Case Law Details

Payal Kedia Vs ACIT (ITAT Jaipur)

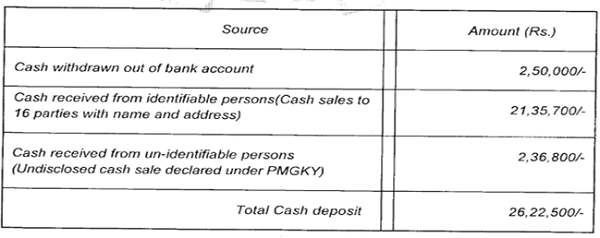

The assessee filed an appeal against the order of the National Faceless Appeal Centre (NFAC) dated 16.07.2025 passed under Section 250 of the Income-tax Act, 1961. The principal dispute related to the addition under Section 68 in respect of cash deposited in the assessee’s bank account during the demonetisation period. The Assessing Officer (AO) had treated the entire cash deposit of Rs.26,22,500 as unexplained cash credit. The CIT(A) partly granted relief by excluding Rs.2,50,000 attributable to cash withdrawn from the bank immediately before deposit and Rs.2,36,800 surrendered under the Pradhan Mantri Garib Kalyan Anna Yojana (PMGKY), thereby sustaining an addition of Rs.21,35,700. The assessee also challenged the application of Section 115BBE and a lump sum disallowance of Rs.5 lakh out of job work and wages expenses, though the Tribunal identified the principal issue as the addition relating to cash deposits during demonetisation.

The assessee explained that the cash deposits of Rs.21,35,700 represented cash received from sales duly recorded in the books of account. In support of this explanation, the assessee furnished complete books of account, cash book, sales bills, and a list of 22 parties from whom cash had been received. TIN numbers were furnished for the parties wherever available, while it was stated that the remaining parties were small-scale unregistered dealers. The assessee also submitted that all such sales had been disclosed in its VAT returns, which had been accepted.

The Revenue rejected the explanation primarily on the basis of an Inspector’s verification of three out of the 22 parties. According to the Inspector’s report, the three parties were not found at their stated addresses and local enquiries indicated that no such firms existed. These parties were M/s Shailender Footwear, M/s Mahaveer General Store and M/s Madhav Footwear. On this basis, the AO treated the cash deposits attributed to sales made to these parties as unexplained and extended the findings to all the remaining parties whose cash collections formed part of the deposits during the demonetisation period.

The Tribunal found no merit in the addition. It observed that the assessee had produced all available evidence to discharge the burden of explaining the source of the cash deposits, including complete books of account, cash book, sales bills, details of purchasers and TIN numbers wherever available. The Tribunal noted that the Revenue had identified only one anomaly relating to the three parties not being found at their stated addresses.

The Tribunal further observed that the AO’s own approach was inconsistent. In the case of M/s Madhav Footwear, the total cash sales during the year amounted to Rs.17,39,208, yet only Rs.6,76,210 relating to the demonetisation period was treated as non-genuine. Similarly, in the case of M/s Shailender Footwear, total cash sales amounted to Rs.10,09,703, while only Rs.3,22,800 relating to the demonetisation period was questioned. The Tribunal held that if the Revenue considered these parties to be non-existent, then the entire sales made to them during the year should have been rejected rather than only the transactions connected with demonetisation deposits. Accepting part of the sales while rejecting only those linked to demonetisation undermined the Revenue’s case.

The Tribunal also held that verification of only three parties on a test-check basis could not justify treating the remaining 19 parties as non-genuine. The cash collected from the three verified parties aggregated about Rs.11,52,910, whereas the disputed cash deposits amounted to Rs.21,35,700. The Tribunal found it unjustified to extend the findings concerning three parties to all other parties without separate verification. It also noted that, in most cases, only the cash collections deposited during the demonetisation period had been treated as arising from bogus sales, while the remaining sales to the same parties during the year had been accepted.

The Tribunal also noted that the assessee had furnished TIN numbers for most parties and had corroborated the sales through VAT returns. It concluded that the assessee had discharged the burden of proving that the cash deposits during the demonetisation period originated from cash collections against recorded sales. In contrast, the Revenue’s conclusion rested on an ad hoc investigation of only three parties and an unwarranted extension of those findings to the remaining parties.

Holding that there was no basis to conclude that the assessee’s explanation was not bona fide or genuine, the Tribunal directed deletion of the addition of Rs.21,35,700 made under Section 68 in respect of cash deposits during the demonetisation period. Accordingly, the appeal of the assessee was allowed.

FULL TEXT OF THE ORDER OF ITAT JAIPUR

The present appeal has been filed by the assessee against the order passed by the National Faceless Appeal Centre (NFAC), Delhi (hereinafter referred to as “Ld. CIT(A)”) dated 16.07.2025 under Section 250 of the Income Tax Act, 1961, (hereinafter referred to as “the Act”).

2. The assessee in this appeal has taken following grounds of appeal:-

1. Necessary cost be awarded to the assessee.

2. The Ld. CIT(A), NFAC has erred on facts and in law in confirming the addition of Rs.21,35,700/- u/s 68 of IT Act by treating the cash deposit during the demonetization period as unexplained cash credit by not accepting the contention of assessee that the same is out of the cash sales duly recorded in the books of accounts which has been offered for tax, thus resulting into double taxation.

3. The lower authorities have erred on facts and in law in taxing the alleged unexplained cash deposit in the bank account w/s 115BBE @ 60% instead of taxing the same @ 30% by ignoring that section 115BBE substituted by Taxation Laws (Second Amendment Act), 2016 which received the assent of President on 15.12.2016 and made applicable from 01.04.2017 is applicable to any transaction from 01.04.2017 onwards and not to any transaction prior to 01.04.2017 as held by Hon’ble Madras High Court in case of SMILE Microfinance Ltd. Vs. ACIT vide order dt. 19.11.2024.

4. The Ld. CIT(A), NFAC has erred on facts and in law in confirming the lump sum disallowance of Rs.5 lacs out of job work expenses and wages expenses of Rs.72,97,548/ claimed by the assessee.

5. The appellant craves to alter, amend and modify any ground of appeal.

3. The solitary issue in the present appeal relates to addition made to the income of the assessee on account of cash deposit in the bank account of the assessee during the demonetization period, the source of which allegedly remain unexplained. The AO had made the addition of the entire cash deposited during the demonetization period amounting to Rs.26,22,500/-, which in turn was restricted by the ld. CIT(A) to Rs.21,35,700/-, giving relief to the extent of cash deposit attributable to cash withdrawal from bank immediately before deposit amounting to Rs 2,50,000/-, and surrender made by the assessee under the Pradhan Mantri Garib Kalyan Anna Yojana(PMGKY) of Rs.2,36,800/-. The assessee’s explanation of the cash deposited in the bank account of the assessee during demonetization period of Rs. 26,22,500 was as under:-

4. Out of the above, the cash deposit attributed to cash sales made by the assessee of Rs. 21,35,700/-, was not treated as duly explained, and therefore, the addition made by the AO to this extent was confirmed.

5. Orders of the Authorities below reveal that in support of the claimthat the cash deposit was out of cash sales made by the assessee, the assessee had submitted the entire list of parties from whom cash was received during this period on account of sales made to them comprising of 22 parties, and all bills raised by the said parties was also furnished to the AO. Complete books of accounts were furnished by the assessee to the AO, and similarly, the entire cash book was also furnished, explaining the source of cash deposited in the bank account of the assessee, during the demonetization period from the different sources as accounted for in its books. The assessee also furnished the TIN number of all the parties to which the cash deposits were attributed, which it could collect from the said parties. With respect to the remaining parties the assessee contended that since they were operating at a very small scale they were all unregistered dealers. The assessee also submitted to have disclosed all the sales in its VAT returns which were also duly accepted.

6. The primary and sole reason, by the Revenue, for rejecting the assessee’s explanation as above, is the fact that the AO investigated the genuineness of the assessee’s claim by conducting verification of the same through an Inspector with respect to 3 parties out of the listed 22 parties submitted by the assessee, and as per the Inspectors’ report the three parties were not found on the given address, and local enquiries revealed that no such Firm existed. The said three parties have been noted to be

- M/s Shailender Footwear to whom total sales of Rs.3,22,800/-,

- M/s Mahaveer General Store to whom total sales of Rs.1,53,900/- and

- M/s Madhav Footwear to whom total sales of Rs. 6,76,210/- was made.

7. As per the Revenue, this exercise carried out by the AO on test check basis applied to all the parties from whom cash was collected by the assessee, and the entire explanation of the assessee, accordingly, rejected.

8. I do not find any merit in the addition made and confirmed by the Revenue Authorities below. The reason for the same is, the assessee had furnished all possible evidencesin discharge of its onus to explain the source of cash deposited being out of cash collected from sales made by it. Entire books of the assessee were produced including cash book, sales bills etc. Even the entire list of parties to whom cash sales was made was furnished giving all possible details relating to them including their TIN Nos. whichever available. The assessee also pointed out that the remaining sellers operating at small scale had no TIN Nos. since they were not required to be registered with the concerned authorities. The only anomaly noted by the Revenue, I find, is with respect to three parties who were not found to exist at the stated address, but surprisingly, the AO has only doubted the genuineness of the cash collected from sales made to these parties and deposited during demonetization period, while the cash collected, otherwise, during the rest of the period of the impugned assessment year stood accepted.

9. In the case of M/s Madhav Footwear, while the total cash sales made to the said party was Rs.17,39,208/-, as per the copy of ledger account of the said party furnished to the Lower Authorities and placed before me, at paper book page No.44, the AO has rejected as non-genuine, the cash collected from sales to the extent of Rs.6,76,210/- only.

10. Similarly, in the case of M/s Shailender Footwear, the total cash sales made to the said party by the assessee amounted to Rs.10,09,703/-as per the copy of ledger account of the said party placed before me at paper book page No.53. However, the AO has doubted the sales made to the said party to the extent of Rs.3,22,800/- only.

11. The premise with the Revenue Authorities being that the said parties did not exist at all, if the said parties did not exist then the entire sales made to these parties needed to be rejected, and not only the sales to which the cash collected during demonetization period, and deposited in the bank account of the assessee needed to be doubted. This act alone of the AO of accepting part of the sale transaction, and rejecting the balance, while finding the said party to be non-existent itself demolishes the case of the Revenue.

12. Further, a mere test check of three parties alone does not entitle the AO to extend his findings with regard to the said parties to the other 19 parties to whom cash collection on account of sales was attributed by the assessee. The cash collected from these three parties comes to around Rs.11,52,910/-(6,76,210+3,22,800+,1,53,900), while the cash deposited in the bank account by the assessee, was way more amounting to Rs.21,35,700/-. It is highly unfair and unjustified to hold, the remaining 19 parties as also in-genuine, merely on the basis of findings, in relation to, three parties. In most of the cases, it is only the cash stated by the assessee to have been collected and deposited during the demonetization period from these 22 parties, which has been treated by the AO to be out of bogus sales, while the remaining sale made by the said parties during the year has been accepted by the AO.

13. Moreover, I find that the assessee furnished the TIN number of majority of the parties, and also corroborated its claim by stating the fact that all sales were disclosed in its VAT returns.

14. It is clear, therefore, that assessee had discharged its onus of proving genuineness of the source of cash deposited in the bank account during demonetization period, attributing it to cash collected from sales made to various parties, while the Revenue’s case rests on an ad hoc exercise of investigation carried out by it revealing three parties to not exist at the stated address and extending its finding in relation to the three parties to the rest of 19 parties from which the assessee had claimed to have collected cash. Further while the AO has accepted sales made to these very parties in the remaining year , he has treated the parties as ingenuine only with respect to the sales transactions carried out during demonetization period.

15. There is no substance at all, therefore, I hold, nor any basis with the AO to hold that the explanation of the assessee of the cash deposited in the bank account was not bona fide or genuine, I, accordingly, direct the addition made to the income of the assessee of Rs.21,35,700/- treating the source of cash deposited in bank account during demonetization period as unexplained, to be deleted.

16. In effect, appeal of the assessee stands allowed.

Order pronounced in the open court on 25.06.2026

Author Bio