Outward Supplies (Sec 37)

> Meaning of Outward Supply : Outward supply, in relation to a taxable person, means supply of goods/ services, whether by sale, transfer, barter, exchange, license, rental, lease, or disposal made or agreed to be made by such person in the course or furtherance of business.

> Explanation of Sec 37:- For the purpose of this chapter, the expression “Details of outward supplies” shall include details of invoice, debit note, credit note and revised invoice in relation to outward supplies.

> Person required to file outward supplies: Every registered taxable person other than

- Input Service Distributor

- Non- Resident

- Composition Scheme holder

- Person paying tax under Sec-51 (TDS)

- Person paying tax under Sec-52 (TCS)

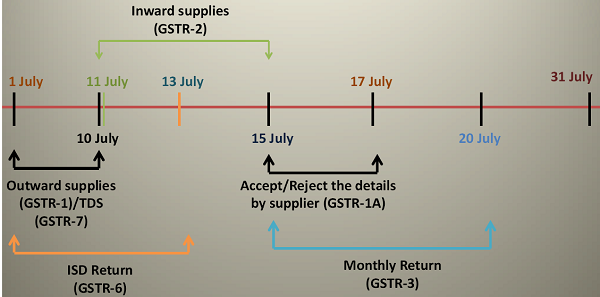

> Due Date: 10th of next month (Extension by board/commissioner) but such person shall not be allowed to furnish outward supplies (GSTR-1) from 11th to 15th of the month.

- Example:- If a registered person fails to furnish the details of outward supplies on 10th of the month then he shall be allowed to furnish details of outward supplies from 16th on wards of the month and he is strictly not allowed to furnish GSTR-1 between 11th to 15th day of the month.

> What other responsibility of outward supplier: Every outward supplier shall either accept or reject the details communicated by inward supplier under 38(3) & (4) between 15th to 17th day of the month.

> What if any mismatch found under sec 42 & 43: Shall discover & rectify such error or omission and shall also pay the tax & interest, if any, in case there is short payment of tax on account of such error or omission

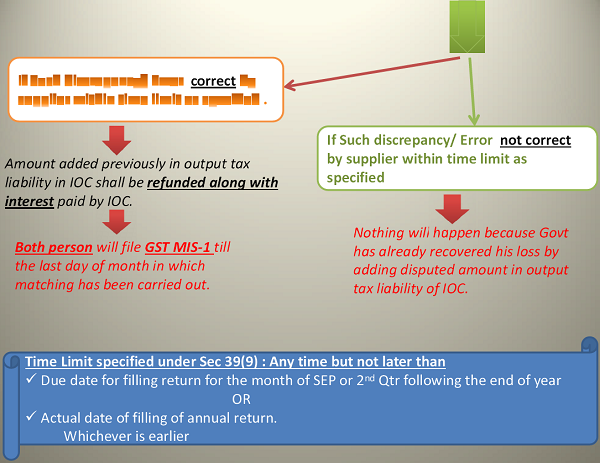

> Is there any time limit for rectification of such error or omission: Yes… Up to the date of filing return under sec 39 (Form: GSTR-3) for the month of Sep following the end of FY to which such details pertains OR filing the relevant annual return (Form: GSTR-9), whichever is earlier.

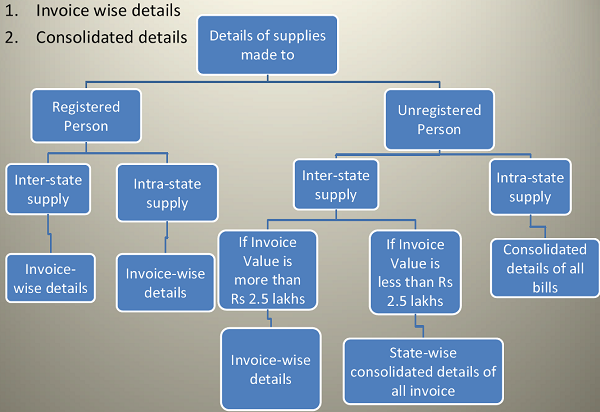

> Rule-1 of the Return Rules has given the way of furnishing details in GSTR-1 in following manner.

Inward Supplies (Sec 38)

> Meaning of Inward Supply: It means receipt of goods/services whether by purchase, acquisition or any other means with or without consideration.

> Person required to file Inward supplies: Every registered taxable person other than

- Input Service Distributor

- Non- Resident

- Composition Scheme holder

- Person paying tax under Sec-51 (TDS)

- Person paying tax under Sec-52 (TCS)

> What details are required to be furnished under inward supplies:-Inward supplies of taxable goods/ services, Including

- Inward supplies on which tax is payable under RCM

- Inward supplies which is taxable under IGST Act

- Inward supplies on which tax is payable under Sec-3 custom tariff act 1975

> Due Date: Between 11th to 15th of next month (Extension by board/ commissioner).

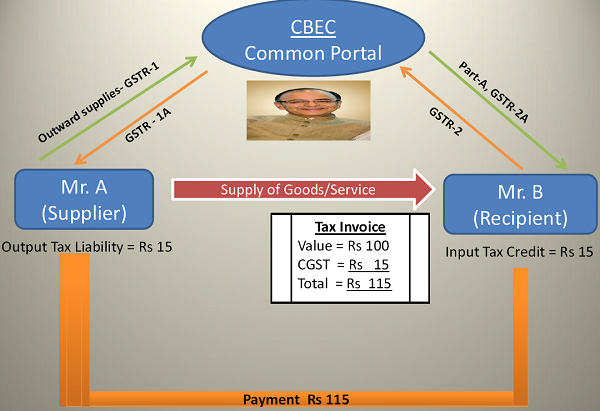

> The Inward supplier shall first verify, validate, modify or delete, if required, the details furnished by outward supplier in his GSTR-1 and which will be available to the inward supplier in FORM PART-A of GSTR-2A

> The inward supplier shall furnish the details of inward supplies in FORM GSTR-2 after reconcile the details prepared by him with the details available in FORM PART A of GSTR-2A furnished by outward supplier.

> The details of supplies modified, deleted, of included by recipient and furnished in GSTR-2 shall be communicated to the supplier and such communication shall be either accept or reject by the outward supplier

within prescribed time limit in sec 37.

> What if any mismatch found under sec 42 & 43: Shall discover & rectify such error or omission and shall also pay the tax & interest, if any, in case there is short payment of tax on account of such error or omission

> Is there any time limit for rectification of such error or omission: Yes… Up to the date of filing return under sec 39 (Form: GSTR-3) for the month of Sep following the end of FY to which such details pertains OR filing the relevant annual return (Form: GSTR-9), whichever is earlier.

> The Recipient shall especially mentioned in GSTR-2 the eligibility of Input tax credit & shall also declare the quantum of ineligible input tax credit.

Return (Sec 39)

> Person required to file Return: Every registered taxable person (FORM: GSTR-3) including

- Input service distributor (GSTR-6)

- Person required to deduct tax under sec 51 i.e. TDS (GSTR-7)

- Non-Resident taxable person (GSTR-5)

- Composition Scheme holder (GSTR-4)

> Due Date :- On or before 20th of the next month

- Input service distributor:-within 13 days after end of such month

- TDS Return:- within 10 days after end of such month

- Composition Scheme holder:- within 18 days after end of such quarter

- Non-Resident taxable person:- within 20 days after end of month or within 7 days after last day of the period of registration, whichever is earlier.

> Payment of taxes:- Every registered person shall pay to the government the tax due not later than the last day on which he is required to furnish such return.

> What if any mismatch found : Shall discover & rectify such error or omission, subject to sec 37 & 38, and shall also rectify the same, subject to payment of interest under this act.

> Is there any time limit for rectification of such error or omission: Yes… Up to the date of filing return under sec 39 for the month of Sep or 2nd quarter following the end of FY to which such details pertains OR filing the relevant annual return (Form: GSTR-9), whichever is earlier.

> The Part-A of GSTR shall be generate electronically based on information furnished in FORM GSTR-1 & GSTR-2.

> Such person shall discharge his liability towards tax, interest, penalty etc by debiting electronic cash ledger or electronic credit ledger and include the details in Part B of the return in FORM GSTR-3.

> Every registered person may claim refund any balance in electronic cash ledger in PART B of the GSTR-3

Monthly Schedule

For e.g. Returns for the month of June

Annual Return (Sec 44)

> Person required to file Annual Return: Every registered taxable person other than

- Input Service Distributor

- Non-Resident

- Casual Taxable Person

- Person paying tax under Sec-51 (TDS)

- Person paying tax under Sec-52 (TCS)

> Due Date: On or before 31st December following end of such financial year.

> If any person whose aggregate turnover during a financial year exceeds Rs. 1 crore then he shall file annual return with copy of audited annual accounts along with reconciliation statement.

> FORMS:

- GSTR-9A: Composition scheme holder

- GSTR-9 :Other than composition scheme holder

- GSTR-9B: Person whose aggregate turnover exceeds Rs 1 Crore.

Matching, Reversal and Reclaim of Input Tax Credit (Sec 42)

>The Details of Inwards supplies furnished by recipients shall be matched with details of outward supplies furnished by suppliers

>The claim of ITC that match with the details of outward supplies shall be finally accepted and communicate such acceptance to the recipients. (FORM GST MIS-1)

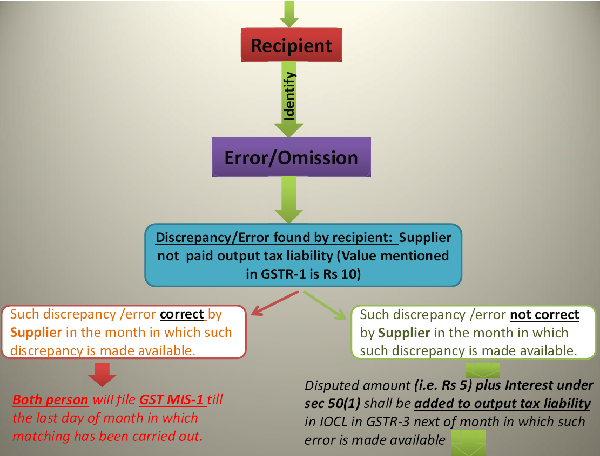

>If ITC claimed by recipients > tax declared or outward supplies not declared : Discrepancy shall communicate to both such person.

>If discrepancy is not rectify by supplier: Add such discrepancy to the output tax liability of the recipients in the subsequent month return & accordingly recipient shall be liable to pay interest from date of credit availing till the corresponding additions.

>After that if supplier rectified such discrepancy in his valid return within time limit {Sec 42(5)}, then recipient allowed to reduce such amount from his output tax liability & interest recovered from recipient shall be paid back by crediting his electronic cash ledger.

Matching, Reversal and Reclaim of Reduction in Output Tax Liability (Sec 43)

> The details of every credit note relating to outward supply shall be matched with reduction in ITC by recipient.

> The claim for reduction in output tax liability by supplier matched with claim for reduction in ITC by recipient shall be finally accepted and communicate such acceptance to the supplier. (FORM GST MIS-3)

> If reduction in output tax liability by supplier> reduction in ITC or credit note not declared by the recipient: Discrepancy shall communicate to both such person.

> If discrepancy is not rectify by recipient: Add such discrepancy to the output tax liability of the supplier & accordingly supplier shall be liable to pay interest from date of claim for reduction in output tax liability till the corresponding additions.

> After that if recipient rectified such discrepancy in his valid return within time limit {Sec 27(7)}, then supplier allowed to reduce such amount from his output tax liability & interest recovered from supplier shall be paid back by crediting his electronic cash ledger.

Matching of claim of ITC (Sec 42)! Reduction in output tax liability (Sec 43)

♦ The following details relating to claim of Input tax credit (Sec 42)/ Reduction in output tax liability (Sec 43) must be matched under sec 42/43 respectively after due date of return(GSTR-3)

– GSTIN of the supplier

– GSTIN of the recipient

– Invoice/debit note date

Sec 42

– Invoice/debit note number

– Credit note date

Sec 43

– Credit note number

– Taxable value

– Tax Amount

♦ Deemed matching of ITC claimed! Reduction in output tax liability: If ITC claimed/ claim Reduction in output tax liability is equal to or less than the output tax paid on such tax invoice or debit note and reduction in input tax credit admitted in his valid return.

♦ Final acceptance of ITC !Reduction in output tax liability and Communication thereof: Final acceptance of claim of ITC/ Reduction in output tax liability shall be made available electronically to registered taxable person (FORM: GST ITC-1)

♦ If ITC/ Reduction in output liability claim more than once on the same invoice: Communicate such information to registered taxable person in FORM GST ITC-1

Miscellaneous Provisions

♦ If Taxable person fails to furnish Outward supplies (GSTR 1) or Inward supplies (GSTR 2) or Monthly return (GSTR 3 & 4) under sec 27 or Final Return (GSTR 10): Late fee shall be Rs 100 per day subject to maximum Rs 5000.

♦ If Taxable person fails to furnish Annual Return (GSTR9):Late fee shall be Rs 100 per day subject to maximum of an amount calculated at a quarter percent of his aggregate turnover.

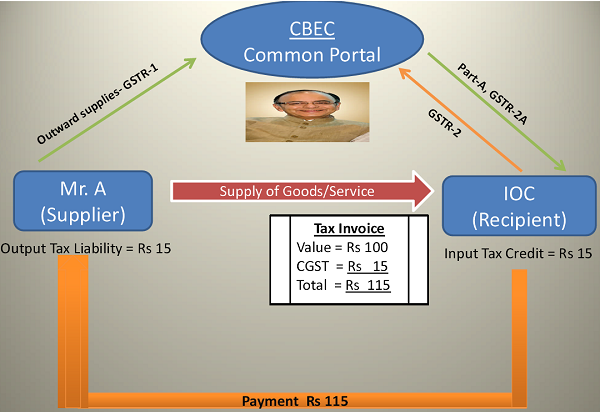

♦ Every person, who has issued a Unique Identity Number and claims refund of the taxes paid on inward supplies, shall furnish the details of such supplies in FORM GSTR-11.

ANALYSIS OF SEC 42

MATCHING, REVERSAL AND RECLAIM OF INPUT TAX CREDIT

CASES

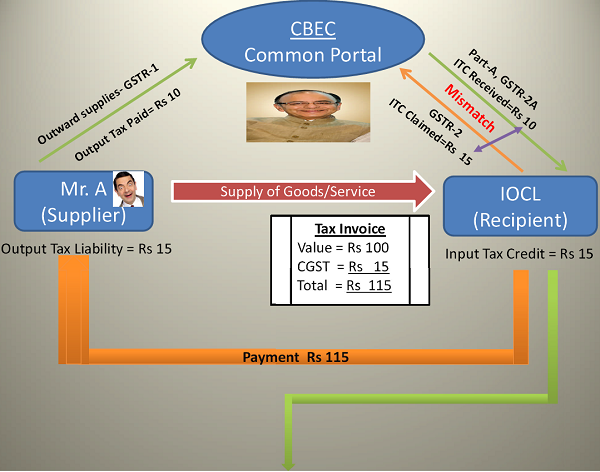

1) Supplier pay his output tax liability Rs 15 and Recipient claim ITC Rs 15.

2) Supplier pay his output tax liability Rs 15 and Recipient claim ITC Rs 10.

3) Supplier pay his output tax liability Rs 15 and Recipient claim ITC 2 times Rs 15. (Duplicate claim)

4) Supplier pay his output tax liability Rs 10 and Recipient claim ITC Rs 15.

5) Supplier pay his output tax liability Rs NIL and Recipient claim ITC Rs 15.

Analysis of Cases

♦ Under Case 1, There is no mismatching between output tax liability paid by supplier and ITC claimed by Recipients. Hence both supplier & recipient will further proceeds for monthly return.

♦ As per Return Rule, Claim of ITC shall be considered as matched if the amount of ITC claimed is equal or less than the output tax paid by supplier. Under case 2, Input tax credit (Rs 10) claimed by recipient is less than the output tax liability (Rs 15) paid by supplier

♦ Under case 3, Recipient claimed ITC more than once on same invoice. In such case, recipient shall file GST MIS-1 electronically through the common portal.

♦ Case 4 & 5 is explained in next slide & Treatment of both cases will remain same

Read more about Goods And Services Tax India

Very Good article. Thanks for sharing.

whether animal feed supplement is still tax free under gst act