Case Law Details

Sanjyot Jay Sheth Vs ITO (ITAT Pune)

Pune ITAT Quashes Reassessment as Reasons in Section 148A(b) and 148A(d) Differed; Notice Also Held Time-Barred under Rajeev Bansal

The Pune ITAT quashed the reassessment proceedings holding that the Assessing Officer fundamentally altered the basis of reopening between the notice issued under section 148A(b) and the order passed under section 148A(d), thereby denying the assessee a meaningful opportunity to respond. The Tribunal observed that while the initial notice alleged escapement relating to the sale of an immovable property, the final order proceeded on an entirely different allegation concerning taxability under section 56(2)(vii)(b) arising from purchase of immovable properties at a value lower than the stamp duty value. Since these new allegations were never put to the assessee through a fresh notice under section 148A(b), the reassessment proceedings were held to be vitiated for violation of the statutory procedure and principles of natural justice.

The Tribunal relied upon several decisions including Usha Rani Girdhar (Delhi High Court), Excel Commodity and Derivative Pvt. Ltd. (Calcutta High Court), Akshar Builders & Developers (Bombay High Court) and Arvind Sahdeo Gupta (Bombay High Court) to reiterate that the Assessing Officer cannot substitute or change the very foundation of reopening after issuance of the section 148A(b) notice without giving the assessee a fresh opportunity to explain the revised allegations.

The Tribunal further held that the reassessment was independently barred by limitation in view of the Supreme Court’s decision in Union of India v. Rajeev Bansal. Applying the principles laid down by the Supreme Court regarding computation of the surviving limitation period under TOLA and the new reassessment regime, it found that after the assessee filed the reply on 06.06.2022, the Assessing Officer had only the surviving seven days to complete the proceedings and issue the notice under section 148. Since both the order under section 148A(d) and the notice under section 148 were issued only on 26.07.2022, they were clearly beyond the permissible period and therefore without jurisdiction. Consequently, the reassessment order was quashed and the Tribunal did not examine the issues on merits, treating them as infructuous.

Cases Discussed

- Hexaware Technologies Ltd (Bombay High Court), [2024] 162 com 225 (Bombay)

- Jagadeesan Mani (Mumbai Trib.), [2024] 166 com 320 (Mumbai Trib.)

- Union of India Vs. Rajeev Bansal (Supreme Court of India), (2024) 167 taxmann.com 70 (SC)

- Arvind Sandeo Gupta Vs. ITO (Bombay High Court), (2023) 153 taxmann.com 244 (Bombay)

- Excel Commodity and Derivative (P.) Ltd. (Calcutta High Court), [2023] 150 com 94 (Calcutta)

- Usha Rani Girdhar Vs. ITO (Delhi High Court), (2023) 146 taxmann.com 547 (Delhi)

- Union of India Vs. Ashish Agarwal (Supreme Court of India), (2022) 138 com 64 (SC)

- Kiran R. Sawlani (Mumbai – Trib.), [2022] 136 com 14 (Mumbai – Trib.)

- Divya Capital One (P.) Ltd. v. Asstt. CIT (Delhi High Court), [2022] 139 taxmann.com 461/445 ITR 436

- Yogesh Maheshwari (Jaipur -Trib.), [2021] 125 com 273 (Jaipur -Trib.)

- Mubarak Gafur Korabu (Pune -Trib.), [2020] 117 com 828 (Pune -Trib.)

- Akshar Builders & Developers (Bombay High Court), [2019] 103 com 162 (Bombay)

- Ramnarayan, ITA No. 767/ Del/ 2024

FULL TEXT OF THE ORDER OF ITAT PUNE

The captioned appeal at the instance of assessee pertaining to A.Y. 2014-15 is against the order dated 18.06.2024 framed by National Faceless Appeal Centre, Delhi passed u/s.250 of the Income Tax Act, 1961 arising out of Assessment order dated 06.04.2023 passed u/s.147 r.w.s.144B of the Act.

2. Assessee has raised following grounds of appeal :

“1. Order without jurisdiction

On facts & circumstances prevailing in the case & as per provisions of Act it be held that the order passed u/ s 147 r.w.s. 144B of the Income Tax Act dt. 06/ 04/ 2023 is without jurisdiction, unlawful, untenable in Law & the same be cancelled.

2. Proper opportunity of being heard

Without prejudice to ground no. 1 & assuming without admitting that order passed u/ s 147 r.w.s. 144B is lawful it may please be held that the order passed is in violation of rules of natural justice in terms of not affording the adequate opportunity & therefore the same be held as null & void. The order passed by assessing office be cancelled.

3. Reference to Valuation Officer

On facts & circumstances prevailing in the case & without prejudice to ground no. 1 & 2 it be held that the assessing officer should have referred the matter to the valuation officer in terms of provisions of Sec. 56(2)(vii) (b) r.w.s. 50C of the Income Tax Act. It further be held that not referring matter to valuation officer renders the order passed is improper. Just & proper relief may be granted to the assessee.

4. Non applicability of Section 56(2)(vii)(b)

Without prejudice to ground no. 1 & 2 & assuming without admitting that order passed is lawful & without violation of rules of natural justice it be held that the additions made of Rs. 3,44,78,500/ – by invoking the provisions of Sec. 56(2)(vii)(b) of the Income Tax Act is not warranted in as much as the transactions is one of purchase of agricultural land. It be held that provisions of Sec. 56(2)(vii)(b) are not applicable to the purchase of agricultural land.

5. Non applicability of Section 149

Without prejudice to ground no. 1 & 2 & assuming without admitting that order passed is lawful & without violation of rules of natural justice it be held that there has been no compliance of the provisions of Sec. 149 which is mandatory, so held by Hon’ble Supreme Court in the case of Ashish Agarwal renders the assessment order passed is null & void. The same may please be cancelled.

6. Non applicability of Section 69C

Without prejudice to ground no. 1 & 2 & assuming without admitting that order passed is lawful & without violation of rules of natural justice it be held that the additions made of Rs. 15,41,580/ – u/ s 69C of the Income Tax Act is not in accordance with the facts prevailing in the case. The additions so made be deleted.

7. General Ground

The assessee be allowed to raise, add, modify, rectify and delete any grounds of appeal at the time of hearing.”

3. So far as the legal issues raised in the Grounds of appeal No.1 are concerned, ld. Counsel for the assessee has made three fold contentions challenging the validity of notice u/s.148 of the Act and that the re-assessment proceedings being valid :

(i) Issuance of notice by Jurisdictional Assessing Officer in place of Faceless Assessing Officer.

(ii) Reasons for reopening mentioned in notice u/s.148A(d) of the Act are different to the reasons mentioned in section 148A(b) of the Act.

(iii) Notice u/s.148 of the Act is barred by limitation in light of the judgment of Hon’ble Supreme Court in the case of Union of India Vs. Rajeev Bansal (2024) 167 taxmann. corn 70 (SC)

4. During the course of hearing, ld. Counsel for the assessee at the outset requested for not pressing first fold of the contention challenging the validity of reassessment proceedings based on the issuance of notice by Jurisdictional Assessing Officer in place of Faceless Assessing Officer therefore the same is dismissed as ‘not pressed’.

5. The second legal issue raised is that notice u/s.148 of the Act deserves to be held as invalid and bad in law because the reasons for reopening mentioned in notice 148A(b) of the Act and the reasons mentioned in the order u/s.148A(d) of the Act are different. Reliance placed on the decision of Hon’ble Delhi High Court in the case of Usha Rani Girdhar Vs. ITO (2023) 146 taxmann.com 547 (Delhi) wherein the Hon’ble Court has observed that description of property mentioned in the notice u/s.148A(b) and 148A(d) were different. The Assessing Officer was required to inform the assessee about the allegation with sufficient particulars so that he/she can put forward his/her defence and in absence of such action at the end of Assessing Officer, notice u/s.148 deserves to be set aside. Reliance also placed on the following decisions :

- Excel Commodity and Derivative (P.) Ltd [2023] 150 com 94 (Calcutta)

- Jagadeesan Mani [2024] 166 com 320 (Mumbai Trib.)

- Akshar Builders & Developers [2019] 103 com 162 (Bombay)

- Arvind Sandeo Gupta [2023] 153 com 244 (Bombay)

- Hexaware Technologies Ltd [2024] 162 com 225 (Bombay)

- Yogesh Maheshwari [2021] 125 com 273 (Jaipur -Trib.)

- Mubarak Gafur Korabu [2020] 117 com 828 (Pune -Trib.)

- Ramnarayan ITA No. 767/ Del/ 2024

- Kiran R. Sawlani [2022] 136 com 14 (Mumbai – Trib.)

6. On the other hand, ld. DR vehemently argued supporting the order of ld.CIT(A) and stated that valid notice u/s.148 of the Act has been issued.

7. We have heard the rival contentions and perused the record placed before us. Since the legal issue raised by the assessee goes to the root cause, we therefore take up in precedence to the issues raised on merits of the case. We observe that the assessee is an individual and did not file regular return of income for A.Y. 2014-15 but furnished the return in response to notice u/s.148 of the Act on 23.08.2022 declaring total income at Rs.1,80,880/-. Assessee has challenged the validity of notice issued u/s.148 of the Act. We observe that notice u/s.148A(b) of the Act has been issued on 20.05.2022 and nature and analysis of information mentioned in this notice reads as under :

//this space is intentionally left blank //

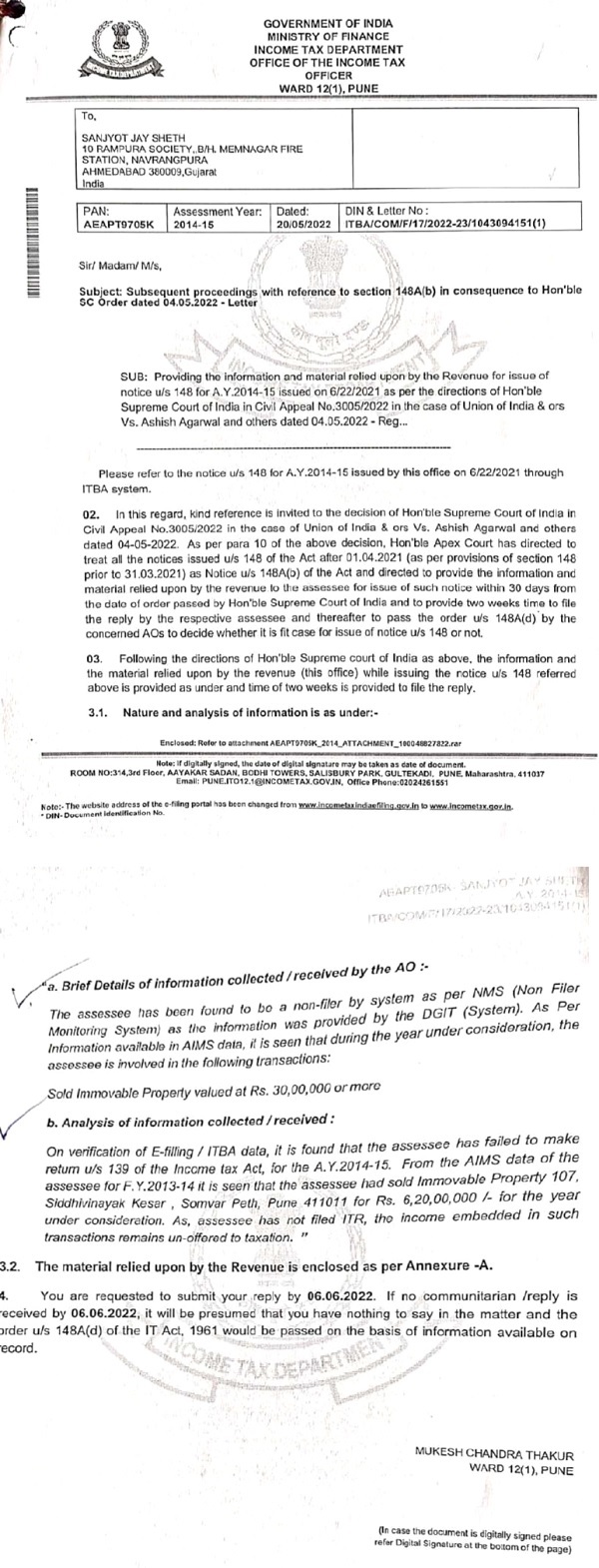

8. The assessee in response to notice u/s.148A(b) of the Act filed reply on 06.06.2022 stating that the alleged “escapement of income from sale of property mentioned in para 3.1(b) referred above is neither sold by me nor owned by me and hence question of suggesting the escapement of income in respect of this property does not arise and therefore requested to withhold the notice”. Thereafter inspite of the assessee having refused to have owned or sold any property mentioned in the notice u/s.148A(b) of the Act, ld. Assessing Officer issued the order u/s.148A(d) of the Act on 26.07.2022 and the same is reproduced below :

9. The above notice u/s.148A(d) of the Act has been followed by notice u/s.148 of the Act on 26.07.2022. Now on perusal of both the notices, we note that in section 148A(b) of the Act, ld. Assessing Officer has alleged that assessee has sold immovable property at Rs.30,00,000/- and further in para 3.1(b) it refers to sale of immovable property of Rs.6.20 crore located at 107, Siddhivinayak Kesar, Somwar Peth, Pune 411011. The assessee has specifically denied to have carried out any such transaction of sale of immovable property of Rs.6.20 crore but thereafter in the order u/s.148A(d) of the Act ld. Assessing Officer has made reference to the previous notice issued u/s.148 of the Act on 23.03.2021, i.e. during Taxation and Other Laws (Relaxation and Amendment of Certain Provisions) Act, 2020 (TOLA) period and wherein in the reasons recorded the allegation was escapement of income to the extent of Rs.3,69,78,500/-. In the final notice u/s.148A(d) of the Act, ld. Assessing Officer observed that “in the case of individual capacity, the difference amount of Rs.3,44,78,500/ – attracts the provisions of section 56(2)(vii)(b) which remained to be offered for taxation for A.Y. 2014-15 and therefore the total amount of Rs.3,69,78,500/- (Rs.25,00,000/- plus Rs.3,44,78,500/) requires to be taxed for A. Y. 2014-15”.

10. Now keeping into consideration the reasons given in notice u/s.148A(b) of the Act and notice u/s.148A(d) of the Act, we find that there is complete disparity. There is allegation of escapement of income in order u/s.148A(d) of the Act is at Rs.3,69,78,500/- but there is no whisper about the said allegation in the notice u/s.148A(b) of the Act. Now once the assessee has given reply to the notice u/s.148A(b) of the Act denying to have carried out any transaction of sale of immovable property of Rs.6.20 crore and thereafter in the final notice u/s.148A(d) of the Act also there is no reference of sale of immovable property at Rs.6.20 crore and in altogether a new issue of escapement of income of Rs.3,69,78,500/-. In such given circumstances, ld. Assessing Officer was required to issue a fresh notice u/s.148A(b) of the Act so as to confront the assessee with the reasons recorded for reopening and the alleged escapement of income. However, no such exercise has been carried out and the notice u/s.148A(b) dated 20.05.2022 is followed by the reply of assesssee on 06.06.2022 and thereafter the final order u/s.148A(d) and notice u/s.148 of the Act has been issued on 26.07.2022 which makes it apparently clear that the reasons which were recorded for initiating the proceedings u/s.148A(b) of the Act are different from the reasons giving rise to alleged escapement of income in the notice u/s.148A(d) of the Act. This action of the Assessing Officer of not issuing a revised notice u/s.148A(b) of the Act vitiates the very basis of reopening proceedings and the notice u/s.148 of the Act is invalid.

11. Our view is fortified by plethora of judicial precedents. We first take note of the judgment of Hon’ble Delhi High Court in the case of Usha Rani Girdhar Vs. ITO (2023) 146 taxmann.com 547 (Delhi) wherein the Hon’ble Court held as under :

“5. Having perused the paper book and having heard the learned counsel for the parties, this Court is of the view that the Kingsway Camp property was mentioned in the notice issued under section 148A(b) of the Act and the petitioner was never asked to explain the transaction with regard to the sale of the Rohini property. This Court finds that not only is the description of the property different in the notice issued under section 148A(b) of the Act and the order passed under section 148A(d) of the Act, but also the sale consideration and circle rate in both the documents are different.

6. It seems to this Court that though the Assessing Officer prior to passing the impugned order under section 148A(d) of the Act realised that he had committed a mistake while issuing the notice under section 148A(b) of the Act, yet he proceeded with the same and even went to the extent of wrongly stating in the section 148A(d) order that he had issued the notice under section 148A(b) of the Act with regard to the Rohini property instead of Kingsway Camp property.

7. A perusal of the file also reveals that the information with the Assessing Officer received from the ITO, Ward 35(1), Delhi was with regard to violation of section 269SS of the Act and not with regard to non-declaration of long term capital gain, for which the notice had been issued. Consequently, the impugned show cause notice is contrary to the record.

8. This Court in Catchy Pro-Build (P.) Ltd. v. Asstt. CIT [2022] 145 com 510/448 ITR 671 High Court has held, ” if the foundational allegation is missing in the notice issued under section 148A(b) of the Act, the same cannot be incorporated by issuing a supplementary notice”.

9. It is further settled law that the intent behind issuing the notice under section 148A(b) of the Act is to inform the assessee of the allegations against him/her with sufficient particulars so that he/she can put forward his/her defence. In the present instance, the assessee specifically replied to the allegation that was mentioned in the notice issued under section 148A(b) of the Act and for this, she cannot be faulted with. On the other hand, the Assessing Officer has been negligent in incorporating the incorrect information and in not admitting the fact that he had committed a mistake while issuing a notice under section 148A(b) of the Act even at the time of passing the order under section 148A(d) of the Act.

10. Keeping in view the aforesaid, present writ petition is allowed and the show cause notice issued under section 148A(b) of the Act as well as the order passed under section 148A(d) of the Act and the notice issued under section 148 of the Act for the Assessment Year 2017-18 are set aside. However, if the law permits, the respondents-revenue to take further steps in the matter, they shall be at liberty to do so. Needless to state that if and when such steps are taken and if the petitioner has a grievance, she shall be at liberty to take her remedies in accordance with law. Accordingly, the present writ petition along with pending applications stands disposed of”

12. Next we take note of the judgment of Hon’ble Calcutta High Court in the case Excel Commodity and Derivative (P) Ltd. Vs. Union of India (2023) 150 taxmann.com 94 (Calcutta) wherein the Hon’ble Court held as follows :

“1. This intra-Court appeal by the writ petitioner is directed against the order dated 30th June, 2022 WPO/ 2298/ 2022.

2. The writ petition was disposed of by setting aside the order impugned therein dated 7th April, 2 section 148A(d) of the Incomed of by sing asid learned Single Bench held that the said order dated 7th April, 2022 is devoid of reasons and without any discussion on the contentions raised by the petitioner in their objections dated 28th March, 2022 to the notice issued by the assessing officer under section 148A(b) of the Act. After having held so and quashing the order dated 7th April, 2022, the learned Single Bench remanded the matter back to the assessing officer to pass a fresh speaking order. Aggrieved by such direction the appellant is before us by way of this appeal.

3. We have elaborately heard Mr. Subash Agarwal, learned counsel for the appellant and Mr. Tilak Mitra, learned standing counsel appearing for the respondent/ revenue. So far as the first portion of the order passed by the learned Single Bench is concerned, the appellant/ assessee has no quarrel as the order impugned in the writ petition has been quashed. The assessee is only aggrieved by the direction issued by the learned Single Bench remanding the matter back to the assessing officer. The issue is whether in the facts and circumstances of the case, such an order of remand was justified and called for.

4. The appellant/ assessee was issued notice under section 148A(b) of the Act dated 22nd March, 2022. The sum and substance of the allegation in the notice was that the appellant/ assessee has done fictitious derivative transactions with M/ s. Blueview Tradecom Put. Ltd. The assessee submitted their detailed reply to the said notice enclosing all relevant documents in support of their claim to justify that they have not indulged in any fictitious derivative transaction. The procedure contemplated under section 148A requires the assessing officer to consider the reply and thereafter pass a reasoned order, if in opinion of the assessing officer, the information furnished by the assessee in their reply is satisfactory, then nothing more requires to be done. On the other hand, if the assessing officer is of the view that the reply furnished by the assessee is not acceptable, then he is to pass a speaking order in terms of clause (d) of Section 148A of the Act. In the instant case, the assessing officer has passed the order under section 148A(d) dated 7th April, 2022. On a reading of the said order, we find that the assessing officer has indirectly accepted the explanation given by the appellant/ assessee that they have not indulged in fictitious derivative transaction. We say so because in the order dated 7th April, 2022 in paragraph 4 therein, the assessing officer alleges that prima facie the appellant/ assessee has taken accommodation entry by way of fund transfer from M/ s. Brightmoon Suppliers Put. Ltd. which is a different company. Thus, the order passed under clause (d) of Section 148A of the Act is not based on the reason for which notice dated 22nd March, 2022 was issued under section 148A(b) of the Act. Therefore, the order dated 7th April, 2022 is illegal and has to be held to be wholly unsustainable. In such factual position, the necessity to remand the matter back to the assessing officer does not arise.

5. Further, we take note of the Circular issued by the Central Board of Direct Taxes (CBDT) dated 22nd August, 2022 giving instruction to the departmental officers with regard to the uploading of data on functionality/ portal of the Income-tax Department. This circular emphasises the earlier circular dated August, 2022 and in paragraph 3 therein, it has been stated as follows:

“(3). Further, it is re-emphasized that –

(i) Before initiating proceedings under section 148/ 147 of the Act, any information available on data-base/portal of the Income-tax Department shall be verified before drawing any adverse inference again the taxpayers. It is not out of place to mention here that the information made available/ data uploaded by the reporting entities may not be fully accurate due to inter alia, error of human nature technical nature, etc. Therefore, due verification may be carried out and opportunity of being heard be given to the taxpayer before initiating proceedings under section 148/ 147 of the Act.

(ii) The supervisory authorities are hereby advised to keep an effective supervision so as to ensure that all extant Instructions/ Guidelines/ Circulars/ SOPs are duly followed by the Assessing Officers in their charge.”

6. From the above it is clear that it has come to the notice of CBDT that in several cases information made available/ data uploaded by the reporting entries are not fully accurate due to error of human nature, technical nature etc. Therefore, the department was advised to effect due verification and opportunity of being heard given to the tax payers before initiating proceedings under section 148/ 147 of the Act. Thus, in the preceding paragraph we have pointed out the factual position in the case on hand and it appears that proper verification was not done on the information which was available with the assessing officer at the time of issuance of notice under section 148A(b) of the Act which has led to an erroneous order dated 7th April, 2022 being passed.

7. In Divya Capital One (P.) Ltd. v. Asstt. CIT [20221 139 taxmann.com 461/445 ITR 436. (Delhi), the Court had considered the new re-assessment claim and held as follows:

“7. This Court is of the view that the new re-assessment scheme (vide amended sections 147 to 151 of the Act) was introduced by the Finance Act, 2021 with the intent of reducing litigation and to promote ease of doing business. In fact, the legislature brought in safeguards in the amended reassessment scheme in accordance with the judgment of the Supreme Court in GKN Driveshafts (India) Ltd. v. ITO (20021125 Taxman 963/(2003) 259 ITR 19 before any exercise of jurisdiction to initiate re-assessment proceedings under section 148 of the Act.

8. This Court is further of the view that under the amended provisions, the term “information” in Explanation 1 to section 148 cannot be lightly resorted to so as to re-open assessment. This information cannot be a ground to give unbridled powers to the Revenue. Whether it is “information to suggest” under amended law or “reason to believe” under erstwhile law the benchmark of “escapement of income chargeable to tax” still remains the primary condition to be satisfied before invoking powers under section 147 of the Act. Merely because the Revenue-respondent classifies a fact already on record as “information” may vest it with the power to issue a notice of re-assessment under section 148A(b) but would certainly not vest it with the power to issue a re-assessment notice under section 148 post an order under section 148A(d).”

8. As pointed out in the aforesaid mentioned decision, the term “information” in Explanation-1 under section 148 cannot be lightly resorted to so as to reopen assessment and this information cannot be a ground to give unbridled power to the revenue. In fact, in the case on hand, the information has been lightly used which resulted in issuance of notice. As pointed out earlier, the assessee had submitted the explanation to the notice along with documents in support of their claim. The assessing officer has given up the said allegation which formed the basis of the notice and proceeded on a fresh ground for alleging that the transaction with some other company was an accommodation entry. Therefore, on that score also the order dated 7th April, 2022 is liable to be set aside in its entirety without giving any opportunity to reopen the matter on a different issue.

9. For the above reasons, the appeal filed by the assessee (APOT/ 132/2022) is allowed and the order dated 7th April, 2022 under section 148A of the Act is set aside and the direction issued by the learned Single Bench remanding the matter to the assessing officer is also set aside. Consequently, no further action can be taken by the department against the appellant/ assessee on the subject issue.

10. In the result, the connected application for stay (IA No. GA/ 1/ 2022) also stands disposed of”

13. In the case of Akshar Builders & Developers Vs. ACIT (2019) 103 taxmann. corn 162 (Bombay), the Hon’ble Jurisdictional High Court observed as under :

“3. The petitioner is a partnership firm, Akshar Builders and Developers (“AB&D” for short). For Assessment Year 2011-12, the petitioner had filed its return of income which was accepted under Section 143(1) of the Income Tax Act, 1961 (“the Act” for short) without scrutiny. To reopen such assessment the impugned notice has been issued. The main ground of challenge raised by the Counsel for the petitioner is that there was no tangible material available with the Assessing Officer to form a belief that the income chargeable to tax has escaped assessment. She pointed out that the Assessing Officer relies on the documents seized during the survey operation against one M/ s. Mudra Real Estate Pvt. Ltd. (“Mudra” for short) which recorded certain cash payments to one M/ s. Akshar Developers (“AD” for short). Counsel submitted that the petitioner AB&D, a partnership firm, has distinct identity and different partners from AB, another partnership firm having different set of partners. She pointed out that both the partnership firms have different PAN numbers. The Assessing Officer, therefore, acted on a material prima facie showing payments by Mudra to AD and reopened the assessment in case of the present petitioner. Counsel further submitted that the reassessment in case of Mudra has now been done by the Assessing Officer, passing order on 31st December, 2018 in which also there is no addition in relation to the said alleged payments by Mudra to AD. In other words, the Department in the assessment in case of Mudra has not relied on the payments in question.

4. On the other hand, learned Counsel for the Department opposed the petition contending that previously assessment was not framed after scrutiny. The Assessing Officer therefore would have much wider scope to copen the assessment. In this regard, he relied upon the decision of the Supreme Court in the case of Asstt. CIT v. Rajesh Jhaveri Stock Brokers (P) Ltd., [2007] 291 ITR 500/ 161 Taxman 316. Counsel submitted that at this stage the sufficiency of material enabling the Assessing Officer to reopen the assessment would not be subject matter of scrutiny by the Court. He further submitted that the Assessing Officer had sufficient material at his command to form a belief that income of the present petitioner chargeable to tax has escaped assessment.

5. Since the factum of reassessment order in case of Mudra is not part of the present proceedings, we may keep the same out of consideration. From the record it emerges that the Assessing Officer has issued notice of reopening of assessment after recording his reasons for doing so. These reasons suggest information available to the Assessing Officer supplied by the Investigation wing of the Department that the assessee had received cash amounts of Rs. 3.54 crores which was not accounted for and not offered to tax. He has referred to statement of one Shri. Sanjay Kumar Hundia, Director of Mudra recorded on 25th January, 2018 suggesting cash payment by Mudra to AB&D. However, the document supplied by the Assessing Officer which is a copy of the ledger account of AD in the books of Mudra, at best suggests that such cash payment was made to AD and not to the AB&D, whereas notice of reopening of assessment is issued against AB&D i.e. the present petitioner. To cover this mismatch, it is now sought to be suggested by the Assessing Officer that Investigation Wing informed him that the two entities are one and the same and AB&D is popularly referred to as AD. However, this being the question of two entities being separate, having different partners and having distinct PAN numbers. These aspects are not disputed by the Revenue either while disposing of the objections raised by the petitioner to the notice of reopening or in the affidavit filed in response to the present petition. We, therefore, proceeded on such basis.

6. It is thus emerges from the record that the Assessing Officer has merely acted upon the information submitted to him by the investigation wing that there is material to suggest that Mudra had paid cash amount to AB&D whereas, the material collected during the survey against Mudra prima faice suggests such cash payment to AD. This would demonstrate total lack of application of mind on the part of the Assessing Officer. If he had perused the material supplied to him by the investigation wing, he would have immediately noticed that material referred would suggest cash payment to AD and not AB&D i.e. the present petitioner.

7. Even in a case where the return filed by the assessee is accepted without scrutiny, as per the settled law, the Assessing Officer can issue a notice of reopening of assessment provided he has reason to believe that income chargeable to tax has escaped assessment. The Assessing Officer cannot proceed mechanically and also on erroneous information that may have been supplied to him. In fact, we note that in the present case the Assessing Officer had issued a notice to a wrong person. The impugned notice is, therefore, set aside.”

14. Hon’ble Bombay High Court yet in another case Arvind Sandeo Gupta Vs. ITO, (2023) 153 taxmann.com 244 (Bombay) has held as under :

“8] We have heard the learned Counsel for the parties at length and with their assistance, we have perused the documents on record. We have also given due consideration to the rival submissions. At the outset, it would be necessary to consider the objection raised by the respondents to the maintainability of the Writ Petition on the ground that the order of assessment having been passed, it could be challenged on all grounds including the invalidity of the notice issued under Section 148 of the Act of 1961 by availing the statutory remedy. The difference between entertainability and maintainability of a proceeding has been succinctly explained by the Hon’ble Supreme Court in M/ s Godrej Sara Lee Ltd. (supra). While the objection to “maintainability” goes to the root of the matter and if such objection is found to be of substance, the Court would be rendered incapable of receiving the lis for adjudication. On the other hand, the question of “maintainability” is within the realm of discretion of the High Court since writ remedy is discretionary in nature. It has been further observed that dismissal of Writ Petition on the ground that the petitioner has not availed the alternate remedy without examining as to whether an exceptional case has been made out for such entertainment would not be proper. After referring to various earlier decisions, the exceptions on the basis of which a writ Court would be justified in entertaining a Writ Petition notwithstanding the availability of an alternate remedy were indicated which includes the aspect where the proceedings are without jurisdiction or the order in that regard is without jurisdiction. If a jurisdictional issue is raised and the controversy is purely a legal one that does not involve any disputed question of fact, then the Writ Petition does not deserve to be thrown out at the threshold. The decision in M/ s Magadh Sugar & Energy Ltd. (supra) has laid down the said principles in its decision dated 24/ 9/ 2021.

In Chhabil Das Agarwal (supra) challenge to the order of assessment was entertained by the High Court. In that context the Hon’ble Supreme Court held that when an equally efficacious alternate remedy was available to the petitioner, the High Court ought not to have entertained the Writ Petition. In the present case, challenge is to the notice issued under Section 148 of the Act of 1961 against which no statutory remedy for challenging the same is available.

9] We may indicate that the challenge raised in the Writ Petition is to the notice issued under Section 148 of the Act of 1961 dated 24/ 3/ 2020 as well as the consequential order of assessment that has been vide order dated 29/ 9/ 2021. The learned Counsel for the petitioner has restricted his challenge only to the legality of the said notice dated 24/ 3/ 2020 and has urged that there is no alternate remedy available for challenging the same. He submitted that the order of assessment is not intended to be challenged in the present proceedings and by way of abundant precaution, a statutory appeal has been filed. If the challenge to the notice dated 24/ 3/ 2020 is not found to be acceptable, the petitioner would then pursue the appeal that has been preferred for challenging the order of assessment.

10] Considering the grounds of challenge that have been put forth by the petitioner namely that the re-opening of the assessment is based on incorrect facts rendering the notice to be unsustainable, the objections raised to the notice being decided in a manner contrary to the decision in GKN Driveshafts (India) Ltd. (supra) coupled with other ancillary challenges, it is found that such challenge can be examined since the same go to the root of the matter. The legal position as regards the effect of such challenge is settled by various decisions of the Hon’ble Supreme Court and this Court. On the limited touchstone based on the decisions referred to hereinabove, we are inclined to consider such challenge subject to an exceptional case being made out. The order of assessment is not being examined in the present proceedings. The conditions specified in Section 147 of the Act of 1961 have been held to be jurisdictional in nature in Cedric De Souza Faria Vs. Deputy Commissioner of Income Tax [(2018) 400 ITR 30]. The distinction between a jurisdictional error and error of law/fact within jurisdiction has been referred to by the Hon’ble Supreme Court in Anshul Jain (supra). The decision in Chhabil Dass Agarwal (supra) has been considered by the Division Bench in Ajay Ajit Tanna Vs. Union of India & Ors. [Writ Petition No. 5098/2022 decided on 8/ 3/ 2023] and by referring to the exception to rule of alternate remedy, it has been held that if the Statutory Authority has not acted in accordance with the provisions of the enactment in question, extraordinary jurisdiction could be exercised. In the said decision, failure on the part of the Assessing Officer to comply with the directions of the Hon’ble Supreme Court was one of the reasons for entertaining challenge to the notice issued under Section 148 of the Act of 1961 in writ jurisdiction. In Greatship (India) Limited (supra), the Hon’ble Supreme Court held that challenge to an assessment order could not have been entertained in exercise of writ jurisdiction. Ratio of this decision therefore would not apply to the facts of the present case.

11] Coming to the challenge as raised to the notice issued under Section 148 of the Act of 1961, it is seen that pursuant to the notice dated 24/ 3/ 2020, reasons for re-opening the case under Section 147 of the Act of 1961 were furnished by the Assessing Officer. According to the Assessing Officer, the petitioner had made investment in the purchase of shares and had earned profit from the sale of shares. An amount of Rs.9,90,314/ – was stated to be credited to the bank account of the petitioner but he had not offered the said amount during the Financial Year 2012-13 pertaining to the Assessment Year 2013-14 for taxation. In this regard, when the objection raised by the petitioner is considered, it is seen that the said amount is towards loss suffered by the petitioner in commodity trading pertaining to the Financial Year 2011-12, Assessment Year 2012-13. The said amount was stated to be paid to M/ s AA+ Commodities on 31/ 3/ 2012. It thus becomes clear that the said amount relates to the Assessment Year 2012-13 and not the Assessment Year 2013-14 as indicated in the notice. Further amount of Rs.9,90,314/ – has been shown as amount of loss sustained by the petitioner which was debited in his account and not credited as mentioned in the notice. The said amount was also included in the return filed by the petitioner.

12] The effect of re-opening the assessment based on wrong facts or conclusions has been considered in Tata Sons Limited (supra). It has been held that if the reasons for re-opening the assessment are based on incorrect facts or conclusions, the notice issued for re-opening cannot be sustained. A similar view has been taken in Punia Capital Put. Ltd. (supra) as well as in Ankita A. Choksey (supra). In paragraph 6 thereof, it has been observed that the reasons to believe that income chargeable to tax has escaped must be based on correct facts and if the facts as recorded in the reasons are not correct and the assessee points out the same in his objections then the order on objections must deal with the same and prima facie establish that the facts stated in its reasons as recorded are correct. If the Assessing Officer has proceeded on fundamentally wrong facts to form reasonable belief that income chargeable to tax has escaped assessment and the Assessing Officer while disposing of the objections does not deal with the factual position asserted by the petitioner, it would be safe to conclude that the Revenue does not dispute the facts stated by the petitioner. On such facts, there could be no reason for the Assessing Officer to believe that income chargeable to tax has escaped assessment.

13] In the aforesaid context, if the order deciding the objections is perused, the same does not state that the facts mentioned by the petitioner were incorrect. In fact, no reasons whatsoever have been assigned and it is reiterated that the petitioner failed to declare any profit/ loss in the income tax return and hence the amount of Rs.9,90,314/ – was treated as profit on the sale of shares. As stated above, despite specific objection that the said amount had been debited in the bank account of the petitioner and it pertained to the losses sustained in commodity trading having been shown in the accounts for the Financial Year 2011-12, Assessment Year 2012-13, it becomes clear that the objections have been decided without due application of mind. As held by the Hon’ble Supreme Court in GKN Driveshafts (India) Ltd. (supra), the objections as raised have to be disposed of by a speaking order that could indicate due application of mind. As stated above, there are no reasons whatsoever assigned for turning down the objections and the facts stated in the notice dated 24/ 3/ 2020 are reiterated. It is seen that alongwith the objections dated 13/ 9/ 2021 copy of the account statement for the Financial Year 2011-12 was also attached. Same has not even been referred to while disposing of the objections on 17/ 9/ 2021. In M/ s. Shodiman Investments Put. Ltd. (supra), it is held that application of mind has to be indicated while forming reasons to believe that income chargeable to tax has escaped assessment.

14] It is also to be noted that by issuing subsequent notice, the ITO has sought further information from the petitioner which information does not form the basis of the reasons assigned for re-opening the proceedings. This is clear from the notice dated 24/ 8/ 2021. The Division Bench in Nivi Trading Limited (supra) has held that if further details are sought or some verification is proposed by the officer, same cannot be a substitute for the reasons that have led the Assessing Officer to believe that an income chargeable to tax has escaped assessment.

15] From the aforesaid, it is clear that the notice dated 24/ 3/ 2020 issued under Section 148 of the Act of 1961 seeking re- opening of the assessment is based on incorrect facts. The objections raised by the petitioner pointing out the relevant facts including the proper Assessment Year to which the said transaction pertained being Assessment Year 2012-13 coupled with the fact that the amount of Rs.9,90,314/ – that was stated to be the amount being profit from the sale of shares having been explained to be the amount of loss, the objections having been decided without any speaking order and not dealing with the undisputed factual aspects leads to the conclusion that the re-opening of the assessment is without there being any reason to believe that the income has escaped assessment. In these facts, the notice dated 24/ 3/ 2020 suffers from fundamental factual errors. An exceptional case thus having been made out to interfere in exercise of writ jurisdiction, the impugned notice dated 24/ 3/ 2020 issued under Section 148 of the Act of 1961 is quashed and set-aside. Consequentially, further steps taken by the respondents based on said notice would no longer survive.

16] Rule is made absolute in the aforesaid terms with no order as to costs.

15. All the above referred judicial precedents are squarely applicable on the facts of the instant case. We therefore considering the fact that issues referred in order u/s.148A(d) of the Act were never confronted to the assessee in notice issued u/s.148A(b) of the Act it clearly proves that no proper opportunity has been given to assessee to rebut the allegations of escapement of income referred in order u/s.148A(d) of the Act and therefore hold that impugned notice u/s.148 of the Act is invalid and bad in law thereby rendering the reassessment proceedings in question as illegal, invalid and bad in law and therefore quashed. Impugned order of ld.CIT(A) is set aside and the assessee succeeds on the second legal issue.

16. Now we take up the third legal issue that notice u/s.148 is barred by limitation in light of the judgment of Hon’ble Apex Court in the case of Union of India Vs. Rajeev Bansal (supra). Even though we have allowed the second fold of contention raised by the assessee that the reassessment proceedings are invalid and bad in law but we still take up of this legal issue also.

17. Ld. Counsel for the assessee submitted that as per the ratio laid down by the Hon’ble Apex court in the case of Union of India Vs. Rajeev Bansal (2024) 167 taxmann.com 70 (SC) ld. Assessing Officer ought to have issued notice u/s.148 of the Act latest by 13.06.2022 whereas the notice u/s.148 of the Act under the new regime has been issued on 26.07.2022 which is barred by limitation and therefore the reassessment proceedings deserves to be quashed.

18. On the other hand, ld. DR failed to controvert the contention made by ld. Counsel for the assessee and submitted that the issue stands covered by the decision of Hon’ble Apex Court in the case of Union of India Vs. Rajeev Bansal (2024) 167 com 70 (SC).

19. We have heard the rival contentions and perused the record placed before us. We observe that in the case of assessee originally the notice u/s.148 of the Act was issued under the old regime during Taxation and Other Laws (Relaxation and Amendment of Certain Provisions) Act, 2020 (TOLA) period 2022. Hon’ble Apex Court in the case of Union of India Vs.Ashish Agarwal (2022) 138 com 64 (SC) has held that for the notices issued post 01.04.2021 during TOLA period, the Revenue authorities were directed to issue the notice under the new regime as the Revenue authorities have issued the reassessment notice under bonafide belief that the amendments may not have yet been enforced. Hon’ble Court exercised its discretionary jurisdiction under Article 142 in order the balance the interest of the Revenue and the assessee and directed that the reassessment notice issued under the old regime shall be deemed to have been issued u/s.148A(b) of the Act under the new regime. Thereafter, the connected issued came up for adjudication before the Hon’ble Apex Court in the case of Union of India Vs. Rajeev Bansal (supra) where the interplay of the decision of Union of India Vs.Ashish Agarwal (supra) with TOLA has been discussed at length at para Nos. 108 to 113 of the order and the same reads as under :

108. The Income Tax Act read with TOLA extended the time limit for issuing reassessment notices under Section 148, which fell for completion from 20 March 2020 to 31 March 2021, till 30 June 2021. All the reassessment notices under challenge in the present appeals were issued from 1 April 2021 to 30 June 2021 under the old regime. Ashish Agarwal (supra) deemed these reassessment notices under the old regime as show cause notices under the new regime with effect from the date of issuance of the reassessment notices. The effect of creating the legal fiction is that this Court has to imagine as real all the consequences and incidents that will inevitably flow from the fiction. 163 Therefore, the logical effect of the creation of the legal fiction by Ashish Agarwal (supra) is that the time surviving under the Income Tax Act read with TOLA will be available to the Revenue to complete the remaining proceedings in furtherance of the deemed notices, including issuance of reassessment notices under Section 148 of the new regime. The surviving or balance time limit can be calculated by computing the number of days between the date of issuance of the deemed notice an 30 June 2021.

109. If this Court had not created the legal fiction and the original reassessment notices were validly issued according to the provisions of the new regime, the notices under Section 148 of the new regime would have to be issued within the time limits extended by TOLA. As a corollary, the reassessment notices to be issued in pursuance of the deemed notices must also be within the time East End Dwellings Co. Ltd. v. Finsbury Borough Council, [1952] AC 109. [Lord Asquith, in his concurring opinion, observed: “If you are bidden to treat an imaginary state of affairs as real, you must surely, unless prohibited from doing so, also imagine as real the consequences and incidents which, if the putative state of affairs had in fact existed, must inevitably have flowed from or accompanied it. 7]. PART F limit surviving under the Income Tax Act read with TOLA. This construction gives full effect to the legal fiction created in Ashish Agarwal (supra) and enables both the assesses and the Revenue to obtain the benefit of all consequences flowing from the fiction. 164

110. The effect of the creation of the legal fiction in Ashish Agarwal (supra) was that it stopped the clock of limitation with effect from the date of issuance of Section 148 notices under the old regime [which is also the date of issuance of the deemed notices]. As discussed in the preceding segments of this judgment, the period from the date of the issuance of the deemed notices till the supply of relevant information and material by the assessing officers to the assesses in terms of the directions issued by this Court in Ashish Agarwal (supra) has to be excluded from the computation of the period of limitation. Moreover, the period of two weeks granted to the assesses to reply to the show cause notices must also be excluded in terms of the third proviso to Section 149.

111. The clock started ticking for the Revenue only after it received the response of the assesses to the show causes notices. After the receipt of the reply, the assessing officer had to perform the following responsibilities: (i) consider the reply of the assessee under Section 149A(c); (ii) take a decision under Section 149A(d) based on the available material and the reply of the assessee; and (iii) issue a notice under Section 148 if it was a fit case for reassessment. Once the clock started ticking, the assessing officer was See State of A P v. A P Pensioners Association, (2005) 13 SCC 161 [28]. [This Court observed that the “legal fiction undoubtedly is to be construed in such a manner so as to enable a person, for whose benefit such legal fiction has been created, to obtain all consequences flowing therefrom. “] PART F required to complete these procedures within the surviving time limit. The surviving time limit, as prescribed under the Income Tax Act read with TOLA, was available to the assessing officers to issue the reassessment notices under Section 148 of the new regime.

112. Let us take the instance of a notice issued on 1 May 2021 under the old regime for a relevant assessment year. Because of the legal fiction, the deemed show cause notices will also come into effect from 1 May 2021. After accounting for all the exclusions, the assessing officer will have sixty-one days [days between 1 May 2021 and 30 June 2021] to issue a notice under Section 148 of the new regime. This time starts ticking for the assessing officer after receiving the response of the assessee. In this instance, if the assessee submits the response on 18 June 2022, the assessing officer will have sixty-one days from 18 June 2022 to issue a reassessment notice under Section 148 of the new regime. Thus, in this illustration, the time limit for issuance of a notice under Section 148 of the new regime will end on 18 August 2022.

113. In Ashish Agarwal (supra), this Court allowed the assesses to avail all the defences, including the defence of expiry of the time limit specified under Section 149(1). In the instant appeals, the reassessment notices pertain to the assessment years 2013-2014, 2014-2015, 2015-2016, 2016-2017, and 2017-2018. To assume jurisdiction to issue notices under Section 148 with respect to the relevant assessment years, an assessing officer has to: (i) issue the notices within the period prescribed under Section 149(1) of the new regime read with TOLA; and (ii) obtain the previous approval of the authority.” PART G specified under Section 151. A notice issued without complying with the preconditions is invalid as it affects the jurisdiction of the assessing officer. Therefore, the reassessment notices issued under Section 148 of the new regime, which are in pursuance of the deemed notices, ought to be issued within the time limit surviving under the Income Tax Act read with TOLA. A reassessment notice issued beyond the surviving time limit will be time- barred.”

20. In light of the above judgment of Hon’ble Apex Court, we move on to examine the facts of the instant case. We note that notice u/s.148 of the Act under the old regime was issued on 23.06.2021 and the surviving period was seven days, i.e. upto 30.06.2021. Notice u/s.148A(b) of the Act issued on 20.05.2022 to which the assessee filed reply on 06.06.2022. Considering the example given in para 112 of the judgment of Hon’ble Apex Court in the case of Union of India Vs. Rajeev Bansal (supra) applying the same on the facts of the instant case, we find that after the filing of reply by the assessee on 06.06.2022 ld. Assessing Officer had seven clear working days to issue notice u/s.148A(d) and notice u/s.148 of the Act latest by 13.06.2022. However, undisputedly, the notice u/s.148A(d) and notice u/s.148 of the Act under the new regime have been issued on 26.07.2022 which is clearly beyond the time limit prescribed by the Hon’ble Apex Court. Ld. DR was fair enough in accepting that the ratio laid down by the Hon’ble Apex Court is applicable on the facts of the instant case and that the u/s.148A(d) and notice u/s.148 of the Act are barred by limitation. We therefore respectfully following the ratio laid down by the Hon’ble Apex Court in the case of Union of India Vs. Rajeev Bansal (supra) hold that notice u/s.148A(d) and notice u/s.148 of the Act are barred by limitation therefore ld. Assessing Officer failed to assume valid jurisdiction for carrying out the reassessment proceedings and the same are hereby deserves to be quashed being invalid and bad in law. Assessee succeeds on the third legal issue.

21. Since we have allowed the appeal of the assessee on legal ground and quashed the reassessment order u/s.147 of the Act, dealing with remaining grounds on merit would be merely academic in nature and therefore they are dismissed as Infructuous.

22. In the result, the appeal of the assessee is allowed as per terms indicated hereinabove.

Order pronounced on this 02nd day of July, 2026.

Author Bio