CA Chitresh Gupta

Introduction

Introduction

In the present indirect taxation system, cascading of tax is significant due to non-availability of ITC at various stages. Following are certain instances of such cascading of taxes

- Permits restricted inter levy credits between Excise and Service Tax.

- No input tax credit of Central Sales Tax, Entry Tax, Octroi and Luxury Tax,;

- Input tax credit of VAT is not available to manufacturers and service providers;

- Input tax credit of Central Excise duty, service tax & CVD is not admissible to dealers in goods;

- No input tax credit of Swachh Bharat Cess available and

- No Cenvat credit of Krishi Kalyan Cess to manufacturers

One of the basic tenets of proposed GST regime is seamless flow of input tax credit across the value chain right from manufacturer to the final consumer. This will result in equitable distribution and efficient allocation of economic resources. Under GST law, ITC will follow supply chain not only in intra-State transactions but also in inter-State transactions. Further, the credit of tax paid at the time of import of goods and services would also be creditable. This is expected to result in significant reduction in cascading of taxes.

Model GST law was first released on 14th June 2016. The first draft had various issues in Input tax credit like definition of Capital goods, non-availability of Input Tax credit on various business expenditures, allowance of credit of only inputs (but not capital goods & input services) at the time of transition between non-taxable dealer or composition dealer to taxable person eligible for claiming Input tax credit. The Revised GST law has been released by CBEC has tried to resolve various earlier issues. It can surely be said that the revised law has tried to simplify and rationalise the procedures which are much more industry friendly than the previous version of GST law.

The scheme of Input tax credit in the Model GST Law can be broadly defined into substantive provisions and procedures where procedures are equally important because these are inter-twined into the timing of taking input credit and quantum of input credit. The proposed GST comprises of following taxes;

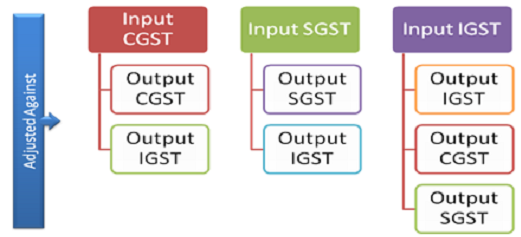

- CGST- Central Goods & Services tax levied by Centre

- SGST- State Goods & Services Tax levied be State

- IGST- Integrated Goods & Services Tax. This tax is levied on Inter-state supply of goods and/or services and levied by Centre.

The analysis of various provisions of Input Tax credit is discussed below;

1. Important Definitions & Concepts

In order to fully comprehend the concept of ITC, it is important to let us analyse following concepts as provided in Revised Model GST Law;

Section 2(56) of Model GST Law: “Input tax credit” means the credit of “input tax” as defined in section 2(55).

Section 2(55) of Model GST Law:”input tax” in relation to a taxable person, means:

- the IGST, including that on the import of goods, CGST and SGST charged on any supply of goods or services to him and

- includes the tax payable under sub-section (3) of section 8 (reverse charge),

- but does not include the tax paid under section 9 (composition);

It is pertinent to note that that as compared to the earlier version of Model GST Law, ‘input tax’ has been defined in a very wide manner. It does not limit itself to the goods and/or services used for making the outward supply.

Section 2 (16) of the IGST Act:“Input tax credit” means the credit of ‘input tax’ as defined in sub-section (15) of section 2.

Section 2 (15) of IGST Act:“input tax” in relation to a taxable person, means

- the Integrated Goods and Services Tax, including that on import of goods, Central Goods and Services Tax or State Goods and Services Tax, as the case may be, charged on any supply of goods and/or services to him and

- includes the tax payable under sub-section (2) of section 5 (reverse charge),

- but does not include the tax paid under section 9 of the CGST/SGST Act;

It may be noted that since “Input tax” is defined as IGST, CGST or SGST charged on any supply of goods and/or services. So, in the IGST Act, input tax consists of all three taxes, IGST, CGST and SGST. It implies that credit of all three can be used for discharging IGST liability.

Section 2(52) of Model GST Law:“input” means any goods other than ‘capital goods’ used or intended to be used by a supplier in the course or furtherance of business;

Section 2(53) of Model GST Law: “input service” means any service used or intended to be used by a supplier in the course or furtherance of business;

Section 2(19) of Model GST Law:“capital goods” means goods, the value of which is capitalised in the books of accounts of the person claiming the credit and which are used or intended to be used in the course or furtherance of business;

It may be seen that the definition of Capital goods has been highly simplified from the definition of capital goods as provided in Cenvat Credit Rules and various VAT Acts.Under the GST regime, ITC in respect of capital goods is allowed to be taken in one go unlike staggered availment presently permitted in Central Excise and Service Tax and in some VAT laws.

Section 2(71) of Model GST Law:“Output tax” in relation to a taxable person, means the CGST/SGST chargeable under this Act on the taxable supply of goods and/or services made by him or by his agent and excludes tax payable by him on reverse charge basis.

Section 2(28) of the IGST Act:“Output tax” in relation to a taxable person, means the IGST chargeable under the Act on the taxable supply of goods and/or services by him or his agent and excludes tax payable by him on reverse charge basis.

It can be inferred from this definition that tax payable by a recipient on reverse charge basis is not an output tax although he is liable to discharge the GST liability. In view of this, he cannot discharge this tax liability by utilising the ITC available with him and he would be required to discharge this tax liability in cash only i.e. through electronic cash ledger only.

Section 2(87) of Model GST Law:“Reverse Charge” means the liability to pay tax by the recipient of supply of goods or services instead of the supplier of such goods or services in respect of such categories of supplies as notified under sub-section (3) of section 8;

It may be noted that provision for Reverse charge liability has been created under section 8(3) of MGL which provides that “the Central or a State Government may, on the recommendation of the Council, by notification, specify categories of supply of goods and/or services the tax on which is payable on reverse charge basis and the tax thereon shall be paid by the recipient of such goods and/or services and all the provisions of this Act shall apply to such person as if he is the person liable for paying the tax in relation to the supply of such goods and/or services.”

Thus, section 2(87) read with section 8(3) of the Model GST law puts the onus of payment of tax in certain supplies on the recipient of goods and/or services. It may be noted that this arrangement has precedence in the present service tax law. The objective of this special provision is to cover those sectors which are difficult to tax because of their unorganised and scattered nature.

2. ELIGIBILITY AND CONDITIONS FOR TAKING INPUT TAX CREDIT

The scheme of claiming ITC is provided under section 16 of Chapter V of the MGL.

2.1 General Provision [Section 16(1)]

Every registered taxable person shall, subject to such conditions and restrictions as may be prescribed and within the time and manner specified in section 44, be entitled to take credit of input tax charged on any supply of goods or services to him which are used or intended to be used in the course or furtherance of his business and the said amount shall be credited to the electronic credit ledger of such person:

PROVIDED that credit of input tax in respect of pipelines and telecommunication tower fixed to earth by foundation or structural support including foundation and structural support thereto shall not exceed—

(a) one-third of the total input tax in the financial year in which the said goods are received,

(b) two-third of the total input tax, including the credit availed in the first financial year, in the financial year immediately succeeding the year referred to in clause (a) in which the said goods are received, and

(c) the balance of the amount of credit in any subsequent financial year.

Analysis

1) Only Registered Person can claim ITC: As per section 16 (1), it appears that only a registered taxable person can avail the credit of input tax and the Unregistered person may not be eligible to avail the credit of input tax.

2) Nexus with Outward Supply: As the registered taxable person is eligible for input tax credit of tax charged on any supply of goods or services to him which are used or intended to be used in the course or furtherance of his business, the taxable person would not be required to prove the direct nexus with the outward supply.

3) Full input tax credit on capital goods in the year of purchase itself except certain situations: It may be noted that full credit on capital goods will be allowed in the year of purchase itself except input tax credit in respect of pipelines and telecommunication tower fixed to earth by foundation etc. which will be allowed in three installments as follows:

|

Ist Year i.e year of purchase |

2nd Year |

3rd Year |

| Up to 1/3 | Upto 2/3 | Balance |

In the current indirect tax regime, CENVAT credit on telecommunication towers was being denied to the telecommunication companies. In GST regime input tax credit of telecommunication tower will be available (though in instalments) to telecom companies.

2.2 CONDITIONS FOR THE AVAILMENT OF ITC [SECTION 16(2)]

Section 16 (2) of the MGL lays down four essential conditions for entitlement of ITC:

- The registered taxable person should be in possession of tax invoice or debit note or such other tax paying document(s) as may be prescribed;

- The taxable person has received the goods and/or services;

- The tax charged on such supply has been actually paid to the appropriate government either in cash or through utilisation of input tax credit; and

- The taxable person should have furnished the return under section 34.

Under the present central indirect tax laws, the filing of return by the recipient is not compulsory in order to take ITC. It may be noted that the supplier is liable to pay GST even on receipt of advance from the customer, even through no supply of goods and/or services has been made; whereas the eligibility for ITC is based on the receipt of goods and/or services.

It may further be noted that even if the recipient has paid the amount of tax to the supplier and the goods and/or services procured are eligible for ITC, no credit would be available until the time the supplier deposits the tax collected by him to the Government. It would be very difficult for the recipient to ensure that the supplier has discharged the GST liability.

Eligibility of ITC in case goods are received in lots: As per explanation to section 16(2), Where the goods against an invoice are received in lots or instalments, the registered taxable person shall be entitled to the credit upon receipt of the last lot or instalment.

Eligibility of ITC in Case Goods are Delivered to Recipient on the directions of taxable person: This is an exception to a condition (b) of sub-section (2) of section 16 [i.e. taxable person has received the goods and/or services]. As per explanation to section 16(2)—For the purpose of clause (b) of section 16(2), it shall be deemed that the taxable person has received the goods where the goods are delivered by the supplier to a recipient or any other person on the direction of such taxable person, whether acting as an agent or otherwise, before or during movement of goods, either by way of transfer of documents of title to goods or otherwise.

Eligibility of ITC – Payment is to be made to supplier of Services within three months: As per second proviso to section 16(2), where a recipient fails to pay to the supplier of services, the amount towards the value of supply of services along with tax payable thereon within a period of three months from the date of issue of invoice by the supplier, an amount equal to the input tax credit availed by the recipient shall be added to his output tax liability, along with interest thereon, in the manner as may be prescribed.

Applicable in case of Payment for services: It is pertinent to note that this provision is applicable where a recipient fails to pay to the supplier of services (not goods) amount towards the value of supply of services along with tax payable thereon within a period of three months from the date of issue of the invoice.

Re-claim of ITC: The section does talk about the reclaim of ITC when payment is made by the recipient to the supplier of services.

3. NO ITC WHERE DEPRECIATION IS CLAIMED ON CAPITAL GOODS [Section 16(3)]

Section 16(3) of the MGL provides that the ITC on capital goods cannot be taken where depreciation on the tax component of the cost of capital goods has been claimed under Income Tax Act, 1961.

This provision has been borrowed from the CENVAT Credit Rules and is based on the principle that the taxable person cannot enjoy double benefit even under two different statutes.

4. TIME LIMIT FOR AVAILING ITC [ SECTION 16(4)]

A taxable person shall not be entitled to take input tax credit in respect of any invoice or debit note for supply of goods or services, after the filing of the return under section 34 for the month of September following the end of financial year to which such invoice or invoice relating to such debit note pertains or filing of the relevant annual return, whichever is earlier.

5. APPORTIONMENT OF CREDIT AND BLOCKED CREDIT [ Section 17]

Proportionate ITC on goods and/or services used partly for business and partly for other purposes [Section 17(1)]

Where the goods and/or services are used by the registered taxable person partly for the purpose of any business and partly for other purposes, the amount of credit shall be restricted to so much of the input tax as is attributable to the purposes of his business.

The Central or a State Government may, by notification issued in this behalf, prescribe the manner in which the credit referred to above may be attributed.

Proportionate ITC on capital goods used partly for business and partly for other purposes: It may be noted that now ITC on capital goods which are used partly for business and partly for other purposes needs to be proportionately availed, unlike the present CENVAT regime.

Eligibility of ITC in Case of Taxable supplies, exempt supplies and Zero rated supplies [Section 17(2)]

Where the goods and/or services are used by the registered taxable person partly for effecting taxable supplies including zero-rated supplies under this Act or under the IGST Act, 2016 and partly for effecting exempt supplies under the said Acts, the amount of credit shall be restricted to so much of the input tax as is attributable to the said taxable supplies including zero-rated supplies.

Explanation.- For the purposes of this sub-section, exempt supplies shall include supplies on which recipient is liable to pay tax on reverse charge basis under sub-section (3) of section 8.

The availability of ITC on various types of supply is summarised in the following table;

|

S.No. |

Nature of Supply |

Whether ITC available |

| 1 | Taxable Supply | Yes |

| 2 | Non-Taxable Supply | No |

| 3 | Exempt Supply | No |

| 4 | Zero Rated Supply | Yes |

The Central or a State Government may, by notification issued in this behalf, prescribe the manner in which the credit referred to above may be attributed. Thus the manner of allocation of the credit will be prescribed in ITC Rules.

Under the present regime, full cenvat credit is allowed on capital goods even if used for both taxable and exempted goods and/or services.

Option to Banking Company Supplying Taxable as well as Exempt Supplies

As per section 17(3), a banking company or a financial institution including a non-banking financial company, engaged in supplying services by way of accepting deposits, extending loans or advances shall have the option to either

- claim proportionate input tax credit as per section 17(2) or

- avail every month an amount equal to fifty per cent of the eligible input tax credit on inputs, capital goods and input services in that month.

The option once exercised shall not be withdrawn during the remaining part of the financial year.

6. NON-ALLOWANCE OF ITC ON CERTAIN GOODS AND / OR SERVICES [Section 17(4)]

Section 17(4) of the Model GST Law provides the negative list with respect to the admissibility of ITC. It is provided that the ITC on following items cannot be availed:

(a) motor vehicles and other conveyances except when they are used;

(i) for making the following taxable supplies, namely

(A) further supply of such vehicles or conveyances; or

(B) transportation of passengers; or

(C) imparting training on driving, flying, navigating such vehicles or conveyances;

(ii) for transportation of goods.

(b) supply of goods and services, namely,

(i) food and beverages, outdoor catering, beauty treatment, health services, cosmetic and plastic surgery except where such inward supply of goods or services of a particular category is used by a registered taxable person for making an outward taxable supply of the same category of goods or services;

(ii) membership of a club, health and fitness centre,

(iii) rent-a-cab, life insurance, health insurance except where the Government notifies the services which are obligatory for an employer to provide to its employees under any law for the time being in force; and

(iv) travel benefits extended to employees on vacation such as leave or home travel concession.

(c) works contract services when supplied for construction of immovable property, other than plant and machinery, except where it is an input service for the further supply of works contract service;

(d) goods or services received by a taxable person for construction of an immovable property on his own account, other than plant and machinery, even when used in course or furtherance of business;

Explanation 1.- For the purpose of this clause, the word “construction” includes re-construction, renovation, additions or alterations or repairs, to the extent of capitalization, to the said immovable property.

Explanation 2.- ‘Plant and Machinery’ means apparatus, equipment, machinery, pipelines, telecommunication tower fixed to earth by the foundation or structural support that are used for making outward supply and includes such foundation and structural supports but excludes land, building or any other civil structures.

(e) goods and/or services on which tax has been paid under section 9;

(f) goods and/or services used for personal consumption;

(g) goods lost, stolen, destroyed, written off or disposed of by way of gift or free samples; and

(h) any tax paid in terms of sections 67, 89 or 90.

In other words, ITC is allowed in respect of taxes paid on all goods and/or services, except listed above, provided they are used or intended to be used in the course or furtherance of business.

7. Availment and Utilisation of ITC

Matching Concept

Provisions contained in section 37 (i.e matching, reversal and reclaim of ITC) of the Model GST Law provides that the ITC would be confirmed only if the inward details filed by the recipient are matched with the outward details furnished by the supplier in his valid return. In the case of the mismatch between the inward and outward details, the supplier would be required to rectify the mismatch and if the mismatch continues, the ITC would have to be reversed by the recipient.

A combined reading of all these provisions indicates that the recipient can avail the ITC, on the provisional basis, immediately on receipt of goods and/or services but the ITC will have to be reversed if the outward and inward supply details are not matched. The said matching would happen only when both the supplier and the recipient have uploaded the respective outward and inward supply details, the supplier has filed his valid return and the recipient has filed his return. It is only after such matching has taken place that the ITC allowed on provisional basis would be confirmed.

8. Conclusion

Revised Model GST Law, 2016 has definitely attempted to resolve some of the glaring concerns of the industry and professional fraternity. However there are still various concerns which are looming large like a very short time period granted for claiming input tax credit (credit of invoice issued in March 2017 can be claimed till September 2017), denial of credit in case of late registration, status of input tax credit on stock lying with units enjoying area based exemption, non-eligibility of credit of central sales tax paid on goods lying in stock on transition date, non-eligibility of ITC till the time the goods or services are received by the recipient etc. The government has acted on the representation of industry and other professional bodies and hope are that the final GST Law will be much more industry friendly can fully address the basic tenet of GST regime which is seamless input tax credit.

CA Chitresh Gupta

B. Com(H), FCA, IFRS (Certified), IDT (Certified)

Author of Book “An Insight into Goods & Service Tax”

Member of IDT Committee of PHD Chamber of Commerce

Member of IDT Committee of NIRC of ICAI (2015-16)

M/s Chitresh Gupta & Associates, Chartered Accountants, Delhi

M – 9910367918, e-mail: gupta_chitresh@yahoo.in, www.gstexperts.net

Author Bio