manner as may be prescribed.

♦ Analysis/Issue

It has been observed that Department by using data available on GST portal have made communications to various taxpayers to reverse input tax credit which is not appearing in GSTR-2A. Pertinently, by referring Section 50(3) of CGST Act, they have also demanded taxpayer to pay interest @ 24% p.a in such cases. Department has conducted investigation at taxpayers premises and have found certain violations of statutory provisions such as ITC as restricted under Section 17(5) being availed, payment to suppliers not being made within 180 days, etc, Department is demanding higher rate of interest in such cases also.

Before we analyse applicability of interest @ 18% or 24% and various cases, it is important to understand that power for chargeability of interest comes only from Section 50 of CGST Act as referred above. Section 50 has made clear distinction between chargeability of interest @ 18% under Section 50(1) and interest @24% under Section 50(3) of the Act. Inspite of two separate sub-sections defining different interest rates, Department has conveniently relied upon Section 50(3) only for all cases/violations made by the taxpayers.

Without making any comment on whether there is any need for reversal of input tax credit in case of mismatch between ITC availed in GSTR-3B and ITC appearing in GSTR-2A, author would prefer commenting only on the present issue of applicability of rate of interest. It cannot be disputed that, only in cases where violation is made under Section 42 (10) read with Section 42(7)/(5)/(3) and Section 43(10) read with Section 43(7)/(5)/(3), interest @24% p.a can be demanded. In all the other cases, interest @ 18% p.a only is applicable unless specific waiver/concession is granted by the Government for specified special period.

Since, the principle is similar for Section 42(10) and 43(10), for the sake of brevity, we are considering analysis of Section 42 only.

If one carefully reads the above chart and provisions of Section 42 (10) r/w 42(7), 42(5) and 42(3), it is clear that only in case where recipient on his own reduces his output liability which was added by virtue of Section 42(5) without any corresponding changes being made by the supplier in his return, then only interest @24% p.a can be demanded.

♦ Whether demand of interest @24% p.a is invalid under Sections 42/43/38 which are in abeyance?

The due date for filing of Form GSTR-2 has not been notified till date. Para 2 of Notification No. 44/2018-Central Tax Dated 10th September 2018 provided as follows:-

2. The time limit for furnishing the details or return, as the case may be, under subsection (2) of section 38 and sub‐section (1) of section 39 of the said Act, for the months of July, 2017 to March, 2019 shall be subsequently notified in the Official Gazette.

It is pretty clear from the above that the time limit for furnishing the return under section 38 have not been notified in official gazette till date and since the time limit for filing the return have not been notified till date, therefore Section 42 itself cannot be used until then. The premise of Section 42 is the details of inward supplies furnished under Section 38 and matching of the same in the manner as provided therein. Since GSTR-2 itself has not been brought in place therefore its matching procedure and implications of non-matching of the credit as provided under section 42(3), 42(5),42(6),42(7) and 42(10) have no application.

♦ Conclusion:

Just like the marriage profile match making has become complex in today’s world with either the horoscope not matching or then the differences in compatibility of couples, the system of ITC match/mismatch also has become complex since the 1st month of implementation of GST because of implementation of provisions of Section 42 (match/mismatch/claim/reclaim) and Section 38 (Form GSTR-2) being failed/deferred and taxpayers have been burdened with GSTR-2A and GSTR-2B reconciliations.

Finally, since the provisions of Section 42 and Section 43 along with Section 38 have not been implemented till date, question of applying Section 42(10)/43(10) having powers of chargeability of interest @24% p.a does not arise at all. Resultantly, if at all demand of interest is raised, it can be only @ 18 % p.a for any violation of provisions such as mismatch of ITC between GSTR-2A and GSTR-3B, availment of ITC restricted under Section 17(5), payment to suppliers not being made within 180 days etc. Authors reserve their comments upon the validity of demand based on GSTR-2A/GSTR-2B which can be discussed separately.

Thank you!!

(Above article was written on 31st July, 2021 & jointly authored by CMA. Anuj Chordiya, CA. Yogesh Ingale and CA. Tushar Ajmera and. Views expressed are strictly personal. For any queries & feedback, reach us at anuj.chordiya@talentax.in)

Author Bio

An interesting subject attended well to make the readers understand the current situation.

Let us hope for a better day with the intended returns implemented and thereby reduce burdens of such undue hardships of the taxpayers.